|

시장보고서

상품코드

2044172

실리콘 에피텍셜 웨이퍼 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Silicon Epitaxial Wafer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

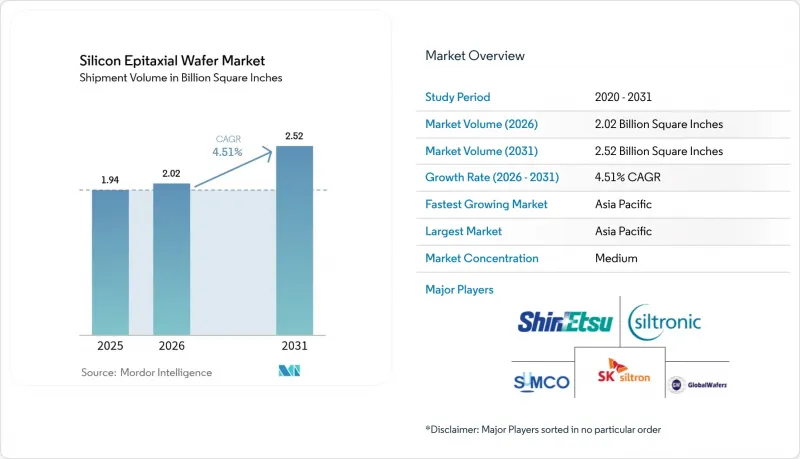

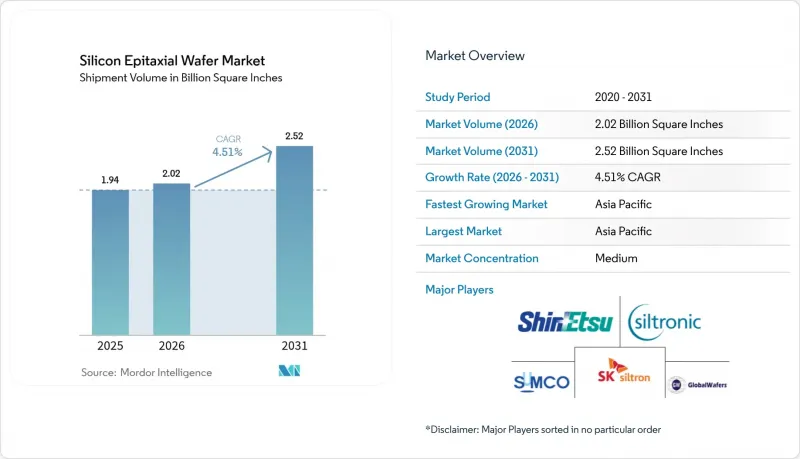

실리콘 에피텍셜 웨이퍼 시장 규모는 2025년 19억 3,859만 평방인치, 2026년 20억 1,827만 평방인치에서, 2031년까지 25억 1,609만 평방인치로 확대되어 2026년부터 2031년까지 CAGR 4.51%를 나타낼 것으로 예측됩니다.

300mm 기판용 더 두껍고 결함이 적은 레이어, 후면 공급 기술 채택, 자동차 전동화 및 온디바이스 AI 추론 수요 증가가 결합되어 생산량의 견조한 바닥을 지탱하고 있습니다. 아시아태평양의 설치된 원자로 수, 정부 보조금, 메모리 생산 능력 증가로 인해 아시아태평양의 생산량은 여전히 우위를 유지하고 있지만, 동위원소 정제된 Si-28 층을 이용한 양자 컴퓨팅 프로토타입은 전략적으로 중요한 미래 틈새 시장을 시사하고 있습니다. 8개의 원자로를 갖춘 300mm 라인의 설비 투자 금액이 1억 2,000만 달러가 넘고, 폴리실리콘 원료 가격의 변동이 겹치면서 소규모 공급업체들은 철수 또는 통합을 강요당하고 있습니다. 기존 기업들은 탄소 발자국에 대한 엄격한 모니터링과 1.5nm 미만의 리소그래피 오버레이 정확도 요건을 충족하기 위해 재생에너지를 이용한 클린룸과 저온 선택적 에피택시 모듈로 전환하고 있습니다.

세계 실리콘 에피택셜 웨이퍼 시장 동향 및 인사이트

300mm 로직 및 메모리 생산 능력 확대에 대한 수요 증가

파운드리 및 반도체 업체들은 2025년부터 2026년까지 TSMC의 피닉스 메가팹, 삼성의 테일러 공장, SK하이닉스의 P&T7 공장 등 신규 300mm 팹에 1,650억 달러를 투자할 것을 약속했습니다. 이 모든 거점들은 2028년까지 연간 5,000만 평방인치 이상의 에피택셜 웨이퍼가 필요하며, 2nm 또는 3nm 로직 웨이퍼의 각 층은 임계값 전압의 편차를 제어하기 위해 엄격하게 조정된 층을 필요로 합니다. 메모리 제조업체들은 고대역폭 메모리의 적층을 12-16층까지 확대하고 있으며, 실리콘 관통전극(TSV) 드릴링 공정에서 휨을 방지하기 위해 응력을 조정한 더 얇은 베이스 웨이퍼를 필요로 하고 있습니다. 로직과 메모리가 결합된 이 파이프라인은 수요의 기준선을 안정화시켜 연마 웨이퍼 수요의 급등과 급락의 패턴으로부터 공급업체를 보호합니다. 인텔과 TSMC의 백사이드 파워 딜리버리(BPD) 로드맵은 직경 300mm 웨이퍼 전체에서 공차를 ±1%까지 더 줄일 수 있습니다.

반도체 소자 미세화, 초저결함 밀도 에피택셜 웨이퍼 수요 견인

3nm에서 등장하여 2nm에서 성숙하는 Gate-all-around 트랜지스터는 허용 결함 밀도를 0.01cm-2 이하로 낮추어 핀 FET 대비 10배 이상 엄격하게 개선되었습니다. 수직 나노시트 스택은 단일 전위로 인한 손상을 증폭시켜 구동 전류를 최대 15%까지 감소시킵니다. 공급업체들은 현재 인시츄 수소 어닐링과 초순수 전구체를 결합하여 설비 투자 부담은 증가하지만 공정 노드 전환이 가능한 공정 노드를 구현하고 있습니다. 전원 레일 및 접지 레일의 설계 규칙이 엄격해짐에 따라 극한의 자외선 노출 시 에피택시로 인한 스트레스로 인한 악영향이 두드러지게 나타나고 있습니다. 이러한 경제적 분화로 인해 프리미엄급 초저결함 제품은 보다 장기적이고 구속력 있는 계약의 등장으로 30-50%의 가격 프리미엄을 얻게 되었습니다.

300mm 에피택시 반응기 및 자동화 설비에 대한 설비 투자 확대

300mm CVD 리액터 1대의 가격은 1,200만-1,500만 달러이며, 신규 라인에는 8-12개의 리액터와 3,000만-5,000만 달러의 자동화 설비가 필요하므로, 클린룸 설치 전 초기 투자금액은 약 1억 5,000만-1억 7,000만 달러에 달할 전망입니다. 000만 달러에 달할 전망입니다. 실트로닉이 2025년 7월에 150mm 생산에서 철수한 사례에서 알 수 있듯이, 소규모 생산업체들은 이 부담을 상각하기 위해 고군분투하고 있습니다. 2024년부터 2025년까지 금리 상승으로 인해 가중평균자본비용(WACC)이 상승했습니다. 이로 인해 일부 확장 계획이 지연되고, 대차대조표상의 현금을 활용할 수 있는 기존 대기업들이 유리한 입장에 서게 되었습니다.

부문 분석

2025년 출하량의 68.49%를 300mm 클래스가 차지하여 최첨단 노드에서의 중심적인 위치를 반영하고, 에피택셜 실리콘 웨이퍼 시장 규모 기준을 확립했습니다. 후면 급전 기술로 층 두께가 15-20% 증가하여 신에츠화학공업과 SUMCO의 리액터 가동률이 향상되었습니다. SEMI는 2023년 이후 평탄도 및 휨(bow) 허용 한계를 30% 강화하여, 공급업체들에게 측정 기술과 공정 제어를 업그레이드할 것을 요구하고 있습니다. 한편, 구식 팹의 리노베이션으로 인해 200mm 수요는 CAGR 4.95%로 계속 확대되고 있으며, 이는 이전 예측과 달리 수요의 종말 추세를 반증하는 결과입니다. 옥메틱(Okmetic)은 2026년 가동 예정인 4억 유로(4억 5,200만 달러) 규모의 반타(Vantaa) 확장 프로젝트를 통해 자동차용 센서 및 혼합 신호 IC용 200mm 생산 능력을 두 배로 늘릴 예정입니다. 한편, 웨이퍼웍스(Wafer Works)와 에피실(Episil)도 200mm 생산량을 확대되고 있습니다. 150mm 이하 시장 규모는 축소되는 추세이지만, 틈새 광전자기기 제조업체는 전문적인 생산 능력을 유지하고 있습니다.

200mm 시장의 모멘텀은 파워 모듈 제조업체들이 실리콘 카바이드(SiC) 게이트 드라이버 및 ADAS 센서 IC용으로 생산라인을 개조하면서 자동차 분야에 크게 견인되고 있습니다. 성숙한 노드 기술에서 중국의 자급자족을 위한 노력도 200mm의 생산량을 더욱 증가시키고 있습니다. 한편, 300mm에 대한 투자는 여전히 아시아태평양에 집중되어 있어 에피택셜 실리콘 웨이퍼 시장에서 아시아태평양의 우위를 확고히 하고 있습니다.

"실리콘 에피택셜 웨이퍼 시장 보고서는 웨이퍼 직경(150mm 이하, 200mm 이상), 반도체 소자 유형(로직, 메모리, 기타), 최종 사용자 산업(가전, 자동차, 산업, 기타), 지역별로 분류되어 있습니다. 분류되어 있습니다. 시장 예측은 수량(평방인치) 단위로 제공됩니다.

지역별 분석

아시아태평양은 2025년 출하량의 80.41%를 차지했으며, 2031년까지 연평균 복합 성장률(CAGR) 5.58%로 확대될 것으로 예측됩니다. 대만이 첨단 로직 생산을 주도하고, 한국이 메모리 시장을 독점하고, 중국의 자급자족 계획이 성숙한 노드에 대한 수요를 증가시키고 있으며, 이 모든 것이 결합되어 이 지역의 에피택셜 실리콘 웨이퍼 시장 규모에서 점유율을 유지하고 있습니다. 일본이 TSMC 구마모토 공장 및 Rapidus에 68억 달러의 지원책을 내놓으면서 국내 공급의 연속성이 확보된 반면, 중국의 수출규제 리스크에 따라 국내 팹의 비축이 진행되고 있습니다. 인도 구자라트 프로젝트는 미래의 발판이 될 것이며, 초기 단계의 웨이퍼는 수입될 것으로 예측됩니다.

북미는 2025년 시장 점유율이 5%대 중반에 머물러 있지만, 'CHIPS and Science Act'의 보조금 혜택을 받고 있습니다. 2025년 5월 가동에 들어간 세계웨이퍼스의 셔먼 공장과 인텔의 오하이오주 메가팹은 2028년까지 연간 1,000만 평방인치 이상 수요를 창출할 것으로 예측됩니다. 유럽은 비용과 인허가 취득에서 뒤쳐져 있지만, 실트로닉의 싱가포르 300mm 라인과 4억 유로(4억 5,200만 달러)의 보조금을 지원받아 2025년 10월 가동에 들어간 세계웨이퍼스의 이탈리아 노바라 공장이 자동차 공급 루트를 공급 루트를 확보하고 있습니다. 남미는 중동, 아프리카와 마찬가지로 수입 의존도가 높아 단기적으로 현지 생산능력 확대 가능성은 제한적일 것으로 보입니다.

지역적 집중은 미국과 유럽에서 전략적 의존도 증가에 대한 우려를 불러일으키고, 보조금 경쟁과 수출 규제를 불러일으키고 있습니다. 그럼에도 불구하고, 아시아태평양의 리액터 도입 실적, 공정 노하우, 클러스터 경제 효과로 인해 향후 10년간 에피택셜 실리콘 웨이퍼 시장에서의 아시아태평양의 우위는 흔들리지 않을 것으로 보입니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The epitaxial silicon wafer market size is projected to expand from 1,938.59 million square inches in 2025, 2,018.27 million square inches in 2026, to 2,516.09 million square inches by 2031, registering a 4.51% CAGR over 2026-2031.

Thicker, ultra-low-defect layers for 300 mm substrates, backside-power-delivery adoption, and rising demand from automotive electrification and on-device AI inference together underpin a durable volume floor. Asia-Pacific's installed reactor base, government subsidies, and memory-capability additions keep regional output dominant, while quantum-computing prototypes on isotopically purified Si-28 layers point to a strategically important future niche. Capital expenditure above USD 120 million for an eight-reactor 300 mm line, coupled with volatile polysilicon feedstock pricing, pushes smaller suppliers to exit or consolidate. Incumbents are moving to renewable-powered cleanrooms and lower-temperature selective-epitaxy modules to satisfy carbon-footprint scrutiny and lithography overlay budgets below 1.5 nm.

Global Silicon Epitaxial Wafer Market Trends and Insights

Rising Demand for 300 mm Logic and Memory Capacity Expansions

Foundries and integrated device makers pledged USD 165 billion to new 300 mm fabs during 2025-2026, including TSMC's Phoenix megafab, Samsung's Taylor facility, and SK Hynix's P&T7 plant. Together, these sites will require more than 50 million square inches of epitaxial wafers annually by 2028, and each 2 nm or 3 nm logic wafer needs a rigorously tuned layer to control threshold-voltage spread. Memory producers are stretching high-bandwidth-memory stacks to 12-16 layers, demanding thinner base wafers with engineered stress to avoid warpage in through-silicon-via drilling. The combined logic-memory pipeline stabilizes baseline demand and shields suppliers from the polished-wafer boom-bust pattern. Intel and TSMC's backside-power-delivery roadmaps further compress tolerance to +-1% across a 300 mm-diameter.

Semiconductor Device Scaling Driving Demand for Ultra-Low-Defect Density Epi Wafers

Gate-all-around transistors debuting at 3 nm and maturing at 2 nm cut the allowable defect density to below 0.01 cm-2, a tenfold tightening compared to fin-FETs. Vertical nanosheet stacks amplify the damage caused by single dislocations, reducing drive current by up to 15%. Suppliers now pair in-situ hydrogen anneals with ultra-high-purity precursors, raising capital intensity but enabling node transitions. Reducing design rules for power and ground rails magnifies the penalty for epi-induced stress during extreme-ultraviolet exposure. The economic split pushes premium ultra-low-defect products to command 30-50% price premiums as stickier, longer contracts emerge.

Escalating Capex for 300 mm Epitaxy Reactors and Automation

A single 300 mm CVD reactor costs USD 12-15 million, and a greenfield line requires 8-12 reactors, plus USD 30-50 million in automation, bringing upfront investment to roughly USD 150-170 million before cleanroom fit-out. Smaller producers struggle to amortize that load, as Siltronic's July 2025 exit from 150 mm production showed. In 2024-2025, rising interest rates led to an increase in the weighted-average cost of capital. This shift resulted in delays for certain expansions and favored established players who could leverage their balance-sheet cash.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Automotive ADAS and Power Electronics Requiring High-Quality Epi Layers

- Government Subsidies for Domestic 300 mm Wafer Fabs in Asia-Pacific

- Volatile Silicon Feedstock Prices Compressing Wafer Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 300 mm class delivered 68.49% of shipments in 2025, reflecting its centrality to leading-edge nodes and setting the baseline for the epitaxial silicon wafer market size. Backside power delivery lifts layer thickness by 15-20%, driving higher reactor utilization at Shin-Etsu and SUMCO. SEMI tightened flatness and bow limits by 30% since 2023, compelling suppliers to upgrade metrology and process control. Conversely, a retrofit wave in older fabs keeps 200 mm demand expanding at a 4.95% CAGR, defying earlier forecasts of terminal decline. Okmetic's EUR 400 million (USD 452 million) Vantaa expansion, operational in 2026, doubled 200 mm capacity to serve automotive sensors and mixed-signal ICs, while Wafer Works and Episil also grew 200 mm output. The 150 mm and smaller pool is shrinking, yet niche optoelectronics players retain specialized capacity.

200 mm momentum is heavily automotive-driven, as power-module makers retrofit lines for silicon-carbide gate drivers and ADAS sensor ICs. China's push for self-sufficiency in mature-node technology further elevates 200 mm volumes. Meanwhile, 300 mm investments stay concentrated in Asia-Pacific, cementing the region's dominance in the epitaxial silicon wafer market.

The Silicon Epitaxial Wafer Market Report is Segmented by Wafer Diameter (Up To 150 Mm, 200 Mm, and More), Semiconductor Device Type (Logic, Memory, and More), End-User Industry (Consumer Electronics, Automotive, Industrial, and More), and Geography. The Market Forecasts are Provided in Terms of Volume (Square Inches).

Geography Analysis

Asia-Pacific commanded 80.41% of 2025 volume and is projected to expand at a 5.58% CAGR through 2031. Taiwan leads advanced-logic output, South Korea dominates memory, and China's self-reliance plan increases mature-node pulls, together underpinning the region's share of the epitaxial silicon wafer market size. Japan's USD 6.8 billion incentive package for TSMC Kumamoto and Rapidus ensures local supply continuity, while China's export-control risks spur stockpiling by domestic fabs. India's Gujarat project adds a future foothold, though initial wafers will be imported.

North America held a mid-single-digit slice in 2025 but benefits from the CHIPS and Science Act grants. GlobalWafers' Sherman plant, opened in May 2025, and Intel's Ohio megafab will together demand more than 10 million square inches a year by 2028. Europe lags on cost and permitting, yet Siltronic's Singapore 300 mm line and GlobalWafers' Novara, Italy site, opened in October 2025 with EUR 400 million (USD 452 million) in subsidies, secure automotive-focused supply routes. South America, along with the Middle East and Africa, remains import-dependent, with limited near-term prospects for indigenous capacity.

Regional concentration raises strategic-dependency alarms in the United States and Europe, prompting subsidy races and export controls. Still, Asia-Pacific's reactor installed base, process know-how, and cluster economics make its dominance in the epitaxial silicon wafer market difficult to dislodge before the next decade.

- Shin-Etsu Handotai Co. Ltd.

- SUMCO Corporation

- GlobalWafers Co. Ltd.

- Siltronic AG

- SK Siltron Co. Ltd.

- Okmetic Oyj

- Wafer Works Corporation

- Poshing Silicon Co. Ltd.

- Simgui Shanghai

- Hebei Semiconductor

- Soitec S.A.

- Episil Technologies Inc.

- MCL Electronic Materials Ltd.

- Siltronix Silicon Technologies

- Advanced Micro-Fabrication Equipment Inc.

- Ferrotec Holdings Corporation

- Topco Scientific Co. Ltd.

- Nova Electronic Materials LLC

- Shenhe Thermo-Magnetics Electronics Co.

- Addison Engineering Inc.

- Virginia Semiconductor Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Value-Chain Analysis

- 4.3 Regulatory Landscape

- 4.4 Impact of Macroeconomic Factors

- 4.5 Technology Analysis

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Market Drivers

- 4.7.1 Semiconductor Device Scaling Driving Demand for Ultra-Low Defect Density Epi Wafers

- 4.7.2 Rising Demand for 300 mm Logic and Memory Capacity Expansions

- 4.7.3 Surge in Automotive ADAS and Power Electronics Requiring High-Quality Epi Layers

- 4.7.4 Government Subsidies for Domestic 300 mm Wafer Fabs in Asia-Pacific

- 4.7.5 Adoption of Backside-Power-Delivery Architectures Boosting Epi Thickness Needs

- 4.7.6 Emergence of Quantum-Computing Qubits on Isotopically Purified Si-28 Epi Layers

- 4.8 Market Restraints

- 4.8.1 Escalating Capex for 300 mm Epitaxy Reactors and Automation

- 4.8.2 Volatile Silicon Feedstock Prices Compressing Wafer Margins

- 4.8.3 Lithography-Induced Pattern Collapse from Epi Stress Mismatches

- 4.8.4 Carbon-Footprint Scrutiny of Energy-Intensive CVD Epitaxy Processes

5 MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1 By Wafer Diameter

- 5.1.1 Up to 150 mm

- 5.1.2 200 mm

- 5.1.3 300 mm

- 5.2 By Semiconductor Device Type

- 5.2.1 Logic

- 5.2.2 Memory

- 5.2.3 Analog

- 5.2.4 Discrete

- 5.2.5 Other Semiconductor Device Types (Optoelectronics, Sensors, Micro)

- 5.3 By End-user

- 5.3.1 Consumer Electronics

- 5.3.1.1 Mobile and Smartphones

- 5.3.1.2 PCs and Servers

- 5.3.2 Industrial

- 5.3.3 Telecommunications

- 5.3.4 Automotive

- 5.3.5 Other End-user Applications

- 5.3.1 Consumer Electronics

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Taiwan

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.5 Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Shin-Etsu Handotai Co. Ltd.

- 6.4.2 SUMCO Corporation

- 6.4.3 GlobalWafers Co. Ltd.

- 6.4.4 Siltronic AG

- 6.4.5 SK Siltron Co. Ltd.

- 6.4.6 Okmetic Oyj

- 6.4.7 Wafer Works Corporation

- 6.4.8 Poshing Silicon Co. Ltd.

- 6.4.9 Simgui Shanghai

- 6.4.10 Hebei Semiconductor

- 6.4.11 Soitec S.A.

- 6.4.12 Episil Technologies Inc.

- 6.4.13 MCL Electronic Materials Ltd.

- 6.4.14 Siltronix Silicon Technologies

- 6.4.15 Advanced Micro-Fabrication Equipment Inc.

- 6.4.16 Ferrotec Holdings Corporation

- 6.4.17 Topco Scientific Co. Ltd.

- 6.4.18 Nova Electronic Materials LLC

- 6.4.19 Shenhe Thermo-Magnetics Electronics Co.

- 6.4.20 Addison Engineering Inc.

- 6.4.21 Virginia Semiconductor Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment