|

시장보고서

상품코드

2072911

독일의 화학제품 물류 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Germany Chemical Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

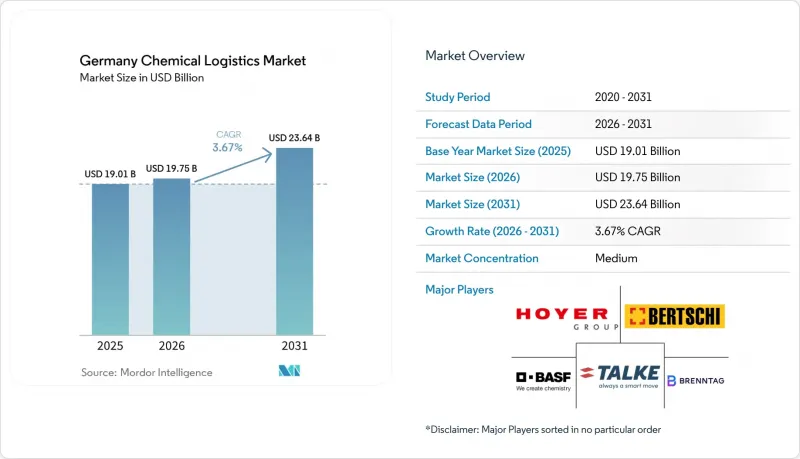

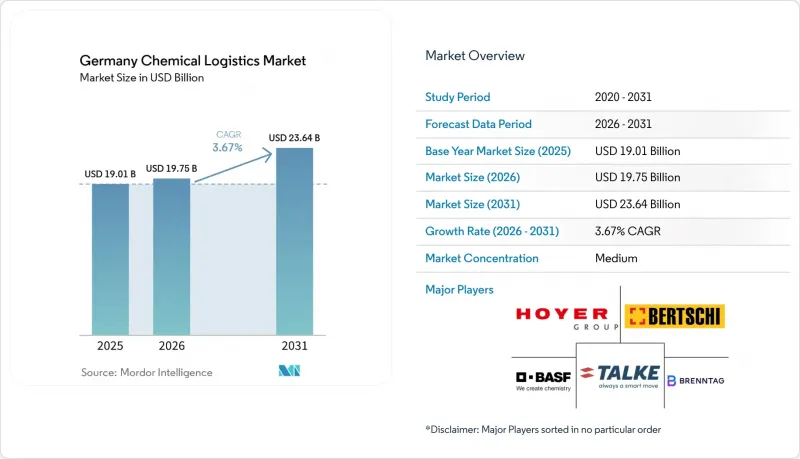

Mordor Intelligence에 의하면, 독일 화학제품 물류 시장 규모는 2025년 190억 1,000만 달러에서 2026년에는 197억 5,000만 달러로 확대되어 2031년까지 236억 4,000만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 3.67%로 성장할 전망입니다.

본 보고서는 서비스 유형(운송, 창고·유통, 부가가치 서비스), 위험물 분류(위험물, 비위험물), 온도 관리(온도 관리 있음, 온도 관리 없음), 최종 이용 산업(의약품, 화장품, 특수 화학제품 등), 지역(노르트라인-베스트팔렌주, 바이에른주, 기타 주)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

독일의 화학제품 물류 시장 동향과 인사이트

국내 화학제품 생산 회복세 가속화: 취약한 회복세가 선택적인 물류 수요를 창출하고 있습니다.

독일의 화학·제약 업계는 2025년 사업 실적이 부진한 상태에서 2026년을 맞이했습니다. 이는 업계 생산량이 3.3% 감소하고, 매출액이 3% 감소했으며, 설비 가동률이 평균 72.5%에 그쳤기 때문입니다. 이러한 배경으로 인해, 독일 화학제품 물류 시장의 회복은 광범위하지 않고 선택적인 수준에 그치고 있습니다. 이는 생산량이 소폭 회복되기만 해도 유조선 이용, 창고 회전율, 포장 업무는 증가하지만, 벌크 화물의 취급량은 완전히 회복되지 않기 때문입니다. 이로 인해 멀티서비스 사업자에게는 어느 정도 여유가 생깁니다. 대량 생산 업체들이 여전히 낮은 가동률로 운영을 이어가는 반면, 제약 관련 물류 흐름이 네트워크의 가동률을 뒷받침할 수 있기 때문입니다. 또한, 독일 화학제품 물류 시장에서 생산이 광범위하게 회복되는 추세가 정착되기 전에 재고 보충 움직임이 주춤해질 경우, 조기에 운송 능력을 확충한 사업자는 이익률 하락에 직면할 가능성이 있음을 의미합니다. 따라서 자산 배분은 핵심 화학제품의 운송량과 규모는 작지만 규제가 엄격한 화물을 모두 처리할 수 있는 혼합형 네트워크로 전환되고 있습니다.

EU-ADR 준수 요건이 전문 업체에 대한 수요를 견인: 전문 역량은 여전히 뚜렷한 차별화 요소

위험물 운송에는 훈련을 받은 직원, 인증된 절차, 규제 대상 물질을 위해 설계된 보관 시설이 필요하기 때문에 규정 준수는 여전히 독일 화학제품 물류 시장 수요를 이끄는 직접적인 원동력입니다. 화주가 거래처 수를 줄이고자 할 경우, 도로 운송, 탱크 취급, 재포장, 검사, 서류 작성 지원을 종합적으로 제공할 수 있는 사업자가 더 유리한 입장에 있습니다. 2025년 10월에 가동을 시작한 레샤코사의 브레멘 물류 센터는 위험물 전용 인프라와 분류에 따른 보관 능력을 확충하고 있으며, 이는 규정 준수가 요구되는 수요에 대응하기 위해 공급업체가 어떻게 투자하고 있는지를 보여줍니다. BASF가 루트비히스하펜에 도입한 dTEX 역시 이와 같은 방향성을 보여주고 있습니다. 이는 트럭 배차를 거의 완벽하게 자동화하고, 부지 진입, 이동 관리, 워크플로우 실행과 같은 디지털 측면을 강화했기 때문입니다. 실제로 독일의 화학제품 물류 시장에서는 규정 준수를 단순한 백오피스 업무의 부담이 아닌, 사업 운영상의 역량으로 인식하는 공급업체가 높이 평가받고 있습니다. 고객들이 감사 대응 체계나 매니지드 서비스 지원을 더욱 중요하게 여기게 됨에 따라, 이러한 격차는 더욱 확대될 가능성이 있습니다.

운전기사 부족과 도로 운임 상승: 단기적인 주요 제약 요인은 여전히 도로 운송 능력

독일의 화학제품 물류 시장에서 화학제품 운송은 여전히 육상 운송이 큰 비중을 차지하고 있기 때문에 자격을 갖춘 운전자가 부족해지면 이용 가능한 운송 능력이 급격히 부족해집니다. 위험물 운송의 경우, 화학물질 화주가 일반 화물 운송보다 더 엄격한 취급 및 안전 요건을 충족할 수 있는 운전자를 필요로 하기 때문에 그 부담은 더욱 커집니다. 이로 인해 경로 계획, 야드 자동화, 네트워크 밀도의 중요성은 높아지지만, 이러한 도구들은 제약을 해소하는 것이 아니라 완화하는 데 그칠 뿐입니다. 또한, 이를 통해 특히 도로 구간을 철도나 터미널에서의 집하·혼재와 연계할 수 있는 사업자에게는 복합운송의 매력을 높여주고 있습니다. 독일의 화학제품 물류 시장에서는 탱크 운송 능력, 철도 접근성, 그리고 엄격한 일정 관리 체계를 갖춘 사업자가 도로 화물 운송이 난항을 겪을 때에도 수익률을 유지하기 쉬운 입장에 있습니다. 따라서 화주들은 물류 입찰에서 회복탄력성과 운송 수단의 유연성을 더욱 중요하게 여기게 되었습니다.

부문별 분석

2025년, 독일의 화학제품 물류 시장에서 운송 부문은 59.2%의 점유율을 차지했으며, 탱커, 철도 화물차, 바지선, 계약 운송에 걸친 수익 기반이 여전히 핵심 운송 활동에 있음을 확인했습니다. 독일의 화학제품 생산 거점은 노르트라인-베스트팔렌주, 바덴-뷔르템베르크주, 바이에른주의 각 클러스터에 분산되어 있으며, 이들 모두 국내의 밀집된 화물 운송망에 의존하고 있기 때문에 도로 운송은 여전히 이 기능에서 가장 큰 비중을 차지하고 있습니다. 철도 업계는 주요 생산업체들에게 전용 화학제품 수송 열차가 핵심 운송 수단으로서의 입지를 확고히 다져가고 있는 만큼, 독일 화학제품 물류 시장에서 그 역할을 지속적으로 강화하고 있습니다. BASF와 Lineas는 2025년 5월, 루트비히스하펜과 안트베르펜 간 화물 셔틀 운행 횟수가 1,000회 왕복을 달성한 것을 기념하며, 정기 철도 노선이 현재 특정 국경을 넘는 화학물질 운송 경로에서 핵심적인 역할을 하고 있음을 부각시켰습니다.

부가가치 서비스는 2031년까지 연평균 성장률(CAGR) 6.50%로 확대될 것으로 예상되며, 독일 화학제품 물류 시장에서 가장 빠르게 성장하고 있는 물류 기능이 될 것입니다. 화학 제조업체들이 플랜트 설비의 유지보수를 위해 지원 업무를 외부에 위탁하는 추세에 따라, 수요는 창고 내 혼합, 라벨 재부착, 드럼통에의 재충전, 검사 및 서류 작성 지원으로 이동하고 있습니다. DACHSER사는 2026년에 라슈타트에 새로운 위험물 창고를 가동할 예정이며, 이러한 시기는 화학제품 생산량이 점차 회복됨에 따라 수요가 더욱 증가할 것이라는 전망을 반영한 것입니다. Leschaco사의 브레멘 지사도 같은 메시지를 전하고 있습니다. 이 시설은 전용 위험물 보관 시설과 규제 대상 화학물질의 흐름에 대응할 수 있는 폭넓은 계약 물류 기능을 모두 갖추고 있기 때문입니다. 그 결과, 독일의 화학제품 물류 시장에서는 단순히 제품을 보관하는 것뿐만 아니라, 업무상의 복잡성을 해소할 수 있는 창고 기능의 가치가 점점 더 중요시되고 있습니다.

2025년 기준으로 위험 화학물질은 독일 화학제품 물류 시장 규모의 63%를 차지하고 있으며, 2031년까지 연평균 성장률(CAGR) 5.67%로 확대되고 있습니다. 이는 ADR(유럽 위험물 운송 규정)을 준수하는 운송, 인증된 보관 시설, 그리고 전문 탱크 자산이 수행하는 핵심적인 역할을 여실히 보여주고 있습니다. 많은 규제 대상 물질은 여전히 전용 운송 및 취급이 필요하기 때문에 기초 화학제품의 생산이 부진한 상황에서도 독일 화학제품 물류 시장에서 이 분야는 구조적으로 중요한 위치를 계속 차지하고 있습니다. 브렌트나흐사는 2025년 2분기에 독일의 유해물질 보관 시설인 GSZ 카이저슬라우테른을 인수하여 중부 유럽에서의 사업 기반을 강화하는 동시에, 규제 대상 물질의 운영 거점을 확대했습니다. 이러한 움직임은 경기 침체기에도 사업자들이 인증된 유해물질 인프라에 장기적인 가치를 인정하고 있음을 보여줍니다.

이 부문의 상업적 논리는 변화하고 있습니다. 왜냐하면, 이익률의 질은 더 이상 순수한 취급량에 좌우되기보다는 인증 유무, 감사에 대한 대응 체계, 그리고 취급의 정확성에 따라 결정되는 경향이 강해지고 있기 때문입니다. 독일의 화학제품 물류 업계에서는 인증을 받은 사업자가 장기적인 거점 계약이나 네트워크 계약을 따낼 수 있는 반면, 전문성이 낮은 운송업체는 가격 변동이 심한 단기 계약 업무로 밀려나고 있습니다. 비위험물 분야에서는 기술적 장벽이 적고, 보다 광범위한 화물 네트워크를 통해 대량의 화물을 운송할 수 있기 때문에 가격 측면에서의 압박이 커지고 있습니다. 한편, 위험물 물류는 기존의 위험물 보관·유통 능력과 시너지를 낼 수 있는 리튬 이온 배터리 취급과 같은 관련 분야에서도 뒷받침을 받고 있습니다. 이에 따라 독일의 화학제품 물류 시장에서는 설비, 교육, 창고 관리, 규정 준수 지원을 단일 운영 모델로 통합할 수 있는 공급업체가 계속해서 우위를 점하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측(금액, 2026-2031년)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the germany chemical logistics market size is expected to increase from USD 19.01 billion in 2025 to USD 19.75 billion in 2026 and reach USD 23.64 billion by 2031, growing at a CAGR of 3.67% over 2026-2031.

This report is Segmented by Service Type (Transportation, Warehousing & Distribution, Value-Added Services), by Hazard Class (Hazardous, Non-Hazardous), by Temperature Control (Temp-Controlled, Non-Temp-Controlled), by End Use Industry (Pharmaceutical, Cosmetics, Specialty Chemicals, and More), and by Region (NRW, Bavaria, Rest of States). The Market Forecasts are Provided in Terms of Value (USD).

Germany Chemical Logistics Market Trends and Insights

Accelerated Domestic Chemical Output Recovery: Fragile Uptick Creates Selective Logistics Demand

Germany's chemical and pharmaceutical base entered 2026 from a weak 2025 operating position, because industry production fell 3.3%, sales declined 3%, and capacity utilization averaged 72.5%. That backdrop keeps recovery in the Germany chemical logistics market selective rather than broad-based, because even a modest pickup in output lifts tanker use, warehouse turns, and packaging activity without fully restoring bulk volumes. This gives multi-service operators a buffer, since pharma-linked flows can support network utilization while bulk producers continue to run at lower rates. It also means providers that add capacity too early in the Germany chemical logistics market may face weaker margins if restocking fades before a broader production recovery takes hold. Asset allocation is therefore moving toward mixed networks that can serve both core chemical volumes and smaller, more regulated shipments.

EU-ADR Compliance Driving Specialist Demand: Specialist Capability Remains a Clear Divider

Compliance remains a direct driver of demand in the Germany chemical logistics market, as hazardous-goods transport requires trained staff, certified processes, and storage assets designed for regulated materials. Operators that can combine road transport, tank handling, repacking, inspection, and documentation support are in a stronger position when shippers want fewer counterparties. Leschaco's Bremen logistics center, commissioned in October 2025, added dedicated hazardous-goods infrastructure and classification-based storage capabilities, demonstrating how providers are investing in compliance-intensive demand. BASF's dTEX deployment at Ludwigshafen also points in the same direction, because it nearly fully automated truck dispatch and strengthened the digital side of site access, movement control, and workflow execution. In practice, the Germany chemical logistics market is rewarding providers that treat compliance as an operating capability rather than a back-office burden. That gap is likely to widen as customers put more value on audit readiness and managed service support.

Driver Shortage and Rising Road Freight Rates: Road Capacity Remains the Main Short-Term Constraint

Road transport still accounts for a large share of chemical movement in the Germany chemical logistics market, so any shortage of qualified drivers quickly tightens available capacity. The pressure is greater in hazardous-goods transport because chemical shippers need drivers who can meet stricter handling and safety requirements than those in standard freight operations. This raises the value of route planning, yard automation, and network density, yet those tools only soften the constraint rather than remove it. It also increases the appeal of intermodal configurations, especially for operators that can connect road legs with rail or terminal-based consolidation. In the Germany chemical logistics market, providers with tank capacity, rail access, and disciplined scheduling are better placed to defend margins when road freight tightens. Shippers are therefore placing more emphasis on resilience and mode flexibility in logistics tenders.

Other drivers and restraints analyzed in the detailed report include:

- Growing Chemiepark-Based Integrated Logistics: Site Logistics Continues to Deepen Switching Costs

- Adoption of IoT Tanks and Digital Twins: Digital Control Is Moving Into Daily Operations

- Rhine Waterway Congestion and Lock Downtime: Corridor Dependence Adds Network Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation held 59.2% of the Germany chemical logistics market share in 2025, confirming that core movement activity still anchors revenue across tankers, rail wagons, barges, and contract haulage. Road transport remained the largest part of this function because Germany's chemical production base is spread across clusters in North Rhine-Westphalia, Baden-Wurttemberg, and Bavaria, all of which depend on dense domestic freight links. Rail continued to strengthen its role in the Germany chemical logistics market as dedicated chemical shuttles moved closer to backbone status for large producers. BASF and Lineas marked the 1,000th round trip of their freight shuttle between Ludwigshafen and Antwerp in May 2025, underscoring that scheduled rail links are now central to selected cross-border chemical lanes.

Value-added services are projected to grow at a 6.50% CAGR through 2031, making this the fastest-expanding logistics function in the Germany chemical logistics market. Demand is shifting toward in-warehouse blending, relabeling, re-drumming, inspection, and documentation support, as chemical producers seek to protect plant capital and outsource support work. DACHSER is commissioning a new hazardous materials warehouse in Rastatt in 2026, and the timing reflects expectations of stronger demand as chemical output gradually improves. Leschaco's Bremen site adds the same message, because the facility combines dedicated hazardous storage with broader contract logistics capability for regulated chemical flows. As a result, the Germany chemical logistics market is placing greater value on warehouse capabilities that can absorb operational complexity rather than just storing product.

Hazardous chemicals accounted for 63% of the Germany chemical logistics market size in 2025 and are expanding at a CAGR of 5.67% through 2031, underscoring the central role of ADR-ready transport, certified storage, and specialized tank assets. This part of the Germany chemical logistics market remains structurally important even when basic chemical output is soft, because many regulated substances still require dedicated transport and handling. Brenntag strengthened its central European footprint in Q2 2025 through the acquisition of GSZ Kaiserslautern, a hazardous substance storage facility in Germany, expanding its operational base for regulated materials. That move indicates that operators still see long-term value in certified hazardous infrastructure even during a weaker cycle.

The commercial logic inside this segment is shifting, because margin quality now depends less on pure volume and more on certification, audit readiness, and handling precision. In the Germany chemical logistics industry, certified operators can compete for long-term site and network contracts, while less specialized carriers are pushed toward more volatile spot work. The non-hazardous side faces more pricing pressure, since larger bulk flows can be routed through broader freight networks with fewer technical barriers. Hazardous logistics also gains support from adjacent categories such as lithium-ion battery handling, which fit well with existing dangerous-goods storage and distribution capability. This keeps the Germany chemical logistics market tilted toward providers that can combine equipment, training, warehousing, and compliance support in one operating model.

Complete Report Scope:

- By Logistics Function

- Transportation

- Road

- Air

- Sea and Inland Waterways

- Rail

- Warehousing, Distribution and Inventory Management

- Value-added Services and Others

- Transportation

- By Hazard Class

- Hazardous Chemicals

- Non-hazardous Chemicals

- By Temperature Control

- Temperature-Controlled (Refrigerated/Heated)

- Non-Temperature-Controlled

- By End Use Industry

- Pharmaceutical

- Cosmetic

- Oil and Gas

- Specialty Chemicals

- Other End-Users

- By Region

- North Rhine-Westphalia

- Bavaria (Bayern)

- Baden-Wurttemberg

- Rest of States

List of Companies Covered in this Report:

- HOYER Group

- Bertschi AG

- TALKE Group

- BASF SE

- Brenntag SE

- Imperial Chemical Logistics GmbH

- Rhenus Group

- Kuehne+Nagel

- DSV (incl. DB Schenker)

- DHL Supply Chain

- CEVA Logistics (CMA CGM)

- GEODIS

- Noerpel Group

- Paneuropa Transport

- Den Hartogh Logistics

- VTG Tanktainer

- Suttons Group

- Leschaco Group

- Stolt-Nielsen

- Univar Solutions

- Lanfer Logistik

- DACHSER SE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview & Role of Logistics in Chemical

- 4.2 Chemical Industry Spending Trends

- 4.3 Market Drivers

- 4.3.1 Accelerated Domestic Chemical Output Recovery

- 4.3.2 EU-ADR Compliance Driving Specialist Demand

- 4.3.3 Export-Oriented Supply-Chain Complexity

- 4.3.4 Growing Chemiepark-Based Integrated Logistics

- 4.3.5 Adoption of IoT Tanks and Digital Twins

- 4.3.6 Green-Hydrogen Corridor Build-Out

- 4.4 Market Restraints

- 4.4.1 Driver Shortage and Rising Road Freight Rates

- 4.4.2 Carbon-Pricing Linked Cost Escalation

- 4.4.3 Scarcity Of Temperature-Controlled Rail Tanks

- 4.4.4 Rhine Waterway Congestion and Lock Downtime

- 4.5 Regulatory Framework

- 4.6 Value Chain and Distribution Channel Architecture Analysis

- 4.7 Technology Innovations Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Rivalry Among Competitors

- 4.9 Evolution of Chemical Logistics Requirements

- 4.10 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size & Growth Forecasts (Value, 2026-2031)

- 5.1 By Logistics Function

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Air

- 5.1.1.3 Sea and Inland Waterways

- 5.1.1.4 Rail

- 5.1.2 Warehousing, Distribution and Inventory Management

- 5.1.3 Value-added Services and Others

- 5.1.1 Transportation

- 5.2 By Hazard Class

- 5.2.1 Hazardous Chemicals

- 5.2.2 Non-hazardous Chemicals

- 5.3 By Temperature Control

- 5.3.1 Temperature-Controlled (Refrigerated/Heated)

- 5.3.2 Non-Temperature-Controlled

- 5.4 By End Use Industry

- 5.4.1 Pharmaceutical

- 5.4.2 Cosmetic

- 5.4.3 Oil and Gas

- 5.4.4 Specialty Chemicals

- 5.4.5 Other End-Users

- 5.5 By Region

- 5.5.1 North Rhine-Westphalia

- 5.5.2 Bavaria (Bayern)

- 5.5.3 Baden-Wurttemberg

- 5.5.4 Rest of States

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 HOYER Group

- 6.4.2 Bertschi AG

- 6.4.3 TALKE Group

- 6.4.4 BASF SE

- 6.4.5 Brenntag SE

- 6.4.6 Imperial Chemical Logistics GmbH

- 6.4.7 Rhenus Group

- 6.4.8 Kuehne+Nagel

- 6.4.9 DSV (incl. DB Schenker)

- 6.4.10 DHL Supply Chain

- 6.4.11 CEVA Logistics (CMA CGM)

- 6.4.12 GEODIS

- 6.4.13 Noerpel Group

- 6.4.14 Paneuropa Transport

- 6.4.15 Den Hartogh Logistics

- 6.4.16 VTG Tanktainer

- 6.4.17 Suttons Group

- 6.4.18 Leschaco Group

- 6.4.19 Stolt-Nielsen

- 6.4.20 Univar Solutions

- 6.4.21 Lanfer Logistik

- 6.4.22 DACHSER SE

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment