|

시장보고서

상품코드

2063867

아시아태평양의 인재 채용 소프트웨어 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Asia Pacific Talent Acquisition Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

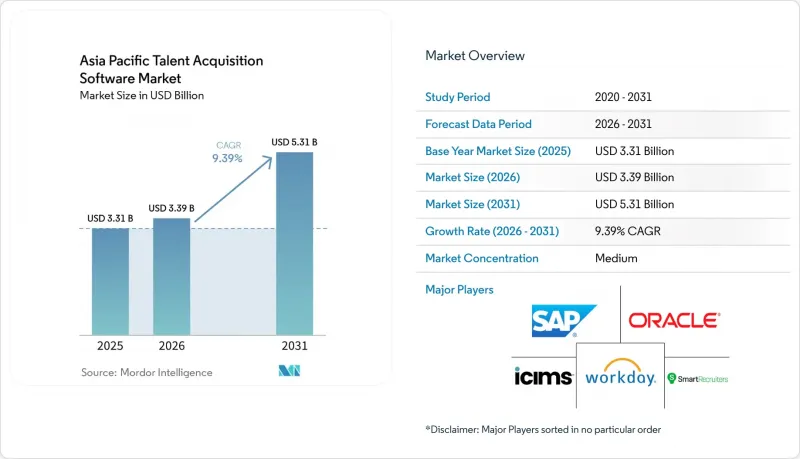

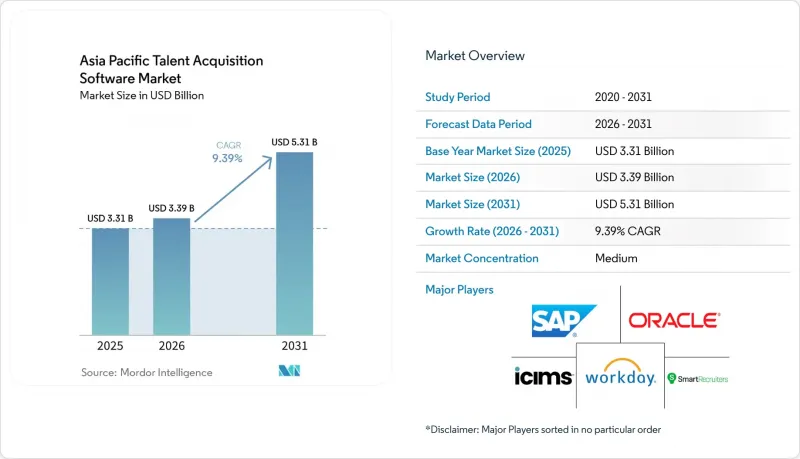

Mordor Intelligence에 의하면, 아시아태평양 인재 채용 소프트웨어 시장 규모는 2025년 33억 1,000만 달러에서 2026년에는 33억 9,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 9.4%로 성장을 지속하여, 2031년에는 53억 1,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 도입 모델(클라우드, On-Premise, 하이브리드), 용도(지원자 추적 시스템, 채용 마케팅 등), 기업 규모(대기업, 중소기업), 업종(정보기술·통신, 헬스케어 및 생명과학 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

아시아태평양 인재 채용 소프트웨어 시장 동향 및 인사이트

AI를 활용한 후보자 매칭 및 선별 절차의 도입 확대

아시아태평양의 인재 채용 소프트웨어 시장에서 AI는 시험적인 도구에서 핵심 운영 계층으로 전환되었습니다. 싱가포르에서는 2025년 2분기 기준으로, 기업의 82%가 채용, 신입 사원 온보딩 또는 교육에 AI를 활용하고 있으며, 이는 지역 평균인 81%와 세계 평균인 67%를 상회하는 수치입니다. 이는 해당 지역에서 AI 주도형 인사 업무 흐름이 얼마나 빠르게 정착되고 있는지를 보여줍니다. 한국에서는 2026년 4월에 발표된 조사에 따르면, 기업의 65%가 AI 채용 에이전트를 이미 도입했거나 도입을 검토 중이며, 특히 인재 발굴과 지원자 심사가 자동화의 주요 대상으로 꼽혔습니다. 이러한 변화가 중요한 이유는 고용주가 더 이상 심사 시간 단축만을 목적으로 AI를 도입하는 것이 아니라, 후보자 풀을 확대하고 대규모 채용에서도 일관된 평가를 수행하기 위해 AI를 활용하고 있기 때문입니다. 중국 및 해당 지역의 주요 기술 허브에서는 AI를 활용한 채용 심사가 이미 표준적인 채용 절차의 일부가 되었으며, 아시아태평양의 인재 채용 소프트웨어 시장에 서비스를 제공하는 벤더에 대한 최소 제품 요구 사항이 높아지고 있습니다. 규제가 강화됨에 따라 구매자들은 단순한 속도나 자동화뿐만 아니라, 감사 추적 기록 제시, 인간의 감독 기능, 설명 가능한 의사결정을 지원할 수 있는 도구를 요구하고 있습니다.

클라우드 우선 전략을 통한 HR 디지털화 가속화

클라우드 서비스는 도입 장벽을 낮추고, 여러 관할 구역에 걸친 규정 준수 사항을 최신 상태로 유지할 수 있기 때문에 아시아태평양의 인재 채용 소프트웨어 시장의 대부분에서 기본 아키텍처로 자리 잡고 있습니다. 특히, 기존 HR 기술 스택이 제한적이었던 시장에서는 조직이 레거시 시스템 전환에 비용을 들이지 않고도 API 우선 시스템으로 직접 전환할 수 있기 때문에 그 가치는 매우 높습니다. Omni HR에 관한 사례 연구에 따르면, 클라우드로 전환한 후 고객 온보딩 시간이 50% 단축되고 IT 비용이 25-30% 절감된 것으로 보고되어, 동남아시아의 소규모 인사 팀에게 클라우드의 경제성이 왜 매력적인지 잘 드러나고 있습니다. 운용 측면에서의 장점도 마찬가지로 중요합니다. 클라우드 플랫폼은 싱가포르의 중앙적립기금(CPF), 말레이시아의 근로자적립기금(EPF), 태국의 사회보험청(SSO) 등 법정 기여 규정 업데이트를 자동화할 수 있으므로, 국경을 초월한 채용 팀이 반복적으로 수작업으로 처리해야 하는 부담을 줄일 수 있기 때문입니다. SAP는 2026년 4월, 2026년 상반기 SuccessFactors 업데이트를 출시하며 이러한 방향성을 한층 더 강화했습니다. 이번 업데이트에서는 채용, 급여 계산, 온보딩의 모든 영역에 에이전트형 AI가 도입되었으며, 지속적인 개선과 모듈 간 데이터 활용을 위해 클라우드 인프라에 의존하는 기능이 탑재되었습니다. 그 결과, 아시아태평양의 인재 채용 소프트웨어 시장에서 클라우드는 더 이상 단순한 기능적 선택지가 아니라, 고도화된 채용 기능을 구현하기 위한 기본 요건으로 자리 잡고 있습니다.

아시아·태평양 지역의 파편화된 데이터 개인정보 보호 규제

아시아태평양의 인재 채용 소프트웨어 시장에서 역량 기반 채용의 중요성이 커지고 있습니다. 이는 직무 요건의 변화가 고정된 자격 정보로는 따라잡을 수 없을 정도로 급속히 진행되고 있기 때문입니다. 2025년 6월에 발표된 조사에 따르면, 직무에 필요한 역량은 2016년부터 2024년 사이에 40% 변화했으며, 2030년까지 추가로 70% 변화할 것으로 예측됩니다. 이 조사에 따르면, 불필요한 자격 요건을 배제함으로써 인도에서는 최대 11.4배, 인도네시아에서는 9.5배, 호주에서는 7.7배까지 후보자 풀을 확대할 수 있는 것으로 나타났습니다. 이러한 변화로 인해 이력서에 대한 의존도가 낮아지고, 구조화된 면접, 평가 도구, 그리고 보다 정교한 역량 매핑에 대한 수요가 증가하고 있습니다. 또한, 기업이 외부 채용을 시작하기 전에 인접한 역량을 갖춘 기존 직원을 파악할 수 있는 사내 인사 이동 도구의 가치도 높아지고 있습니다. 싱가포르에서는 ‘MyCareersFuture’나 ‘Workforce Singapore’와 같은 프로그램을 통해 이러한 변화에 대응하기 위한 공공 정책적 지원을 강화하고 있습니다. 이러한 프로그램들은 역량 기반 선발을 지원하는 소프트웨어와 고용주의 채용 관행을 조화시키는 것을 목적으로 합니다.

부문별 분석

2025년에는 클라우드 기반 솔루션 도입이 68.7%를 차지하며, 이미 아시아태평양 인재 채용 소프트웨어 시장의 지출에서 핵심을 이루고 있는 것으로 나타났으며, 2031년까지 연평균 성장률(CAGR) 10.6%로 성장할 것으로 전망됩니다. 이 조합이 주목받는 이유는 주요 모델이 신규 도입, 중소기업으로의 확대, 그리고 공공 부문의 현대화를 통해 여전히 시장 점유율을 확대하고 있기 때문입니다. 실무적인 관점에서 볼 때, 구매자가 클라우드를 선택하는 이유는 빈번한 기능 업데이트, 채용 프로세스 전반에 걸친 손쉬운 통합, 그리고 On-Premise 환경에서의 유지보수 부담 경감을 원하기 때문입니다. 또한, 규정 준수 측면에서도 설득력이 있습니다. 국경을 넘어 사업을 전개하는 고용주는 사내의 긴 릴리스 주기를 기다리지 않고도 법령이나 데이터 처리 워크플로를 업데이트할 수 있는 시스템이 필요하기 때문입니다. 많은 조직에게 있어 결정해야 할 사항은 더 이상 ‘클라우드인가, On-Premise인가’가 아니라, ‘워크플로우의 어느 부분을 클라우드로 옮겨야 하는가’, 그리고 ‘나머지 On-Premise 시스템을 얼마나 신속하게 연결할 수 있는가’에 있습니다.

또한, 클라우드 도입은 아시아태평양 인재 채용 소프트웨어 업계의 제품 방향성을 뒷받침하고 있습니다. 왜냐하면 새로운 AI 기능은 지속적인 모델 업데이트와 모듈 간 데이터 접근에 의존하고 있기 때문입니다. SAP의 2026년 4월 상반기 릴리스에서는 채용 및 온보딩 프로세스 전반에 에이전트형 AI가 통합되면서, 현대의 인재 워크플로가 클라우드 인프라에 의존하고 있다는 사실이 다시 한번 부각되었습니다. 또한 AWS는 ‘Omni HR’ 사례 연구에서 클라우드 전환을 통해 온보딩 시간을 50% 단축하고 IT 비용을 25-30% 절감했다는 운영상의 이점을 보고하고 있습니다. 이는 사내 지원 체계가 제한적인 지역의 인사팀에게 있어 매우 관련성이 높은 결과라고 할 수 있습니다. On-Premise형 시스템은 데이터 주권이 여전히 심각한 설계상의 과제로 남아 있는 일본이나 한국의 국방 분야 및 일부 금융 환경 등 규제가 엄격한 환경에서는 여전히 일정한 입지를 차지하고 있습니다. 따라서 하이브리드 방식은 기업이 기밀 데이터를 국내에 보관하면서 클라우드 기반의 분석 및 매칭 도구를 활용할 수 있는 ‘가교 모델’로서 주목을 받고 있습니다. 바로 이러한 균형 덕분에, 아시아태평양의 인재 채용 소프트웨어 시장이 지속적으로 클라우드로 전환되고 있음에도 불구하고, 특정 부문에서는 현지 인프라를 배제하지 않고 있는 것입니다.

2025년 기준으로, 지원자 추적 시스템(ATS)은 용도 부문 매출의 29.8%를 차지하며, 용도 수준에서 아시아태평양 인재 채용 소프트웨어 시장에서 가장 큰 단일 부문으로 자리매김하고 있습니다. ATS는 채용 요건, 지원자의 동의, 워크플로우 추적, 채용 관련 문서 관리에 있어 기록 시스템의 역할을 수행하기 때문에 많은 도입 사례에서 출발점으로서의 역할을 계속해서 수행하고 있습니다. 대기업들은 여전히 이 계층을 업무의 기반으로 삼고, 여기에 후보자 관계 관리, 채용 마케팅, 분석, 온보딩 등의 모듈을 단계적으로 추가하고 있습니다. 개인정보 보호 규제로 인해 보다 명확한 감사 추적 기록과 체계적인 기록이 요구됨에 따라, 이 역할의 중요성은 더욱 커지고 있습니다. 또한, 구매 패턴 역시 기존 공급업체에 유리하게 작용하고 있습니다. 왜냐하면 핵심 워크플로가 확립되면, 인접한 모듈은 교체하는 것보다 추가하는 편이 더 쉽기 때문입니다. 이것이 바로 아시아태평양의 채용 소프트웨어 시장 전체가 더욱 전문적인 도구로 확대되는 가운데서도 ATS가 중심적인 위치를 유지하고 있는 이유입니다.

현재 가장 빠르게 성장세를 보이고 있는 분야는 면접 관리 및 평가 분야로, 고용주들이 자격이나 경력만을 중시하는 경향이 줄어들면서 2031년까지 연평균 성장률(CAGR) 11.4%를 나타낼 것으로 전망됩니다. 스킬 변화에 관한 조사는 이러한 변화를 설명하는 한 가지 요인이 됩니다. 직무 요건이 급속히 변화하고 있기 때문에 정적인 이력서만으로는 미래의 적성을 보여주는 지표로서의 신뢰성이 떨어지고 있기 때문입니다. 이에 대응하여 고용주는 역량 평가, 지도형 면접, 직무 관련 평가 등 보다 체계적인 평가 절차를 마련하고 있습니다. 그 결과, 선발 과정에서 일관된 채점, 면접관 팀의 조정, 그리고 보다 정확한 증거 수집을 지원하는 소프트웨어에 대한 수요가 증가하고 있습니다. 따라서 용도의 구조는 더욱 다층화되어 있으며, ATS가 프로세스의 중심을 담당하고, 그 주변에서 평가 도구가 확대되고 있습니다. 아시아태평양의 인재 채용 소프트웨어 시장 공급업체들에게 있어 이것이 의미하는 바는 분명합니다. 핵심 워크플로를 확보하는 것은 유익하지만, 성장은 점점 더 그 주변에서 이루어지는 기술 중심의 평가를 얼마나 잘 지원할 수 있는지에 달려 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the asia pacific talent acquisition software market size is expected to grow from USD 3.31 billion in 2025 to USD 3.39 billion in 2026 and is forecast to reach USD 5.31 billion by 2031 at 9.4% CAGR over 2026-2031.

This report is Segmented by Deployment Model (Cloud, On-Premise, and Hybrid), Application (Applicant Tracking System, Recruitment Marketing, and More), Enterprise Size (Large Enterprises and Small and Medium Enterprises), Industry Vertical (Information Technology and Telecom, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia Pacific Talent Acquisition Software Market Trends and Insights

Rising Adoption Of AI-Based Candidate Matching And Screening

AI has moved from a pilot tool to a core operating layer in the Asia Pacific talent acquisition software market. In Singapore, 82% of organizations were already using AI for hiring, onboarding, or training in Q2 2025, ahead of the regional average of 81% and the global average of 67%, indicating how quickly the region has normalized AI-led people workflows. In South Korea, a survey published in April 2026 found that 65% of companies had adopted or were considering AI recruiting agents, with sourcing and applicant review standing out as the main targets for automation. This shift matters because employers are no longer buying AI only to reduce screening time; they are also using it to widen candidate reach and support more consistent evaluation across large hiring volumes. In China and major technology hubs across the region, AI-assisted screening has already become part of standard recruitment practice, raising the minimum product expectations for vendors serving the Asia Pacific talent acquisition software market. As regulations become tighter, buyers also want tools that can show audit trails, provide human oversight, and support explainable decision-making rather than just speed and automation.

Accelerating Cloud-First HR Digitalization

Cloud delivery has become the default architecture for much of the Asia Pacific talent acquisition software market because it reduces deployment friction and keeps compliance updates up to date across multiple jurisdictions. The value case is especially strong in markets where earlier HR technology stacks were limited, as organizations can move directly to API-first systems rather than spend on legacy migrations. A case study on Omni HR reported a 50% reduction in customer onboarding time and 25-30% lower IT costs after the cloud migration, underscoring why cloud economics are appealing to lean HR teams in Southeast Asia. The operational case is equally important because cloud platforms can automate updates to statutory contribution rules, such as Singapore's Central Provident Fund, Malaysia's Employees Provident Fund, and Thailand's Social Security Office, reducing the need for repeated manual effort for cross-border hiring teams. SAP reinforced this direction in April 2026 when it released the 1H 2026 SuccessFactors update, featuring agentic AI across recruiting, payroll, and onboarding, with features that depend on cloud infrastructure for continuous improvement and cross-module data use. As a result, cloud is no longer a feature choice in the Asia Pacific talent acquisition software market; it is increasingly the base requirement for advanced recruiting capability.

Fragmented Data-Privacy Regulations Across Asia-Pacific

Skills-based hiring is becoming more important in the Asia Pacific talent acquisition software market because job requirements are changing faster than static credentials can reflect. Research published in June 2025 found that the skills required for jobs changed by 40% between 2016 and 2024 and are projected to change by another 70% by 2030. The same research showed that removing unnecessary qualification filters can expand the potential candidate pool by up to 11.4 times in India, 9.5 times in Indonesia, and 7.7 times in Australia. That change reduces reliance on resumes as the main filter and raises demand for structured interviews, assessment tools, and better skills mapping. It also increases the value of internal mobility tools that can identify existing employees with adjacent skills before an employer starts an external search. Singapore has added public policy support to this shift through programs tied to MyCareersFuture and Workforce Singapore, which help align employer practices with software that supports competency-based selection.

Other drivers and restraints analyzed in the detailed report include:

- Intensifying Competition For Digital Talent In High-Growth Sectors

- Shift Toward Skills-Based Hiring Frameworks

- Integration Complexity With Legacy HR Information Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based deployment accounted for 68.7% in 2025, indicating it already represented the core of spending in the Asia Pacific talent acquisition software market, and it is also projected to grow at a 10.6% CAGR through 2031. That combination is notable because the leading model is still gaining share through new implementations, expansion into SMEs, and public-sector modernization. In practical terms, buyers are choosing the cloud because they want frequent feature updates, easier integration across recruiting steps, and less local maintenance. The compliance argument is strong as well, since cross-border employers need systems that can update statutory and data-handling workflows without long internal release cycles. For many organizations, the decision is no longer cloud versus on-premise, but how much of the workflow should sit in the cloud and how quickly the remaining local systems can be connected.

Cloud adoption also supports the product direction of the Asia Pacific talent acquisition software industry, as new AI functions depend on continuous model updates and data access across modules. SAP's April 2026 1H release embedded agentic AI across recruiting and onboarding, which reinforced the dependence of modern talent workflows on cloud infrastructure. AWS also documented operational gains in its Omni HR case study, where cloud migration reduced onboarding time by 50% and lowered IT costs by 25-30%, a result with clear relevance for regional HR teams with limited internal support. On-premise systems still hold a place in highly regulated settings such as defense and some financial environments in Japan and South Korea, where data sovereignty remains a serious design issue. Hybrid deployment is therefore gaining traction as a bridge model, since it lets employers keep sensitive data in-country while still using cloud-based analytics and matching tools. That balance explains why the Asia Pacific talent acquisition software market continues to move toward the cloud, while not eliminating local infrastructure in certain segments.

Applicant tracking systems accounted for 29.8% of application-layer revenue in 2025, making ATS the largest single segment in the Asia Pacific talent acquisition software market at the application level. ATS remains the entry point for many purchases because it acts as the system of record for requisitions, applicant consent, workflow tracking, and hiring documentation. Large enterprises still treat this layer as the operational backbone onto which candidate relationship management, recruitment marketing, analytics, and onboarding modules are added over time. That role has become even more important as privacy rules require clearer audit trails and more structured records. The purchasing pattern also favors incumbents because once the core workflow is in place, adjacent modules are easier to add than replace. This is why ATS retains a central position even while the broader Asia Pacific talent acquisition software market expands into more specialized tools.

The fastest-growing momentum now lies in interview management and assessment, which is projected to grow at a 11.4% CAGR through 2031 as employers place less weight on credentials alone. Research on skills change helps explain the shift because rapid movement in job requirements makes static resumes weaker indicators of future fit. Employers are responding by building more structured evaluation processes, including competency checks, guided interviews, and role-relevant assessments. That in turn lifts demand for software that supports consistent scoring, panel coordination, and better evidence capture during the selection process. The application mix is therefore becoming more layered, with ATS holding the process center while assessment tools expand around it. For vendors in the Asia Pacific talent acquisition software market, the implication is clear: winning the core workflow is helpful, but growth increasingly depends on how well they support skills-led evaluation around it.

List of Companies Covered in this Report:

- SAP SE

- Oracle Corporation

- Workday Inc.

- Automatic Data Processing Inc.

- International Business Machines Corporation

- Cornerstone OnDemand Inc.

- iCIMS Inc.

- SmartRecruiters Inc.

- Jobvite Inc.

- Greenhouse Software Inc.

- Lever Inc.

- Avature Limited

- Bullhorn Inc.

- Workable Technology Limited

- Zoho Corporation Pvt. Ltd.

- Eightfold AI Inc.

- BambooHR LLC

- Ceridian HCM Holding Inc.

- Randstad N.V.

- Recruit Holdings Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Cloud-First HR Digitalization

- 4.2.2 Rising Adoption of AI-Based Candidate Matching and Screening

- 4.2.3 Intensifying Competition for Digital Talent in High-Growth Sectors

- 4.2.4 Government Incentives for Workforce Digital Transformation

- 4.2.5 Expansion of Internal Talent Marketplaces Among Large Enterprises

- 4.2.6 Shift Toward Skills-Based Hiring Frameworks

- 4.3 Market Restraints

- 4.3.1 Fragmented Data-Privacy Regulations Across Asia-Pacific

- 4.3.2 Integration Complexity with Legacy HR Information Systems

- 4.3.3 Persistent AI Bias and Explainability Concerns

- 4.3.4 Cost Barriers Limiting SME Adoption of Advanced Platforms

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Application

- 5.2.1 Applicant Tracking System (ATS)

- 5.2.2 Candidate Relationship Management (CRM)

- 5.2.3 Recruitment Marketing

- 5.2.4 Onboarding

- 5.2.5 Interview Management and Assessment

- 5.2.6 Other Applications

- 5.3 By End User Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End User Enterprise Industry Vertical

- 5.4.1 Information Technology (IT) and Telecom

- 5.4.2 Banking, Financial Services and Insurance (BFSI)

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Industrial Manufacturing

- 5.4.5 Retail and eCommerce

- 5.4.6 Government and Public Sector

- 5.4.7 Other End User Enterprise Industry Verticals

- 5.5 By Country

- 5.5.1 China

- 5.5.2 India

- 5.5.3 Japan

- 5.5.4 South Korea

- 5.5.5 Singapore

- 5.5.6 Malaysia

- 5.5.7 Thailand

- 5.5.8 Australia

- 5.5.9 Rest of Asia Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Workday Inc.

- 6.4.4 Automatic Data Processing Inc.

- 6.4.5 International Business Machines Corporation

- 6.4.6 Cornerstone OnDemand Inc.

- 6.4.7 iCIMS Inc.

- 6.4.8 SmartRecruiters Inc.

- 6.4.9 Jobvite Inc.

- 6.4.10 Greenhouse Software Inc.

- 6.4.11 Lever Inc.

- 6.4.12 Avature Limited

- 6.4.13 Bullhorn Inc.

- 6.4.14 Workable Technology Limited

- 6.4.15 Zoho Corporation Pvt. Ltd.

- 6.4.16 Eightfold AI Inc.

- 6.4.17 BambooHR LLC

- 6.4.18 Ceridian HCM Holding Inc.

- 6.4.19 Randstad N.V.

- 6.4.20 Recruit Holdings Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment