|

시장보고서

상품코드

2073103

그린 IT 자산관리(ITAM) 소프트웨어 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Green IT Asset Management (ITAM) Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

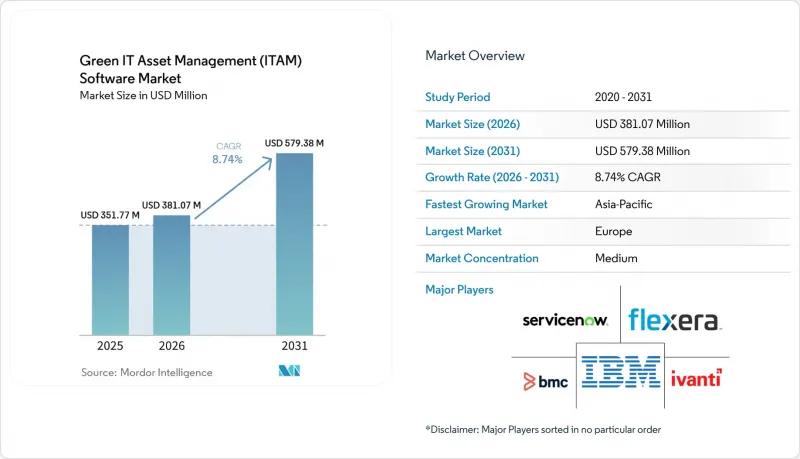

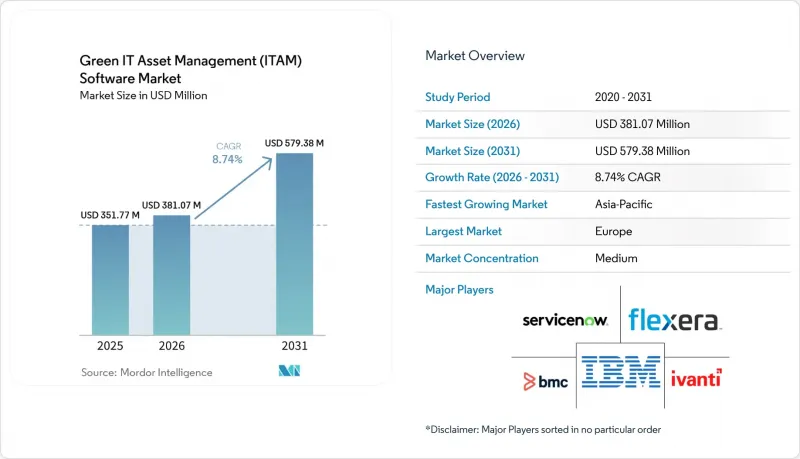

Mordor Intelligence에 의하면, 그린 IT 자산관리(ITAM) 소프트웨어 시장 규모는 2025년 3억 5,177만 달러에서 2026년에는 3억 8,107만 달러로 확대되어 2031년까지 5억 7,938만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 8.74%로 성장할 전망입니다.

본 보고서는 제공 형태(소프트웨어 및 서비스), 도입 형태(클라우드, On-Premise, 하이브리드), 기업 규모(대기업 및 중소기업), 최종 이용 산업(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 산업 제조, 에너지 및 유틸리티 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 그린 IT 자산 관리(ITAM) 소프트웨어 시장 동향과 인사이트

ESG와 관련된 IT 탄소 회계 요건

지속가능성 보고 의무화로 인해 그린 IT 자산 관리(ITAM) 소프트웨어 시장은 단순한 비용 관리의 범위를 넘어, 규정 준수 기반으로서 그 위상이 변화하고 있습니다. 기업은 보다 광범위한 환경 보고 요건에 대응하기 위해 하드웨어 자산, SaaS 구독, 사용 패턴, 갱신 주기 및 재사용 활동에 대해 보다 명확한 기록을 유지해야 합니다. 정적 스프레드시트는 규제 대상 기관이 현재 내부 보고 시스템에 기대하는 수준의 자산 연속성을 제공하지 못하기 때문에 이 작업에는 더 이상 적합하지 않습니다. Alliance Green IT는 2025년 보고서에서 조직의 47%가 이미 환경 목표를 지원하기 위해 ITAM 프로세스를 활용하고 있다고 밝혔으며, 이는 도입이 더욱 확대되기 전부터 환경 관련 활용 사례가 이미 주류로 자리 잡아가고 있었음을 보여줍니다. 또한 GLPI는 2025년에 탄소를 중심으로 한 자산 수명 주기 관리의 역할이 커지고 있음을 강조했습니다. 이는 재고 관리와 환경 측정을 결합한 플랫폼으로의 전환을 촉진하는 것입니다. 이에 따라 그린 IT 자산 관리(ITAM) 소프트웨어 시장에서는 단순한 라이선스 대조에만 그치지 않고, 신뢰할 수 있는 디바이스 수준의 기록과 확실한 라이프사이클 워크플로우를 입증할 수 있는 벤더에 대한 수요가 높아지고 있습니다.

AI를 활용한 자산 감지 및 라이선싱 최적화

AI는 그린 IT 자산 관리(ITAM) 소프트웨어 시장의 운영 모델을 변화시키고 있습니다. 이는 수동 방식의 자산 거버넌스만으로는 현대 소프트웨어 자산의 규모를 따라잡을 수 없기 때문입니다. Flexera는 2025년의 "ITAM의 현황" 보고서는 해당 회사의 Technopedia 카탈로그가 210만 건 이상의 소프트웨어 사용권을 포괄하고 있다고 밝히며, 기업 내 자산 감지 및 표준화 과정에서 발생하는 인식 부담의 규모를 부각시켰습니다. Xensam은 2024년 12월, 자사의 용도 라이브러리가 50만 개에 달했으며, 인식된 SaaS 용도이 전년 대비 50% 증가했다고 보고했는데, 이는 소프트웨어 가시화에 대한 수요가 얼마나 급속히 확대되고 있는지를 반영하고 있습니다. 또한 Flexera의 조사에 따르면, 2025년에 자사의 IT 자산을 완벽하게 파악하고 있다고 확신하는 기업은 43%에 그쳐, 전년도의 47%에서 감소했습니다. 이는 복잡성이 여전히 많은 팀이 기존 방식으로 모니터링할 수 있는 속도를 능가하는 속도로 증가하고 있음을 보여줍니다. 그 결과, 그린 IT 자산 관리(ITAM) 소프트웨어 시장에서는 AI 기반의 감지 기능이 더욱 중요시되고 있습니다. 이는 수작업의 부담을 줄이면서, 승인되지 않은 용도, 미사용 라이선스 및 섀도 AI 활동을 파악할 수 있기 때문입니다. 이러한 변화로 인해 AI 네이티브 벤더들은 더 높은 가격 책정을 정당화할 수 있게 되었습니다. 왜냐하면 구매자들은 현재 자동 감지 기능을 프리미엄 기능이 아닌 기본적인 운영 요건으로 여기고 있기 때문입니다.

자산 데이터의 품질 저하로 인해 보고서의 정확도가 제한됨

그린 IT 자산 관리(ITAM) 소프트웨어 시장에서 가장 큰 운영상의 과제는 여전히 자산 데이터의 품질이 낮다는 점입니다. Lansweeper사는 2025년에 역동적인 환경에서는 수동 기록이 금세 신뢰성을 잃게 되며, 시간이 지남에 따라 라이프사이클, 이용 현황, 규정 준수 관련 기록의 정확도가 떨어지기 때문에 자동 인벤토리가 중요하다고 지적했습니다. 조달 시스템, CMDB 도구, 엔드포인트 기록 간의 명칭 불일치는 여전히 기록 중복이나 제조업체 식별 정보의 불일치를 초래하고 있으며, 그 결과 탄소 귀속 분석 및 라이선스 현황 파악이 어려워지고 있습니다. 이 문제는 기업이 에너지, 디바이스, 클라우드 데이터를 공식적인 지속가능성 보고서에 연계하려고 할 때 더욱 심각해집니다. 따라서 그린 IT 자산 관리(ITAM) 소프트웨어 시장은 여전히 강력한 정상화 엔진에 의존하고 있습니다. 왜냐하면, 그것들이 없다면 디스커버리의 포괄성이 아무리 뛰어나더라도 보고에 적합한 결과를 얻을 수 없기 때문입니다.

부문별 분석

서비스 분야는 2026년부터 2031년까지 연평균 성장률(CAGR) 11.19%로 확대될 것으로 예상되며, 그린 IT 자산 관리(ITAM) 소프트웨어 시장에서 가장 두드러진 성장을 보일 것으로 전망됩니다. 이러한 성장은 멀티 환경의 전체 자산에 걸친 데이터 정규화, 디스커버리 설계, 워크플로 설정 및 지속적인 최적화와 관련된 업무 부하 증가를 반영하고 있습니다. 기업들은 AI의 기능 강화만으로는 도입에 드는 노력을 줄일 수 없다는 사실을 깨닫기 시작하고 있습니다. 왜냐하면 AI는 여전히 적절한 통합, 규칙 조정 및 정책 설계에 의존하고 있기 때문입니다. 또한, ITAM, SaaS 관리 및 지출 거버넌스를 단일 운영 프레임워크로 통합하려는 구매자가 늘어나면서 서비스에 대한 수요도 증가하고 있습니다. 이에 따라 도입 파트너나 벤더 주도의 서비스 팀은 기업 내 도입 과정에서 더 큰 역할을 담당하게 되었습니다.

2025년, 소프트웨어는 매출 점유율의 77.96%를 차지하며 그린 IT 자산 관리(ITAM) 소프트웨어 시장의 상업적 기반이 되었습니다. 구매자들은 여전히 정기적인 검토 업무보다 지속적이고 실시간으로 운영되는 디스커버리 플랫폼을 선호하고 있습니다. 이는 플랫폼 모델이 정식 평가 기간 사이에 발생하는 가시성의 공백을 메우기 위함입니다. FinOps Foundation과 ITAM Forum은 2025년 6월, 워킹그룹을 구성하고, 행사 세션을 공동 개최하며, 또한 'SaaS를 위한 FinOps' 교육 과정 제공을 포함한 전략적 파트너십을 발표했습니다. 이는 통합형 도입을 둘러싼 보다 광범위한 서비스 생태계의 부상을 뒷받침하는 것입니다. 조달 팀이 도입 성과에 대한 명확한 책임 소재를 요구하고 있기 때문에 소프트웨어에 체계적인 온보딩 및 관리형 최적화 기능을 결합한 공급업체는 중견 기업 시장에서 사업을 더욱 확대할 가능성이 높을 것으로 보입니다. 따라서 그린 IT 자산 관리(ITAM) 소프트웨어 업계에서는 소프트웨어를 수익의 기반층으로 유지하면서, 서비스를 통해 고객 가치를 확대하고 실행 위험을 줄이고 있습니다.

하이브리드 모델은 2026년부터 2031년까지 연평균 성장률(CAGR) 12.13%를 나타낼 것으로 예측되며, 그린 IT 자산 관리(ITAM) 소프트웨어 시장에서 가장 빠르게 성장하는 모델이 될 전망입니다. 이러한 경향은 조직이 여전히 보안, 주권, 인프라 상황에 따라 서로 다른 운영 모델을 필요로 하고 있다는 점에서 엔터프라이즈 아키텍처가 표준화가 아닌 공존을 통해 형성되고 있음을 보여줍니다. 하이브리드 설계를 통해 기업은 통제된 환경에서 On-Premise 자산 탐색을 유지하면서, 클라우드 서비스를 통해 분석 및 보고 기능을 확장함으로써 보다 광범위한 거버넌스를 실현할 수 있습니다. 이 구조는 모든 워크로드와 자산 범주를 단일 환경으로 이전할 수 없는 전 세계 기업에 적합합니다. 또한, 클라우드와 On-Premise의 기록을 통합하여 해석할 수 있도록 함으로써 자산 인텔리전스의 가치를 높입니다.

2025년 그린 IT 자산 관리(ITAM) 소프트웨어 시장에서 클라우드가 62.03%를 차지했습니다. 이는 구매자들이 SaaS 방식으로 제공되는 자산 탐색 기능과 보다 신속한 기능 업데이트를 선호하고 있음을 뒷받침합니다. 또한, 클라우드의 대규모 특성은 인프라 오버헤드가 적고, 분산된 팀이 관리하기 쉽다는 장점도 반영하고 있습니다. 한편, 은행, 정부, 국방 분야에서는 데이터 주권 및 에어갭 환경으로 인해 외부 텔레메트리 모델의 활용이 제한되고 있으므로, On-Premise 구축의 중요성은 여전히 높습니다. Flexera는 2025년 보고서에서 클라우드 환경에서의 “BYOL(Bring-Your-Own-License)에 대한 상황에 대해, 유의미한 가시성을 확보하고 있는 기업은 고작 27%에 불과하다고 지적하고 있으며, 이것이 하이브리드 거버넌스가 여전히 주요 구매 요건으로 남아 있는 이유 중 하나입니다. 따라서 그린 IT 자산 관리(ITAM) 소프트웨어 업계는 서로 분리된 도구들로 관리하는 방식에서 벗어나, 클라우드 사용 현황, 라이선스 권한 기록, 엔드포인트 데이터를 단일 거버넌스 계층으로 통합하는 도입 모델로 전환하고 있습니다.

지역별 분석

2025년, 북미는 그린 IT 자산 관리(ITAM) 소프트웨어 시장 점유율의 37.02%를 차지하며, 지역별로는 가장 큰 기여를 한 지역이 되었습니다. 미국은 기업의 디지털화가 깊이 뿌리내리고 있으며, FinOps의 실천이 성숙 단계에 이르렀고, 또한 소프트웨어 감사 활동이 명확한 투자 수익률(ROI)을 뒷받침할 만한 충분한 수준을 유지하고 있기 때문에 여전히 수요의 중심지입니다. Flexera는 2025년 보고서에서 Microsoft, IBM, SAP가 감사 프로그램을 주도하고 있으며, 조사 대상 조직의 각각 50%, 37%, 32%에 달한다고 보고했으며, 이는 해당 지역에서 예방적 자산 거버넌스가 여전히 상업적으로 매력적인 이유를 설명해 줍니다. 캐나다에서는 공공 부문의 디지털 현대화를 통해 수요가 확대되고 있으며, 멕시코에서는 니어쇼어링을 주도하는 기업 IT 확장의 혜택을 누리고 있습니다. 이러한 상황으로 인해 북미는 그린 IT 자산 관리(ITAM) 소프트웨어 시장에서 여전히 가장 성숙한 지역으로 자리매김하고 있습니다.

유럽은 지속가능성 보고에 대한 수요가 IT 거버넌스와 환경적 책임성을 더욱 밀접하게 연결하고 있기 때문에 그린 IT 자산 관리(ITAM) 소프트웨어 시장에서 여전히 핵심 지역으로 자리 잡고 있습니다. 대기업의 경우, 보다 광범위한 공시 체계 속에서 스코프 3 측정, 수명 주기에 관한 증거, 그리고 보다 엄격한 하드웨어 관리를 지원할 수 있는 자산 기록에 대한 필요성이 높아지고 있습니다. 얼라이언스 그린 IT의 2025년 조사에 따르면, 조직의 47%가 이미 환경 목표 달성을 지원하기 위해 ITAM 프로세스를 활용하고 있으며, 이는 다른 많은 지역에 비해 환경 측면에서의 활용 사례가 더욱 확고함을 보여줍니다. 이로 인해 유럽은 탄소 배출에 대한 인식이 높은 수명 주기 관리 및 관련 업무 프로세스의 도입에 있어 가장 중요한 지역 중 하나가 되었습니다.

아시아태평양의 그린 IT 자산 관리(ITAM) 소프트웨어 시장은 2026년부터 2031년까지 연평균 성장률(CAGR) 12.92%로 확대될 것으로 예상되며, 지역별 부문 중 가장 빠른 성장세를 보일 전망입니다. 중국, 인도, 일본, 한국, 호주의 각 조직에서는 급속한 클라우드 전환과 소프트웨어 포트폴리오의 확대에 따라, 더욱 복잡해진 하이브리드 환경의 관리가 진행되고 있습니다. 특히 인도에서는 대형 IT 서비스 기업과 세계 역량 센터들이 클라우드 네이티브 워크로드와 대규모 SAP 및 Oracle 환경을 보다 적절하게 관리해야 할 필요성으로 인해 시장이 활성화되고 있습니다. 또한 일본에서도 디지털 전환(DX) 프로그램의 일환으로 기업의 클라우드 도입이 확대됨에 따라 신규 도입 기회가 늘어나고 있습니다. ServiceNow와 Lenovo는 2026년 5월, 호주, 뉴질랜드, 홍콩, 싱가포르, 아일랜드를 대상으로 한 전략적 제휴 확대를 발표했습니다. 이는 공급업체가 국제적인 기업 고객을 대상으로 지역에 특화된 사업 모델을 구축해 나가고 있음을 보여줍니다. 남미에서는 브라질이 주도적인 역할을 하고 있으며, 지속가능성 대응 및 SaaS 도입이 수요를 뒷받침하고 있습니다. 중동 및 아프리카는 아직 규모는 작지만 지속적으로 성장하고 있으며, 사우디아라비아와 아랍에미리트가 국가 차원의 디지털화 프로그램 및 기업 기술 거버넌스에 대한 투자 강화를 통해 주도적인 역할을 수행하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the green IT asset management (ITAM) software market size is expected to increase from USD 351.77 million in 2025 to USD 381.07 million in 2026 and reach USD 579.38 million by 2031, growing at a CAGR of 8.74% over 2026-2031.

This report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-Use Industry (IT and Telecom, BFSI, Industrial Manufacturing, Energy and Utilities, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Green IT Asset Management (ITAM) Software Market Trends and Insights

ESG-Linked IT Carbon Accounting Requirements

Mandatory sustainability reporting has moved the Green IT Asset Management (ITAM) Software Market closer to compliance infrastructure than simple cost control. Enterprises are being asked to maintain clearer records on hardware fleets, SaaS subscriptions, utilization patterns, refresh cycles, and reuse activity when they support broader environmental reporting. Static spreadsheets are no longer enough for that task because they cannot provide the asset-level continuity that regulated organizations now expect from internal reporting systems. Alliance Green IT reported in 2025 that 47% of organizations already used ITAM processes to support ecological objectives, indicating that environmental use cases were becoming mainstream before adoption widened further. GLPI also highlighted the growing role of carbon-focused asset lifecycle management in 2025, which supports the direction toward platforms that combine inventory control with environmental measurement. This is pushing the Green IT Asset Management (ITAM) Software Market toward vendors that can demonstrate reliable device-level records and credible lifecycle workflows, rather than just license reconciliation.

AI-Driven Asset Discovery and License Optimization

AI is changing the operating model of the Green IT Asset Management (ITAM) Software Market because manual asset governance can no longer keep pace with modern software estates. Flexera stated in its 2025 State of ITAM Report that its Technopedia catalog covered more than 2.1 million software use rights, underscoring the scale of the recognition burden for enterprise discovery and normalization. Xensam reported in December 2024 that its application library had reached 500,000 titles, including a 50% year-over-year increase in recognized SaaS applications, reflecting how quickly software visibility needs are expanding. Flexera also found that only 43% of enterprises felt confident in complete IT estate visibility in 2025, down from 47% the prior year, indicating that complexity is still growing faster than many teams can monitor with traditional methods. As a result, the Green IT Asset Management (ITAM) Software Market is placing greater emphasis on AI-led discovery, as it can surface unauthorized applications, idle licenses, and shadow AI activity with less manual effort. That shift is helping AI-native vendors justify higher pricing because buyers now see automated discovery as a basic operating requirement rather than a premium feature.

Poor Asset Data Quality Limits Reporting Accuracy

The largest operating challenge in the Green IT Asset Management (ITAM) Software Market is still poor asset data quality. Lansweeper noted in 2025 that automated inventory is important because manual records quickly lose reliability in dynamic environments, weakening lifecycle, utilization, and compliance records over time. Naming gaps across procurement systems, CMDB tools, and endpoint records still result in duplicate records and inconsistent manufacturer identities, which in turn weaken carbon attribution and license positions. That problem becomes more serious when firms try to connect energy, device, and cloud data to formal sustainability reporting. The Green IT Asset Management (ITAM) Software Market, therefore, still depends on strong normalization engines, because without them, even good discovery coverage does not produce reporting-grade output.

Other drivers and restraints analyzed in the detailed report include:

- Rising Software and SaaS Waste Reduction Mandates

- Hybrid Cloud and Multi-Environment Visibility Needs

- Complex Integrations Delay Value Realization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services are projected to expand at a 11.19% CAGR from 2026 to 2031, making it the fastest-growing segment within the Green IT Asset Management (ITAM) Software Market. That growth reflects the rising workload tied to data normalization, discovery design, workflow configuration, and ongoing optimization across multi-environment estates. Enterprises are finding that stronger AI capabilities do not, by themselves, reduce deployment effort, because AI still depends on clean integrations, rule tuning, and policy design. Service demand is also rising as more buyers seek to combine ITAM, SaaS management, and spend governance into a single operating framework. This is giving implementation partners and vendor-led service teams a larger role in enterprise rollouts.

Software held a 77.96% revenue share in 2025, making it the commercial anchor of the Green IT Asset Management (ITAM) Software Market. Buyers still prefer continuous, real-time discovery platforms over periodic review engagements because the platform model closes visibility gaps between formal assessments. The FinOps Foundation and ITAM Forum announced a strategic partnership in June 2025 that included working groups, shared event tracks, and a FinOps for SaaS training course, which supports the rise of a broader service ecosystem around converged deployments. Vendors that bundle software with structured onboarding and managed optimization are likely to win more mid-market business because procurement teams want clearer ownership over implementation outcomes. The Green IT Asset Management (ITAM) Software Industry is therefore keeping software as the base revenue layer while services expand account value and reduce execution risk.

Hybrid deployment is projected to grow at a 12.13% CAGR from 2026 to 2031, making it the fastest-growing deployment model in the Green IT Asset Management (ITAM) Software Market. This pattern shows that enterprise architecture is being shaped by coexistence rather than standardization, as organizations still need different operating models across varying security, sovereignty, and infrastructure conditions. Hybrid designs let companies keep on-premises discovery in controlled environments while extending analytics and reporting through cloud services for broader governance. That structure fits global organizations that cannot shift every workload or asset category into a single environment. It also enhances the value of asset intelligence by enabling the interpretation of cloud and on-premises records together.

Cloud accounted for 62.03% of the Green IT Asset Management (ITAM) Software Market in 2025, underscoring buyers' preference for SaaS-delivered discovery and faster feature updates. Cloud scale also reflects the appeal of lower infrastructure overhead and easier administration for distributed teams. On-premises deployments continue to matter in banking, government, and defense, where data sovereignty or air-gapped environments limit the use of external telemetry models. Flexera reported in 2025 that only 27% of enterprises had meaningful visibility into bring-your-own-license positions in cloud environments, which helps explain why hybrid governance remains a central buying requirement. The Green IT Asset Management (ITAM) Software Industry is therefore moving toward deployment models that integrate cloud usage, entitlement records, and endpoint data within a single governance layer rather than across isolated tools.

Complete Report Scope:

- By offering

- Software

- Services

- By Deployment Mode

- Cloud

- On-Premises

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By End-Use Industry

- IT and Telecom

- BFSI

- Industrial Manufacturing

- Energy and Utilities

- Oil and Gas

- Retail and E-Commerce

- Construction and Infrastructure

- Government and Public Sector

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Geography Analysis

North America held 37.02% of the Green IT Asset Management (ITAM) Software Market share in 2025, making it the largest regional contributor. The United States remains the center of demand because enterprise digitization is deep, FinOps practices are mature, and software audit activity remains high enough to support a clear return on investment. Flexera reported in 2025 that Microsoft, IBM, and SAP led audit programs reaching 50%, 37%, and 32% of surveyed organizations, which helps explain why proactive asset governance remains commercially attractive in the region. Canada is adding demand through public-sector digital modernization, while Mexico is benefiting from nearshoring-led enterprise IT expansion. These conditions keep North America the most mature region in the Green IT Asset Management (ITAM) Software Market.

Europe remains a core region for the Green IT Asset Management (ITAM) Software Market because sustainability reporting needs are pulling IT governance and environmental accountability closer together. Large enterprises increasingly need asset records that can support Scope 3 measurement, lifecycle evidence, and more disciplined hardware management inside broader disclosure frameworks. Alliance Green IT found in 2025 that 47% of organizations already used ITAM processes to support ecological objectives, which reflects a stronger environmental use case than in many other regions. This is making Europe one of the most important regions for carbon-aware lifecycle management and the adoption of related workflows.

The Asia-Pacific Green IT Asset Management (ITAM) Software Market is projected to expand at a 12.92% CAGR from 2026 to 2031, making it the fastest-growing regional segment. Organizations across China, India, Japan, South Korea, and Australia are managing more complex hybrid estates after rapid cloud migration and broader software portfolio growth. India is becoming especially active because large IT services firms and global capability centers need better control over cloud-native workloads and significant SAP and Oracle footprints. Japan is also opening more first-time deployment opportunities as enterprise cloud adoption expands under digital transformation programs. ServiceNow and Lenovo announced an expanded strategic agreement in May 2026 across Australia, New Zealand, Hong Kong, Singapore, and Ireland, which shows how vendors are building more region-specific operating models for international enterprise buyers. South America is led by Brazil, where sustainability alignment and SaaS adoption are supporting demand. The Middle East and Africa are expanding from a smaller base, with Saudi Arabia and the United Arab Emirates leading through national digitization programs and stronger investment in enterprise technology governance.

- Flexera Software LLC

- USU Software AG

- Lansweeper NV

- Matrix42 AG

- Certero Limited

- Belarc, Inc.

- Eracent, Inc.

- InvGate, LLC

- SysAid Technologies Ltd.

- Asset Panda, LLC

- Freshworks Inc.

- ManageEngine, Zoho Corporation Pvt. Ltd.

- Xensam AB

- ServiceNow, Inc.

- Ivanti, Inc.

- BMC Software, Inc.

- SolarWinds Worldwide, LLC.

- SaaSwedo

- OpenText Corporation

- IBM Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Software and SaaS Waste Reduction Mandates

- 4.2.2 ESG-Linked IT Carbon Accounting Requirements

- 4.2.3 Hybrid Cloud and Multi-Environment Visibility Needs

- 4.2.4 AI-Driven Asset Discovery and License Optimization

- 4.2.5 Software Audit Exposure and True-Up Avoidance Pressure

- 4.2.6 FinOps and SAM Convergence for Technology Spend Governance

- 4.3 Market Restraints

- 4.3.1 Poor IT Asset Data Quality and Normalization Gaps

- 4.3.2 Integration Complexity Across Legacy, Cloud, and SaaS Tools

- 4.3.3 Shortage of Skilled ITAM and Software Licensing Specialists

- 4.3.4 Privacy Concerns Around Continuous Endpoint and Telemetry Collection

- 4.4 Industry Value-Chain Analysis

- 4.4.1 Privacy Concerns Around Continuous Endpoint and Telemetry Collection

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By offering

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End-Use Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Industrial Manufacturing

- 5.4.4 Energy and Utilities

- 5.4.5 Oil and Gas

- 5.4.6 Retail and E-Commerce

- 5.4.7 Construction and Infrastructure

- 5.4.8 Government and Public Sector

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Flexera Software LLC

- 6.4.2 USU Software AG

- 6.4.3 Lansweeper NV

- 6.4.4 Matrix42 AG

- 6.4.5 Certero Limited

- 6.4.6 Belarc, Inc.

- 6.4.7 Eracent, Inc.

- 6.4.8 InvGate, LLC

- 6.4.9 SysAid Technologies Ltd.

- 6.4.10 Asset Panda, LLC

- 6.4.11 Freshworks Inc.

- 6.4.12 ManageEngine, Zoho Corporation Pvt. Ltd.

- 6.4.13 Xensam AB

- 6.4.14 ServiceNow, Inc.

- 6.4.15 Ivanti, Inc.

- 6.4.16 BMC Software, Inc.

- 6.4.17 SolarWinds Worldwide, LLC.

- 6.4.18 Saaswedo

- 6.4.19 OpenText Corporation

- 6.4.20 IBM Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment