|

시장보고서

상품코드

2063975

중국의 콤바인 수확기 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)China Combine Harvesters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

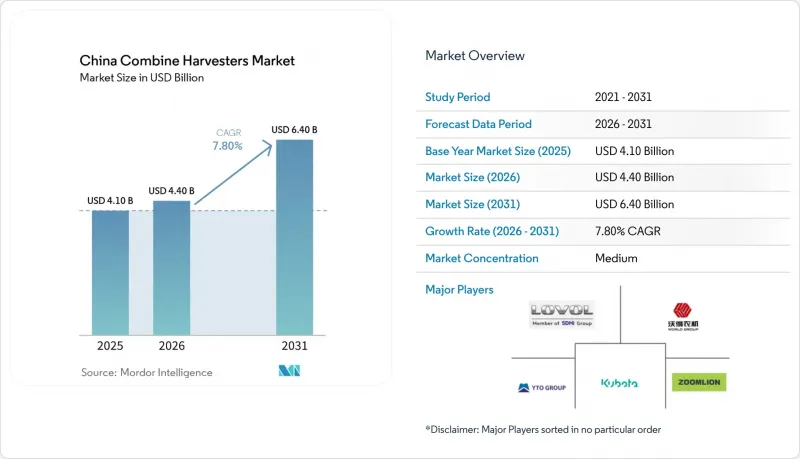

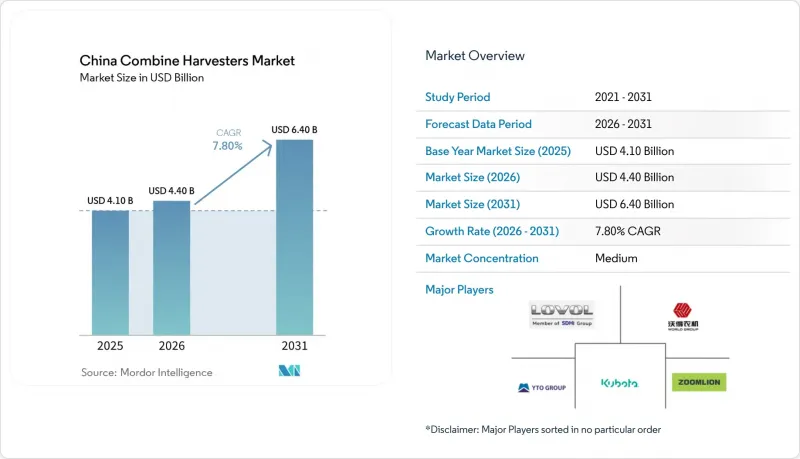

Mordor Intelligence에 의하면, 중국의 콤바인 수확기 시장 규모는 2025년에 41억 달러로 평가되었고, 2026년에는 44억 달러로 추정되고, 2031년까지 64억 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 7.8%로 성장할 전망입니다.

본 보고서는 유형별(자주식, 트랙터 견인식, PTO 구동식 모듈형 콤바인), 출력 범위별(120마력 미만, 120-200마력, 201-300마력 및 그 이상), 동향별(바퀴식 및 크롤러식)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

중국의 콤바인 수확기 시장 동향 및 인사이트

보조금을 통한 기계화 추진

중국의 2026년도 농업기계 구입 기금은 33억 3,000만 달러로 확대되어, 2024년 대비 10.7% 증가했습니다. 또한, 고수확량 콤바인에 대한 보조율은 기존 기종의 30%에서 35-40%로 인상되었습니다. 산시성은 초당 6kg의 처리 능력을 갖춘 크롤러식 모델에 대한 보조금 상한선을 5,250달러에서 6,300달러로 인상하여, 탄젠셜 드럼식 장치의 퇴출을 가속화했습니다. 면화 수확기는 현재 1만 1,200달러의 보조금 지원 대상이며, 지원 범위가 주요 곡물을 넘어 확대되고 있는 것으로 확인되었습니다. 2024-2026년 카탈로그에서는 보조금 수령 자격 요건으로 베이두(BeiDou) 수신기와 손실 센서의 탑재가 의무화됨에 따라, 제조업체들은 텔레매틱스 기능을 기본 사양으로 장착할 수밖에 없게 되었습니다. 헤이룽장성에서는 65만 헥타르에 걸쳐 북두 유도식 수확기를 도입하여, 중복으로 인한 낭비를 최대 12% 줄였습니다. 장쑤성의 농업협동조합은 실시간 수확량 매핑 기능을 갖춘 3,000대를 도입하여, 이를 바탕으로 가변 시비를 실시했습니다. 이러한 일련의 정책 덕분에 250마력 기계의 투자 회수 기간이 6년에서 4년으로 단축되었으며, 이는 연간 출하 대수의 직접적인 증가와 교체 주기의 가속화로 이어지고 있습니다.

농촌 지역의 노동력 부족과 인건비 급등

60세 이상 농촌 주민의 비율은 2005년 9.55%에서 2021년에는 18.57%로 상승했으며, 2030년까지 30%를 나타낼 것으로 예측됩니다. 루펑 지역의 수작업 수확 근로자들의 일당은 2024년에 17달러까지 상승하였고, 2020년 대비 35% 증가했습니다. 기계화 서비스 요금은 0.067헥타르당 8-11달러이며, 이를 통해 소규모 농가에서는 0.067헥타르당 42달러를 순절감할 수 있습니다. 인증된 수확기 운전자는 1,170만 명인 반면, 기계 조작 인력은 5,010만 명으로, 기술 격차가 확대되고 있습니다. 허베이성의 문안협동조합은 15대의 콤바인에 톱니 모양의 체를 추가로 장착하여 곡물 손실률을 0.85%로 낮췄습니다. 내몽골의 나이만 기에서는 75,133.3헥타르를 452개의 협동조합으로 통합하여, 40대의 콤바인으로 구성된 기계군이 600헥타르 단위의 구획을 작업할 수 있도록 했습니다. 농가의 연령 중앙값이 55세를 넘고, 도시로의 이주로 인해 젊은 노동력이 감소하는 가운데, 기계화는 치솟는 인건비에 대한 유일한 현실적인 대책이 되고 있습니다.

높은 기계 도입 비용과 자금 조달 부족

자주식 200-300마력 콤바인의 보조금 적용 전 가격은 2만 8,000-4만 9,000달러로, 이는 1.33헥타르를 경작하는 가구의 3-5년 치 순농업소득에 해당합니다. 보조금 환급은 구매 후 최대 6개월까지 지연되기 때문에 가교 자금에 의존할 수밖에 없습니다. 농촌신용조합의 금리는 4.5-6.0%이지만, 담보 규정에 따라 신청자의 최대 절반은 이용할 수 없습니다. 정저우 중롄의 4LZ-9B 모델 정가는 2만 5,200-3만 800달러이지만, 6,800달러의 보조금을 받은 후에도 실질적인 지출액은 평균 가구 가처분 소득의 40%를 상회합니다. 리스 보급률은 15% 미만으로, 북미의 40%와 비교하면 낮은 수준입니다. Weichai Lovol 산하의 Feidi Leasing과 Zoomlion Financial은 계약금 4,200달러, 월 1,100달러의 24개월 할부 상품을 제공하고 있지만, 이용률은 10% 미만에 그치고 있습니다. 300마력을 넘는 모델의 경우 부담이 더욱 커지며, 가격은 8만 4,000달러에 달할 전망입니다. 그 때문에 특히 시범 운영 구역 이외의 지역에서는 자금 부족으로 인해 차량 교체 시기가 늦어지고 있습니다.

부문별 분석

2025년, 중국 콤바인 수확기 시장 규모의 64%를 자가주행식 콤바인이 차지했으며 가장 큰 점유율을 기록했습니다. 실내가 넓고 진동이 적어 고령의 운전자가 선호하는 선택지입니다. 듀얼 축류 구조는 1.2%라는 손실 상한을 충족하며, 접선 드럼 방식에 비해 15-20% 더 높은 처리 능력을 발휘합니다. 수확량이 절반으로 줄어드는 벼 수확기는 처리 능력이 40% 저하되지만, 볏짚을 남겨두는 논에서는 여전히 사용되고 있습니다. 트랙터 견인형 부문은 2031년까지 연평균 성장률(CAGR) 8.9%로 확대될 것으로 예측되며, 다른 부문을 웃도는 성장이 예상됩니다. 이는 가격이 11,200-1만 6,800달러인 트랙터 견인형 기계가 쓰촨성의 좁은 계단식 논에서 여전히 유용하기 때문입니다. 전용 수확기를 사용하기에는 경제성이 떨어지는 유채나 땅콩 재배지에서는 PTO 모듈러 키트의 도입이 확대되고 있습니다. 자주식 기계로의 전환은 중국 콤바인 수확기 시장이 연구개발 자금의 대부분을 어디에 투자하고 있는지를 여실히 보여주고 있습니다.

자주식 모델로의 전환은 스마트 콤바인에 대한 보조금 정책과도 부합합니다. 2025년에 출하된 북두(BeiDou) 탑재 기기의 70%는 사후 장착이 아닌 공장 출하 시에 이미 장착되어 있었습니다. 300-800헥타르를 관리하는 협동조합들 사이에서는 고액의 초기 투자를 정당화할 수 있기 때문에 장비 교체 의향이 가장 높습니다. 트랙터 견인형 모델은 여전히 초급 수준의 기계화를 뒷받침하고 있지만, 조작성이 떨어지는 점이 작업자의 관심을 저해하고 있습니다. 모듈식 키트는 기존 트랙터에 유연하게 장착할 수 있다는 장점이 있지만, 작물 밀도가 높은 밀밭에서는 한계가 있습니다. 보조금 동향과 더욱 엄격해진 손실 기준을 고려할 때, 중국의 콤바인 수확기 시장은 고사양 자가주행 섀시 쪽으로 돌이킬 수 없이 기울고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the china combine harvester market size expanded to USD 4.1 billion in 2025 and is projected to reach USD 4.4 billion in 2026, and USD 6.4 billion by 2031, growing at a CAGR of 7.8% from 2026 to 2031.

This report is Segmented by Type ( Self-Propelled, Tractor-Pulled, and PTO-Powered Modular Combines), by Power Range (Less Than 120 HP, 120-200 HP, 201-300 HP, and More), and by Movement ( Wheel Type and Crawler Type). The Market Forecasts are Provided in Terms of Value (USD).

China Combine Harvesters Market Trends and Insights

Subsidy-Backed Mechanization Push

China's 2026 machinery purchase fund grew to USD 3.33 billion, a 10.7% increase over 2024, and high-feed-rate combines now receive 35-40% reimbursement, up from 30% for legacy machines. Shaanxi lifted the subsidy ceiling for six-kilogram-per-second tracked models from USD 5,250 to USD 6,300, accelerating the retirement of tangential-drum units. Cotton pickers now qualify for USD 11,200, confirming that support extends beyond staple grains. The 2024-2026 catalog also links eligibility to BeiDou receivers and loss sensors, forcing manufacturers to bundle telematics. Heilongjiang deployed BeiDou-guided harvesters across 650,000 hectares, trimming overlap waste by up to 12%. Jiangsu cooperatives installed 3,000 units with live yield mapping, which informs variable-rate fertilization. This policy suite cuts payback from 6 to 4 years for 250-horsepower machines, directly boosting annual shipments and speeding up replacement cycles.

Rural Labor Shortage and Rising Wage Costs

The share of rural residents aged 60 and above climbed from 9.55% in 2005 to 18.57% in 2021 and is forecast to hit 30% by 2030. Daily wages for manual harvesters in Lufeng rose to USD 17 in 2024, up 35% from 2020. Mechanized services charge USD 8-11 per 0.067 hectares, resulting in a net saving of USD 42 per 0.067 hectares for smallholders. Certified harvester operators stand at 11.7 million, while the machinery workforce is 50.1 million, widening the skills gap. Wen'an Cooperative in Hebei retrofitted 15 combines with serrated sieves, reducing grain loss to 0.85%. Inner Mongolia's Naiman Banner consolidated 75,133.3 hectares into 452 cooperatives, allowing fleets of 40 combines to serve 600-hectare blocks. As the median farmer age surpasses 55 and urban migration drains young workers, mechanization becomes the only feasible hedge against escalating labor costs.

High Upfront Machine Cost and Credit Gaps

Self-propelled 200-300 horsepower combines cost USD 28,000-49,000 before subsidy, which is equivalent to three to five years of net farm income for households tilling 1.33 hectares. Subsidy reimbursement lags purchase by up to six months, forcing reliance on bridge loans. Rural credit unions charge 4.5-6.0% interest, yet collateral rules exclude up to half of applicants. Zhengzhou Zhonglian's 4LZ-9B lists at USD 25,200-30,800; after a USD 6,800 subsidy, the net outlay still exceeds the average household disposable income by 40%. Leasing penetration is below 15%, compared with 40% in North America. Weichai Lovol's Feidi Leasing and Zoomlion Financial offer 24-month plans with a USD 4,200 down payment and USD 1,100 monthly payments, yet uptake is under 10%. The burden is steeper for models with more than 300 horsepower, costing USD 84,000. Financial constraints, therefore, slow fleet renewal, especially outside pilot zones.

Other drivers and restraints analyzed in the detailed report include:

- National Food-Security Agenda Elevating Grain-Loss Standards

- BeiDou-Enabled Smart-Harvester Subsidy Incentives

- Fragmented Land Holdings Limit Large-Machine Utility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Self-propelled combines captured 64% of the China combine harvester market size in 2025, representing the largest share. Wider cabs and lower vibration make them the preferred choice for aging operators. Dual-axial-flow architectures meet the 1.2% loss ceiling and deliver 15-20% higher throughput than tangential drums. Half-feed rice persists in straw-retention paddies, though at a 40% throughput penalty. The tractor-pulled segment is projected to expand at a CAGR of 8.9% through 2031, outpacing other segments, as tractor-pulled units, priced at USD 11,200-16,800, remain relevant for Sichuan's narrow terraces. PTO modular kits are gaining traction in rapeseed and peanut plots where dedicated harvesters are uneconomical. The pivot to self-propelled machines underscores where the China combine harvester market will direct most R&D funding.

Self-propelled adoption also aligns with smart-harvester subsidies; 70% of BeiDou-equipped units shipped in 2025 were factory-installed rather than retrofitted. Replacement intent is strongest among cooperatives managing 300-800 hectares that can justify the higher outlay. Tractor-pulled models still anchor entry-level mechanization, yet a lack of comfort stalls operator interest. Modular kits benefit from flexible deployment on existing tractors but face limits in heavy wheat stands. Given subsidy bias and stricter loss norms, the China combine harvester market is tilting irrevocably toward high-spec self-propelled chassis.

List of Companies Covered in this Report:

- Weichai Lovol Intelligent Agricultural Technology CO., LTD

- Jiangsu World Agriculture Machinery Co., Ltd.

- China First Tractor Group (YTO Group)

- Zoomlion Heavy Industry Science & Technology Co., Ltd.

- KUBOTA Corporation

- Deere & Company

- CNH Industrial N.V.

- AGCO Corporation

- CLAAS KGaA mbH

- Shandong Shifeng Group

- Zhengzhou Zhonglian Harvest Machinery

- Zhejiang Liulin Agricultural Equipment

- Xingguang Agricultural Machinery

- Rostselmash

- Sampo Rosenlew

- Yanmar Co., Ltd.

- Shandong Wuzheng Group

- Preet Agro Industries

- Iseki & Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Subsidy-backed mechanization push

- 4.2.2 Rural labor shortage and rising wage costs

- 4.2.3 National food-security agenda elevating grain-loss standards

- 4.2.4 BeiDou-enabled smart-harvester subsidy incentives

- 4.2.5 Stricter grain-loss quotas for state grain procurement

- 4.2.6 Land-consolidation pilot zones demanding high-HP machines

- 4.3 Market Restraints

- 4.3.1 High upfront machine cost and credit gaps

- 4.3.2 Fragmented land holdings limit large-machine utility

- 4.3.3 Harvest-window compression causing seasonal over-capacity

- 4.3.4 China VI non-road diesel compliance costs

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Buyers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 Self-propelled

- 5.1.1.1 Full-feed axial-flow

- 5.1.1.2 Full-feed tangential-drum

- 5.1.1.3 Half-feed rice combines

- 5.1.2 Tractor-pulled (trailing)

- 5.1.3 PTO-powered modular combines

- 5.1.1 Self-propelled

- 5.2 By Power Range (HP)

- 5.2.1 Less than 120 HP

- 5.2.2 120 - 200 HP

- 5.2.3 201 - 300 HP

- 5.2.4 More than 300 HP

- 5.3 By Movement

- 5.3.1 Wheel Type

- 5.3.1.1 Two-wheel-drive

- 5.3.1.2 Four-wheel-drive

- 5.3.2 Crawler Type

- 5.3.2.1 Rubber-track crawlers

- 5.3.2.2 Steel-track crawlers

- 5.3.1 Wheel Type

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Weichai Lovol Intelligent Agricultural Technology CO., LTD

- 6.4.2 Jiangsu World Agriculture Machinery Co., Ltd.

- 6.4.3 China First Tractor Group (YTO Group)

- 6.4.4 Zoomlion Heavy Industry Science & Technology Co., Ltd.

- 6.4.5 KUBOTA Corporation

- 6.4.6 Deere & Company

- 6.4.7 CNH Industrial N.V.

- 6.4.8 AGCO Corporation

- 6.4.9 CLAAS KGaA mbH

- 6.4.10 Shandong Shifeng Group

- 6.4.11 Zhengzhou Zhonglian Harvest Machinery

- 6.4.12 Zhejiang Liulin Agricultural Equipment

- 6.4.13 Xingguang Agricultural Machinery

- 6.4.14 Rostselmash

- 6.4.15 Sampo Rosenlew

- 6.4.16 Yanmar Co., Ltd.

- 6.4.17 Shandong Wuzheng Group

- 6.4.18 Preet Agro Industries

- 6.4.19 Iseki & Co.