|

시장보고서

상품코드

2065485

아시아태평양의 GPU 냉각 솔루션 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Asia-Pacific GPU Cooling Solutions - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

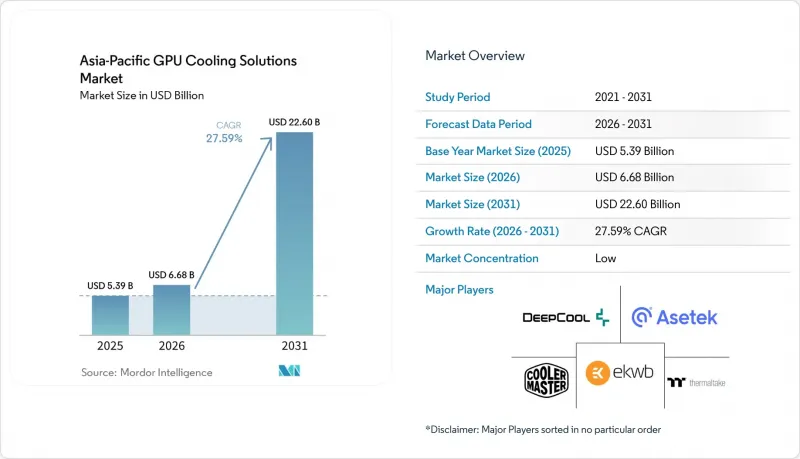

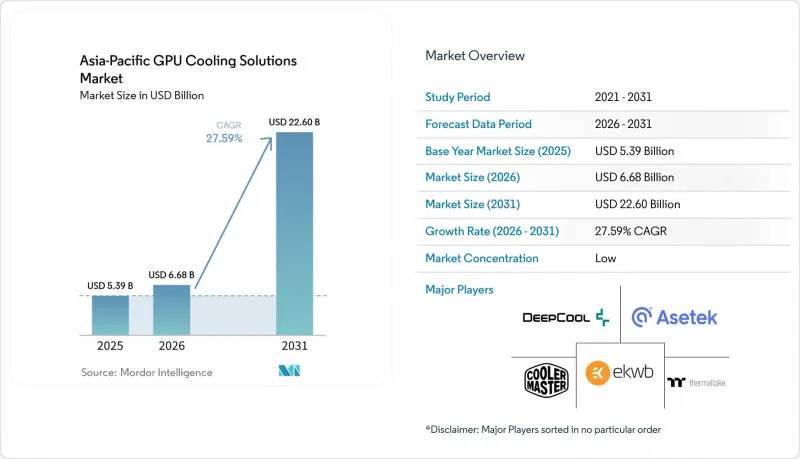

아시아태평양의 GPU 냉각 솔루션 시장 규모는 2025년 53억 9,000만 달러로 평가되었고, 2026년에는 66억 8,000만 달러로 추정되고, 2026-2031년 CAGR 27.59%로 성장을 지속할 전망이며, 2031년에는 226억 달러에 이를 것으로 예측됩니다.

본 보고서는 냉각 기술별(공랭식, 수랭식(직접 투 칩), 침지 냉각, 하이브리드 냉각), 냉각 수준별(컴포넌트 수준 냉각 및 서버/랙 수준 냉각), 도입 형태별(하이퍼스케일 클라우드, 엔터프라이즈, 엣지), GPU 전력 밀도별(300W 미만, 300W-700W, 700W 이상), 국가별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

아시아태평양의 GPU 냉각 솔루션 시장 동향 및 인사이트

아시아태평양 지역 각국 정부의 데이터센터 에너지 효율에 관한 규제

아시아태평양의 GPU 냉각 솔루션 시장은 에너지 효율을 단순한 ‘권장 사항’에서 ‘설계 요건’으로 전환하는 정책 프레임워크의 혜택도 누리고 있습니다. GB/T 44989-2024에 기반한 중국의 친환경 데이터센터 프레임워크 및 관련 에너지 효율 규제로 인해, 대규모 데이터 시설, 특히 고밀도 컴퓨팅 환경을 지원하는 시설의 운영 요건이 더욱 엄격해지고 있습니다. 일본의 2026년도 제로 에미션 데이터센터 상용화 프로그램과 탈탄소화 시설에 대한 광범위한 보조금 지원 덕분에, 첨단 냉각 설비에 대한 투자 회수 기간이 단축되고 있습니다. 2026년 5월에 통과된 한국의 ‘AI 데이터센터 특별법’은 국가 주도의 AI 인프라가 고밀도 시설에 대한 보다 신속한 조달과 보다 직접적인 정책 지원 하에 추진될 것임을 시사하고 있습니다. 실용적인 관점에서 볼 때, 이러한 프레임워크는 기존의 공랭식 설계로는 대응하기 어려운 GPU를 다량으로 사용하는 공간에서 더 낮은 PUE 목표를 달성할 수 있는 냉각 시스템을 뒷받침하는 것입니다. 아시아태평양의 GPU 냉각 솔루션 시장에 있어, 이는 GPU의 전력 밀도 향상이 이미 촉발했던 기술적 변화를 규제 준수가 더욱 가속화하고 있음을 의미합니다.

액체 냉각 방식의 고밀도 엣지·마이크로 데이터센터의 보급

두 번째 수요층은 하이퍼스케일 모델과는 확연히 구별되며, 최종 사용자의 워크로드와 더 가까운 곳에 위치한 소규모 AI 시설에서 발생하고 있습니다. Preferred Networks, 인터넷 이니셔티브 재팬, 그리고 JAIST는 직접 액체 냉각 설계, 물 대 공기 비율 7:3, 설계 PUE 1.1, WUE 0이라는 사양으로 일본에서 ‘AImod’의 운영을 시작했습니다. 이는 고밀도 도시 지역 AI 인프라에 있어 중요한 참고 사례가 되고 있습니다. 이러한 아키텍처가 주목받는 이유는 많은 엣지 사이트나 모듈형 사이트에서는 기존의 대형 냉각 시스템에 필요한 공간, 물, 또는 기계 설비의 설치 면적을 확보할 수 없기 때문입니다. 또한, 서울에 위치한 NHN Cloud의 7,656대 GPU 클러스터를 통해, 액체 냉각이 고밀도 구축을 지원하면서도 기존의 공랭 방식에 비해 에너지 효율을 향상시킬 수 있음을 입증했습니다. 추론 워크로드가 공장, 통신 거점, 교통 거점, 도시 주변 시설로 점점 더 가까이 다가옴에 따라, 일본, 한국, 싱가포르 및 일부 동남아시아 시장에서 소형 액체 냉각에 대한 수요가 더욱 두드러지고 있습니다. 그 결과, 아시아태평양의 GPU 냉각 솔루션 시장은 하이퍼스케일 캠퍼스를 넘어 확장되고 있으며, 랙 일체형 냉각 업체와 소형 CDU 공급업체의 고객 기반이 더욱 넓어지고 있습니다.

냉각수 공급망의 변동

두 번째 주요 제약 요인은 액침 방식 도입에 사용되는 특수 냉각수 공급망이 압박받고 변동이 심하다는 점입니다. 이 초안에서는 아시아태평양 지역의 대부분에서 유전체 액체의 조달처가 여전히 집중되어 있으며, 수입에 의존하고 있다는 점이 지적되고 있습니다. 이로 인해 공급 상황이 어려워질 경우, 사업자는 리드타임 관련 위험이나 인증 지연에 직면하게 됩니다. PFAS 관련 화학물질에 대한 규제 압력과 3M사의 Novec 제품 라인 철수는 여러 사업장에서 수명이 긴 냉각액이 필요한 기업들에게 추가적인 불확실성을 야기하고 있습니다. 이에 대응하여 지역 기업들은 현지에서 대체 방안을 마련하기 시작했으며, 그 일례로 2026년 5월 한국에서 S-Oil과 GST가 제휴를 맺고, 국내 냉각액 및 장비의 역량을 활용한 침지 냉각 솔루션 개발에 착수했습니다. 이는 유익한 첫걸음이지만, AI 클러스터의 도입 확대가 예상되는 가운데, 지역의 생산 능력은 아직 초기 단계에 머물러 있습니다. 아시아태평양의 GPU 냉각 솔루션 시장에서 이러한 상황은 ‘직접 투 칩(Direct-to-Chip)’ 시스템의 매력을 유지하고 있습니다. 왜냐하면 이 방식은 여전히 침지 냉각의 광범위한 보급을 저해하고 있는 유체에 대한 의존성을 부분적으로 피할 수 있기 때문입니다.

부문별 분석

2025년, 아시아태평양의 GPU 냉각 솔루션 시장 규모에서 공랭식은 49.15%를 차지했으며, 여전히 최대 냉각 기술 부문으로서의 위상을 유지했습니다. 한편, 액침 냉각 시장은 2031년까지 연평균 성장률(CAGR) 24.12%로 확대될 것으로 전망됩니다. 이러한 상황은 해당 지역에서 공기 흐름을 주로 활용하는 열 관리 방식을 기반으로 구축되었으며, 아직 완전한 액체 냉각으로의 전환 기준점에 도달하지 못한 기업, 공공 부문 및 소비자용 GPU 시스템의 도입 대수가 많기 때문입니다. 아시아태평양의 GPU 냉각 솔루션 시장에서는 게이밍, 워크스테이션 및 저밀도 서버 환경에서 여전히 상당수의 공랭식 시스템이 사용되고 있습니다. 특히, 예산이나 시설상의 제약으로 인해 대규모 업그레이드가 지연되고 있는 분야에서는 이러한 경향이 두드러집니다. 한편, 최신 AI 하드웨어가 열 밀도를 기존 공랭식 설계의 허용 작동 범위를 넘어 끌어올리고 있기 때문에 2031년까지 침지 냉각이 가장 빠르게 성장하는 기술 분야가 되고 있습니다.

직접 투 칩(DTC) 수냉 방식은 기존 인프라와 차세대 GPU의 전력 소비 범위를 연결하는 가장 실용적인 가교로서 그 입지를 공고히 하고 있습니다. 대부분의 경우, 침지 냉각보다 혼란을 최소화하면서 기존 서버 설계에 도입할 수 있기 때문에 전체 시스템을 재구축하지 않고도 새로운 가속기를 지원해야 하는 기업, 코로케이션 업체, 공공 부문 구매자들에게 매력적인 선택지가 되고 있습니다. 하이브리드 냉각 기술 역시 고밀도 도시 지역에서의 도입과 관련해 주목을 받고 있습니다. 특히, 고발열 부품에는 액체 냉각을, 시스템의 나머지 부분에는 잔류 공기 냉각을 도입하고자 하는 사업자들 사이에서 그 수요가 증가하고 있습니다. 일본의 AImod 시설은 물과 공기를 결합한 하이브리드 모델이 소규모 AI 도입 환경에서 높은 효율을 실현할 수 있음을 보여준 점에서 유익한 사례로 꼽힙니다. 아시아태평양의 GPU 냉각 솔루션 업계 전반에서는 기술 구성이 액체 기반 설계로 전환되고 있지만, 그 전환 경로는 시설의 연식, 워크로드의 강도, 그리고 가용 자본에 따라 여전히 차이가 있습니다.

2025년 기준으로 아시아태평양의 GPU 냉각 솔루션 시장 규모 중 서버 랙 수준의 냉각이 61.25%의 점유율을 차지했으며, 이는 예측 기간 동안 가장 빠르게 성장하는 냉각 수준이기도 합니다. 이러한 조합은 AI 데이터센터의 아키텍처에 발생한 뚜렷한 변화를 반영하고 있으며, 현재 랙은 개별 구성 요소의 집합체가 아니라 열 및 전력을 통합한 영역으로 취급되고 있습니다. 아시아태평양의 GPU 냉각 솔루션 시장이 이러한 방향으로 나아가고 있는 것은 통합형 GPU 시스템이 냉각액 경로 공유, 공통 모니터링 및 협력적인 페일세이프 제어 기능을 갖춘 긴밀하게 연동된 클러스터 형태로 도입되기 시작했기 때문입니다. 따라서 AI 팩토리나 국가 차원의 컴퓨팅 시설에서는 개별 구성 요소 수준의 솔루션보다 랙 수준의 냉각이 더 큰 가치를 제공합니다.

컴포넌트 수준의 냉각은 열 관리가 여전히 카드 단위로 이루어지고 도입 규모가 훨씬 작은 소비자용 게임, 워크스테이션 시스템 및 소규모 전문 환경에서는 여전히 중요합니다. 대만과 중국에 거점을 둔 공급업체들은 특히 애프터마켓 및 프로슈머 대상 채널에서 판매량 기반을 통해 계속해서 혜택을 누리고 있습니다. 그렇긴 하지만, 고밀도 AI 클러스터에는 시스템 전반에 걸친 협력적인 열 관리가 필요해짐에 따라, 매출 구성은 랙 규모의 플랫폼으로 점차 전환되고 있습니다. 서울에 위치한 NHN Cloud의 액체 냉각 클러스터는 이 모델의 운영상 유효성을 입증하고 있으며, 매우 대규모의 GPU 환경 전반에 걸쳐 압력, 유량, 온도를 모니터링하고 이에 연동된 랙 수준의 관리가 이루어지고 있습니다. 이러한 변화로 인해 랙 수준공급업체는 더 강력한 가격 결정력을 확보하는 동시에, 연구 개발(R&D)을 분배 장치, 매니폴드 시스템 및 연계된 랙 냉각 제어에 집중할 수 있게 됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the asia-Pacific gPU cooling solutions market size is expected to grow from USD 5.39 billion in 2025 to USD 6.68 billion in 2026 and is forecast to reach USD 22.60 billion by 2031 at 27.59% CAGR over 2026-2031.

This report is Segmented by Cooling Technology (Air Cooling, Liquid Cooling (Direct-To-Chip), Immersion Cooling, and Hybrid Cooling), Cooling Level (Component-Level Cooling and Server / Rack-Level Cooling), Deployment (Hyperscale-Cloud, Enterprise, and Edge), GPU Power Density (Below 300W, 300W - 700W, and Above 700W), and Country. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific GPU Cooling Solutions Market Trends and Insights

Data-Center Energy Efficiency Mandates By Asia-Pacific Governments

The Asia-Pacific GPU cooling solutions market is also benefiting from policy frameworks that turn energy efficiency from a preference into a design requirement. China's green data center framework under GB/T 44989-2024 and related energy efficiency rules is tightening the operating envelope for large data facilities, especially those that support dense compute deployments. Japan's fiscal 2026 zero-emission data center commercialization program and its broader subsidy support for decarbonized facilities are reducing the payback period for advanced cooling investments. South Korea's AI Data Center Special Act, cleared in May 2026, signaled that sovereign AI infrastructure will move forward with faster procurement and more direct policy support for high-density facilities. In practical terms, these frameworks favor cooling systems that can support lower PUE targets in GPU-heavy halls where legacy air designs struggle. For the Asia-Pacific GPU cooling solutions market, this means regulatory compliance is now reinforcing the same technology shift that GPU power density has already set in motion.

Proliferation Of Liquid-Cooled High-Density Edge Micro-Data Centers

A second layer of demand is coming from compact AI facilities that sit outside the hyperscale model and closer to end-use workloads. Preferred Networks, Internet Initiative Japan, and JAIST brought AImod into operation in Japan with a direct liquid cooling design, a 7:3 water-to-air ratio, a design PUE of 1.1, and a WUE of 0, which makes it an important reference point for dense urban AI infrastructure. That type of architecture is relevant because many edge and modular sites cannot absorb the space, water, or mechanical plant footprint associated with larger conventional cooling systems. NHN Cloud's 7,656-GPU cluster in Seoul also showed that liquid cooling can support dense deployment while improving energy performance compared with conventional air-cooled setups. As inference workloads move closer to factories, telecom sites, transport nodes, and city-edge facilities, the need for compact liquid cooling becomes more visible across Japan, South Korea, Singapore, and selected Southeast Asian markets. The Asia-Pacific GPU cooling solutions market is therefore widening beyond hyperscale campuses, which gives rack-integrated cooling vendors and compact CDU suppliers a broader customer base.

Supply-Chain Volatility For Coolant Fluids

The second major restraint is the tight and changing supply chain for specialty cooling fluids used in immersion deployments. The draft highlighted that dielectric fluid sourcing remains concentrated and import-dependent across much of the Asia-Pacific, which exposes operators to lead-time risk and qualification delays when supply conditions tighten. Regulatory pressure on PFAS-linked chemistries and the exit of 3M's Novec line have added another layer of uncertainty for operators that need long-life fluid choices across multiple sites. In response, regional players have started to build local alternatives, including the May 2026 partnership between S-Oil and GST in South Korea to develop an immersion cooling solution around domestically linked fluid and equipment capabilities. That is a useful first step, but regional capacity is still early relative to the expected rise in AI cluster deployment. In the Asia-Pacific GPU cooling solutions market, this keeps direct-to-chip systems attractive because they avoid part of the fluid dependency that still slows broader immersion adoption.

Other drivers and restraints analyzed in the detailed report include:

- Tax Incentives For Green IT Infrastructure In China And Japan

- Rising GPU Thermal Design Power In AI Workloads

- High Capital Expenditure Of Immersion Cooling Retrofits

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air cooling held 49.15% of the Asia-Pacific GPU cooling solutions market size in 2025, which kept it as the largest cooling technology segment, while immersion cooling is projected to expand at a 24.12% CAGR through 2031. That position came from the region's large installed base of enterprise, public sector, and consumer GPU systems that were built around airflow-heavy thermal management and have not yet crossed the threshold for full liquid adoption. The Asia-Pacific GPU cooling solutions market still has meaningful air-cooled volume in gaming, workstation, and lower-density server environments, particularly where budgets or facility limitations delay major upgrades. At the same time, immersion cooling is the fastest-growing technology segment through 2031 because the newest AI hardware is pushing heat density beyond the comfortable operating range of traditional air designs.

Direct-to-chip liquid cooling is gaining ground as the most practical bridge between installed infrastructure and next-generation GPU power envelopes. It can often be introduced into existing server designs with less disruption than immersion, which makes it attractive for enterprise, colocation, and public sector buyers that need to support newer accelerators without rebuilding entire halls. Hybrid cooling is also gaining traction in dense urban deployments, especially where operators want liquid cooling for high-heat components and residual air support for the rest of the system. Japan's AImod facility is a useful signal because it showed how a water-air hybrid model can achieve strong efficiency results in a compact AI deployment. Across the Asia-Pacific GPU cooling solutions industry, the technology mix is shifting toward liquid-based designs, but the transition path still differs by facility age, workload intensity, and available capital.

Server-rack-level cooling accounted for 61.25% share of the Asia-Pacific GPU cooling solutions market size in 2025, and it is also the fastest-growing cooling level over the forecast period. That combination reflects a clear architectural change in AI data centers, where the rack is now treated as a unified thermal and power domain rather than a collection of separate components. The Asia-Pacific GPU cooling solutions market is moving in this direction because integrated GPU systems are now deployed in tightly linked clusters with shared coolant routing, common monitoring, and coordinated fail-safe controls. Rack-level cooling, therefore, carries more value in AI factories and sovereign compute sites than isolated component-level solutions.

Component-level cooling still matters in consumer gaming, workstation systems, and lower-scale professional environments where thermal management remains card-specific, and the deployment unit is much smaller. Vendors based in Taiwan and China continue to benefit from that volume base, especially in aftermarket and prosumer channels. Even so, the revenue mix is migrating upward toward rack-scale platforms because dense AI clusters now require thermal management that is coordinated across the whole system. NHN Cloud's liquid-cooled cluster in Seoul illustrated the operational case for this model, with rack-level management tied to pressure, flow, and temperature monitoring across a very large GPU environment. That shift gives rack-level vendors stronger pricing power and keeps R&D focused on distribution units, manifold systems, and coordinated rack cooling controls.

List of Companies Covered in this Report:

- Cooler Master Technology Inc.

- Deepcool Industries Co., Ltd.

- Asetek A/S

- Noctua GmbH

- EKWB d.o.o.

- Alphacool International GmbH

- Thermaltake Technology Co., Ltd.

- Corsair Gaming Inc.

- Gigabyte Technology Co., Ltd.

- Micro-Star International Co., Ltd.

- ASUSTeK Computer Inc.

- ZALMAN Tech Co., Ltd.

- Arctic GmbH

- NZXT, Inc.

- Phanteks B.V.

- SilverStone Technology Co., Ltd.

- Aquacomputer GmbH and Co. KG

- Bykski Technology Co., Ltd.

- Bitspower International Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising GPU Thermal Design Power in AI Workloads

- 4.2.2 Data-Center Energy Efficiency Mandates by Asia-Pacific Governments

- 4.2.3 Proliferation of Liquid-Cooled High-Density Edge Micro-Data Centers

- 4.2.4 Tax Incentives for Green IT Infrastructure in China and Japan

- 4.2.5 Vertical Integration of Hyperscalers into Direct-to-Chip Cooling Hardware

- 4.2.6 Emergence of Immersion-Ready GPU Reference Designs from Semiconductor OEMs

- 4.3 Market Restraints

- 4.3.1 High Capital Expenditure of Immersion Cooling Retrofits

- 4.3.2 Supply-Chain Volatility for Coolant Fluids

- 4.3.3 Limited Skilled Workforce for Liquid Loop Commissioning

- 4.3.4 Lack of Common Open Standards Across Cooling Technologies

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Cooling Technology

- 5.1.1 Air Cooling

- 5.1.2 Liquid Cooling (Direct-to-Chip)

- 5.1.3 Immersion Cooling

- 5.1.4 Hybrid Cooling

- 5.2 By Cooling Level

- 5.2.1 Component-Level Cooling

- 5.2.2 Server / Rack-Level Cooling

- 5.3 By Deployment

- 5.3.1 Hyperscale / Cloud

- 5.3.2 Enterprise

- 5.3.3 Government and Research (HPC)

- 5.3.4 Edge

- 5.4 By GPU Power Density

- 5.4.1 Below 300W

- 5.4.2 300W - 700W

- 5.4.3 Above 700W

- 5.5 By Country

- 5.5.1 China

- 5.5.2 Japan

- 5.5.3 South Korea

- 5.5.4 India

- 5.5.5 Southeast Asia

- 5.5.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cooler Master Technology Inc.

- 6.4.2 Deepcool Industries Co., Ltd.

- 6.4.3 Asetek A/S

- 6.4.4 Noctua GmbH

- 6.4.5 EKWB d.o.o.

- 6.4.6 Alphacool International GmbH

- 6.4.7 Thermaltake Technology Co., Ltd.

- 6.4.8 Corsair Gaming Inc.

- 6.4.9 Gigabyte Technology Co., Ltd.

- 6.4.10 Micro-Star International Co., Ltd.

- 6.4.11 ASUSTeK Computer Inc.

- 6.4.12 ZALMAN Tech Co., Ltd.

- 6.4.13 Arctic GmbH

- 6.4.14 NZXT, Inc.

- 6.4.15 Phanteks B.V.

- 6.4.16 SilverStone Technology Co., Ltd.

- 6.4.17 Aquacomputer GmbH and Co. KG

- 6.4.18 Bykski Technology Co., Ltd.

- 6.4.19 Bitspower International Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment