|

시장보고서

상품코드

2065488

북미의 GPU 냉각 솔루션 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)North America GPU Cooling Solutions - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

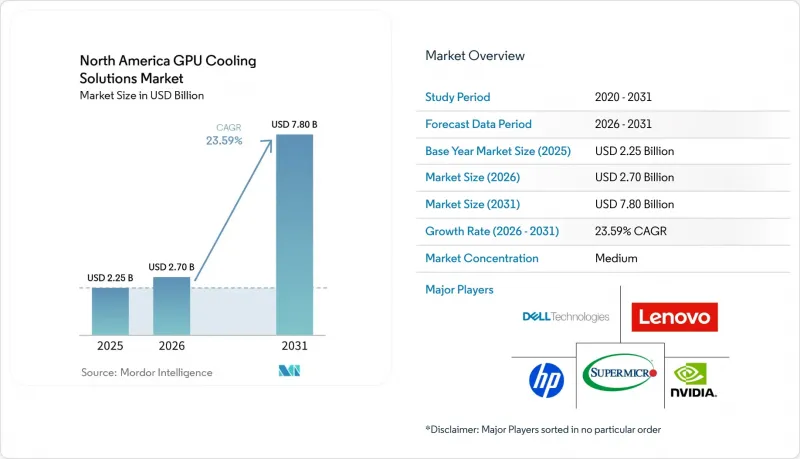

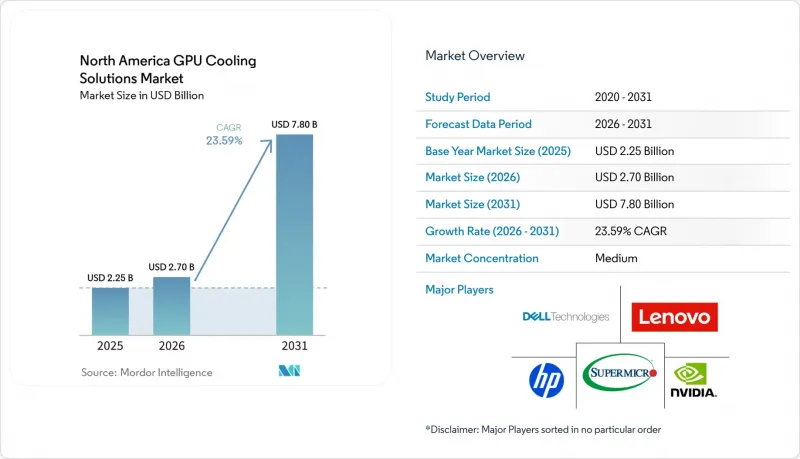

북미의 GPU 냉각 솔루션 시장 규모는 2025년 22억 5,000만 달러로 평가되었고, 2026년 27억 달러로 추정되고, 2031년까지 78억 달러로 확대될 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR)은 23.59%를 나타낼 전망입니다.

본 보고서는 냉각 기술별(공랭식, 수랭식(직접 투 칩), 침지 냉각, 하이브리드 냉각), 냉각 수준별(컴포넌트 수준 냉각 및 서버/랙 수준 냉각), 도입 형태별(하이퍼스케일 클라우드, 엣지, 기타), GPU 전력 밀도별(300W 미만, 300W-700W, 700W 이상), 국가별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

북미의 GPU 냉각 솔루션 시장 동향 및 인사이트

생성형 AI 및 대규모 언어 모델을 위한 GPU 워크로드의 급증

북미 GPU 냉각 솔루션 시장에서 수요를 가장 강력하게 견인하고 있는 요인은 기존의 클라우드 워크로드에서 고밀도 가속기를 핵심으로 하는 AI 팩토리로의 전환입니다. NVIDIA Blackwell Ultra는 GPU당 열설계 전력(TDP)을 약 2,000W까지 높였습니다. 이는 이전 A100 세대의 약 700 W에 비해 대폭 증가한 수치로, 많은 기존 공랭식 설계가 실용적인 작동 범위를 벗어나게 되는 원인이 되고 있습니다. 이러한 변화가 중요한 이유는 운영자가 더 이상 단시간의 훈련 부하만을 냉각시키는 것이 아니라, 훨씬 더 긴 기간에 걸쳐 높은 열 부하가 지속되는 지속적인 추론 처리에 대비하고 있기 때문입니다. 2025년에 실시된 H100 시스템에 대한 조사 결과, 지속적인 부하 조건에서 수냉식 노드는 동급의 공냉식 시스템에 비해 GPU당 약 17% 더 높은 TFLOPS 성능을 발휘하는 것으로 밝혀졌습니다. 이는 열 설계가 현재 실용적인 연산 성능과 직접적으로 연결되어 있음을 보여줍니다. 북미의 GPU 냉각 솔루션 시장에서는 열 아키텍처가 처리량, 신뢰성, 전력 효율에 동시에 영향을 미치게 되면서, GPU 조달과 병행하여 냉각 관련 결정이 내려지는 사례가 늘고 있습니다.

데이터센터의 PUE 감소를 위한 액체 냉각 도입 확대

액체 냉각은 단순한 효율 향상 수단에서 벗어나, 현재의 AI 플랫폼을 상용 규모로 지원하려는 시설에 있어 필수적인 설계 요건으로 자리 잡고 있습니다. NVIDIA는 2025년에 자사의 Blackwell 플랫폼이 수냉 환경에서 물 이용 효율을 300배 이상 향상시킬 수 있다고 발표했습니다. 이는 사업자들이 액체 냉각 시스템을 단순한 옵션의 최적화가 아닌, 핵심 인프라 계획의 일부로 간주하고 있는 이유를 뒷받침해 줍니다. 또한 Vertiv사는 NVIDIA GB300 NVL72 플랫폼용 자체 레퍼런스 아키텍처를 통해 연간 에너지 소비량을 25% 절감하고 전력 발자국을 30% 줄일 수 있었습니다고 보고했으며, 이를 통해 구매자에게 대규모 도입 시 운영상의 이점이 더욱 명확해졌습니다. 이러한 성과는 콜로케이션의 경제성을 변화시키고 있습니다. 왜냐하면 전력 오버헤드를 줄이고 뛰어난 열 제어 능력을 입증할 수 있는 시설은 하이퍼스케일러나 기업의 조달 주기에서 더 유리한 입지를 확보할 수 있기 때문입니다. 따라서 북미 GPU 냉각 솔루션 시장은 랙의 고밀도화, 더욱 엄격해진 에너지 목표, 그리고 가동 시간과 시설 효율을 모두 향상시키는 냉각 시스템에 대한 구매자의 선호라는 복합적인 요인의 영향으로 성장하고 있습니다.

침지 냉각 시스템 개조에 따른 막대한 초기 설비 투자

침지 냉각은 기존 시설에 도입하는 데 있어 여전히 뚜렷한 장벽에 직면해 있습니다. 이는 기존 데이터센터가 이 시스템이 요구하는 바닥 하중, 배관 배치 및 서비스 모델을 충족하도록 건설되지 않았기 때문입니다. 이 과제는 시설 전체를 중단하지 않고 AI 용량을 확대해야 하는 엔터프라이즈 및 코로케이션 사이트에서 가장 두드러지게 나타납니다. 또한, 부하가 가해지는 수냉식 구조의 경우 구조 보강이 필요할 수도 있으며, 그 결과 개조 결정은 단순한 장비 교체라기보다는 대규모 건축 프로젝트에 가깝게 됩니다. 이것이 바로 북미 GPU 냉각 솔루션 시장에서 기존 엔터프라이즈 환경보다 신규 건설되는 하이퍼스케일 시설에서의 수냉식 냉각 도입이 급속도로 진행되고 있는 이유입니다. 직접 투 칩(DTC) 시스템은 높은 GPU 밀도를 유지하면서 업무에 미치는 영향을 최소화하여 수냉 방식을 도입할 수 있기 때문에 대부분의 경우 첫 단계로 선호됩니다.

부문별 분석

2025년, 북미 GPU 냉각 솔루션 시장 규모에서 공랭식은 47.90%의 점유율을 유지했습니다. 이는 처음부터 액체 냉각 인프라를 염두에 두고 설계되지 않았던 기업 시설 및 코로케이션 시설에서의 방대한 도입 실적을 바탕으로 한 것입니다. 이러한 상황은 새로운 설계상의 선호라기보다는 기존 설비 용량을 반영한 것입니다. 이는 북미의 GPU 냉각 솔루션 시장이 현재, 기존 시설이 대응할 수 있었던 것보다 훨씬 더 고밀도인 GPU 클러스터를 중심으로 구축되고 있기 때문입니다. 랙이 현재의 고밀도 AI 구성으로 전환되면, 전력이나 공간을 크게 희생하지 않고도 공랭식의 물리적 한계를 관리하는 것이 훨씬 더 어려워집니다. 이것이 바로 현재 대부분의 새로운 하이퍼스케일 AI 도입에서 액체 냉각 시스템을 추후 업그레이드 사항으로 취급하지 않고, 액체 냉각 지원 또는 완전한 액체 냉각 계획을 바탕으로 시작하는 이유입니다.

직접 투 칩(DTC) 방식의 액체 냉각은 열 성능과 관리 가능한 시설 변경 간의 균형이 잘 잡혀 있어, 현재 고밀도 GPU 시스템에서 주요 도입 방식으로서의 입지를 확고히 하고 있습니다. 각 벤더의 제품 발표를 살펴보면, 북미 GPU 냉각 솔루션 시장에서 공급 측의 준비 상황이 시범 단계를 훨씬 넘어섰음을 알 수 있습니다. Vertiv는 2025년에 NVIDIA GB300 NVL72 플랫폼용 검증된 레퍼런스 아키텍처를 공개했으며, Supermicro는 NVIDIA Blackwell 시스템을 중심으로 한 수냉식 제품군을 확대했습니다. 이 모든 것은 액체 냉각을 우선시하는 인프라로의 명확한 상업적 전환을 보여줍니다. 이머전 냉각은 최첨단 AI 클러스터의 랙당 전력 소비량이 100kW를 초과함에 따라 보다 적극적인 열 제거 전략이 필요해짐에 따라, 여전히 24.12%라는 성장률을 기록하며 가장 빠르게 확대되고 있는 기술 분야입니다. 또한, 많은 업체들이 동일한 섀시 내에서 서로 다른 세대의 GPU와 다양한 열 프로파일에 대응해야 하기 때문에 하이브리드 설계는 북미 GPU 냉각 솔루션 업계에서 여전히 중요한 위치를 차지하고 있습니다.

2025년 기준으로, 서버 및 랙 수준의 냉각은 북미 GPU 냉각 솔루션 시장 점유율의 59.35%를 차지했으며, 2031년까지 가장 빠르게 성장할 냉각 수준이기도 합니다. 이러한 이중적 지위는 구매자가 현재 AI 인프라의 주요 열 관리 및 조달 단위로 개별 구성 요소가 아닌 랙을 인식하고 있음을 보여줍니다. 북미의 GPU 냉각 솔루션 시장에서는 GPU 패키지, 메모리, 상호 연결이 긴밀하게 연계된 단일 열 구역으로 설계되고 있기 때문에 이러한 변화가 더욱 가속화되고 있습니다. DCX사는 2026년 1월, 차세대 NVIDIA 도입 환경을 위한 온수 냉각용 8 MW 시설 분배 장치(FDU)를 발표했으며, 여러 대의 소형 레거시 CDU를 중앙 집중식 설계로 대체함으로써 이러한 방향성을 반영했습니다.

컴포넌트 수준의 냉각이 여전히 중요한 이유는 표준 설치 면적 내에서 전력 밀도가 높아짐에 따라 각 서버 노드에서 더욱 정밀한 열 제어가 필요해지기 때문입니다. 2026년 3월, ZutaCore사는 자사의 ‘OmniTherm’ 콜드플레이트가 싱글 슬롯 PCIe 폼팩터의 NVIDIA RTX PRO 6000 Blackwell Server Edition GPU를 대상으로 물을 사용하지 않는 2상 냉각을 실현했다고 발표했습니다. 이는 정밀 냉각이 여전히 상업적인 차별화 요소임을 보여줍니다. 2026년 5월, Accelsius사는 이러한 추세를 더욱 가속화하는 형태로 ‘NeuCool IR150’을 발표했습니다. 이는 2상식 CDU, 42U 랙 공간 및 통합 매니폴드를 단일 섀시에 결합하여 최대 150 kW를 지원하는 랙 레벨 솔루션입니다. 이처럼 공급업체들이 두 가지 기능을 하나의 도입 가능한 시스템으로 통합하는 사례가 늘어나고 있기 때문에 컴포넌트 수준과 랙 수준의 냉각 간 경계는 점점 더 모호해지고 있습니다. 이는 북미 GPU 냉각 솔루션 업계가 개별 냉각 부품이 아닌 통합형 열 관리 플랫폼으로 전환되고 있음을 보여주는 보다 명확한 징후 중 하나입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the north america gPU cooling solutions market size is projected to expand from USD 2.25 billion in 2025 and USD 2.70 billion in 2026 to USD 7.80 billion by 2031, registering a CAGR of 23.59% between 2026 to 2031.

This report is Segmented by Cooling Technology (Air Cooling, Liquid Cooling (Direct-To-Chip), Immersion Cooling, and Hybrid Cooling), Cooling Level (Component-Level Cooling and Server / Rack-Level Cooling), Deployment (Hyperscale-Cloud, Edge, and More), GPU Power Density (Below 300W, 300W - 700W, and Above 700W), and Country. The Market Forecasts are Provided in Terms of Value (USD).

North America GPU Cooling Solutions Market Trends and Insights

Surge In GPU Workloads For Generative AI And Large Language Models

The strongest demand trigger in the North America GPU cooling solutions market is the move from traditional cloud workloads to AI factory deployments built around high-density accelerators. NVIDIA Blackwell Ultra raises thermal design power to around 2,000 W per GPU, compared with around 700 W for the earlier A100 generation, which pushes many legacy air-cooled layouts beyond their practical operating range. That shift matters because operators are no longer cooling short training bursts alone; they are preparing for sustained inference activity that keeps thermal stress high for far longer periods. A 2025 study on H100 systems found that liquid-cooled nodes delivered around 17% higher TFLOPS per GPU under sustained load than comparable air-cooled systems, which shows that thermal design is now tied directly to usable compute output. In the North America GPU cooling solutions market, cooling decisions are increasingly being made alongside GPU procurement because thermal architecture now affects throughput, reliability, and power efficiency at the same time.

Growing Adoption Of Liquid Cooling To Reduce Data Center PUE

Liquid cooling has moved from an efficiency upgrade to a design requirement for facilities that intend to support current AI platforms at commercial scale. NVIDIA stated in 2025 that its Blackwell platform can improve water efficiency by more than 300x in liquid-cooled deployments, which reinforces why operators are treating liquid systems as part of core infrastructure planning rather than optional optimization. Vertiv also reported that its reference architecture for the NVIDIA GB300 NVL72 platform reduced annual energy consumption by 25% and lowered the power footprint by 30%, which gives buyers a clearer operating case for large-scale deployment. These gains are changing colocation economics because facilities that can prove lower power overhead and better thermal control are better positioned in hyperscaler and enterprise procurement cycles. The North America GPU cooling solutions market is therefore being pulled forward by the combined effect of denser racks, tighter energy targets, and buyer preference for cooling systems that improve both uptime and facility efficiency.

High Upfront Capex For Immersion Cooling Retrofits

Immersion cooling still faces a clear adoption barrier in retrofit settings because older halls were not built for the floor loading, piping layout, and service model these systems demand. That challenge is most visible in enterprise and colocation sites where operators need to add AI capacity without shutting down the broader facility. A loaded immersion configuration can also require structural reinforcement, which pushes the retrofit decision closer to a major building project rather than a simple equipment swap. This is why the North America GPU cooling solutions market shows faster immersion uptake in greenfield hyperscale builds than in legacy enterprise environments. Direct-to-chip systems often become the preferred first step because they offer a lower-disruption path into liquid cooling while still supporting higher GPU density.

Other drivers and restraints analyzed in the detailed report include:

- Increased Preference For Modular, Scalable Cooling Architectures

- Advances In Heat Pipe And Vapor Chamber Technologies

- Supply Chain Volatility In Coolant Fluids And Pump Components

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air cooling retained a 47.90% share of the North America GPU cooling solutions market size in 2025, supported by the large installed base of enterprise and colocation facilities that were not originally designed for liquid infrastructure. That position reflects existing capacity more than new design preference, because the North America GPU cooling solutions market is now being built around far denser GPU clusters than earlier halls could support. Once racks move into current high-density AI configurations, the physical limit of air cooling becomes much harder to manage without large power and space penalties. This is why most new hyperscale AI deployments now start with liquid-ready or fully liquid-cooled plans instead of treating liquid systems as a later upgrade.

Direct-to-chip liquid cooling has consolidated its position as the main deployment path for current high-density GPU systems because it balances thermal performance with manageable facility change. Product launches across the vendor base show that supply-side readiness has moved well beyond pilot status in the North America GPU cooling solutions market. Vertiv published a validated reference architecture for the NVIDIA GB300 NVL72 platform in 2025, and Supermicro expanded its liquid-cooled portfolio around NVIDIA Blackwell systems, which together point to a clear commercial shift toward liquid-first infrastructure. Immersion cooling is still the fastest-growing at 24.12% technology category because frontier AI clusters are moving beyond 100 kW per rack and need more aggressive heat removal strategies. Hybrid designs also remain relevant in the North America GPU cooling solutions industry because many operators must support mixed GPU generations and varied thermal profiles within the same hall.

Server and rack-level cooling held 59.35% of the North America GPU cooling solutions market share in 2025 and is also the fastest-growing cooling level through 2031. That dual position shows how buyers now treat the rack, rather than the individual component, as the main thermal and procurement unit for AI infrastructure. The North America GPU cooling solutions market is reinforcing this shift because GPU packages, memory, and interconnects are being designed as one tightly linked thermal zone. DCX reflected that direction in January 2026 when it introduced its 8 MW Facility Distribution Unit for warm-water cooling in next-generation NVIDIA deployments, replacing multiple smaller legacy CDUs with a centralized design.

Component-level cooling still matters because each server node needs tighter thermal control as power density rises inside standard footprints. In March 2026, ZutaCore said its OmniTherm cold plate enabled waterless two-phase cooling for NVIDIA RTX PRO 6000 Blackwell Server Edition GPUs in a single-slot PCIe form factor, which shows that precision cooling remains a commercial differentiator. Accelsius added to that trend in May 2026 with the NeuCool IR150, a rack-level solution that combines a two-phase CDU, 42U of rack space, and integrated manifolds in a single enclosure supporting up to 150 kW. The boundary between component and rack-level cooling is therefore becoming less rigid because suppliers increasingly package both functions into one deployable system. This is one of the clearer signs that the North America GPU cooling solutions industry is moving toward integrated thermal platforms rather than isolated cooling parts.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Super Micro Computer, Inc.

- Cisco Systems, Inc.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Lenovo Group Limited

- ASUSTeK Computer Inc.

- Giga-Byte Technology Co., Ltd.

- Cooler Master Technology Inc.

- EKWB d.o.o.

- Noctua GmbH

- Arctic GmbH

- Asetek A/S

- Fujitsu Limited

- ZutaCore, Inc.

- Vertiv Holdings Co.

- Rittal GmbH and Co. KG

- Schneider Electric SE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in GPU Workloads for Generative AI and Large Language Models

- 4.2.2 Growing Adoption of Liquid Cooling to Reduce Data Center PUE

- 4.2.3 Increased Preference for Modular, Scalable Cooling Architectures

- 4.2.4 Advances in Heat Pipe and Vapor Chamber Technologies

- 4.2.5 Data Center Sustainability Mandates and Carbon-Neutral Targets

- 4.2.6 Government Incentives for Edge Data Centers in Rural Areas

- 4.3 Market Restraints

- 4.3.1 High Upfront Capex for Immersion Cooling Retrofits

- 4.3.2 Supply Chain Volatility in Coolant Fluids and Pump Components

- 4.3.3 Skill Gap in Designing and Maintaining Liquid-Cooled Racks

- 4.3.4 Reliability Concerns Around Dielectric Fluid Contamination

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Cooling Technology

- 5.1.1 Air Cooling

- 5.1.2 Liquid Cooling (Direct-to-Chip)

- 5.1.3 Immersion Cooling

- 5.1.4 Hybrid Cooling

- 5.2 By Cooling Level

- 5.2.1 Component-Level Cooling

- 5.2.2 Server / Rack-Level Cooling

- 5.3 By Deployment

- 5.3.1 Hyperscale / Cloud

- 5.3.2 Enterprise

- 5.3.3 Government and Research (HPC)

- 5.3.4 Edge

- 5.4 By GPU Power Density

- 5.4.1 Below 300W

- 5.4.2 300W - 700W

- 5.4.3 Above 700W

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Super Micro Computer, Inc.

- 6.4.5 Cisco Systems, Inc.

- 6.4.6 Dell Technologies Inc.

- 6.4.7 Hewlett Packard Enterprise Company

- 6.4.8 Lenovo Group Limited

- 6.4.9 ASUSTeK Computer Inc.

- 6.4.10 Giga-Byte Technology Co., Ltd.

- 6.4.11 Cooler Master Technology Inc.

- 6.4.12 EKWB d.o.o.

- 6.4.13 Noctua GmbH

- 6.4.14 Arctic GmbH

- 6.4.15 Asetek A/S

- 6.4.16 Fujitsu Limited

- 6.4.17 ZutaCore, Inc.

- 6.4.18 Vertiv Holdings Co.

- 6.4.19 Rittal GmbH and Co. KG

- 6.4.20 Schneider Electric SE

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment