|

시장보고서

상품코드

2073593

미국의 미량영양소 비료 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Micronutrient Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

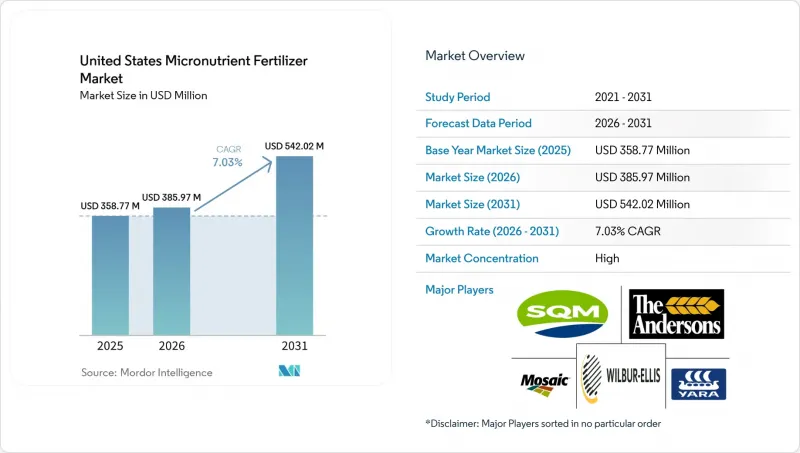

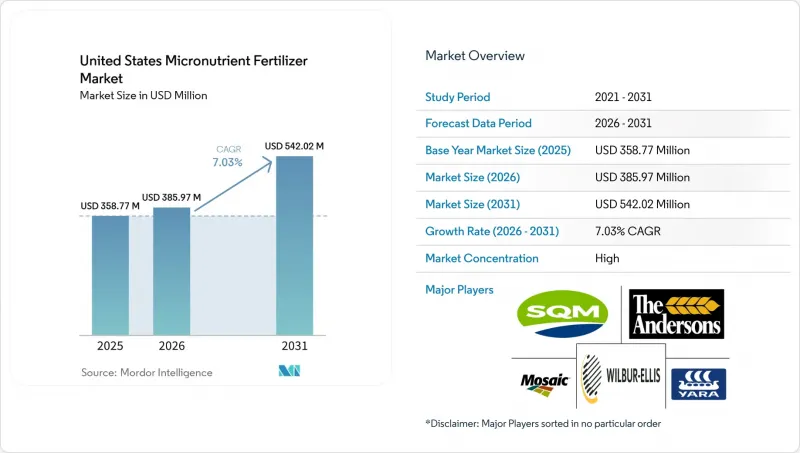

Mordor Intelligence에 의하면, 미국의 미량영양소 비료 시장 규모는 2025년 3억 5,877만 달러로 평가되었습니다. 2026년에는 3억 8,597만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 7.03%로 성장을 지속하여, 2031년까지 5억 4,202만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품별(붕소, 구리, 철, 망간, 몰리브덴, 아연, 기타), 형태별(기존 및 특수형), 시용 방법별(비료 관개, 엽면 시비, 토양 시비), 작물 유형별(밭작물, 원예작물, 잔디 및 관상용 작물)로 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(미터톤) 단위로 제시되어 있습니다.

미국의 미량영양소 비료 시장 동향 및 인사이트

정밀 시비를 통한 미량영양소 살포

가변 시비율에 대응하는 살포기 및 액체 주입 장치를 통해, 그리드 샘플링 및 수확량 지도를 통해 파악된 공간적 변동에 맞추어, 한 번의 작업으로 1에이커당 0.5-4파운드의 아연, 붕소 또는 혼합 패키지를 시비할 수 있게 되었습니다. 대학의 포장 실험에 따르면, 균일 시비에 비해 영양분 이용 효율이 15-25% 향상되고, 총 시비량도 감소하는 것으로 나타났습니다. 기기 제조업체들은 기존 기기에 미량영양소 모듈을 탑재함으로써 추가 비용을 절감하고, 미국의 미량영양소 비료 시장 전반에 걸친 보급을 가속화하고 있습니다. 소매 농업 전문가들은 데이터 레이어를 활용하여 미국 농무부(USDA)의 프로그램 및 탄소 등록 제도를 위한 환경적 이점을 문서화함으로써 농가의 입지를 더욱 공고히 하고 있습니다.

확인된 아연 및 붕소 결핍

토양 조사 결과에 따르면, 네브래스카주 동부 농지의 47%가 아연의 임계치를 밑돌고 있으며, 31%는 붕소도 부족한 것으로 나타났습니다. 수확량 증가, 인과의 경쟁 작용, 그리고 최소한의 경작으로 인해 이러한 결핍 위험은 더욱 높아지고 있습니다. 미국의 미량영양소 비료 시장이 3-4년 주기로 정기적인 엽면 및 토양 진단 방식으로 전환됨에 따라, 입상 황산아연, 붕산 및 킬레이트화 액제에 대한 수요가 증가하고 있습니다. 농업 전문가들의 추산에 따르면, 심각한 결핍을 해소함으로써 옥수수 수확량이 1에이커당 10-20부셸 증가하여, 미량영양소에 대한 1에이커당 15-25달러의 추가 비용을 쉽게 회수할 수 있다고 합니다.

N-P-K 비료와의 가격 차이

미량영양소의 시비와 기존 N-P-K 비료 간의 비용 차이는 수익률이 낮은 광대한 농지를 경영하는 농가에게 경제적 장벽이 되고 있습니다. 미량영양소가 혼합된 비료는 1에이커당 15-25달러가 드는 반면, N-P-K 비료는 8-12달러입니다. 줄기 작물의 이익률은 1에이커당 50-150달러 정도인 경우가 많기 때문에 명확한 수확량 증가가 입증되지 않는 한 생산자들은 도입을 주저하게 됩니다. 시험 결과에 따르면, 옥수수의 경우 1에이커당 3-5부셸(bu), 대두의 경우 1-2부셸(bu)의 수확량 증가만으로도 수익성이 확보되는 것으로 나타났으나, 토양 유형에 따라 결과는 제각각입니다. 이 때문에 미국에서는 미량영양소 비료가 명백히 결핍된 농지에 보급되는 데 제한이 따르고 있습니다.

부문별 분석

2025년, 아연은 미국의 미량영양소 비료 시장에서 31.5%라는 최대 점유율을 차지했습니다. 이는 고수확 재배 시스템에서 아연 결핍이 여전히 흔히 발생하는 옥수수, 대두, 밀의 생산 과정에서 아연이 널리 사용되고 있다는 사실에 기인합니다. 아연 결핍 토양이나 알칼리성 토양에서의 지속적인 수요에 더해, 높은 pH의 관개 조건까지 더해져 그 입지를 더욱 공고히 하고 있습니다. 구리도 또한 그 영양학적 이점과 옥수수, 대두, 특수 작물 생산에 있어 특정 작물 보호 프로그램에서 사용됨에 따라 중요한 제품 범주로 자리 잡고 있습니다. 한편, 붕소는 적용 범위가 비교적 좁음에도 불구하고, 결핍이 발생하기 쉬운 지역에서 계속해서 주목을 받고 있습니다.

몰리브덴은 규모는 작지만, 2031년까지 연평균 성장률(CAGR)이 7.3%를 나타낼 것으로 예측되는 가장 빠르게 성장하고 있는 제품 카테고리입니다. 이러한 성장은 특히 콩과 작물의 생산 시스템에서 생물학적 질소 고정 및 질소 이용 효율에 대한 관심이 높아지고 있는 데 기인합니다. 서방형 영양소 공급 특성을 지닌, 기계화학적 방법으로 개질된 Mo-Zn 복합재료에 대한 지속적인 연구는 이 분야의 향후 제품 혁신을 뒷받침할 가능성이 있습니다. 또한, 2세대 킬레이트제 및 건조 분산성 분말 제제의 발전으로 인해 석회질 토양에서의 성능이 향상되어, 프리미엄 가격 책정의 기회가 생겨나고 있습니다. 캘리포니아주의 특산 작물 생산자들은 점적 관개와 항공 살포 모두에서 탱크 내 안정성이 뛰어난 혼합물을 선호하며, 여러 미량영양소를 조합한 시비 프로그램을 점점 더 많이 도입하고 있는데, 이것이 미량영양소 시장의 추가적인 성장을 뒷받침하고 있습니다.

기존의 황산염, 산화물 및 염기성 염은 저렴한 비용과 폭넓은 입수 가능성 덕분에 2025년 미국의 미량영양소 비료 시장 규모의 76.3%를 차지했습니다. 지배적인 위치를 차지하고 있음에도 불구하고, 특수 형태의 제품은 2031년까지 연평균 성장률(CAGR) 6.6%를 기록하며 성장하고 있습니다. 액상 제제는 제초제와 병용하여 균일하고 가변적인 비율로 시용할 수 있게 해주는 반면, 서방형 코팅은 용출 및 토양 내 고착을 줄여줍니다. 이는 모래 토양이 많은 플로리다주의 감귤 과수원에서 매우 중요합니다. 수용성 분말은 원예 및 잔디 관리에서 엽면 흡수를 촉진합니다. 현장 실증 결과에 따르면, 특히 탄소 배출 감축 프로그램이 효율성 향상을 통한 부가가치를 인정하는 경우, 수확량 증가와 물류 간소화가 가격 프리미엄을 상쇄하는 것으로 나타났습니다.

폴리머 코팅 및 나노캡슐화 기술의 발전이 차별화를 촉진하고 있으며, 공급업체들은 기초적인 범용 제품을 넘어선 이익률 확대를 목표로 하고 있습니다. 시장을 선도하는 기업들의 독자적인 화학 기술에 대한 투자는 특수 제품 분야로의 전략적 전환을 보여주고 있으며, 이를 통해 미국의 미량영양소 비료 산업 전반의 고도화가 진행되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 보고서의 내용

제3장 주요 요약 및 주요 조사 결과

제4장 주요 업계 동향

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 비료 업계 CEO가 직면하는 중요 전략적 과제

KTHAccording to Mordor Intelligence, the united states micronutrient fertilizer market size is projected to grow from USD 358.77 million in 2025 to USD 385.97 million in 2026 and is forecast to reach USD 542.02 million by 2031 at 7.03% CAGR over 2026-2031.

This report is Segmented by Product (Boron, Copper, Iron, Manganese, Molybdenum, Zinc, Others), Form (Conventional and Specialty), Application Mode (Fertigation, Foliar, Soil), and Crop Type (Field Crops, Horticultural Crops, Turf & Ornamental). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

United States Micronutrient Fertilizer Market Trends and Insights

Precision-Rate Micronutrient Application

Variable-rate spreaders and liquid injectors now deliver zinc, boron, or blended packages at 0.5-4 lb per acre within a single pass, matching spatial variability identified through grid sampling and yield maps. University field trials show 15-25% higher nutrient-use efficiency and lower total applied pounds relative to uniform rates. Equipment makers bundle micronutrient modules into existing hardware, cutting incremental costs and accelerating adoption across the United States micronutrient fertilizers market. Retail agronomists leverage the data layer to document environmental benefits for USDA programs and carbon registries, further strengthening farmers.

Documented zinc and boron shortages

Soil surveys reveal 47% of eastern Nebraska fields below critical zinc thresholds, with 31% also lacking boron. Higher yields, phosphorus antagonism, and minimal tillage intensify the risks of shortages. As the United States micronutrient fertilizers market pivots toward routine tissue and soil diagnostics every three to four years, demand for granular zinc sulfate, boric acid, and chelated liquids rises. Agronomists calculate that correcting severe deficiencies can add 10-20 bushels per acre in corn, easily covering an extra USD 15-25 per-acre expenditure on micronutrients.

Price premium versus N-P-K

The cost differential between micronutrient applications and traditional N-P-K fertilizers creates economic resistance among broad-acre farmers operating on thin profit margins. Micronutrient blends cost USD 15-25 per acre, compared to USD 8-12 for N-P-K. With row-crop margins often ranging from USD 50 to USD 150 per acre, growers hesitate unless a clear yield improvement is proven. Trials indicate a break-even point at 3-5 bushels per acre (bu) corn or 1-2 bushels per acre (bu) soybean yield gains, with results not uniform across soil types . This restraint limits the penetration of United States micronutrient fertilizers into clearly deficient fields.

Other drivers and restraints analyzed in the detailed report include:

- Specialty-crop acreage expansion

- USDA cost-share for micronutrient plans

- Tank-mix issues with phosphate starters

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Zinc held the largest United States micronutrient fertilizers market share at 31.5% in 2025, supported by widespread use across corn, soybean, and wheat production, where zinc deficiencies remain common in high-yielding systems. Sustained demand from zinc-deficient and alkaline soils, coupled with high-pH irrigation conditions, reinforces its position. Copper also remains an important product category due to its nutritional benefits and use in certain crop protection programs across corn, soybean, and specialty crop production, while boron continues to gain traction in deficiency-prone regions despite its relatively narrow application margins.

Molybdenum, though a smaller segment, is the fastest-growing product category, with a projected CAGR of 7.3% through 2031. Growth is driven by increasing emphasis on biological nitrogen fixation and nitrogen-use efficiency, particularly in legume production systems. Ongoing research into mechanochemically modified Mo-Zn composites with slow-release nutrient delivery characteristics may support future product innovation within the segment. Additionally, advancements in second-generation chelates and dry dispersible powder formulations improve performance in calcareous soils, enabling premium pricing opportunities. Specialty growers in California are increasingly adopting multi-micronutrient application programs that favor tank-stable blends for both drip and aerial applications, supporting broader micronutrient market expansion.

Conventional sulfates, oxides, and basic salts accounted for 76.3% of the United States micronutrient fertilizer market size in 2025, due to their low cost and broad availability. Despite dominance, specialty forms are growing at a 6.6% CAGR through 2031. Liquids enable uniform, variable-rate placement alongside herbicides, while controlled-release coatings reduce leaching and soil tie-up, which is critical in sandy Florida citrus groves. Water-soluble powders boost foliar uptake for horticulture and turf managers. Field evidence shows yield benefits and simplified logistics offsetting premiums, especially where carbon programs grant additional value for efficiency gains.

Advances in polymer coatings and nano-encapsulation drive differentiation as suppliers seek to expand their margins beyond basic commodities. Investments in proprietary chemistries by market leaders signal a strategic pivot to specialty value pools, elevating the overall sophistication of the United States micronutrient fertilizers industry.

Complete Report Scope:

- Product

- Boron

- Copper

- Iron

- Manganese

- Molybdenum

- Zinc

- Others

- Form

- Conventional

- Speciality

- CRF

- Liquid Fertilizer

- SRF

- Water Soluble

- Application

- Soil

- Foliar

- Fertigation

- Crop Type

- Field Crops

- Horticultural Crops

- Turf & Ornamental

List of Companies Covered in this Report:

- The Mosaic Company

- The Andersons Inc.

- Yara International ASA

- Wilbur-Ellis Company LLC

- Sociedad Quimica y Minera de Chile SA

- Nutrien Ltd.

- Helena Agri-Enterprises LLC (Marubeni Corp.)

- Brandt Inc.

- Koch Agronomic Services (Koch Industries Inc.)

- Nouryon

- Haifa Group

- ICL Group Ltd.

- BASF SE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY & KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Precision-Rate Micronutrient Application Gains Traction

- 4.5.2 Rising Zinc and Boron Deficiencies in Corn Belt Soils

- 4.5.3 Expansion of Specialty-Crop Acreage in California and Florida

- 4.5.4 USDA Cost-Share Programs Cover Micronutrient Plans

- 4.5.5 Emergence of In-Furrow Chelated Blends for Low-pH Soils

- 4.5.6 Carbon-Credit Programs Reward Higher Nutrient-Use Efficiency

- 4.6 Market Restraints

- 4.6.1 Price Premium Versus N-P-K Discourages Broad-Acre Adoption

- 4.6.2 Volatility in Corn and Soybean Prices Affecting Input Spend

- 4.6.3 Tank-Mix Compatibility Issues with Phosphate Starters

- 4.6.4 Regenerative "Input-Light" Movements Among Large Growers

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Product

- 5.1.1 Boron

- 5.1.2 Copper

- 5.1.3 Iron

- 5.1.4 Manganese

- 5.1.5 Molybdenum

- 5.1.6 Zinc

- 5.1.7 Others

- 5.2 Form

- 5.2.1 Conventional

- 5.2.2 Speciality

- 5.2.2.1 CRF

- 5.2.2.2 Liquid Fertilizer

- 5.2.2.3 SRF

- 5.2.2.4 Water Soluble

- 5.3 Application

- 5.3.1 Soil

- 5.3.2 Foliar

- 5.3.3 Fertigation

- 5.4 Crop Type

- 5.4.1 Field Crops

- 5.4.2 Horticultural Crops

- 5.4.3 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 The Mosaic Company

- 6.4.2 The Andersons Inc.

- 6.4.3 Yara International ASA

- 6.4.4 Wilbur-Ellis Company LLC

- 6.4.5 Sociedad Quimica y Minera de Chile SA

- 6.4.6 Nutrien Ltd.

- 6.4.7 Helena Agri-Enterprises LLC (Marubeni Corp.)

- 6.4.8 Brandt Inc.

- 6.4.9 Koch Agronomic Services (Koch Industries Inc.)

- 6.4.10 Nouryon

- 6.4.11 Haifa Group

- 6.4.12 ICL Group Ltd.

- 6.4.13 BASF SE