|

시장보고서

상품코드

2063929

PTO 구동 콤바인 수확기 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)PTO Powered Combine Harvesters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

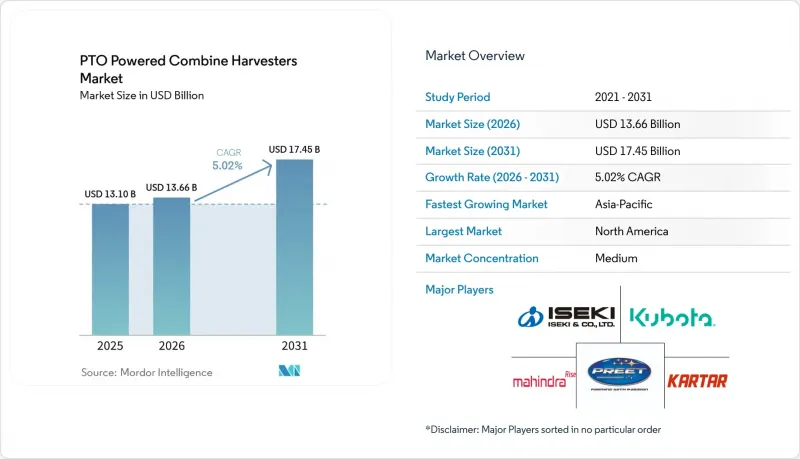

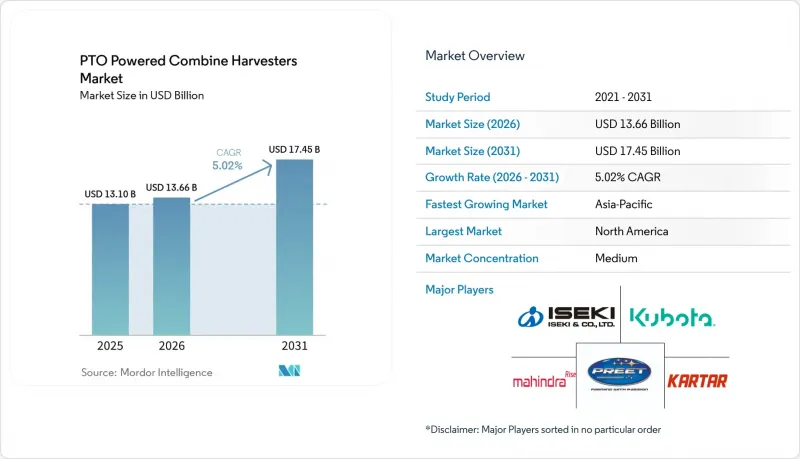

Mordor Intelligence에 의하면, PTO 구동 콤바인 수확기 시장 규모는 2025년 131억 달러로 평가되었고, 2026년 136억 6,000만 달러로 추정되고, 2031년까지 174억 5,000만 달러로 확대될 전망이며, 2026-2031년 CAGR 5.02%를 나타낼 것으로 예측됩니다.

본 보고서는 하위 유형별(표준형, 대용량형, 특수 작물용), 이동 방식별(바퀴식 및 크롤러식), 출력별(150HP 이하, 150-300HP, 300HP 이상), 용도별(밀, 쌀, 기타), 지역별(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

세계의 PTO 구동 콤바인 수확기 시장 동향 및 분석

보조금 중심의 기계화 프로그램

유럽 전역에서 시행되고 있는 농업 기계화 지원 프로그램과 저금리 농업 투자 제도는 설비 투자를 최소화하는 것을 목표로, 기존 트랙터와 호환되는 장비의 도입을 촉진하고 있습니다. 프랑스에서는 유럽 투자 기금과 프랑스 농림부가 2025년 5월에 ‘프랑스 농업 국가 이니셔티브’를 확대했습니다. 투자액이 20억 유로(22억 7,000만 달러)를 넘는 이 계획은 2028년까지 1만 5,000명 이상의 농업 종사자를 지원할 것으로 예측됩니다. 이 대출 프로그램은 농업 기계에 대한 투자와 현대화를 촉진하는 데 중점을 두고 있으며, 농장 및 협동조합이 기계에 대한 접근성을 개선하는 동시에 수확 기계 도입에 따른 재정적 부담을 완화할 수 있도록 지원합니다.

남미에서 렌터카 차량의 급속한 확산

남미 전역에서 농업 기계 대여 및 도급업체를 통한 수확 서비스에 대한 수요가 증가하고 있습니다. 이는 농업 종사자들이 기계 소유보다는 유연한 이용을 우선시하는 경향이 강해지고 있기 때문입니다. 계절적인 수확 수요, 상품 가격 변동, 자체 주행식 기계의 높은 구입 비용 등의 요인이 공동 이용이나 리스 기반 운영 모델의 도입을 촉진하고 있습니다. 임대 플랫폼이나 외부 위탁 기계화 서비스 제공업체를 활용함으로써, 농업 종사자들은 수확 성수기에는 장비 이용률을 극대화하고, 비수기에는 유휴 장비로 인한 비용을 최소화할 수 있습니다. 이러한 추세는 비용 대비 효과가 높고 트랙터와 호환되는 수확 솔루션을 찾는 중소규모 곡물 생산자들 사이에서 특히 두드러지며, 그 결과 지역 농업 시장에서 PTO 구동식 콤바인에 대한 수요가 증가하고 있습니다.

소규모 농지에서 트랙터 출력에 대한 부착 장비 비율의 제약

소규모 농업 종사자가 많은 지역에서는 저마력 트랙터가 널리 사용되고 있기 때문에 안정적이고 효율적인 성능을 발휘하기 위해 높은 엔진 출력이 필요한 대형 PTO 구동 콤바인 수확기와의 운용상 호환성이 제한되고 있습니다. 토지의 세분화와 농업 기계화의 진전이 제한적이기 때문에 특히 중소규모 농업 종사자들에게 있어 대용량 수확용 부착 장치에 대한 투자의 경제적 타당성이 떨어지고 있습니다. 수확기에는 농업 종사자들이 대여한 고출력 트랙터에 의존하는 경우가 많으며, 이로 인해 운영 비용이 증가하여 PTO식 수확 시스템의 비용 이점이 상쇄됩니다. 또한, 저출력 트랙터용으로 설계된 소형 PTO식 수확기 모델은 일반적으로 처리 능력이 낮기 때문에 농번기 동안의 수확 효율과 경작 면적의 커버 범위가 제한됩니다.

부문별 분석

2025년, PTO 구동 콤바인 수확기 시장에서 표준 부문이 46%라는 가장 높은 점유율을 차지했습니다. 이 부문은 아시아태평양, 북미, 유럽의 혼합 곡물 재배 지역에서 널리 사용되고 있는 중형 HP 트랙터와의 폭넓은 호환성을 강점으로 삼고 있습니다. 농업 종사자들은 소유 비용이 저렴하고 유지보수가 용이하며, 기존 트랙터들과 호환성이 뛰어나기 때문에 표준 모델을 선호합니다. 또한, 사후 장착이 가능한 정밀 농업 시스템과 애프터마켓 모니터링 기술의 보급이 확대됨에 따라, 기계의 수명과 운영 효율이 향상되고 있습니다.

대용량 부문은 2026-2031년 연평균 성장률(CAGR) 7.6%라는 가장 높은 성장률을 기록하며 확대될 것으로 전망됩니다. 이러한 수요 증가는 수확 작업 중 곡물 손상을 최소화하는 콩류, 유지종자, 깨지기 쉬운 곡물용 작물별 수확 시스템의 도입 확대에 힘입은 것입니다. 각 제조업체들은 다양한 작물의 조건과 세분화된 농지에 적합한 조정형 탈곡 시스템, 가변식 선별 기술, 소형 수확용 부착 장치를 잇달아 도입하고 있습니다. 심화되는 노동력 부족과 수확 후 손실 감축에 대한 관심이 높아짐에 따라, 특수한 농업 용도로의 도입이 계속해서 확대되고 있습니다.

2025년 기준으로, PTO 구동 콤바인 수확기 시장 점유율의 62%를 바퀴식 시스템이 차지했습니다. 이러한 보급은 도입 비용이 저렴하고, 관리가 용이하며, 주요 곡물 생산 지역의 건조 지대 농지 조건에 적합하기 때문입니다. 농업 종사자들은 뛰어난 도로 주행 성능과 기존 농업 인프라와의 호환성을 이유로 바퀴식 시스템을 선호합니다. 또한, 이 부문은 교체용 부품을 쉽게 구할 수 있다는 점과, 트랙식 시스템에 비해 유지보수가 덜 복잡하다는 장점도 누리고 있습니다. 서스펜션 시스템과 지형 적응성의 발전 덕분에, 상업 농업 분야에서 합리적인 가격을 유지하면서도 작업 효율이 더욱 향상되고 있습니다.

크롤러 방식 시스템은 2026-2031년 연평균 성장률(CAGR) 8.2%로 성장할 것으로 전망됩니다. 이러한 성장은 견인력 향상과 토양 다짐 감소가 필수적인 논 농업 환경에서 이 기술의 도입이 확대됨에 따라 이루어지고 있습니다. 벼 재배 지역의 강우량 변동과 논 건조 기간의 단축으로 인해, 험한 지형에서도 가동 가능한 크롤러식 수확 시스템에 대한 수요가 증가하고 있습니다. 논 재배 지역의 농업 종사자들은 몬순 시즌 동안 수확의 연속성을 확보하고 논에서의 수확 손실을 최소화하기 위해 크롤러식 시스템을 점점 더 많이 도입하고 있습니다.

지역별 분석

북미는 2025년에 PTO 구동 콤바인 수확기 시장 점유율의 31.9%를 차지한 것으로 평가되었습니다. 이러한 성장은 광범위한 농업 기계화, 트랙터 보급률의 높음, 대규모 곡물 생산 지역에서의 수확기 활발한 수요에 기인합니다. 미국과 캐나다의 농업 종사자들은 기상 조건으로 인해 수확 가능 기간이 단축되거나, 계절별 작업의 성수기에 발생하는 긴급한 수확 수요에 대응하기 위해 PTO식 수확 시스템의 도입을 확대되고 있습니다. 캐나다 통계청에 따르면, 2025년 캐나다의 밀 생산량은 3,496만 톤에 달할 것으로 예상되며, 이는 상업용 곡물 생산 분야에서 기계화 수확 솔루션에 대한 수요를 견인하고 있습니다. 또한, 임대 차량의 활발한 운용과 정밀 농업 기술의 보급이 확대되고 있는 점도 지역 전체 농업 부문에서 수확 기기의 활용을 촉진하고 있습니다.

아시아태평양 시장은 농업 기계화의 확대, 농업 인력 부족의 심화, 세분화된 농업 구조 속에서 트랙터 연동형 수확 시스템의 도입 증가에 힘입어 2026-2031년 연평균 성장률(CAGR) 7.9%라는 가장 높은 성장률을 기록하며 확대될 것으로 전망됩니다. 인도나 중국 등의 국가들은 농업 생산성 향상과 수확 후 손실 감소를 목적으로 기계화된 농업 관행을 지속적으로 추진하고 있습니다. 주요 농업 경제권에서 소규모 농지 소유 구조는 기존 트랙터와 호환되는 모듈식 저비용 수확 솔루션을 선호하는 경향이 있습니다. 반자율 제어, 정밀 농업 기술, 소형 수확 플랫폼의 도입 확대 역시 지역적 수요를 뒷받침하고 있습니다. 쌀과 밀의 재배 면적 확대는 아시아태평양 농업 시장 전체에서 수확 장비의 장기적인 도입을 지속적으로 뒷받침하고 있습니다.

남미에서는 생산자들이 초기 소유 비용을 절감하고 계절별 재배 주기에 맞추어 장비를 유연하게 활용하기를 원함에 따라, 도급업체를 통한 수확 및 기계 공유 사업이 지속적으로 확대되고 있습니다. 브라질 국립식량공급공사(CONAB)에 따르면, 2024-2025년 수확기 동안 브라질의 곡물 생산량은 사상 최고치인 3억 5,020만 톤에 달했으며, 주요 곡물 생산 지역 전반에 걸쳐 기계화 수확 능력에 대한 수요가 증가하고 있습니다. 계절적 수확 수요 증가에 따라, 렌탈 업체 및 농업 서비스 제공업체들은 남미 전역에서 트랙터와 호환되는 수확 시스템의 도입을 확대되고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the pTO powered combine harvester market size is projected to grow from USD 13.10 billion in 2025 and USD 13.66 billion in 2026, to USD 17.45 billion by 2031, registering a CAGR of 5.02% from 2026 to 2031.

This report is Segmented by Sub-Type (Standard, High-Capacity, and Specialty-Crop), by Movement Type (Wheel and Crawler), by Power Output (Below 150 HP, 150-300 HP, and Above 300 HP), by Application (Wheat, Rice, and More), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global PTO Powered Combine Harvesters Market Trends and Insights

Subsidy-Led Mechanization Programs

Farm mechanization support programs and low-interest agricultural investment schemes across Europe are promoting the adoption of equipment compatible with existing tractor fleets, aiming to minimize capital expenditure. In France, the European Investment Fund and the French Ministry of Agriculture expanded the National Initiative for French Agriculture in May 2025. This initiative, with an investment volume exceeding EUR 2 billion (USD 2.27 billion), is projected to support over 15,000 farmers by 2028 . The financing program focuses on enhancing agricultural equipment investment and modernization, enabling farms and cooperatives to improve access to machinery while reducing financial barriers to adopting harvesting equipment.

Rapid Rental-Fleet Penetration in South America

The demand for agricultural machinery rental and contractor-based harvesting services is growing across South America as farmers increasingly prioritize flexible equipment access over ownership. Factors such as seasonal harvesting needs, fluctuating commodity prices, and the high acquisition costs of self-propelled machinery are driving the adoption of shared-utilization and lease-based operating models. Rental platforms and outsourced mechanized service providers allow farms to maximize equipment usage during peak harvest periods while minimizing idle machinery costs during off-seasons. This trend is particularly prominent among small and medium-sized grain producers seeking cost-effective, tractor-compatible harvesting solutions, thereby boosting the demand for PTO powered combine harvesters in the regional agricultural market.

High Attachment-to-Tractor Power-Ratio Limits on Small Plots

The prevalent use of low-horsepower tractors in smallholder farming regions restricts the operational compatibility of larger PTO powered combine harvesters, which require higher engine output for stable and efficient performance. Fragmented landholdings and limited farm mechanization reduce the economic viability of investing in high-capacity harvesting attachments, particularly for small and medium-sized farmers. During harvesting periods, farmers often depend on rented higher-horsepower tractors, which increases operational costs and diminishes the cost benefits of PTO based harvesting systems. Furthermore, compact PTO harvester models designed for low-horsepower tractors generally offer lower throughput, limiting harvesting efficiency and acreage coverage during peak agricultural seasons.

Other drivers and restraints analyzed in the detailed report include:

- Hybrid PTO Driveline Retrofits that Cut Fuel

- Predictive-Maintenance IoT Kits Sold as Aftermarket

- Import Tariffs on Gearbox Components

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The standard segment accounted for the largest 46% share of the PTO powered combine harvester market in 2025. This segment benefits from broad compatibility with medium-horsepower tractors, which are widely used in mixed-grain farming regions across Asia-Pacific, North America, and Europe. Farmers prefer standard models due to their lower ownership costs, ease of maintenance, and compatibility with existing tractor fleets. Additionally, the growing availability of retrofit precision farming systems and aftermarket monitoring technologies is enhancing machinery lifecycles and operational efficiency.

The high-capacity segment is projected to grow at the fastest CAGR of 7.6% from 2026 to 2031. Demand growth is supported by rising adoption of crop-specific harvesting systems for pulses, oilseeds, and fragile grains that minimize grain damage during harvesting operations. Manufacturers are increasingly introducing adjustable threshing systems, variable cleaning technologies, and compact harvesting attachments suitable for diverse crop conditions and fragmented agricultural fields. Growing labor shortages and increasing focus on reducing post-harvest losses continue to strengthen adoption across specialty agricultural applications.

Wheel systems accounted for 62% of the PTO powered combine harvester market share in 2025. Their widespread adoption is attributed to lower acquisition costs, easier servicing requirements, and suitability for dryland farming conditions in major grain-producing regions. Farmers prefer wheel systems due to their superior road mobility and compatibility with existing agricultural infrastructure. Additionally, the segment benefits from the strong availability of replacement parts and lower maintenance complexity than tracked systems. Advances in suspension systems and terrain adaptability are further enhancing operational efficiency while preserving affordability for commercial farming operations.

Crawler systems are projected to grow at a CAGR of 8.2% from 2026 to 2031. This growth is driven by increasing adoption in wet-field agricultural conditions, where improved traction and reduced soil compaction are critical. Variability in rainfall and shorter field-drying periods in rice-producing regions are boosting demand for tracked harvesting systems capable of operating in challenging terrain. Farmers in paddy cultivation areas are increasingly adopting crawler systems to ensure harvesting continuity and minimize field losses during monsoon seasons.

Geography Analysis

North America is projected to account for 31.9% of the PTO-powered combine harvester market share in 2025. This growth is attributed to extensive farm mechanization, high tractor penetration, and strong seasonal demand for harvesting in large grain-producing regions. Farmers in the United States and Canada are increasingly adopting PTO harvesting systems to address contingency harvesting needs during compressed weather windows and peak seasonal operations. According to Statistics Canada, Canada's wheat production reached 34.96 million metric tons in 2025, driving demand for mechanized harvesting solutions in commercial grain operations. Additionally, strong rental fleet activity and the growing adoption of precision agriculture technologies are supporting the utilization of harvesting equipment across the regional agricultural sector.

The Asia-Pacific market is projected to grow at the fastest 7.9% CAGR from 2026 to 2031 due to expanding farm mechanization, rising agricultural labor shortages, and increasing adoption of tractor-compatible harvesting systems across fragmented farming structures. Countries such as India and China continue to promote mechanized farming practices to improve agricultural productivity and reduce post-harvest losses. Smaller landholdings in major agricultural economies favor modular and lower-cost harvesting solutions compatible with existing tractor fleets. The growing adoption of semiautonomous controls, precision farming technologies, and compact harvesting platforms is also strengthening regional demand. Expanding rice and wheat cultivation areas continue to support long-term harvesting equipment adoption across Asia-Pacific agricultural markets.

South America continues to witness increasing adoption of contractor-based harvesting and machinery-sharing operations as growers seek lower upfront ownership costs and flexible equipment access during seasonal crop cycles. Brazil's cereal production reached a record 350.2 million metric tons in the 2024-25 harvest season, according to Companhia Nacional de Abastecimento (CONAB), strengthening demand for mechanized harvesting capacity across major grain-producing regions . Rising seasonal harvesting demand is encouraging rental fleet operators and agricultural service providers to expand the deployment of tractor-compatible harvesting systems across South America.

- Kubota Corporation

- ISEKI & CO., LTD.

- Mahindra & Mahindra Ltd.

- Kartar Agro Industries Private Limited

- Preet Agro Industries Private Limited

- Deere & Company

- CNH Industrial N.V.

- AGCO Corporation

- CLAAS KGaA mbH

- SDF S.p.A.

- Yanmar Holdings Co., Ltd.

- Zoomlion Heavy Industry Science and Technology Co., Ltd.

- Rostselmash JSC

- International Tractors Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Subsidy-led mechanization programs

- 4.2.2 Rapid rental-fleet penetration in South America

- 4.2.3 Hybrid PTO driveline retrofits that cut fuel

- 4.2.4 Predictive-maintenance IoT kits sold as aftermarket

- 4.2.5 Emergence of compact crawler PTO harvesters for hilly farms

- 4.2.6 Carbon-credit income for low-emission PTO operations

- 4.3 Market Restraints

- 4.3.1 High attachment-to-tractor power-ratio limits on small plots

- 4.3.2 Scarcity of trained PTO-combine operators

- 4.3.3 Seasonal idle time driving low return-on-investment

- 4.3.4 Import tariffs on gearbox components

- 4.4 Porter's Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Sub-Type

- 5.1.1 Standard

- 5.1.2 High-Capacity

- 5.1.3 Specialty-Crop

- 5.2 By Movement Type

- 5.2.1 Wheel

- 5.2.2 Crawler

- 5.3 By Power Output

- 5.3.1 Below 150 HP

- 5.3.2 150-300 HP

- 5.3.3 Above 300 HP

- 5.4 By Application

- 5.4.1 Wheat

- 5.4.2 Rice

- 5.4.3 Soybean

- 5.4.4 Other Crops

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Turkey

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Kubota Corporation

- 6.4.2 ISEKI & CO., LTD.

- 6.4.3 Mahindra & Mahindra Ltd.

- 6.4.4 Kartar Agro Industries Private Limited

- 6.4.5 Preet Agro Industries Private Limited

- 6.4.6 Deere & Company

- 6.4.7 CNH Industrial N.V.

- 6.4.8 AGCO Corporation

- 6.4.9 CLAAS KGaA mbH

- 6.4.10 SDF S.p.A.

- 6.4.11 Yanmar Holdings Co., Ltd.

- 6.4.12 Zoomlion Heavy Industry Science and Technology Co., Ltd.

- 6.4.13 Rostselmash JSC

- 6.4.14 International Tractors Limited