|

시장보고서

상품코드

2073597

중국의 미량영양소 비료 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)China Micronutrient Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

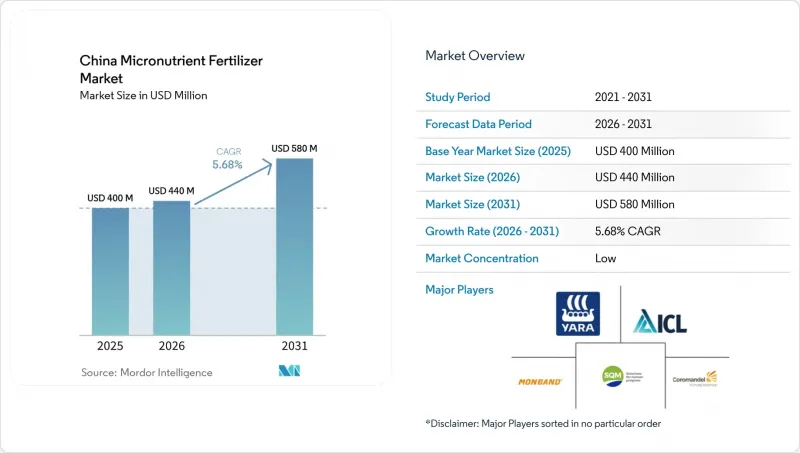

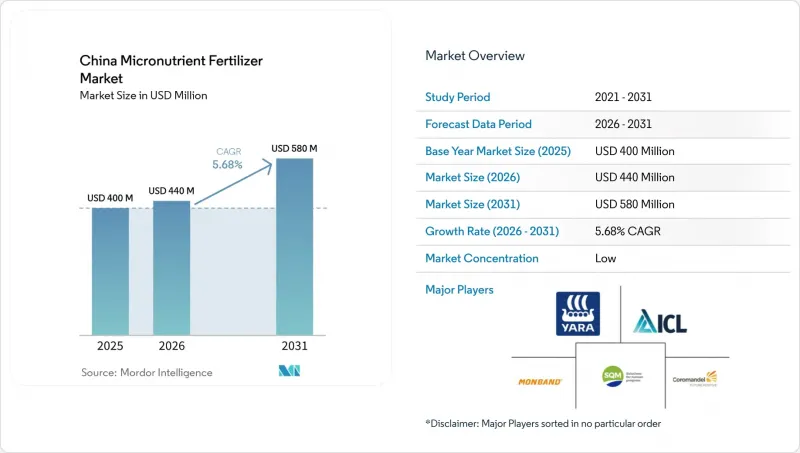

Mordor Intelligence에 의하면, 중국의 미량영양소 비료 시장 규모는 2025년 4억 달러에서 증가해, 2026년에는 4억 4,000만 달러에 이를 것으로 추정되고 있습니다. 본 보고서는 제품별(붕소, 동, 철, 망간, 몰리브덴, 아연, 기타), 시용 방법별(시비 관개, 엽면살포, 토양시용) 및 작물 유형별(밭농사 작물, 원예 작물, 잔디·관상용 작물) 마다 분류되고 있습니다.시장 예측은 금액(달러) 및 수량(메트릭톤)으로 제시되고 있습니다.

중국의 미량영양소 비료 시장 동향 및 분석

정밀 농업의 도입이 미량영양소 수요를 가속화

중국의 농업 기술 혁명은 영양분의 시비 위치와 시기를 최적화하는 가변 시비 시스템을 통해 미량 원소 비료 수요를 견인하고 있습니다. 정부가 지원하는 스마트 농업 이니셔티브 덕분에 생산 지역 전체에서 스마트 농업 기술 도입률이 27.6%에 달했으며, GPS 유도식 살포기에 대응하는 정밀하게 배합된 미량영양소 혼합물에 대한 수요가 발생하고 있습니다. 이러한 기술적 혁신 덕분에 농가들은 토양 검사 데이터를 바탕으로 밭마다 최적의 양으로 미량영양소를 시비할 수 있게 되었으며, 시비 효율과 총 소비량 모두 향상되고 있습니다. IoT 센서와 드론을 활용한 모니터링 시스템을 통합함으로써, 특히 아연과 붕소의 정밀한 관리가 필요한 고부가가치 작물의 경우, 미량영양소의 시비를 실시간으로 조절할 수 있게 되었습니다. 정밀 농업의 도입이 확대됨에 따라, 농가들이 일률적인 시비 대신 대상 작물을 선별한 영양 관리 프로그램을 통해 수확량 잠재력을 최적화함에 따라, 1헥타르당 미량영양소 사용량이 증가하고 있습니다.

의무화된 토양 영양분 분석 프로그램

2025년에 시행된 중국 농업부의 토양 검사 지침에 따르면, 농가들은 비료 보조금을 신청하기 전에 인증을 받은 토양 영양분 분석을 실시해야 하며, 이로 인해 미량영양소의 구매 패턴이 근본적으로 변화하고 있습니다. 이러한 정책 전환으로 인해 농가들이 정부의 지원 프로그램을 이용하려면 영양소 결핍을 입증해야 하므로, 토양별 미량영양소 권장량에 대한 수요가 필연적으로 발생하고 있습니다. 이러한 검사 의무화는 특히 토양 분석 서비스나 맞춤형 배합 능력을 제공하는 미량영양소 공급업체에 이점을 가져다줄 것입니다. 이는 농가들이 검사, 권장, 제품 공급을 결합한 통합적인 솔루션을 원하기 때문입니다. 각 성별 시행 상황은 집행의 엄격도에 차이가 있으며, 허난성이나 산동성과 같은 주요 곡물 생산 지역에서는 가장 엄격한 준수 요건이 부과되고 있습니다. 이 규제 체계에 따라 미량영양소 비료는 "임의의 투입 자재"에서 "문서화된 필수품"으로 변모하여, 모든 작물의 유형과 시용 방법에 있어 지속적인 판매량 성장을 뒷받침하고 있습니다.

도시화로 인한 경작지 감소

도시 개발의 압박으로 인해 중국의 경작 가능 면적이 감소하고 있으며, 농업의 집약화가 진행되고 있음에도 불구하고, 이는 미량영양소 비료 판매량 증가에 있어 구조적인 역풍이 되고 있습니다. 공업용지 및 주택용지로의 토지 용도 변경으로 인해 연간 약 20만 헥타르가 농업 생산에서 사라지고 있으며, 이로 인해 토양 시비형 미량영양소 제품의 잠재 시장이 직접적으로 축소되고 있습니다. 이러한 제약으로 인해 업계는 총 시비량을 늘리는 대신, 1헥타르당 양분 효율을 극대화하는 부가가치가 높은 솔루션으로 방향을 전환할 수밖에 없게 되었습니다. 연안 지역에서는 토지 이용 압력이 가장 심각하여, 남아 있는 농지의 통합이 진행되고 있으며, 대량 임베디드과 정밀 시비 기술을 중시하는 보다 대규모적이고 효율적인 농업 경영으로 전환되고 있습니다. 농가들이 줄어든 경작 면적에서 최대 수확량을 추구하는 가운데, 이러한 토지적 제약은 역설적으로 고품질 미량영양소 제품에 대한 수요를 뒷받침하고 있지만, 궁극적으로는 시장 전체의 성장 가능성을 제한하게 될 것입니다.

부문별 분석

아연은 농업용 토양에서 광범위하게 나타나는 아연 결핍과 작물의 성장, 영양분 흡수, 수확량 증대에 있어 아연이 수행하는 필수적인 역할에 힘입어, 2025년에는 중국의 미량영양소 비료 시장에서 가장 큰 점유율(34.6%)을 차지했습니다. 특히 곡물, 유지종자, 원예작물 분야의 아연 수요는 계속해서 견조한 양상을 보이고 있습니다. 또한, 킬레이트화 및 수용성 아연 제제의 사용이 증가함에 따라 영양소 이용 효율이 향상되고 있습니다. 정부 주도의 토양 검사 사업과 정밀 영양 관리 프로그램을 통해 주요 농업 지역 전반에서 아연 비료 소비가 더욱 확대되고 있습니다.

붕소는 2026년부터 2031년까지 연평균 성장률(CAGR) 8.9%를 나타낼 것으로 예측되며, 가장 빠르게 성장하는 제품 부문이 될 것으로 전망됩니다. 이러한 성장은 과일, 채소 및 기타 고부가가치 작물의 재배 확대에 힘입은 바가 크며, 이러한 작물에서 붕소는 개화, 수분, 착과 및 작물의 품질에 있어 필수적인 역할을 하고 있습니다. 비료 및 관개 시스템과 특수 영양소 프로그램의 도입이 확대되고 있는 점도, 특히 집약적인 원예 생산 지역에서 붕소계 비료에 대한 수요를 더욱 높이고 있습니다. 한편, 철, 구리, 망간, 몰리브덴 등 기타 미량영양소는 작물별 영양 결핍 해소에 지속적으로 기여하고 있으며, 중국의 미량영양소 비료 시장 전체의 성장에 기여하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 보고서의 내용

제3장 주요 요약 및 주요 조사 결과

제4장 주요 업계 동향

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 비료 업계 CEO가 직면하는 중요 전략적 과제

KTHAccording to Mordor Intelligence, the china micronutrient fertilizer market size is estimated at USD 440.0 million in 2026, up from USD 400.0 million in 2025. This report is Segmented by Product (Boron, Copper, Iron, Manganese, Molybdenum, Zinc, and Others), by Application Mode (Fertigation, Foliar, and Soil), and by Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

China Micronutrient Fertilizer Market Trends and Insights

Precision-Farming Adoption Accelerates Micronutrient Demand

China's agricultural technology revolution drives micronutrient fertilizer demand through variable-rate application systems that optimize nutrient placement and timing. Government-backed smart agriculture initiatives have achieved 27.6% adoption of intelligent agriculture technologies across production areas, creating demand for precision-formulated micronutrient blends compatible with GPS-guided applicators . This technological shift enables farmers to apply micronutrients at field-specific rates based on soil testing data, increasing both application efficiency and total consumption volumes. The integration of Internet of Things sensors and drone-based monitoring systems allows real-time adjustment of micronutrient applications, particularly for high-value crops requiring precise zinc and boron management. Precision farming adoption correlates with higher per-hectare micronutrient usage as farmers optimize yield potential through targeted nutrition programs rather than blanket applications.

Mandated Soil Nutrient Testing Programs

China's Ministry of Agriculture soil testing directive, effective 2025, requires certified soil nutrient analysis before farmers can claim fertilizer subsidies, fundamentally altering micronutrient purchasing patterns. This policy shift creates mandatory demand for soil-specific micronutrient recommendations, as farmers must demonstrate nutrient deficiencies to access government support programs. The testing mandate particularly benefits micronutrient suppliers offering soil analysis services and customized blending capabilities, as farmers seek integrated solutions combining testing, recommendation, and product supply. Provincial implementation varies in enforcement rigor, with major grain-producing regions like Henan and Shandong showing the strictest compliance requirements. This regulatory framework transforms micronutrient fertilizers from optional inputs to documented necessities, supporting sustained volume growth across all crop types and application methods.

Arable-Land Shrinkage Due to Urbanization

Urban development pressure reduces China's cultivable land area, creating a structural headwind for volume-based micronutrient fertilizer growth despite intensification efforts. Land conversion to industrial and residential uses removes approximately 200,000 hectares annually from agricultural production, directly reducing the addressable market for soil-applied micronutrient products. This constraint forces the industry toward value-added solutions that maximize nutrient efficiency per hectare rather than expanding total application volumes. Coastal provinces experience the most severe land pressure, driving consolidation of remaining farmland into larger, more efficient operations that favor bulk purchasing and precision application technologies. The land constraint paradoxically supports premium micronutrient products as farmers seek maximum yield from reduced acreage, but ultimately limits total market expansion potential.

Other drivers and restraints analyzed in the detailed report include:

- Government Subsidies Favor Chelated Formulations

- Expansion Of High-Tech Greenhouses in Yangtze Delta

- Trace-Metal Contamination Limits Application Rates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Zinc accounted for the largest China micronutrient fertilizer market share, 34.6% in 2025, supported by widespread zinc deficiencies in agricultural soils and its essential role in enhancing crop growth, nutrient uptake, and yield performance. Demand for zinc remains particularly strong in cereals, oilseeds, and horticultural crops. Additionally, the increasing adoption of chelated and water-soluble zinc formulations is improving nutrient-use efficiency. Government-led soil testing initiatives and precision nutrient management programs are further boosting zinc fertilizer consumption across key agricultural regions.

Boron is anticipated to be the fastest-growing product segment, with a projected CAGR of 8.9% during 2026 to 2031. This growth is driven by the expanding cultivation of fruits, vegetables, and other high-value crops, where boron is critical for flowering, pollination, fruit set, and crop quality. The rising adoption of fertigation systems and specialty nutrient programs is further increasing demand for boron-based fertilizers, particularly in intensive horticultural production areas. Meanwhile, other micronutrients such as iron, copper, manganese, and molybdenum continue to address crop-specific nutrient deficiencies, contributing to the overall growth of the China micronutrient fertilizer market.

Complete Report Scope:

- Product

- Boron

- Copper

- Iron

- Manganese

- Molybdenum

- Zinc

- Others

- Application Mode

- Fertigation

- Foliar

- Soil

- Crop Type

- Field Crops

- Horticultural Crops

- Turf & Ornamental

List of Companies Covered in this Report:

- Yara International ASA

- ICL Group Ltd

- Hebei Monband Water Soluble Fertilizer Co. Ltd

- Sociedad Quimica y Minera de Chile SA

- Coromandel International Ltd.

- Kingenta Group

- Sinochem Holdings Corp. Ltd.

- ChemChina

- Grupa Azoty S.A.

- The Mosaic Company

- Nutrien Ltd.

- Haifa Chemicals Ltd.

- Tradecorp International S.A. (Rovensa Group)

- Anhui Huaheng Biotechnology Co., Ltd.

- Sichuan Shucan Chemical Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY & KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Primary Nutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Primary Nutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Precision-farming adoption accelerates micronutrient demand

- 4.6.2 Mandated soil nutrient testing programs

- 4.6.3 Government subsidies favoring chelated formulations

- 4.6.4 Expansion of high-tech greenhouses in Yangtze Delta

- 4.6.5 Rapid growth of specialty fruit exports

- 4.6.6 Domestic production of zinc sulfate reaches scale economies

- 4.7 Market Restraints

- 4.7.1 Arable-land shrinkage due to urbanization

- 4.7.2 Trace-metal contamination limits application rates

- 4.7.3 Volatility in raw-material prices

- 4.7.4 Farmer price-sensitivity amid rising input costs

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Product

- 5.1.1 Boron

- 5.1.2 Copper

- 5.1.3 Iron

- 5.1.4 Manganese

- 5.1.5 Molybdenum

- 5.1.6 Zinc

- 5.1.7 Others

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Yara International ASA

- 6.4.2 ICL Group Ltd

- 6.4.3 Hebei Monband Water Soluble Fertilizer Co. Ltd

- 6.4.4 Sociedad Quimica y Minera de Chile SA

- 6.4.5 Coromandel International Ltd.

- 6.4.6 Kingenta Group

- 6.4.7 Sinochem Holdings Corp. Ltd.

- 6.4.8 ChemChina

- 6.4.9 Grupa Azoty S.A.

- 6.4.10 The Mosaic Company

- 6.4.11 Nutrien Ltd.

- 6.4.12 Haifa Chemicals Ltd.

- 6.4.13 Tradecorp International S.A. (Rovensa Group)

- 6.4.14 Anhui Huaheng Biotechnology Co., Ltd.

- 6.4.15 Sichuan Shucan Chemical Co., Ltd.