|

시장보고서

상품코드

2072914

중국의 화학제품 물류 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)China Chemical Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

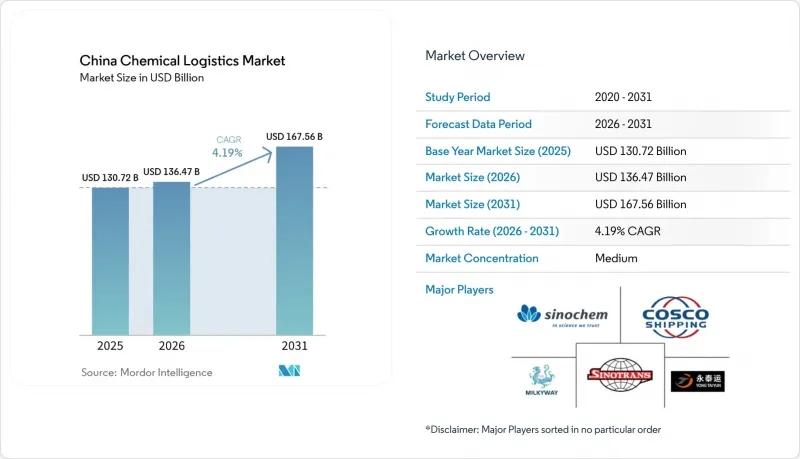

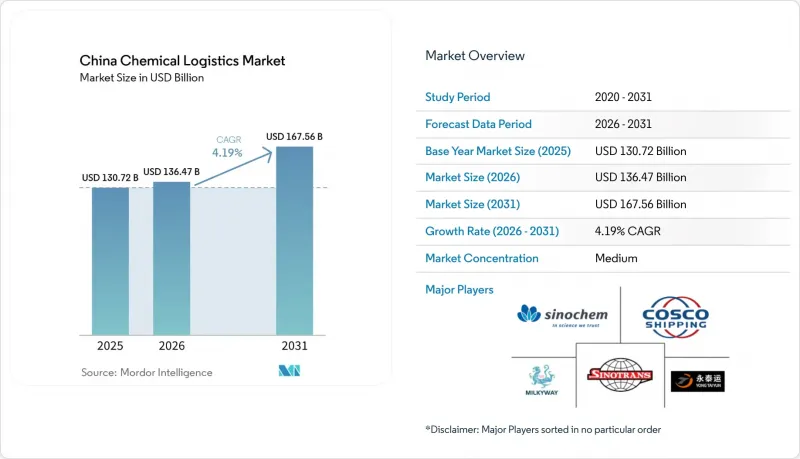

Mordor Intelligence에 의하면, 중국 화학제품 물류 시장 규모는 2025년에 1,307억 2,000만 달러, 2026년에 1,364억 7,000만 달러되어, 2031년까지 1,675억 6,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 4.19%로 성장할 전망입니다.

본 보고서는 서비스별(운송, 창고·유통, 부가가치 서비스), 위험물 분류별(위험물 및 비위험물), 온도 관리별(온도 관리 있음 및 온도 관리 없음), 최종 이용 산업별(의약품, 화장품, 특수 화학제품 등), 지역별(북부, 북동부, 동부 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

중국 화학제품 물류 시장 동향과 인사이트

석유화학 생산 능력의 서쪽에서 동쪽으로의 이동이 국내 운송량을 끌어올렸습니다.

중국의 화학제품 물류 시장은 해안 지역의 클러스터에서 내륙 및 서부 각 성으로 석유화학 생산 능력이 이동함에 따라 재편되고 있습니다. 신장, 닝샤, 산시, 쓰촨 지역의 석탄 화학 산업에 대한 투자로 인해 메탄올, 에틸렌글리콜, 방향족 화합물, 아세트산의 장거리 국내 수송량이 증가하고 있습니다. 기존 화동 지역의 물류 시스템은 수출입 흐름을 중심으로 구축되었기 때문에 내륙 지역을 기점으로 하는 이러한 국내 운송 노선에서는 효율이 떨어지고 있습니다. 우한항의 강릉 석유화학 터미널은 이러한 변화에 대한 직접적인 대응책이라고 할 수 있습니다. 이 터미널은 양쯔강 중·업스트림에 대규모 공공 석유화학 허브를 추가함으로써, 내륙의 생산 거점과 동부 수요 거점을 더욱 긴밀하게 연결해 줄 것이기 때문입니다. 허베이성이 2025년까지 총액 2,010억 위안(278억 달러)에 달하는 60건의 화학 프로젝트를 우선적으로 추진하겠다는 방침을 밝힌 것은 내륙으로의 물류망 확장이 중국 서부 지역에만 국한된 것이 아니라, 새로운 화물 수요를 위한 북쪽 방향의 축도 구축되고 있음을 보여줍니다. 이러한 생산 지도의 변화에 따라, 중국의 화학제품 물류 시장에서는 해안 항구를 거점으로 하는 화물 운송 네트워크에만 의존하는 것이 아니라, 하천, 철도, 도로 운송을 단일 서비스 플랫폼에서 통합할 수 있는 사업자가 높이 평가받고 있습니다.

IMO의 2026년 탈탄소화 목표가 화학제품 탱커 선단의 선박 교체를 촉구하고 있습니다.

중국의 화학제품 물류 시장은 IMO의 탈탄소화 및 선박 효율 기준과 관련된 선단 교체 주기에 의해서도 견인되고 있습니다. 광저우 조선 국제는 2025년, 474,500 DWT급 LR1형 화학제품·제품 운반선 4척 중 첫 번째 선박을 예정보다 빨리 인도했습니다. 이 선박들은 EEDI 3단계 요건을 충족할 뿐만 아니라, 듀얼 연료로 개조할 여지도 확보되어 있습니다. 난징 탱커사도 2025년에 메탄올 운반이 가능한 6,600 dwt 스테인리스제 화학제품 운반선 3척을 발주했으며, 2028년 상반기에 인도될 예정입니다. 이는 운임 시세가 부진한 상황에서도 선주들이 여전히 자본을 투자하고 있음을 보여줍니다. SSY의 예측에 따르면, 전 세계 화학제품 운반선 수주 잔고의 46%가 2026년에 인도될 전망이며, 이는 노후 선박이 선단에서 퇴역하기 전에 단기적인 공급 압박이 발생할 가능성이 있음을 시사합니다. 또한, COSCO SHIPPING Energy Transportation도 2025년 5월에 9,200 dwt급 스테인리스 스틸 화학제품 운반선 1척을 발주한 바 있으며, 이는 국내 운항사들이 여전히 연안 전문 운송 능력을 확대하고 있음을 뒷받침하고 있습니다. 따라서 중국의 화학물질 물류 시장은 탈탄소화 관련 규정 준수 및 위험물 화물 감시가 개별 규제 워크플로가 아닌 단일 디지털 운영 시스템을 통해 처리되는 구조로 전환되고 있습니다.

2025년의 "쿠니요시" 사고 이후 터널 통행 규제 강화

2025년의 “‘코쿠료’ 사고로 인해 터널 통행 규제가 강화된 결과, 중국의 화학물질 물류 시장에서는 일부 위험물 운송 노선에서 소요 시간이 늘어나는 상황에 직면하고 있습니다. 이는 허난성, 산서성, 산시성, 쓰촨성, 구이저우성 등의 성들이 성 간 운송에 있어 터널이 다수 존재하는 도로 인프라에 크게 의존하고 있기 때문에 중요한 문제가 되고 있습니다. 경로가 제한되거나 통행 가능 시간대가 좁아지면, 영향을 받은 차선에서는 하류에 위치한 화학제품 사용자들이 요구하는 '저스트 인 타임' 배송 주기를 유지할 수 없게 됩니다. 2026년 2월에 도입된 교통운수부의 개정 “위험물 도로 운송 규정”에 따라, 위성 감시를 통한 경로 준수 관리가 강화되었습니다. 이로 인해 노선 이탈에 대한 벌칙이 강화되면서, 통합된 차량 관리 시스템을 갖추지 못한 중소규모 운송업체의 비용 부담이 커지고 있습니다. 많은 중소규모 도로 운송 사업자들은 대형 운송 회사와 같은 속도로 신기술을 도입하거나 규정 준수 비용을 감당할 수 없기 때문에 이러한 비용 압박은 업계 재편을 가속화할 가능성이 있습니다. 따라서 중국의 화학제품 물류 시장에서는 화주 수요가, 안전한 우회 경로를 철저히 확보할 수 있음을 입증할 수 있는 업체나, 도로의 신뢰성이 떨어졌을 때 운송량을 다른 운송 수단으로 전환할 수 있는 업체로 점차 이동하고 있습니다.

부문별 분석

2025년, 운송 부문은 매출의 64.77%를 차지하며 중국 화학제품 물류 시장 규모에서 가장 큰 비중을 차지했습니다. 이러한 위상은 중국 화학제품 물류 시장이 자산 집약적이라는 특성을 반영한 것으로, 화학 물질 운송은 여전히 순수한 디지털 중개 모델이 아닌 탱크로리, 철도 화물차, 연안 유조선, 내륙 수로의 연계에 의존하고 있습니다. 도로 운송은 산업 클러스터 간 단거리 위험물 운송에 있어 경로 설정의 유연성을 제공하기 때문에 여전히 지역 내 운송의 주요 수단으로 자리 잡고 있습니다. 해운 및 내륙 수로는 대량 화물의 지방 간 운송을 주로 담당하고 있으며, 우한 석유화학 터미널은 연간 355만 톤의 처리 능력을 갖추고 있어 이 시스템의 중요한 공공 거점으로 자리 잡고 있습니다.

부가가치 서비스는 2031년까지 연평균 성장률(CAGR) 7.31%를 나타낼 것으로 예측되며, 이는 물류 기능 중 가장 빠른 성장 속도입니다. HOYER사가 2025년 11월 상하이의 코베스트로 통합 사업장에서 진행한 확장 공사가 그 이유를 보여줍니다. 해당 사이트에서는 자동 충전, 온도 관리 창고, 24시간 감시 체계를 규제 준수가 요구되는 단일 서비스 모델로 통합하고 있기 때문입니다. 중국의 화학제품 물류 시장에서 이러한 성장 추세는 단순한 운송뿐만 아니라, 외주화를 통한 배합 지원, 공장 내 업무 및 서류 작성 위주의 서비스에 대한 지출 증가를 시사하고 있습니다.

2025년 기준으로 중국 화학물질 물류 시장의 66.5%를 위험 화학물질이 차지하고 있으며, 2031년까지의 예상 연평균 성장률(CAGR)은 6.19%로 가장 높은 성장세를 보이고 있습니다. 이 두 분야가 시장을 주도하고 있다는 사실은 중국 화학물류 시장이 여전히 가연성 액체, 부식성 물질, 반응성 제품 및 특수한 취급이 필요한 배터리 관련 소재를 중심으로 구성되어 있음을 보여줍니다. 새로운 규정 준수 환경은 이러한 경향을 더욱 강화하고 있습니다. 왜냐하면 위험물은 면허를 취득한 운송업체, 경로 관리, 그리고 보다 체계적인 추적 시스템이 없으면 운송할 수 없기 때문입니다. 2026년 5월부터 시행되는 중국의 “위험화학물질 안전법”는 위험 화학물질의 전체 수명 주기에 걸친 운영 기준을 강화함으로써 이러한 변화를 뒷받침하고 있습니다.

그 결과, 이미 디지털 관리 시스템이나 규제를 준수하는 자산을 보유한 사업자로 시장 점유율 이동이 가속화되고 있습니다. 부식성 물질에 대한 RFID 연계 관리는 검사 요건이 강화되고 있는 물류 거점 및 보관 환경에서 규율의 수준을 한층 더 높이고 있습니다. 비위험 화학물질은 여전히 중국 화학물질 물류 시장에서 큰 비중을 차지하고 있으며, 주로 베이스 폴리머, 비료, 식품용 화학 원료 등이 보다 광범위한 화물 기준에 따라 취급되고 있습니다. 그렇긴 하지만, 많은 화주들이 위험물 운송의 운영상 이점을 실감하고 추적성 도구를 광범위한 포트폴리오 전반으로 확대하고 있기 때문에 위험물과 비위험물의 서비스 품질 격차는 점차 좁혀지고 있습니다. 즉, 위험물 규제는 해당 부문 자체를 형성할 뿐만 아니라, 중국의 화학물질 물류 시장 전체에서 서비스에 대한 기대치도 높이고 있는 것입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측(금액, 2026-2031년)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the china chemical logistics market size is projected to be USD 130.72 billion in 2025, USD 136.47 billion in 2026, and reach USD 167.56 billion by 2031, growing at a CAGR of 4.19% from 2026 to 2031.

This report is Segmented by Service (Transportation, Warehousing and Distribution, and Value-Added Services), by Hazard Class (Hazardous and Non-Hazardous), by Temperature Control (Controlled and Non-Controlled), by End Use Industry (Pharmaceutical, Cosmetic, Specialty Chemicals, and More), and by Region (North, Northeast, East, and More). The Market Forecasts are Provided in Terms of Value (USD).

China Chemical Logistics Market Trends and Insights

Petrochemical Capacity West-To-East Shift Boosting Domestic Lane Volumes

The China chemical logistics market is being reshaped by the shift of petrochemical capacity from coastal clusters toward inland and western provinces. Coal-to-chemicals investments in Xinjiang, Ningxia, Shaanxi, and Sichuan are boosting long-haul domestic shipments of methanol, ethylene glycol, aromatics, and acetic acid. Existing East China logistics systems were built more around import and export flows, so they are less efficient for these inland-origin domestic lanes. The Jiangling Petrochemical Terminal at Wuhan Port is a direct response to that change because it adds a large public petrochemical node on the upper-middle Yangtze and connects more inland output with eastern demand centers. Hebei's 2025 push to prioritize 60 chemical projects worth CNY 201 billion (USD 27.8 billion) shows that inland chain extension is not limited to western China and is also building a northern vector for new freight demand. As that production map changes, the China chemical logistics market is placing a premium on operators that can combine river, rail, and road movements on a single service platform rather than rely solely on coastal port-based freight networks.

IMO 2026 Decarbonization Targets Forcing Fleet Renewal of Chemical Tankers

The China chemical logistics market is also being driven by a fleet renewal cycle tied to IMO decarbonization and vessel-efficiency standards. Guangzhou Shipyard International delivered the first of 4,74,500-dwt LR1 chemical and product tankers ahead of schedule in 2025, and the vessels met EEDI Phase 3 requirements while also reserving dual-fuel conversion capability. Nanjing Tanker Corporation also ordered 3 methanol-ready 6,600-dwt stainless steel chemical tankers in 2025, with delivery planned for the first half of 2028, indicating that owners are still committing capital despite a softer rate backdrop. SSY expected 46% of the global chemical tanker orderbook to deliver in 2026, suggesting near-term supply pressure may emerge before older tonnage leaves the fleet. COSCO SHIPPING Energy Transportation also ordered a 9,200-dwt stainless-steel chemical tanker in May 2025, reinforcing that domestic operators are still expanding specialized coastal capacity. The China chemical logistics market is therefore moving toward a structure in which decarbonization compliance and hazardous-cargo monitoring are increasingly handled through a single digital operating system rather than through separate regulatory workflows.

Tightened Tunnel Restrictions after the 2025 Guoliang Accident

The China chemical logistics market is facing longer route times on several hazardous road corridors after tighter tunnel controls followed the 2025 Guoliang incident. This matters because provinces such as Henan, Shanxi, Shaanxi, Sichuan, and Guizhou depend heavily on tunnel-rich road infrastructure for inter-provincial movement. When routes are restricted or time windows are narrowed, affected lanes can no longer support the same just-in-time delivery rhythm demanded by downstream chemical users. The Ministry of Transport's revised dangerous-goods road transport regulations, introduced in February 2026, strengthened satellite-monitored route compliance. It raised penalties for deviations, which increases the cost burden on smaller carriers without integrated fleet systems. That cost pressure is likely to accelerate consolidation, as many smaller road operators cannot absorb new technology and compliance costs at the same pace as larger fleets. The China chemical logistics market is therefore seeing shipper demand shift toward providers that can either prove safe rerouting discipline or switch volumes to other modes when roads become less reliable.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce Demand for Specialty Packaging Chemicals (Inks, Coatings, Adhesives)

- Growth of Lithium-Ion Battery Recycling Clusters in Southwest China

- Rail-Tank-Wagon Shortage Because of Steel Capacity Curbs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation accounted for 64.77% of revenue in 2025, making it the largest component of the China chemical logistics market size. That position reflects the asset-heavy nature of the China chemical logistics market, where chemical movement still depends on tank trucks, rail wagons, coastal tankers, and inland waterway links rather than on pure digital brokerage models. Road transport remains the key intra-regional mode because it offers routing flexibility for short-haul dangerous goods movements across industrial clusters. Sea and inland waterways handle much of the higher-volume inter-provincial flow, and the Wuhan petrochemical terminal adds a meaningful public node to that system with 3.55 million tons of annual capacity.

Value-added services are forecast to grow at a 7.31% CAGR through 2031, which is the fastest pace among logistics functions. HOYER's November 2025 expansion at the Covestro Integrated Site in Shanghai shows why, because the site combines automated filling, temperature-controlled warehousing, and round-the-clock monitoring into one compliance-heavy service model. In the China chemical logistics market, that growth path points to higher spending on outsourced blending support, in-plant operations, and documentation-intensive services rather than on transport alone.

Hazardous chemicals accounted for 66.5% of the China chemical logistics market in 2025 and posted the fastest projected CAGR of 6.19% through 2031. This dual lead shows that the China chemical logistics market remains centered on flammable liquids, corrosives, reactive products, and battery-related materials that require specialized handling. The new compliance environment strengthens that position because hazardous cargo cannot move without licensed carriers, route controls, and more structured traceability. China's Hazardous Chemicals Safety Law, effective from May 2026, is reinforcing that shift by raising operating standards across the hazardous chemical lifecycle.

The result is faster share migration toward operators that already have digital control systems and compliant assets. RFID-linked management for corrosives is adding another layer of discipline in parks and storage environments where inspection requirements are rising. Non-hazardous chemicals still account for a substantial share of the China chemical logistics market, mainly through base polymers, fertilizers, and food-grade chemical ingredients, which are handled under broader freight standards. Even so, the distinction between hazardous and non-hazardous service quality is narrowing, as many shippers are extending traceability tools across their broader portfolios after seeing the operational benefits of hazardous cargo. That means hazardous regulation is not only shaping its own segment, but also lifting service expectations across the wider China chemical logistics market.

Complete Report Scope:

- By Logistics Function

- Transportation

- Road

- Air

- Sea and Inland Waterways

- Rail

- Warehousing, Distribution and Inventory Management

- Value-added Services and Others

- Transportation

- By Hazard Class

- Hazardous Chemicals

- Non-hazardous Chemicals

- By Temperature Control

- Temperature-Controlled (Refrigerated/Heated)

- Non-Temperature-Controlled

- By End Use Industry

- Pharmaceutical

- Cosmetic

- Oil and Gas

- Specialty Chemicals

- Other End-Users

- By Region

- North

- Northeast

- East

- Central

- South

- Southwest

- Northwest

List of Companies Covered in this Report:

- Sinotrans Limited

- Sinochem Logistics

- Milkyway Chemical Supply Chain Service Co., Ltd.

- Yongtaiyun Chemical Logistics

- China COSCO Shipping Logistics

- China Railway Special Cargo Logistics

- Xiamen Xiangyu Group

- Shanghai Huayi Group Logistics

- Oriental Logistics Group

- Stolt Tank Containers

- HOYER Group

- Bertschi Group

- Leschaco China

- Sinopec Chemical Commercial Holding

- China National Chemical Engineering Logistics

- CIMC ENRIC Logistics

- SF Supply Chain

- CEVA Logistics China

- DHL Supply Chain China

- Shanghai Chemical Industrial Logistics (SCIL)

- Kerry Logistics Network Ltd.

- Den Hartogh Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview & Role of Logistics in Chemical

- 4.2 Chemical Industry Spending Trends

- 4.3 Market Drivers

- 4.3.1 Sino-EU Dangerous-Goods Transport Accords Easing Cross-Border Compliance

- 4.3.2 Petrochemical Capacity West-To-East Shift Boosting Domestic Lane Volumes

- 4.3.3 E-Commerce Demand for Specialty Packaging Chemicals (Inks, Coatings, Adhesives)

- 4.3.4 IMO 2026 Decarbonization Targets Forcing Fleet Renewal of Chemical Tankers

- 4.3.5 Beijing-Tianjin-Hebei "Haz-Chem One-Permit" Pilot Reducing Administrative Costs

- 4.3.6 Growth of Lithium-Ion Battery Recycling Clusters in Southwest China

- 4.4 Market Restraints

- 4.4.1 Tightened Tunnel Restrictions after 2025 Guoliang Accident

- 4.4.2 Rail-Tank-Wagon Shortage Because of Steel Capacity Curbs

- 4.4.3 Mandatory RFID Tracking for Class-8 Corrosives Raising Compliance Cost

- 4.4.4 Rising Coastal Port Congestion Surcharges for IMO Type II Cargoes

- 4.5 Regulatory Framework

- 4.6 Value Chain and Distribution Channel Architecture Analysis

- 4.7 Technology Innovations Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Rivalry Among Competitors

- 4.9 Evolution of Chemical Logistics Requirements

- 4.10 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size & Growth Forecasts (Value, 2026-2031)

- 5.1 By Logistics Function

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Air

- 5.1.1.3 Sea and Inland Waterways

- 5.1.1.4 Rail

- 5.1.2 Warehousing, Distribution and Inventory Management

- 5.1.3 Value-added Services and Others

- 5.1.1 Transportation

- 5.2 By Hazard Class

- 5.2.1 Hazardous Chemicals

- 5.2.2 Non-hazardous Chemicals

- 5.3 By Temperature Control

- 5.3.1 Temperature-Controlled (Refrigerated/Heated)

- 5.3.2 Non-Temperature-Controlled

- 5.4 By End Use Industry

- 5.4.1 Pharmaceutical

- 5.4.2 Cosmetic

- 5.4.3 Oil and Gas

- 5.4.4 Specialty Chemicals

- 5.4.5 Other End-Users

- 5.5 By Region

- 5.5.1 North

- 5.5.2 Northeast

- 5.5.3 East

- 5.5.4 Central

- 5.5.5 South

- 5.5.6 Southwest

- 5.5.7 Northwest

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Sinotrans Limited

- 6.4.2 Sinochem Logistics

- 6.4.3 Milkyway Chemical Supply Chain Service Co., Ltd.

- 6.4.4 Yongtaiyun Chemical Logistics

- 6.4.5 China COSCO Shipping Logistics

- 6.4.6 China Railway Special Cargo Logistics

- 6.4.7 Xiamen Xiangyu Group

- 6.4.8 Shanghai Huayi Group Logistics

- 6.4.9 Oriental Logistics Group

- 6.4.10 Stolt Tank Containers

- 6.4.11 HOYER Group

- 6.4.12 Bertschi Group

- 6.4.13 Leschaco China

- 6.4.14 Sinopec Chemical Commercial Holding

- 6.4.15 China National Chemical Engineering Logistics

- 6.4.16 CIMC ENRIC Logistics

- 6.4.17 SF Supply Chain

- 6.4.18 CEVA Logistics China

- 6.4.19 DHL Supply Chain China

- 6.4.20 Shanghai Chemical Industrial Logistics (SCIL)

- 6.4.21 Kerry Logistics Network Ltd.

- 6.4.22 Den Hartogh Logistics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment