|

시장보고서

상품코드

2073652

독일의 비료 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Germany Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

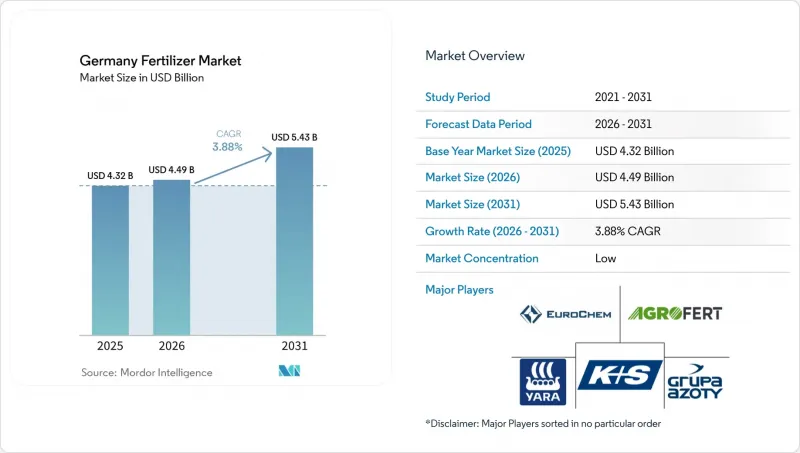

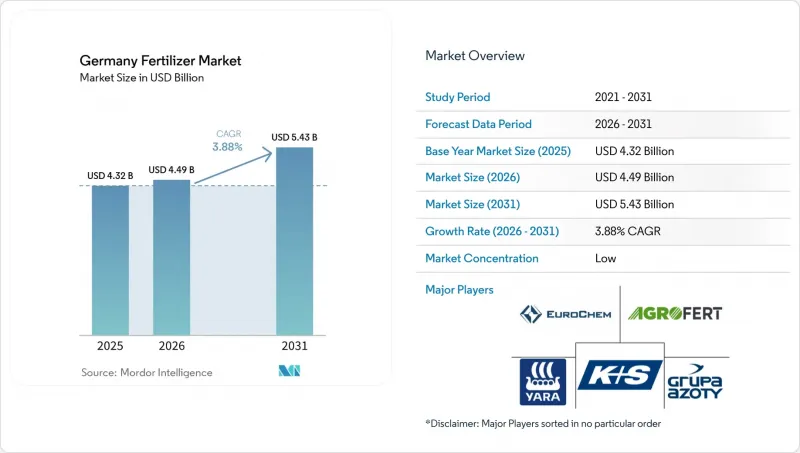

Mordor Intelligence에 의하면, 2026년 독일 비료 시장 규모는 43억 2,000만 달러로 추정되고 있어 2025년 44억 9,000만 달러에서 확대해, 2031년에는 54억 3,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 3.88%로 성장할 것으로 전망됩니다.

본 보고서는 유형별(복합비료 및 단일비료), 형태별(기존 및 특수형), 시비 방법별(시비 관개, 엽면 시비, 토양 시비), 그리고 작물 유형별(밭작물, 원예작물, 잔디 및 관상용 작물)로 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(미터톤) 단위로 제시되어 있습니다.

독일 비료 시장 동향과 인사이트

정밀 농업 분야의 비료 및 관개 열풍

독일에서 일어나고 있는 정밀 농업의 혁명은 비료 시비 방식을 근본적으로 변화시키고 있으며, 상업 농가에서의 비료 시비 및 관개 시스템 도입률은 그 어느 때보다 높아지고 있습니다. IoT 센서, GPS 유도식 시비 장비, 가변 시비 기술의 통합을 통해 농가에서는 그 어느 때보다 정밀하게 양분 공급을 최적화할 수 있게 되었으며, 투입 비용을 절감하면서도 작물의 수확량을 극대화할 수 있게 되었습니다. 현재 디지털 농업 플랫폼이 토양 상태를 실시간으로 모니터링하고 있으며, 기상 패턴, 작물의 생육 단계, 영양분의 이용 가능성에 따라 비료량을 동적으로 조정할 수 있게 되었습니다.

고효율 비료에 대한 수요

서방형, 안정화된 질소 및 질산화 억제제를 함유한 제품은 영양분의 휘발 및 침출을 방지합니다. 이는 질산염 취약 지역이 농지의 28%에 달하는 상황에서 중요한 장점이 되고 있습니다. BASF가 루트비히스하펜에 1억 5,000만 유로(1억 6,300만 달러)를 투자함에 따라, 우레아제 억제제 코팅제의 현지 공급이 확대되고 있습니다. 한편, 농가들이 비료 시비 횟수 감소와 수확량 안정성 향상을 높이 평가함에 따라 고가 제품의 가격 차이는 점차 줄어들고 있습니다. 일반적으로 기존 제품보다 20-30% 비싼 고효율 비료의 프리미엄 가격은 시비 횟수 감소와 작물 수확량 증가를 통해 상쇄되고 있어, 선진적인 농가에게 이러한 기술은 경제적으로 실현 가능한 것이 되고 있습니다.

질산염 시비 상한선 강화

독일에서는 개정된 비료 규정에 따라 질산염 시비 제한이 점점 더 엄격해지고 있어, 기존의 비료 사용 방식이 제약을 받게 되면서 농가들은 영양 관리 전략을 재검토할 수밖에 없는 상황에 처해 있습니다. 질산염에 취약한 지역의 추가 지정에 따라, 현재 독일 농지의 약 28%가 해당 대상에 포함되어 있으며, 작물의 필요량에 비해 최대 20%의 질소 시비량 감축이 의무화되어 있습니다. 이러한 규제는 그동안 수확량을 극대화하기 위해 다량의 질소 시비에 의존해 온 집약적인 작물 생산 시스템에 있어 특히 큰 과제가 되고 있습니다.

부문별 분석

2025년 현재, 단일 영양소 비료는 독일 비료 시장 점유율의 65.8%를 차지하고 있으며, 이는 정밀한 영양 관리와 비용 최적화를 가능하게 하는 단일 영양소 제품을 독일 농가들이 선호하는 경향을 반영하고 있습니다. 이 부문이 시장을 독점하고 있는 배경에는 토양 검사 결과와 작물별 요건에 따라 비료 시비 계획을 유연하게 맞춤 설정할 수 있다는 점이 있습니다. 요소는 높은 영양분 함량과 정밀 시비 장비와의 호환성 덕분에 여전히 주요 질소 공급원으로 자리 잡고 있습니다. 한편, 염화칼륨(MoP)은 주요 칼륨 비료로서 확고한 입지를 유지하고 있습니다. 또한, 토양 검사 프로그램을 통해 집약형 재배 시스템에서 영양소 결핍이 계속해서 확인됨에 따라, 아연, 붕소, 망간 제품을 포함한 단일 미량 원소 비료에 대한 수요도 증가하고 있습니다.

복합비료는 나머지 시장 점유율을 차지하고 있으며, 인건비 측면에서 단일 시비 프로그램이 여러 가지 단일 비료 처리 방식보다 선호되는 지역에서 인기가 높아지고 있습니다. 이 부문은 가장 빠른 성장이 예상되며, 2026년부터 2031년까지 연평균 성장률(CAGR) 4.7%를 나타낼 것으로 전망됩니다. 이러한 성장은 균형 잡힌 영양 배합에 대한 수요 증가, 비료 시비 효율 향상, 그리고 영양 관리의 간소화에 힘입어 이루어지고 있습니다. DAP 및 NPK 복합비료와 같은 제품은 영양소 공급 최적화를 중시하는 통합 영양 관리 기법과 정밀 농업 시스템의 도입으로 인해 혜택을 보고 있습니다. 운영 효율과 균형 잡힌 작물 영양에 대한 관심이 높아짐에 따라, 독일 전역의 복합비료 수요는 더욱 증가할 것으로 예측됩니다.

2025년 기준으로 독일 비료 시장 규모의 81.1%를 기존 비료가 차지하고 있으며, 이는 독일 농업에서 기존의 입상 및 알갱이 형태의 복합 비료가 여전히 중요한 위치를 차지하고 있음을 보여줍니다. 이 부문의 안정성은 농가들이 기존 제품에 익숙해져 있다는 점과, 기존의 시비 장비 및 저장 인프라와의 높은 호환성을 반영하고 있습니다. 입상 요소, DAP 및 칼륨 제품은 경쟁력 있는 가격으로 신뢰할 수 있는 영양분 공급을 실현하며, 독일의 작물 생산 분야에서 여전히 주력 제품으로서의 위상을 유지하고 있습니다. 기존 비료는 확립된 공급망, 표준화된 품질 사양, 그리고 모든 농업 지역에서 제품공급을 보장하는 광범위한 유통망의 혜택을 누리고 있습니다.

특수 비료는 규제 압력과 성능 향상을 추구하는 농가 수요에 힘입어, 2031년까지 연평균 성장률(CAGR)이 5.2%에 달하며 가장 빠르게 성장하고 있는 부문입니다. 방출 조절 비료(CRF)는 고부가가치 작물 생산 분야에서 시장 점유율을 확대하고 있으며, 영양분의 방출을 식물의 흡수 패턴에 맞출 수 있다는 특징 덕분에 프리미엄 가격 책정이 정당화되고 있습니다. 수용성 비료는 온실 재배 및 시비 관개 분야에서 강력한 성장세를 보이고 있으며, 이러한 분야에서는 정확한 양분 관리와 식물의 신속한 반응이 성공의 중요한 요인으로 작용하고 있습니다. 방출 조절 비료(SRF)는 질산염 침출 규제로 인해 서방형 제제가 선호되는 환경을 고려해야 하는 지역에서 활용되고 있습니다. 액체 비료는 기존의 엽면 살포라는 틈새 용도에서 토양 주입 및 시비 관개 시스템으로 용도가 확대되고 있으며, 건조 제품에 비해 혼합 성능이 향상되고 취급 비용도 절감되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 개 보고서의 내용

제3장 주요 요약 및 주요 조사 결과

제4장 주요 업계 동향

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 비료 업계 CEO가 직면하는 중요 전략적 과제

JHSAccording to Mordor Intelligence, germany fertilizer market size in 2026 is estimated at USD 4.32 billion, growing from 2025 value of USD 4.49 billion with 2031 projections showing USD 5.43 billion, growing at 3.88% CAGR over 2026-2031.

This report is Segmented by Type (Complex and Straight), by Form (Conventional and Specialty), by Application Mode (Fertigation, Foliar, and Soil), and by Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Germany Fertilizer Market Trends and Insights

Precision-ag fertigation boom

Germany's precision agriculture revolution is fundamentally reshaping fertilizer application methods, with fertigation systems experiencing unprecedented adoption rates among commercial growers. The integration of IoT sensors, GPS-guided application equipment, and variable-rate technology enables farmers to optimize nutrient delivery with unprecedented precision, reducing input costs while maximizing crop yields. Digital agriculture platforms now monitor soil conditions in real-time, allowing for dynamic fertilizer adjustments based on weather patterns, crop growth stages, and nutrient availability.

Demand for enhanced-efficiency fertilizers

Controlled-release, stabilized nitrogen, and nitrification-inhibitor products shield nutrients from volatilization and leaching, a key advantage as nitrate-vulnerable zones rise to 28% of farmland. BASF's investment of EUR 150 million (USD 163 million) at Ludwigshafen expands the local supply of urease-inhibitor coatings, while premium pricing gaps tighten as growers factor in fewer passes and higher yield stability. The premium pricing of enhanced-efficiency fertilizers, typically 20-30% higher than conventional products, is being offset by reduced application frequency and improved crop performance, making these technologies economically viable for progressive farmers.

Stricter Nitrate Application Caps

Germany's implementation of increasingly restrictive nitrate application limits under the revised Fertilizer Ordinance is constraining traditional fertilizer usage patterns and forcing farmers to reconsider their nutrient management strategies. The designation of additional nitrate-vulnerable zones, now covering approximately 28% of German agricultural land, imposes mandatory reductions in nitrogen application rates of up to 20% compared to crop requirements. These restrictions are particularly challenging for intensive crop production systems that have historically relied on high nitrogen inputs to maximize yields.

Other drivers and restraints analyzed in the detailed report include:

- Greenhouse and hydroponic expansion

- Rising crop prices and farm income

- Volatile Gas and Phosphate-Rock Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Straight fertilizers command 65.8% of Germany fertillizers market share in 2025, reflecting German farmers' preference for single-nutrient products that enable precise nutrient management and cost optimization. The segment's dominance stems from the flexibility it provides in customizing fertilizer programs based on soil testing results and crop-specific requirements. Urea remains the leading nitrogen source due to its high nutrient content and compatibility with precision application equipment, while muriate of potash (MoP) maintains a strong position as the primary potassium fertilizer. Demand for straight micronutrient fertilizers, including zinc, boron, and manganese products, is also increasing as soil testing programs continue to identify nutrient deficiencies in intensive cropping systems.

Complex fertilizers account for the remaining market share and are gaining popularity in regions where single-application nutrient programs are preferred over multiple straight fertilizer treatments due to labor cost considerations. The segment is projected to be the fastest-growing, registering a CAGR of 4.7% from 2026 to 2031. Growth is driven by increasing demand for balanced nutrient formulations, improved application efficiency, and simplified nutrient management. Products such as DAP and NPK formulations are benefiting from the adoption of integrated nutrient management practices and precision farming systems that emphasize optimized nutrient delivery. The growing focus on operational efficiency and balanced crop nutrition is anticipated to further support demand for complex fertilizers across Germany.

Conventional fertilizers maintain 81.1% of the Germany fertillizers market size in 2025, demonstrating the continued importance of traditional granular and prilled formulations in German agriculture. The segment's stability reflects farmers' familiarity with conventional products and their compatibility with existing application equipment and storage infrastructure. Granular urea, DAP, and potash products remain the workhorses of German crop production, offering reliable nutrient delivery at competitive prices. Conventional fertilizers benefit from established supply chains, standardized quality specifications, and widespread dealer networks that ensure product availability across all agricultural regions.

Specialty fertilizers represent the fastest-growing segment, with a 5.2% CAGR through 2031, driven by regulatory pressures and farmer demand for enhanced performance characteristics. Controlled-release fertilizers (CRF) are gaining market share in high-value crop production, where their ability to synchronize nutrient release with plant uptake patterns justifies premium pricing. Water-soluble fertilizers are experiencing robust growth in greenhouse and fertigation applications, where precise nutrient control and rapid plant response are critical success factors. Slow-release fertilizers (SRF) are finding applications in environmentally sensitive areas where nitrate leaching restrictions favor extended-release formulations. Liquid fertilizers are expanding beyond their traditional foliar application niche into soil injection and fertigation systems, offering improved mixing capabilities and reduced handling costs compared to dry products.

Complete Report Scope:

- Type

- Complex

- Straight

- Micronutrients

- Boron

- Copper

- Iron

- Manganese

- Molybdenum

- Zinc

- Others

- Nitrogenous

- Urea

- Others

- Phosphatic

- DAP

- MAP

- SSP

- TSP

- Potassic

- MoP

- SoP

- Secondary Macronutrients

- Calcium

- Magnesium

- Sulfur

- Micronutrients

- Form

- Conventional

- Speciality

- CRF

- Liquid Fertilizer

- SRF

- Water Soluble

- Application Mode

- Fertigation

- Foliar

- Soil

- Crop Type

- Field Crops

- Horticultural Crops

- Turf and Ornamental

List of Companies Covered in this Report:

- AGLUKON Spezialduenger GmbH & Co. KG

- AGROFERT A.S. (AGROFERT Group)

- BASF SE

- Bayer AG

- CF Industries Holdings Inc.

- EuroChem Group AG

- Grupa Azoty S.A.

- Haifa Group

- ICL Group Ltd.

- Kingenta Ecological Engineering Group Co., Ltd. (Kingenta Group)

- K+S Aktiengesellschaft

- Mosaic Company

- Nutrien Ltd.

- PhosAgro PJSC

- Yara International ASA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Precision-ag fertigation boom

- 4.6.2 Demand for enhanced-efficiency fertilizers

- 4.6.3 Greenhouse and hydroponic expansion

- 4.6.4 Rising crop prices and farm income

- 4.6.5 Federal Humus carbon-credit scheme

- 4.6.6 Green-ammonia import corridors

- 4.7 Market Restraints

- 4.7.1 Stricter nitrate application caps

- 4.7.2 Volatile gas and phosphate-rock costs

- 4.7.3 Protest-driven policy uncertainty

- 4.7.4 Protein-crop rotation cannibalizing N demand

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Type

- 5.1.1 Complex

- 5.1.2 Straight

- 5.1.2.1 Micronutrients

- 5.1.2.1.1 Boron

- 5.1.2.1.2 Copper

- 5.1.2.1.3 Iron

- 5.1.2.1.4 Manganese

- 5.1.2.1.5 Molybdenum

- 5.1.2.1.6 Zinc

- 5.1.2.1.7 Others

- 5.1.2.2 Nitrogenous

- 5.1.2.2.1 Urea

- 5.1.2.2.2 Others

- 5.1.2.3 Phosphatic

- 5.1.2.3.1 DAP

- 5.1.2.3.2 MAP

- 5.1.2.3.3 SSP

- 5.1.2.3.4 TSP

- 5.1.2.4 Potassic

- 5.1.2.4.1 MoP

- 5.1.2.4.2 SoP

- 5.1.2.5 Secondary Macronutrients

- 5.1.2.5.1 Calcium

- 5.1.2.5.2 Magnesium

- 5.1.2.5.3 Sulfur

- 5.1.2.1 Micronutrients

- 5.2 Form

- 5.2.1 Conventional

- 5.2.2 Speciality

- 5.2.2.1 CRF

- 5.2.2.2 Liquid Fertilizer

- 5.2.2.3 SRF

- 5.2.2.4 Water Soluble

- 5.3 Application Mode

- 5.3.1 Fertigation

- 5.3.2 Foliar

- 5.3.3 Soil

- 5.4 Crop Type

- 5.4.1 Field Crops

- 5.4.2 Horticultural Crops

- 5.4.3 Turf and Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 AGLUKON Spezialduenger GmbH & Co. KG

- 6.4.2 AGROFERT A.S. (AGROFERT Group)

- 6.4.3 BASF SE

- 6.4.4 Bayer AG

- 6.4.5 CF Industries Holdings Inc.

- 6.4.6 EuroChem Group AG

- 6.4.7 Grupa Azoty S.A.

- 6.4.8 Haifa Group

- 6.4.9 ICL Group Ltd.

- 6.4.10 Kingenta Ecological Engineering Group Co., Ltd. (Kingenta Group)

- 6.4.11 K+S Aktiengesellschaft

- 6.4.12 Mosaic Company

- 6.4.13 Nutrien Ltd.

- 6.4.14 PhosAgro PJSC

- 6.4.15 Yara International ASA