|

시장보고서

상품코드

2065490

유럽의 GPU 냉각 솔루션 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe GPU Cooling Solutions - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

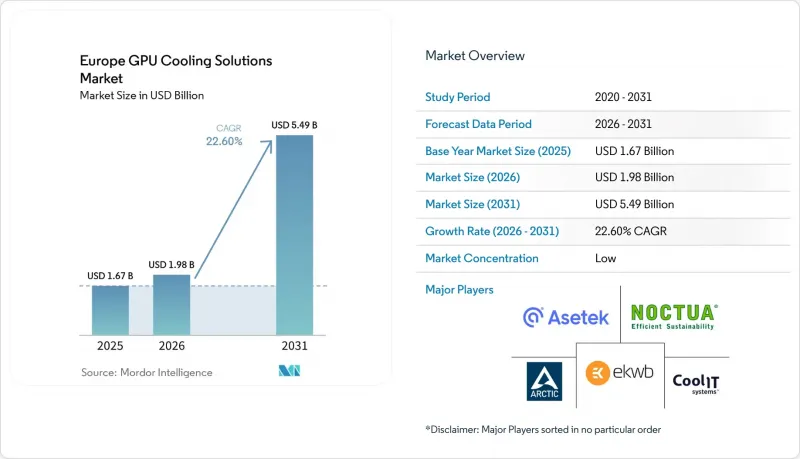

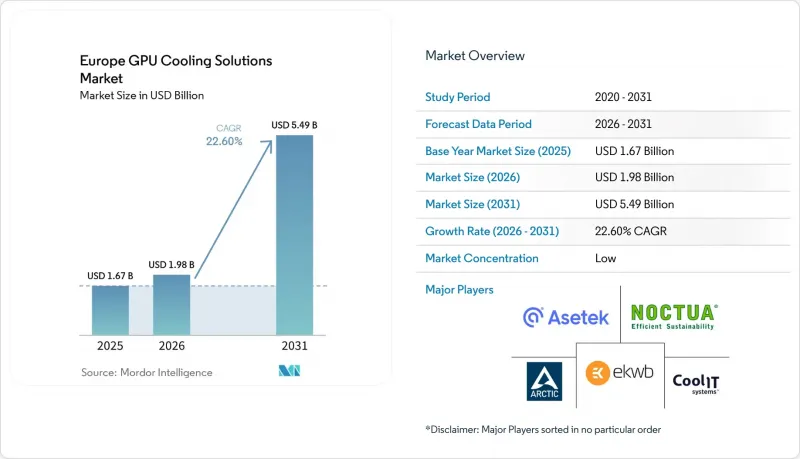

유럽의 GPU 냉각 솔루션 시장 규모는 2025년에 16억 7,000만 달러로 평가되었고, 2026년에 19억 8,000만 달러로 추정되고, 2031년까지 54억 9,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 22.6%로 성장할 전망입니다.

본 보고서는 냉각 기술별(공랭식, 수랭식(직접 투 칩), 침지 냉각, 하이브리드 냉각), 냉각 수준별(컴포넌트 수준 냉각 및 서버/랙 수준 냉각), 도입 형태별(하이퍼스케일 클라우드, 엔터프라이즈, 엣지), GPU 전력 밀도별(300W 미만, 300W-700W, 700W 이상), 국가별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

유럽의 GPU 냉각 솔루션 시장 동향 및 인사이트

AI 도입 가속화가 GPU 출하량을 견인하고 있습니다.

유럽의 GPU 냉각 솔루션 시장은 단일 GPU 조달에서 랙 규모의 AI 시스템으로 전환되고 있으며, 이러한 변화에 따라 냉각은 단순한 보조 기능에서 핵심적인 설계 선택 사항으로 변화하고 있습니다. NVIDIA와 제휴한 HPE의 차세대 AI 팩토리 포트폴리오에는 초대형 모델을 위해 구축된 수냉식 랙 스케일 시스템이 포함되어 있으며, 이는 첨단 GPU 도입이 현재 도입 초기부터 통합된 열 설계 아키텍처에 의존하고 있음을 보여줍니다. 뮌헨에 위치한, 약 1만 대의 Blackwell GPU를 핵심으로 하는 도이치 텔레콤의 ‘Industrial AI Cloud’는 유럽의 주권 AI 프로그램이 이미 고밀도 냉각 인프라에 대한 즉각적인 수요로 이어지고 있음을 보여줍니다. 이러한 시스템의 규모가 확대됨에 따라, OEM 인증을 받은 콜드 플레이트, 매니폴드 및 냉각수 공급 장치는 유럽의 GPU 냉각 솔루션 시장에서 하드웨어 스택의 표준 구성 요소로 자리 잡고 있습니다. 하이퍼스케일 도입이 확대됨에 따라 구성 요소의 인증, 유지보수 및 시스템에 대한 숙련도가 향상되므로, 이러한 표준화를 통해 향후 기업 구매자의 도입 장벽이 낮아질 것으로 보입니다.

유럽연합(EU)의 데이터센터 효율성에 관한 더욱 엄격한 지침

유럽의 GPU 냉각 솔루션 시장은 데이터센터의 에너지 성능에 관한 공시 규정이 강화됨에 따라 형성되고 있습니다. ‘에너지 효율 지침’에서는 IT 설비의 정격 전력이 500 kW를 초과하는 데이터센터에 대해 에너지 성능 데이터 공개를 의무화하고 있으며, 위임 규정(EU) 2024/1364에서는 PUE, 물 사용 효율, 열 재이용 등의 지표에 관한 보고 체계가 정해져 있습니다. 사업자가 이러한 지표를 매년 보고하게 되면, 비효율적인 냉각 방식의 선택이 규제 당국, 고객, 투자자들의 눈에 더 잘 띄게 됩니다. 이로 인해, 특히 고품질 폐열을 수익화할 수 있는 시설에서 액체 냉각 시스템이나 하이브리드 시스템을 도입해야 할 상업적 근거가 더욱 확고해집니다. 실용적인 관점에서 볼 때, 냉각 시스템의 업그레이드를 통해 동일한 투자 주기 내에서 운영 성과와 규정 준수 요건을 모두 충족할 수 있게 되었기 때문에 유럽의 GPU 냉각 솔루션 시장은 그 혜택을 누리고 있습니다.

시설 개보수에 따른 고액의 초기 설비 투자(CAPEX)

유럽의 GPU 냉각 솔루션 시장에서는 사업자들이 구형 공랭식 홀을 액체 냉각 지원 시설로 전환하려 할 때 여전히 뚜렷한 비용 장벽에 직면하고 있습니다. 기존 시설을 업그레이드할 때는 대부분의 경우 구조 보강, 새로운 배관 경로 설치, 소화 시스템 재설계 및 통로 설계 변경이 필요하기 때문에 단순히 장비를 교체하는 것보다 전환 과정이 더 복잡해집니다. 이러한 비용 구조는 사내에 대규모 열공학 팀을 보유하고 있지 않거나, 자본 승인까지 걸리는 기간이 긴 기업에게 특히 큰 과제가 됩니다. 그 결과, 많은 사업자들은 완전한 액체 냉각 시스템으로 전환하기 전의 중간 단계로 리어 도어형 열교환기나 하이브리드 구성을 채택하고 있습니다. 이로 인해, 액체 냉각의 장기적인 운영 경제성이 더 유리하더라도 유럽의 GPU 냉각 솔루션 시장에서 전환 속도는 둔화되고 있습니다.

부문별 분석

2025년 기준, 유럽 GPU 냉각 솔루션 시장에서 공랭식 제품의 점유율은 46.8%를 차지했습니다. 이는 GPU의 전력 밀도가 대폭 상승하기 전에 건설된 기업용 및 코로케이션 시설의 방대한 도입 실적을 바탕으로 한 것입니다. 한편, 침지 냉각은 2031년까지 연평균 24.12%의 성장률을 기록하며 확대될 것으로 전망됩니다. 유럽의 GPU 냉각 솔루션 시장에서 기존 설비는 여전히 중요한 역할을 하고 있습니다. 이는 공랭식 시스템에 대한 단기적인 수요를 유지하는 동시에, 수냉식 및 하이브리드 냉각 시스템 공급업체들에게 예측 가능한 개조 프로젝트를 창출하기 위함입니다. 한편, 새로운 AI 도입은 다른 방향으로 나아가고 있습니다. 현재, 럭스케일의 GPU 시스템은 도입 초기부터 액체 냉각을 전제로 설계되고 있습니다. 하이브리드 구성은 사업자가 기존 홀을 유지하면서 더 높은 열 부하에 대응할 수 있는 새로운 GPU 포드를 준비할 수 있게 해주기 때문에 이 두 가지 현실을 연결하는 실용적인 가교 역할을 하고 있습니다.

액체 침지 냉각은 표준 공랭식 레이아웃의 쾌적한 작동 범위를 초과하는 랙 밀도를 지원할 수 있기 때문에 유럽의 GPU 냉각 솔루션 시장에서 가장 빠르게 성장하고 있는 기술 분야입니다. 이러한 변화는 고밀도 랙 환경을 위해 설계된 Alphacool사의 ‘2026 ES RTX 6000 Pro’ 서버 에디션 GPU 쿨러와 같은 제품 차원의 혁신에 힘입어 이루어지고 있습니다. 또한 Submer사는 OCP EMEA 2026에서 2CRSi사 및 Eneos사와 공동으로 액침 냉각 방식을 채택한 AI 추론용 레퍼런스 설계를 발표했습니다. 이는 액침 냉각 기반의 도입을 위한 상업적 생태계가 더욱 확대되고 있음을 시사합니다. PFAS 관련 냉각액에 대한 불확실성은 여전히 2상 시스템에 대한 조달 측면에서 신중함을 불러일으키고 있지만, 현재로서는 유럽의 GPU 냉각 솔루션 시장이 액체 냉각 방식으로 전환되는 추세를 막기보다는 오히려 단상 솔루션의 입지를 강화하는 요인이 되고 있습니다.

2025년 유럽 GPU 냉각 솔루션 시장 규모에서 서버 및 랙 수준의 냉각이 59%의 점유율을 차지했으며, 새로운 AI 인프라의 주요 구매 단위로 자리매김했습니다. 유럽 GPU 냉각 솔루션 시장에서 이러한 우위는 서버, 매니폴드 및 냉각수 분배 장치가 하나의 운영 패키지로 인증되는 ‘랙 퍼스트’ 설계 모델을 반영한 것입니다. HPE의 액체 냉각 방식 NVL72 플랫폼은 열 관리가 시설의 부가 설비로 나중에 추가되는 것이 아니라, 현재는 랙 규모의 조달 과정에 이미 포함되어 있음을 보여줍니다. 이로 인해 기반이 되는 부품이 여러 공급업체로부터 공급되는 경우에도 지출은 랙 수준에 계속 집중됩니다.

컴포넌트 수준의 냉각은 유럽의 GPU 냉각 솔루션 업계에서 특히 워크스테이션, 부서급 HPC 클러스터 및 맞춤형 GPU 구축 분야에서 여전히 중요한 역할을 하고 있습니다. Alphacool은 2025년, NVIDIA RTX 5090 및 5080 그래픽 카드를 위한 새로운 Core 시리즈 GPU 수냉 쿨러를 출시하며 이 제품군을 확대했습니다. 이는 특수 부품에 대한 수요가 여전히 활발함을 보여줍니다. 앞으로 컴포넌트 수준 수요는 저전력 및 특수 환경으로 점차 좁혀질 것으로 보이지만, 서버 및 랙 수준의 시스템은 유럽의 GPU 냉각 솔루션 시장에서 계속해서 대규모 계약을 수주할 것으로 보입니다. 그 결과, 이 부문에서는 럭스 스케일에서 명확한 프리미엄 계층과, 컴포넌트 수준에서 보다 전문적인 계층이 형성되게 됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the europe gPU cooling solutions market size is projected to be USD 1.67 billion in 2025, USD 1.98 billion in 2026, and reach USD 5.49 billion by 2031, growing at a CAGR of 22.6% from 2026 to 2031.

This report is Segmented by Cooling Technology (Air Cooling, Liquid Cooling (Direct-To-Chip), Immersion Cooling, and Hybrid Cooling), Cooling Level (Component-Level Cooling and Server / Rack-Level Cooling), Deployment (Hyperscale-Cloud, Enterprise, and Edge), GPU Power Density (Below 300W, 300W - 700W, and Above 700W), and Country. The Market Forecasts are Provided in Terms of Value (USD).

Europe GPU Cooling Solutions Market Trends and Insights

Accelerated AI Adoption Driving GPU Shipments

The Europe GPU Cooling Solutions market is moving from single-GPU procurement toward rack-scale AI systems, and that shift is changing cooling from a support feature into a core design choice. HPE's next-generation AI factory portfolio with NVIDIA includes liquid-cooled rack-scale systems built for very large models, which shows how advanced GPU deployments now depend on integrated thermal architecture from launch. Deutsche Telekom's Industrial AI Cloud in Munich, built around 10,000 Blackwell GPUs, shows how sovereign AI programs in Europe are already translating into immediate demand for high-density cooling infrastructure. As these systems scale, OEM-qualified cold plates, manifolds, and coolant delivery units become standard parts of the hardware stack in the Europe GPU Cooling Solutions market. That standardization should lower adoption friction for enterprise buyers over time because component qualification, servicing, and system familiarity improve as hyperscale deployments expand.

Stricter European Union Data-Center Efficiency Directives

The Europe GPU Cooling Solutions market is also being shaped by stricter disclosure rules around data center energy performance. The Energy Efficiency Directive requires data centers above 500 kW installed IT power to make energy performance data publicly available, and Delegated Regulation (EU) 2024/1364 sets the reporting framework for indicators such as PUE, water usage effectiveness, and heat reuse. Once operators must report these metrics every year, inefficient cooling choices become more visible to regulators, customers, and investors. That creates a stronger commercial case for liquid and hybrid systems, especially in facilities that can also monetize higher-grade waste heat. In practical terms, the Europe GPU Cooling Solutions market benefits because cooling upgrades now support both operational performance and compliance needs within the same investment cycle.

High Up-Front CAPEX for Facility Retrofits

The Europe GPU Cooling Solutions market still faces a clear cost barrier when operators try to convert older air-cooled halls into liquid-ready facilities. Brownfield upgrades often require structural reinforcement, new piping routes, revised fire suppression integration, and changes to aisle design, which makes the transition more complex than a simple equipment swap. That cost profile is especially difficult for enterprise buyers that do not have large internal thermal engineering teams or long capital approval windows. As a result, many operators are using rear-door heat exchangers and hybrid configurations as intermediate steps before moving to full liquid systems. This slows the pace of conversion in the Europe GPU Cooling Solutions market, even when the long-term operating economics of liquid cooling are more favorable.

Other drivers and restraints analyzed in the detailed report include:

- Mainstream Liquid Cooling Adoption in Hyperscale Facilities

- Rising Edge-AI Deployments in 5G Micro-Data Centers

- Supply-Chain Risk for Fluorocarbon-Free Coolants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air cooling held 46.8% of the European GPU Cooling Solutions market share in 2025, supported by the large installed base of enterprise and colocation facilities built before GPU power density moved materially higher, while immersion cooling is projected to expand at the 24.12% pace through 2031. In the European GPU Cooling Solutions market, the installed base still matters because it preserves near-term demand for air systems while creating a predictable retrofit pipeline for liquid and hybrid suppliers. New greenfield AI deployments are moving in a different direction, with rack-scale GPU systems now being designed around liquid cooling from launch. Hybrid layouts are becoming the practical bridge between those two realities because they let operators protect older halls while preparing new GPU pods for higher thermal loads.

Immersion cooling is the fastest-growing technology segment in the Europe GPU Cooling Solutions market because it can manage rack densities that stretch beyond the comfortable operating range of standard air layouts. That shift is being supported by product-level innovation such as Alphacool's 2026 ES RTX 6000 Pro server-edition GPU cooler, which was engineered for dense rack environments. Submer also introduced an immersion-cooled AI inference reference design with 2CRSi and Eneos at OCP EMEA 2026, which points to a broader commercial ecosystem for immersion-based deployments. PFAS-related fluid uncertainty is still creating procurement caution for two-phase systems, but for now it is strengthening the position of single-phase solutions rather than stopping the Europe GPU Cooling Solutions market from moving toward liquid methods.

Server and rack-level cooling accounted for 59% share of the Europe GPU Cooling Solutions market size in 2025 and remained the main buying unit for new AI infrastructure. In the Europe GPU Cooling Solutions market, that dominance reflects a rack-first design model in which servers, manifolds, and coolant distribution units are qualified as one operating package. HPE's liquid-cooled NVL72 platforms show how thermal management is now embedded inside rack-scale procurement rather than added later as a facility accessory H. This keeps spending concentrated at the rack level even when the underlying parts are supplied by multiple vendors.

Component-level cooling still plays a meaningful role in the Europe GPU Cooling Solutions industry, especially in workstations, departmental HPC clusters, and custom GPU builds. Alphacool expanded that product space with new Core series GPU water coolers for NVIDIA RTX 5090 and 5080 cards in 2025, which shows that specialized component demand remains active. Over time, component-level demand is likely to narrow toward lower-power and specialized environments, while server and rack-level systems keep capturing the larger contracts in the Europe GPU Cooling Solutions market. That leaves the segment with a clear premium tier at rack scale and a more specialized tier at the component level.

List of Companies Covered in this Report:

- Asetek A/S

- CoolIT Systems Inc.

- Noctua GmbH

- EKWB d.o.o

- Arctic GmbH

- be quiet! (Listan GmbH)

- Alphacool International GmbH

- Schneider Electric SE

- Vertiv Group Corp.

- Nvidia Corporation

- Dell Technologies Inc.

- ASUS Tek Computer Inc.

- Giga-byte Technology Co. Ltd.

- Lenovo Group Ltd.

- Hewlett Packard Enterprise Co.

- Midas Immersion Cooling S.L.

- Submer Technologies S.L.

- Asperitas B.V.

- Rittal GmbH and Co. KG

- LiquidStack Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated AI Adoption Driving GPU Shipments

- 4.2.2 Stricter European Union Data-Center Efficiency Directives

- 4.2.3 Mainstream Liquid Cooling Adoption in Hyperscale Facilities

- 4.2.4 Rising Edge-AI Deployments in 5G Micro-Data Centers

- 4.2.5 Surging Venture Capital Into Immersion-Cooling Start-ups

- 4.2.6 Heat-Reuse Contracts With District Heating Networks

- 4.3 Market Restraints

- 4.3.1 High Up-Front CAPEX for Facility Retrofits

- 4.3.2 Supply-Chain Risk for Fluorocarbon-Free Coolants

- 4.3.3 Limited Skilled Labor for Coolant-System Maintenance

- 4.3.4 Uncertain Standards for Direct-to-Chip Manifolds

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Cooling Technology

- 5.1.1 Air Cooling

- 5.1.2 Liquid Cooling (Direct-to-Chip)

- 5.1.3 Immersion Cooling

- 5.1.4 Hybrid Cooling

- 5.2 By Cooling Level

- 5.2.1 Component-Level Cooling

- 5.2.2 Server / Rack-Level Cooling

- 5.3 By Deployment

- 5.3.1 Hyperscale / Cloud

- 5.3.2 Enterprise

- 5.3.3 Government and Research (HPC)

- 5.3.4 Edge

- 5.4 By GPU Power Density

- 5.4.1 Below 300W

- 5.4.2 300W - 700W

- 5.4.3 Above 700W

- 5.5 By Country

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Asetek A/S

- 6.4.2 CoolIT Systems Inc.

- 6.4.3 Noctua GmbH

- 6.4.4 EKWB d.o.o

- 6.4.5 Arctic GmbH

- 6.4.6 be quiet! (Listan GmbH)

- 6.4.7 Alphacool International GmbH

- 6.4.8 Schneider Electric SE

- 6.4.9 Vertiv Group Corp.

- 6.4.10 Nvidia Corporation

- 6.4.11 Dell Technologies Inc.

- 6.4.12 ASUS Tek Computer Inc.

- 6.4.13 Giga-byte Technology Co. Ltd.

- 6.4.14 Lenovo Group Ltd.

- 6.4.15 Hewlett Packard Enterprise Co.

- 6.4.16 Midas Immersion Cooling S.L.

- 6.4.17 Submer Technologies S.L.

- 6.4.18 Asperitas B.V.

- 6.4.19 Rittal GmbH and Co. KG

- 6.4.20 LiquidStack Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment