|

시장보고서

상품코드

2072751

북미의 콤바인 수확기 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)North America Combine Harvesters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

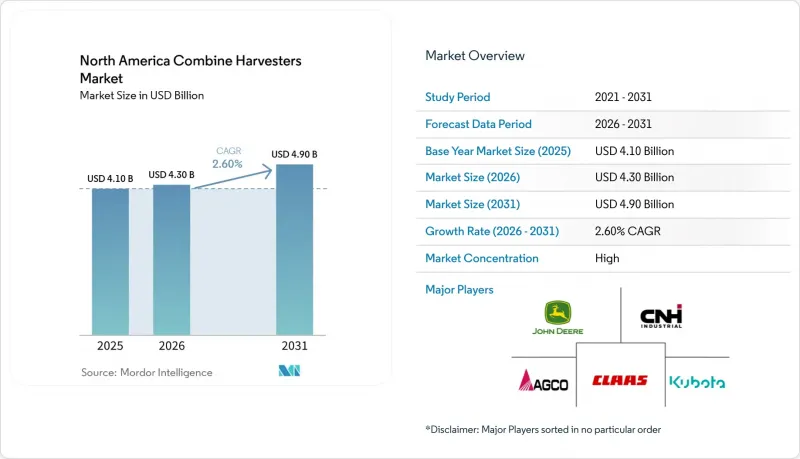

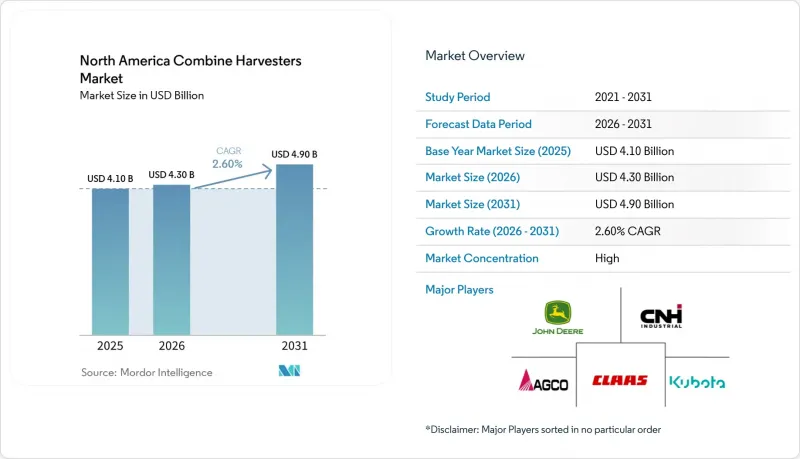

Mordor Intelligence에 의하면, 북미의 콤바인 수확기 시장 규모는 2025년 41억 달러로 평가되었고, 2026년 43억 달러로 추정되고, 2031년까지 49억 달러로 확대될 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR)은 2.60%를 나타낼 전망입니다.

본 보고서는 제품 유형별(기존 스트로워커식 콤바인, 로터리식 콤바인, 하이브리드식 콤바인 및 크롤러식 콤바인), 출력 등급별(200 HP 미만, 200-300 HP, 300-400 HP 및 400 HP 이상), 국가별(미국, 캐나다, 멕시코 및 기타 북미)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

북미의 콤바인 수확기 시장 동향 및 분석

인건비 급등과 노동력 부족

세계은행의 데이터가 보여주듯이, 농업 종사자 수의 감소로 인해 대규모 곡물 농장에서의 완전 기계화 도입이 가속화되고 있습니다. 농업 종사자 수는 2024년 1.56%에서 2025년에는 1.52%로 감소했습니다. 2024년, Deere &Company사는 수확의 일관성, 생산성 및 조작 편의성을 향상시키기 위해 '예측 지상 속도 자동화' 기능과 자동 수확 설정을 갖춘 S7 시리즈 콤바인을 발표했습니다. 노스다코타주, 몬태나주, 서스캐처원주, 앨버타주 등의 지역에서는 시간당 임금이 높은데도 불구하고 심각한 노동력 부족에 직면해 있습니다. 이로 인해 임금 인플레이션이 발생하고, 자율형 및 반자율형 콤바인의 투자 수익률이 높아지면서, 결과적으로 노동 수요 감소로 이어지고 있습니다. 고도의 자동화 기능을 탑재한 콤바인의 리스 계약률이 상승하고 있으며, 이는 인력 요구 사항을 최소화하는 기능에 대한 투자 의지를 반영하고 있습니다. 그 결과, 노동력 제약이 프리미엄 가격 책정을 촉진하며, 북미의 콤바인 수확기 시장에서 첨단 기술로의 지속적인 전환을 뒷받침하고 있습니다.

정밀 농업의 도입 및 통합

콤바인 수확기는 위치 정보가 포함된 수확량, 수분, 단백질 등의 측정값을 클라우드 대시보드로 스트리밍하는 '이동식 데이터센터'로 진화했습니다. 디아사의 '2025 SmartPan' 통합 기능은 트럭이 엘리베이터에 도착하기 전에 곡물 품질 분석 결과를 제공함으로써, 운영자를 해당 회사의 생태계에 안정적으로 정착시키고 있습니다. 체서피크만과 오대호 지역에서 미국 환경보호청(EPA)의 영양염 관리 규정 등 규제 요인으로 인해, 추적 가능한 농업 데이터에 대한 수요가 증가하고 있습니다. 내장형 분석 기능은 가변 비료 시비 계획도 지원하며, 수확과 투입 자재의 시비 간의 연계를 완성합니다. 이러한 시너지 효과로 인해 장비에 대한 충성도이 높아지고, 교체 비용이 증가하여 북미 콤바인 수확기 시장의 장기적인 성장 기반이 되고 있습니다.

첨단형 콤바인의 높은 초기 투자 비용

첨단 콤바인의 높은 초기 투자 비용은 북미 콤바인 수확기 시장을 현저히 제약하고 있으며, 특히 미국 농업 경영의 90%를 차지하는 중소규모 농장에 큰 영향을 미치고 있습니다. AGCO 코퍼레이션은 2024년 3분기 순매출이 약 25억 달러였습니다고 보고했는데, 이는 농업 경영의 이익률 축소로 인해 생산자들이 기계 구매를 미루면서 농기계 수요가 부진해져 전년 동기 대비 감소한 것을 반영한 것입니다. 소규모 농업 경영자들은 중고 농기계나 계절별 대여를 점점 더 선호하는 추세이며, 이로 인해 교체 주기가 길어지고 있습니다. 멕시코에서는 농장의 평균 규모가 500에이커 미만이기 때문에 아직 발전 단계에 있는 협동조합 모델이 없다면 신형 기계를 도입하는 것은 경제적으로 타당하지 않은 상황입니다. 이러한 추세는 해당 지역의 소규모 농업 경영자들이 직면한 경제적 제약을 해결하기 위해, 장비 공유나 리스 같은 대안적인 소유 모델의 중요성이 커지고 있음을 여실히 보여주고 있습니다.

부문별 분석

로터리식 콤바인은 수분 함량이 높은 옥수수를 처리하는 뛰어난 성능 덕분에 2025년에는 북미 콤바인 수확기 시장의 65%를 차지하며 최대 시장 부문을 주도했습니다. 기존의 스트로워커식 모델은 건조한 밀 재배 지역에서 여전히 사용되고 있지만, 재배 면적이 옥수수나 대두로 전환됨에 따라 그 점유율은 줄어들고 있습니다. AGCO사의 'Gleaner' 시리즈가 선도하는 하이브리드 구조는 다양한 품목에 대응할 수 있는 유연성이 필요한 수확 도급업자들 사이에서 작은 틈새 시장을 차지하고 있습니다. 로터리식 콤바인의 우위는 유지될 전망이지만, 경쟁의 초점은 플랫폼의 범용성으로 옮겨가고 있으며, 각 OEM 업체들은 농가가 4시간 이내에 바퀴와 크롤러를 교체할 수 있는 퀵 어태치식 액슬 키트를 추가하고 있습니다.

크롤러식 콤바인은 가장 빠르게 성장하고 있으며, 2026-2031년 연평균 성장률(CAGR) 7.8%라는 최고 수준을 기록할 것으로 전망됩니다. 이는 비가 많이 내리는 가을로 인해 수확 기간이 단축되고 토양 다짐의 위험이 높아지는 상황에서도, 다른 모든 제품 유형을 능가하는 성장률입니다. 크롤러식 장비에 대한 수요 증가는 주로 점토질 토양이 급속히 포화되는 노스다코타주, 미네소타주 및 캐나다 동부 지역에서 비롯되고 있습니다. 접지 면적이 넓어지면 접지압이 감소하여, 봄철 파종을 위한 토양의 경작 상태가 유지됩니다. 또한, 운영자들은 트랙식 콤바인의 높은 재판매 가격을 높이 평가하고 있으며, 이로 인해 바퀴식 콤바인과의 총 소유 비용 차이가 줄어들고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the north america combine harvesters market size is projected to expand from USD 4.10 billion in 2025 and USD 4.30 billion in 2026 to USD 4.90 billion by 2031, registering a CAGR of 2.60% between 2026 and 2031.

This report is Segmented by Product Type (Conventional Straw-Walker Combines, Rotary Combines, Hybrid Combines, and Tracked Combines), by Power Class (Below 200 HP, 200 To 300 HP, 300 To 400 HP, and Above 400 HP), by Country (United States, Canada, Mexico, and Rest of North America). The Market Forecasts are Provided in Terms of Value (USD).

North America Combine Harvesters Market Trends and Insights

Rising Labor Costs and Labor Shortages

A decline in agricultural employment is accelerating the adoption of full mechanization across large grain farms, as indicated by World Bank data. Employment in agriculture decreased to 1.52% in 2025, compared to 1.56% in 2024. In 2024, Deere & Company introduced the S7 Series combines featuring Predictive Ground Speed Automation and automated harvest settings to improve harvesting consistency, productivity, and ease of operation. Regions such as North Dakota, Montana, Saskatchewan, and Alberta are experiencing significant labor shortages despite high hourly wages. This has led to wage inflation, enhancing the return on investment for autonomous and semi-autonomous harvesters, thereby reducing labor demand. Leasing rates for combines equipped with advanced automation are increasing, reflecting a willingness to invest in features that minimize workforce requirements. Consequently, labor constraints are driving premium pricing and supporting the ongoing shift toward advanced technology in the North America combine harvesters market.

Precision-Agriculture Adoption and Integration

Combines have evolved into rolling data centers that stream location-tagged yield, moisture, and protein metrics to cloud dashboards. Deere's 2025 SmartPan integration delivers grain-quality analytics before the truck reaches the elevator, locking operators into its ecosystem. Regulatory drivers such as the Environmental Protection Agency (EPA) nutrient-management rules in the Chesapeake Bay and Great Lakes regions heighten demand for traceable agronomic data. Embedded analytics also support variable-rate fertilizer planning, closing the loop between harvest and input application. These synergies intensify equipment stickiness, raise switching costs, and underpin long-run growth for the North America combine harvesters market.

High Upfront Capital Costs for Advanced Combines

High upfront capital costs for advanced combine harvesters significantly constrain the North America combine harvesters market, particularly impacting small and medium-sized farms, which constitute 90% of farming operations in the United States. AGCO Corporation reported approximately USD 2.5 billion in net sales in Q3 2024, reflecting a year-over-year decline amid weaker agricultural equipment demand as growers delayed machinery purchases because of tighter farm margins. Smaller operators increasingly favor used units or seasonal rentals, lengthening upgrade cycles. In Mexico, the average farm size is below 500 acres, rendering new machines uneconomical without cooperative models that are still nascent. This trend underscores the growing importance of alternative ownership models, such as equipment sharing and leasing, to address the economic constraints faced by smaller farming operations in the region.

Other drivers and restraints analyzed in the detailed report include:

- Government Subsidies and Preferential Financing

- Original Equipment Manufacturer (OEM) Subscription-Based Autonomous Software Upgrades

- Rural Connectivity Gaps Limiting Real-Time Telematics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rotary combines led the largest segment, with 65% of the North America combine harvesters market share in 2025, owing to superior throughput in high-moisture corn. Conventional straw-walker models persist in drier wheat belts, but their share erodes as acreage tilts toward corn and soybeans. Hybrid architectures, championed by AGCO's Gleaner line, capture a small niche among custom harvesters that need multi-crop flexibility. Rotary dominance will remain intact, but the competitive narrative is shifting toward platform versatility, with Original Equipment Manufacturer (OEM) adding quick-attach axle kits that let growers convert between wheels and tracks in under four hours.

Tracked combines are the fastest-growing, forecast to post the fastest 7.8% CAGR through 2026 to 2031, outpacing all other product types as wetter autumns shorten harvest windows and soil-compaction risk climbs. Rising demand for tracks comes primarily from North Dakota, Minnesota, and eastern Canada, where clay soils saturate quickly. Larger contact patches lower ground pressure, preserving soil tilth for spring planting. Operators also value higher resale prices for tracked units, narrowing total cost-of-ownership gaps with wheeled alternatives.

Complete Report Scope:

- By Product Type

- Conventional Straw-Walker Combines

- Rotary Combines

- Hybrid Combines

- Tracked Combines

- By Power Class

- Below 200 HP

- 200 to 300 HP

- 300 to 400 HP

- Above 400 HP

- By Country

- United States

- Canada

- Mexico

- Rest of North America

List of Companies Covered in this Report:

- Deere & Company

- Case IH Agriculture

- CNH Industrial N.V.

- AGCO Corporation

- CLAAS KGaA mbH

- Kubota Corporation

- Rostselmash Joint-Stock Co.

- Sampo Rosenlew Oy

- Yanmar Holdings Co., Ltd.

- Same Deutz-Fahr Italia S.p.A.

- TRIBINE Harvester LLC

- Zoomlion Heavy Industry Science & Technology Co., Ltd.

- Oxbo International Corporation

- Preet Tractors Private Ltd.

- ISEKI & Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising labor costs and labor shortages

- 4.2.2 Precision-agriculture adoption and integration

- 4.2.3 Government subsidies and preferential financing

- 4.2.4 Accelerated fleet-replacement cycles on large farms

- 4.2.5 Original Equipment Manufacturer (OEM)subscription-based autonomous software upgrades

- 4.2.6 Interoperability standards for grain cart-combine automation

- 4.3 Market Restraints

- 4.3.1 High upfront capital costs for advanced combines

- 4.3.2 Commodity-price volatility impacting farm cash flow

- 4.3.3 Semiconductor and hydraulic component supply-chain constraints

- 4.3.4 Rural connectivity gaps limiting real-time telematics

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Conventional Straw-Walker Combines

- 5.1.2 Rotary Combines

- 5.1.3 Hybrid Combines

- 5.1.4 Tracked Combines

- 5.2 By Power Class

- 5.2.1 Below 200 HP

- 5.2.2 200 to 300 HP

- 5.2.3 300 to 400 HP

- 5.2.4 Above 400 HP

- 5.3 By Country

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Mexico

- 5.3.4 Rest of North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market-level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for key Companies, Products and Services, and Recent Developments)

- 6.4.1 Deere & Company

- 6.4.2 Case IH Agriculture

- 6.4.3 CNH Industrial N.V.

- 6.4.4 AGCO Corporation

- 6.4.5 CLAAS KGaA mbH

- 6.4.6 Kubota Corporation

- 6.4.7 Rostselmash Joint-Stock Co.

- 6.4.8 Sampo Rosenlew Oy

- 6.4.9 Yanmar Holdings Co., Ltd.

- 6.4.10 Same Deutz-Fahr Italia S.p.A.

- 6.4.11 TRIBINE Harvester LLC

- 6.4.12 Zoomlion Heavy Industry Science & Technology Co., Ltd.

- 6.4.13 Oxbo International Corporation

- 6.4.14 Preet Tractors Private Ltd.

- 6.4.15 ISEKI & Co., Ltd.