|

시장보고서

상품코드

2073599

인도의 미량영양소 비료 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)India Micronutrient Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

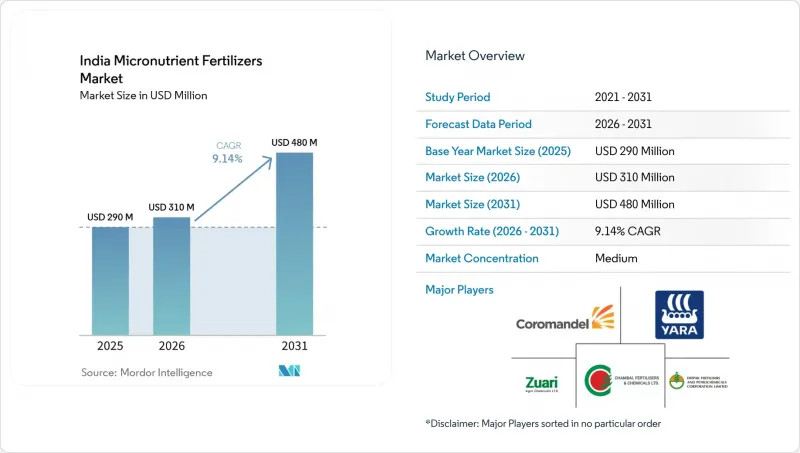

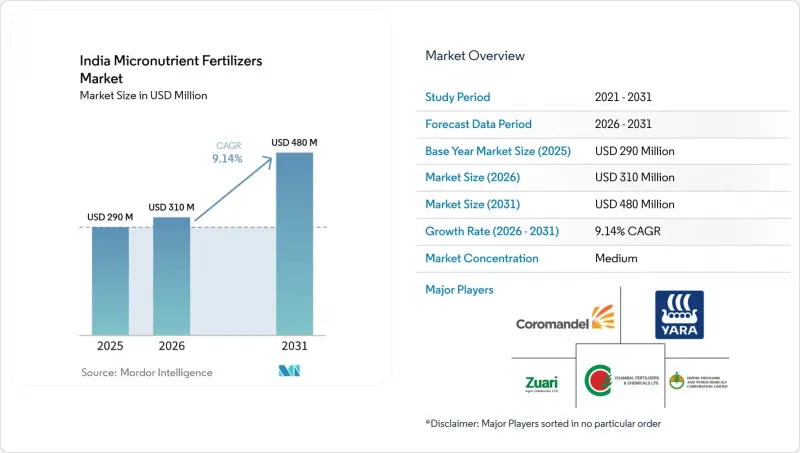

Mordor Intelligence에 의하면, 인도의 미량영양소 비료 시장 규모는 2025년 2억 9,000만 달러로 평가되었습니다. 2026년에는 3억 1,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 9.14%로 성장을 지속하여, 2031년에는 4억 8,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 유형(붕소, 구리, 철, 망간, 몰리브덴, 아연 등), 시비 방법(비료 관개, 엽면 시비 등) 및 작물 유형(밭작물, 원예작물 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(미터톤) 단위로 제시되어 있습니다.

인도의 미량영양소 비료 시장 동향 및 분석

집약적 농업이 이루어지는 지역에서 토양 미량영양소의 고갈이 진행되고 있습니다.

펀자브 주, 하리야나 주, 그리고 우타르 프라데시 주 서부 지역에서 벼, 밀, 면화의 연속적인 윤작으로 인해 아연, 붕소, 철분의 저장량이 자연적인 보충 속도를 웃도는 속도로 고갈되고 있으며, 그 결과 주요 영양소의 사용량이 증가하고 있음에도 불구하고 수확량 증가세가 둔화되고 있습니다. '토양 건강 카드'해당 자료에 따르면, 펀자브 주의 경작지 78%, 하리야나 주의 65%에서 현재 아연 결핍이 확인되고 있습니다. 경제학자들은 이러한 부족으로 인한 연간 생산량 손실이 막대할 것으로 추산하고 있습니다. 아연 보충 시비를 통해 밀의 경우 헥타르당 200-400kg, 쌀의 경우 300-600kg의 수확량 증가가 예상에 따라, 각 지역 당국은 농업 보급 활동을 강화하고 있습니다. “비료 관리령(FCO)”이에 따른 미량영양소 표시 의무화와 검사 능력 확충은 품질 보증의 기반이 되고 있으며, 인도의 미량영양소 비료 시장에 구조적으로 긍정적인 요인으로 작용하고 있습니다.

강화 NPK 복합비료(NBS-2)에 대한 정부 보조금 확대

2024년 12월부터 미량영양소가 강화된 DAP 및 NPK 등급 비료가 농가 직접 지원 대상이 되며, 소매 가격이 40-50% 인하됨에 따라 마하라슈트라 주, 카르나타카 주, 안드라프라데시주, 타밀나두주에서의 채택률은 2022년 15%에서 2024년에는 28%로 상승했습니다. NBS 체계 내 예산 배분은 2023-24 회계연도의 7,950억 루피(96억 2,000만 달러)에서 2024-25 회계연도에는 8,750억 루피(105억 달러)로 증가했으며, IFFCO나 Coromandel 등의 제조업체들이 블렌딩 능력을 35% 확대하는 데 힘을 실어주고 있습니다. 1차 농업신용협동조합을 통한 디지털 추적을 통해 유용 위험이 줄어들었으며, 의무화된 비료관리령(FCO)의 규격에 따라 판매되는 모든 포대에 아연, 붕소 또는 철이 기능적 수준으로 함유되어 있음을 보장합니다. 보조금이 앞당겨 지급되기 때문에 시장 확대의 대부분은 향후 2시즌 이내에 이루어질 것으로 예상되지만, 균형 잡힌 영양에 대한 인식은 지급 기간이 끝난 후에도 지속될 것입니다.

제2·제3층 농업자재 시장에서 위조품 및 불량품의 유통

미량영양소 혼합물인 척하는 저품질 분말이 비하르주, 우타르프라데시주, 오디샤주공급량의 15-20%를 차지하고 있으며, 이 지역에서는 소규모 판매업자들이 농업 자재 소매 시장을 독점하고 있습니다. 실험실 검사 결과, 금속 함량이 표시된 수치보다 30-50% 낮아 농작물 흉작을 초래하고 있으며, 이로 인해 정품 구매 의욕이 떨어지고 있습니다. 검사관 인력 부족과 인증 검사 기관의 부재가, “비료 관리령”에 근거한 법 집행에 지장을 주고 있습니다. 대기업들은 QR 코드를 통한 인증 시스템을 도입하고 있지만, 스마트폰 보급률의 격차와 낮은 디지털 문해력 때문에 그 확산이 더딘 실정입니다. 인증 체계가 확대되고 판매업체에 대한 감사가 강화되기 전까지는 위조품의 유출로 인해 단기적으로 인도의 미량영양소 비료 시장의 연평균 성장률(CAGR)이 1.2포인트 하락할 것으로 전망됩니다.

부문별 분석

2025년, 인도의 미량영양소 비료 시장에서 아연 제제는 35.9%의 점유율을 차지했으며, 이 나라에서 가장 널리 나타나는 토양 영양소 결핍 문제를 해결하는 데 있어 아연 제제가 수행하는 지극히 중요한 역할이 부각되었습니다. 특히 쌀, 밀, 옥수수 재배 분야에서 수요는 계속해서 견조한 양상을 보이고 있으며, 이러한 작물의 경우 아연 시비가 수확량 증대와 영양분 이용 효율 개선으로 직접 이어지고 있습니다. 또한, 토양 검사 활동과 균형 잡힌 비료 시비 프로그램의 확대를 통해 이 부문의 입지는 더욱 공고해지고 있습니다.

시장은 점차 붕소계 제품으로 전환되고 있으며, 2026년부터 2031년까지 연평균 성장률(CAGR) 10.6%를 나타낼 것으로 전망됩니다. 과일, 채소, 유지종자, 플랜테이션 작물의 재배 확대가 개화, 수분, 결실, 작물 생육에 중요한 역할을 하는 붕소 수요를 견인하고 있습니다. 또한, 특수 미량영양소 혼합물 및 비료 관개(퍼티게이션)용 제제의 채택이 확대됨에 따라, 기존의 아연 제품을 뛰어넘는 새로운 성장 기회가 창출되고 있습니다. 철, 구리, 망간, 몰리브덴을 함유한 비료는 인도의 다양한 농업 시스템에서 작물 및 지역 특유의 영양 결핍 문제를 해결하는 데 있어 계속해서 중요한 보조적 역할을 수행하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 주요 요약 및 주요 조사 결과

제3장 보고서의 내용

제4장 주요 업계 동향

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 비료 업계 CEO가 직면하는 중요 전략적 과제

KTHAccording to Mordor Intelligence, the india micronutrient fertilizers market size is projected to grow from USD 290.0 million in 2025 to USD 310.0 million in 2026 and is forecast to reach USD 480.0 million by 2031 at 9.14% CAGR over 2026 to 2031.

This report is Segmented by Product Type (Boron, Copper, Iron, Manganese, Molybdenum, Zinc, and More), by Application Mode (Fertigation, Foliar, and More), and by Crop Type (Field Crops, Horticultural Crops, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

India Micronutrient Fertilizers Market Trends and Insights

Rising Soil Micronutrient Depletion Across Intensively Farmed Districts

Continuous rice-wheat and cotton cycles in Punjab, Haryana, and Western Uttar Pradesh have depleted zinc, boron, and iron reserves faster than natural replenishment, resulting in reduced yield gains despite increased macronutrient use. Soil Health Card data show that 78% of Punjab's and 65% of Haryana's cultivated soils now test zinc-deficient . Economists estimate significant annual output losses associated with these gaps. Corrective zinc applications deliver 200-400 kg per-hectare wheat gains and 300-600 kg rice gains, prompting district authorities to intensify extension outreach. Mandatory micronutrient labeling under the Fertilizer Control Order (FCO) and expanded lab testing capacity serve as a backstop for quality assurance, making the driver structurally positive for the India micronutrient fertilizers market.

Government Subsidy Extension for Fortified NPK Blends (NBS-2)

Beginning December 2024, micronutrient-fortified DAP and NPK grades will qualify for direct farm-gate support, reducing retail prices by 40-50% and increasing adoption in Maharashtra, Karnataka, Andhra Pradesh, and Tamil Nadu from 15% in 2022 to 28% in 2024 . The budgetary outlay under the NBS window increased from INR 795 billion (USD 9.62 billion) in 2023-24 to INR 875 billion (USD 10.5 billion) in 2024-25, encouraging manufacturers such as IFFCO and Coromandel to expand their blending capacity by 35%. Digital tracking through Primary Agricultural Credit Societies reduces the risk of diversion, and the mandatory Fertilizer Control Order (FCO) specifications ensure that every bag sold contains functional levels of zinc, boron, or iron. The subsidy is front-loaded, so the bulk of market lift is projected within the next two seasons, though balanced nutrition awareness will persist beyond the payout period.

Counterfeit and Spurious Product Circulation in Tier-2/3 Agri-Inputs Markets

Subpar powders masquerading as micronutrient blends account for 15-20% of the supply in Bihar, Uttar Pradesh, and Odisha, where small dealers dominate input retail. Lab tests reveal that metal contents are 30-50% below the labels, causing crop failures that discourage legitimate purchases. Limited inspectorates and a lack of accredited laboratories hinder enforcement under the Fertilizer Control Order. Large producers have added QR code verification, and the smartphone penetration gaps and poor digital literacy are slowing down take-up. Until authentication scales and dealer audits tighten, counterfeit leakage will shave 1.2 percentage points off the India micronutrient fertilizers market CAGR in the near term.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Specialty Chelated Formulations by Horticulture Clusters

- Emerging Nano-Micronutrient Products from Ag-Tech Startups

- Logistics Bottlenecks for Bulk Micronutrient Movement to Land-Locked Regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Zinc formulations accounted for 35.9% of the India micronutrient fertilizers market share in 2025, highlighting their critical role in addressing one of the country's most prevalent soil nutrient deficiencies. Demand remains particularly strong in the cultivation of rice, wheat, and maize, where zinc application is directly associated with improved yields and enhanced nutrient-use efficiency. The segment's position has been further reinforced by the expansion of soil-testing initiatives and balanced fertilization programs.

The market is gradually shifting toward boron-based products, which are projected to register a CAGR of 10.6% during 2026-2031. The increasing cultivation of fruits, vegetables, oilseeds, and plantation crops is driving demand for boron, which plays a vital role in flowering, pollination, fruit set, and crop development. Additionally, the growing adoption of specialty micronutrient blends and fertigation-compatible formulations is creating new growth opportunities beyond traditional zinc products. Fertilizers containing iron, copper, manganese, and molybdenum continue to play an important supporting role in addressing crop- and region-specific nutrient deficiencies across India's diverse agricultural systems.

Complete Report Scope:

- Product

- Boron

- Copper

- Iron

- Manganese

- Molybdenum

- Zinc

- Others

- Application Mode

- Fertigation

- Foliar

- Soil

- Crop Type

- Field Crops

- Horticultural Crops

- Turf and Ornamental

List of Companies Covered in this Report:

- Coromandel International Limited

- Chambal Fertilizers and Chemicals Limited

- Indian Farmers Fertiliser Cooperative Limited

- Deepak Fertilizers and Petrochemicals Corporation Limited

- Zuari Agro Chemicals Limited

- Rashtriya Chemicals and Fertilizers Limited

- Aries Agro Limited

- Tata Chemicals Limited

- Mangalore Chemicals and Fertilizers Limited

- Nagarjuna Fertilizers and Chemicals Limited

- BASF India Limited

- Compo Expert India Private Limited

- Haifa Chemicals Ltd

- Yara Fertilisers India Private Limited

- Sociedad Quimica y Minera de Chile S.A. (SQM) India Private Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 EXECUTIVE SUMMARY & KEY FINDINGS

3 REPORT OFFERS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Rising Soil Micronutrient Depletion Across Intensively Farmed Districts

- 4.6.2 Government Subsidy Extension for Fortified NPK Blends (NBS-2)

- 4.6.3 Rapid Adoption of Specialty Chelated Formulations by Horticulture Clusters

- 4.6.4 Expansion of Fertigation Infrastructure under Pradhan Mantri Krishi Sinchayee Yojana (PMKSY) Micro-Irrigation Scheme

- 4.6.5 Emerging Nano-Micronutrient Products from Indian Ag-Tech Start-Ups

- 4.6.6 Carbon-Credit Premium for Micronutrient-Driven Yield Boosts

- 4.7 Market Restraints

- 4.7.1 Counterfeit and Spurious Product Circulation in Tier-2/3 Agri-Inputs Markets

- 4.7.2 Volatility in Mined Zinc and Boron Concentrate Prices

- 4.7.3 Limited Farmer Awareness in Eastern and North-Eastern States

- 4.7.4 Logistics Bottlenecks for Bulk Micronutrient Movement to Land-Locked Regions

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Product

- 5.1.1 Boron

- 5.1.2 Copper

- 5.1.3 Iron

- 5.1.4 Manganese

- 5.1.5 Molybdenum

- 5.1.6 Zinc

- 5.1.7 Others

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf and Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (Includes Global Level Overview, Market Level overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Coromandel International Limited

- 6.4.2 Chambal Fertilizers and Chemicals Limited

- 6.4.3 Indian Farmers Fertiliser Cooperative Limited

- 6.4.4 Deepak Fertilizers and Petrochemicals Corporation Limited

- 6.4.5 Zuari Agro Chemicals Limited

- 6.4.6 Rashtriya Chemicals and Fertilizers Limited

- 6.4.7 Aries Agro Limited

- 6.4.8 Tata Chemicals Limited

- 6.4.9 Mangalore Chemicals and Fertilizers Limited

- 6.4.10 Nagarjuna Fertilizers and Chemicals Limited

- 6.4.11 BASF India Limited

- 6.4.12 Compo Expert India Private Limited

- 6.4.13 Haifa Chemicals Ltd

- 6.4.14 Yara Fertilisers India Private Limited

- 6.4.15 Sociedad Quimica y Minera de Chile S.A. (SQM) India Private Limited