|

시장보고서

상품코드

2063930

북미의 통합 시설 관리 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)North America Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

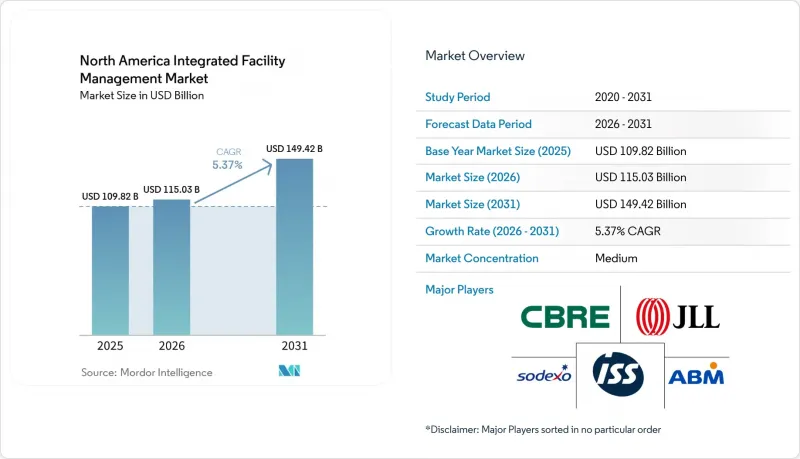

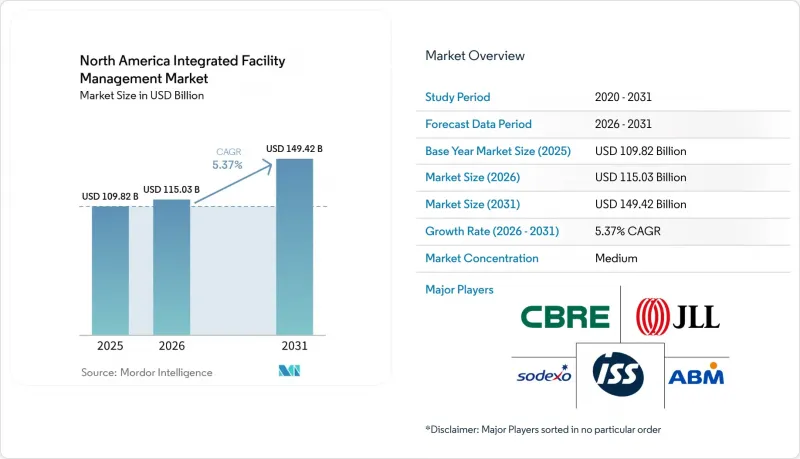

Mordor Intelligence에 의하면, 북미의 통합 시설 관리(FM) 시장 규모는 2025년 1,098억 2,000만 달러로 평가되었고, 2026년 1,150억 3,000만 달러로 추정되고, 2031년까지 1,494억 2,000만 달러로 확대될 전망이며, 2026-2031년 CAGR 5.4%를 나타낼 것으로 예측됩니다.

본 보고서는 서비스 유형별(하드 시설 관리(자산 관리, MEP 및 HVAC 서비스 등), 소프트 시설 관리(사무 지원 및 보안, 청소 서비스, 케이터링 서비스 등)), 최종 사용자별(상업, 의료, 산업 및 공정 부문, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

북미의 통합 시설 관리 시장 동향 및 인사이트

운영 비용 최적화에 대한 수요 증가

북미의 통합 시설 관리 시장은 단기적인 인플레이션 우려보다는 비용 관리의 필요성에 의해 주도되고 있습니다. JLL의 조사에 따르면, FM 리더의 81%가 공급업체 수를 줄이고 계약을 통합하며, 데이터 기반의 벤치마킹을 주요 비용 절감 수단으로 활용할 계획인 것으로 나타났습니다. 이는 단일 서비스 공급업체보다 통합 서비스 제공업체에 더 직접적인 이점을 주는 것입니다. ABM은 2025 회계연도에 전년 대비 12% 증가한 사상 최대 규모인 19억 달러의 신규 수주를 기록했다고 발표했으며, 이러한 실적이 단일 창구를 통한 책임 체계와 측정 가능한 운영 비용 절감을 요구하는 고객 수요에 기인한 것이 및 분석했습니다. 이는 IFM이 단순한 아웃소싱 서비스의 형태로만 여겨지는 것이 아니라, 총 소유 비용을 절감하는 수단으로서 점점 더 높이 평가받고 있음을 의미합니다. 이러한 변화는 대규모의 분산된 포트폴리오를 보유한 조직에게 특히 중요한데, 계약 통합이 진행될수록 단일 IFM 제공업체가 담당할 수 있는 서비스 범위가 확대되기 때문입니다.

비핵심 서비스의 아웃소싱 확대

북미의 통합 시설 관리 시장은 기술 및 업무 공간 지원 기능 전반에 걸친 아웃소싱 확대의 혜택을 누리고 있습니다. 아웃소싱의 동향은 청소나 케이터링에 그치지 않고, 빌딩 자동화, 에너지 관리, MEP(기계·전기·배관) 유지보수 분야로까지 확대되고 있으며, 이에 따라 각 계약의 평균 금액이 상승하고 있습니다. ABM은 자사가 직접 운영하는 인재 모델을 통해 직원의 최대 90%를 하청이 아닌 직접 고용으로 유지할 수 있다고 밝혔으며, 이러한 특징은 지점 간 서비스 품질의 편차를 줄여주기 때문에 조달 담당자들의 관심을 끌고 있습니다. 존슨컨트롤스는 2026년 보고서에서 직원의 95%가 주당 최소 3일은 사무실에 출근하고 있다고 밝혔습니다. 이는 테넌트가 현재, 많은 사내 팀이 대규모로 제공할 수 있는 범위를 넘어서는 보다 일관된 현장 대응과 서비스 밀도를 필요로 하고 있음을 의미합니다. 이로 인해 아웃소싱된 FM의 고객 기반이 확대되면서, 그동안 내부적인 이유로 미뤄왔던 통합 계약에 더 많은 조직이 참여하고 있습니다.

숙련된 기술자와 FM 인력의 부족

북미의 통합 시설 관리 시장은 공급업체의 사업 확장 속도를 제한하는 구조적인 인력 부족 문제에 계속해서 직면하고 있습니다. REMI Network가 인용한 IFMA의 데이터에 따르면, 북미 시설 관리직의 평균 채용 기간은 2025년 3분기에 3.6개월에 달했습니다. JLL의 조사에서도 FM 리더의 45%가 숙련 기술 인력 부족을 주요 우려 사항으로 꼽았으며, 이러한 압박은 지방이나 생활비가 높은 지역에서 가장 심한 것으로 나타났습니다. 의료시설 관리(HFM) 부문에서는 'HFM Magazine'이 HVAC(공조·환기·급배수) 기술직의 채용 난이도가 94%에 달했다고 보도했으며, 이는 기술적으로 고도의 환경 분야에서 인력 부족이 얼마나 심각해지고 있는지를 보여주고 있습니다. 이 문제는 단순한 채용 활동의 문제에 그치지 않습니다. IFMA의 추산에 따르면, 기존 시설 관리자의 40%가 2026년까지 은퇴할 것으로 예상되며, 이로 인해 북미의 통합 시설 관리 시장에서 계약의 복잡성이 증가하는 한편, 노하우 상실 위험도 높아지고 있기 때문입니다.

부문별 분석

하드 시설 관리는 북미 통합 시설 관리 시장에서 가장 빠르게 성장하고 있는 서비스 유형으로, 2031년까지 연평균 성장률(CAGR) 6.7%로 확대될 것으로 전망됩니다. 가동 시간이 직접적인 운영 가치로 이어지는 데이터센터, 반도체 팹, 의료시설에 대한 투자가 이어지는 가운데, 자산 관리, MEP 서비스, 소방 시스템 등 안전 부문 전반에 걸쳐 수요가 증가하고 있습니다. CBRE 보고서에 따르면, 2025년 북미 데이터센터의 순흡수 면적은 사상 최고치인 2,497.6만 제곱피트에 달했으며, 주요 시장의 공실률은 1.4%까지 하락했습니다. 이는 기술 집약적인 서비스 계약의 장기적인 파이프라인을 뒷받침하는 요인이 되고 있습니다. 또한, 존슨 컨트롤즈의 조사에 따르면, 2026년에 새로운 AI 도입을 계획하고 있는 시설 관리자의 52%가 AI 투자의 최우선 과제로 예측 유지보수를 꼽았으며, 이는 엔지니어링 및 데이터 처리 역량을 갖춘 하드 FM 제공업체의 입지를 강화하는 요인이 될 것입니다.

소프트 FM은 2025년 북미 통합 시설 관리 시장 점유율의 62.3%를 차지했으며, 상업시설, 공공시설, 호텔 및 리조트 시설을 막론하고 여전히 가장 큰 수익 기반이 되고 있습니다. 북미의 통합 시설 관리 산업에서는 청소 서비스, 사무 지원 및 보안, 케이터링 서비스가 여전히 소프트 FM 수요의 대부분을 차지하고 있지만, 그중에서도 청소는 여전히 가격에 가장 민감한 부문으로 남아 있습니다. 존슨컨트롤즈의 보고서에 따르면, 2026년에는 조직의 75%가 공간 관리 및 계획을 위해 업무 공간 관리 기술을 활용할 것이며, 이에 따라 소프트 FM 서비스 제공은 입주율 분석 및 실시간 인력 배치 결정으로 한 걸음 더 다가서고 있습니다. 이러한 변화로 인해, 서비스 제공업체가 서비스 성과를 이용률 동향 및 사용자 경험과 연계할 수 있게 되면, 소프트 FM 계약은 데이터 중심적인 성격이 더욱 강해져 그 정당성을 주장하기가 더 쉬워집니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the north america integrated facility management market size is projected to expand from USD 109.82 billion in 2025 and USD 115.03 billion in 2026 to USD 149.42 billion by 2031, registering a CAGR of 5.4% between 2026 to 2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), End User (Commercial, Healthcare, Industrial and Process Sector, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America Integrated Facility Management Market Trends and Insights

Growing Demand for Operational Cost Optimization

The North America integrated facility management market is being pushed by cost control more than by short-term inflation concerns. JLL found that 81% of FM leaders planned to consolidate contracts with fewer suppliers and use data-led benchmarking as their main cost-reduction tools, which directly favors integrated providers over single-service vendors. ABM reported record new sales bookings of USD 1.9 billion in fiscal 2025, up 12% year over year, and linked that performance to client demand for single-source accountability and measurable operating savings. This means IFM is increasingly being assessed as a way to reduce total occupancy cost, not only as an outsourced service package. That shift is especially relevant for organizations with large and dispersed portfolios because each contract consolidation expands the service scope that one IFM provider can hold.

Increased Outsourcing of Non-Core Services

The North America integrated facility management market is also benefiting from broader outsourcing across technical and workplace support functions. The outsourcing trend now extends beyond janitorial and catering into building automation, energy management, and MEP maintenance, which raises the average value of each contract. ABM said its self-performing workforce model can keep as much as 90% of staff directly employed rather than subcontracted, and that feature is gaining procurement appeal because it reduces service variability across locations. Johnson Controls reported in 2026 that 95% of employees were in the office at least 3 days per week, which means occupiers now need more consistent onsite response and service density than many in-house teams can deliver at scale. This is widening the buyer base for outsourced FM and pulling more organizations into integrated contracts that they had previously delayed for internal reasons.

Shortage of Skilled Technicians and FM Workforce

The North America integrated facility management market continues to face a structural labor constraint that limits how quickly providers can scale. IFMA data cited by REMI Network showed that the average time to fill a facility management role in North America reached 3.6 months in Q3 2025. JLL also found that 45% of FM leaders viewed skilled trade labor shortages as a primary concern, with the pressure strongest in rural locations and high cost-of-living areas. In healthcare FM, HFM Magazine reported a 94% fill difficulty rate for HVAC trades, which shows how severe the shortage has become in technically sensitive environments. The problem is larger than recruitment alone because IFMA estimates that 40% of existing facilities managers will retire by 2026, which raises the risk of knowledge loss at the same time that contract complexity is rising in the NA integrated facility management market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Smart Building Technologies

- Stringent Energy Efficiency and Sustainability Regulations

- High Upfront Costs of Integrated Digital Platforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hard facility management is the fastest-growing service type in the North America integrated facility management market and is forecast to expand at a 6.7% CAGR through 2031. Demand is rising across asset management, MEP services, and fire systems and safety as investment continues in data centers, semiconductor fabs, and healthcare campuses where uptime has direct operating value. CBRE reported record net absorption of 2,497.6 MW in North American data centers during 2025, while vacancy in primary markets fell to 1.4%, which supports a long pipeline of technically intensive service contracts. Johnson Controls also found that predictive maintenance was the top AI investment priority for 52% of facility managers planning new AI deployments in 2026, which strengthens the position of Hard FM providers with engineering and data capability.

Soft facility management held 62.3% of the North America integrated facility management market share in 2025 and remains the largest revenue base across commercial, institutional, and hospitality properties. In the North America integrated facility management industry, cleaning services, office support and security, and catering services still account for most Soft FM demand, although cleaning remains the most price-sensitive part of the mix. Johnson Controls reported that 75% of organizations used workplace management technology for space management and planning in 2026, which is pushing soft service delivery closer to occupancy analytics and real-time staffing decisions. That shift is making Soft FM contracts more data-aware and more defensible when providers can connect service output with utilization trends and user experience.

List of Companies Covered in this Report:

- CBRE Group Inc.

- Jones Lang LaSalle Incorporated

- Sodexo S.A.

- ISS A/S

- ABM Industries Incorporated

- Cushman and Wakefield plc

- Compass Group PLC

- Aramark

- GDI Integrated Facility Services Inc.

- EMCOR Group Inc.

- BGIS

- Johnson Controls International plc

- Colliers International Group Inc.

- Apleona GmbH

- Mitie Group plc

- Serco Group plc

- Allied Universal

- Atalian Servest

- Honeywell International Inc.

- C&W Services

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Operational Cost Optimization

- 4.2.2 Increased Outsourcing of Non-Core Services

- 4.2.3 Rapid Adoption of Smart Building Technologies

- 4.2.4 Stringent Energy Efficiency and Sustainability Regulations

- 4.2.5 Rising Tariff-Induced Supply Chain Reconfigurations Favoring Local IFM Providers

- 4.2.6 Expansion of Data Center Corridors Driving Specialized 24/7 FM Contracts

- 4.3 Market Restraints

- 4.3.1 Shortage of Skilled Technicians and FM Workforce

- 4.3.2 High Upfront Costs of Integrated Digital Platforms

- 4.3.3 Client Concerns Around Vendor Lock-In in Single-Source Contracts

- 4.3.4 State-Level Variability in Licensing and Compliance Standards

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 By End User

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-User Industries

- 5.3 By Geography

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 CBRE Group Inc.

- 6.4.2 Jones Lang LaSalle Incorporated

- 6.4.3 Sodexo S.A.

- 6.4.4 ISS A/S

- 6.4.5 ABM Industries Incorporated

- 6.4.6 Cushman and Wakefield plc

- 6.4.7 Compass Group PLC

- 6.4.8 Aramark

- 6.4.9 GDI Integrated Facility Services Inc.

- 6.4.10 EMCOR Group Inc.

- 6.4.11 BGIS

- 6.4.12 Johnson Controls International plc

- 6.4.13 Colliers International Group Inc.

- 6.4.14 Apleona GmbH

- 6.4.15 Mitie Group plc

- 6.4.16 Serco Group plc

- 6.4.17 Allied Universal

- 6.4.18 Atalian Servest

- 6.4.19 Honeywell International Inc.

- 6.4.20 C&W Services

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment