|

시장보고서

상품코드

2063963

스페인의 컨테이너보드 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Spain Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

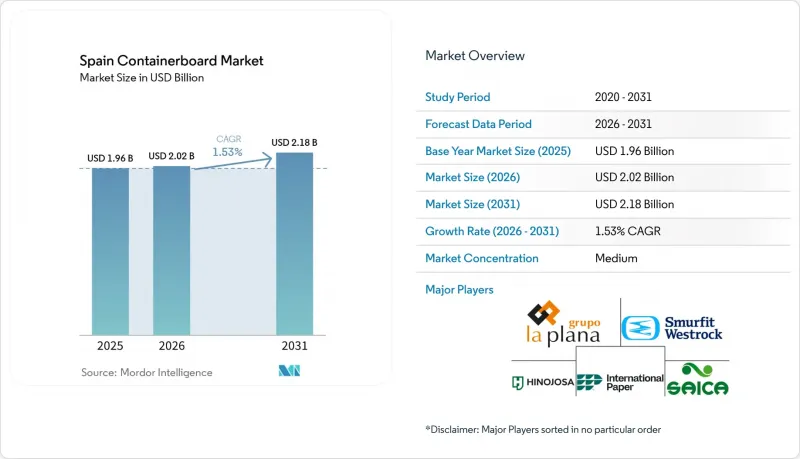

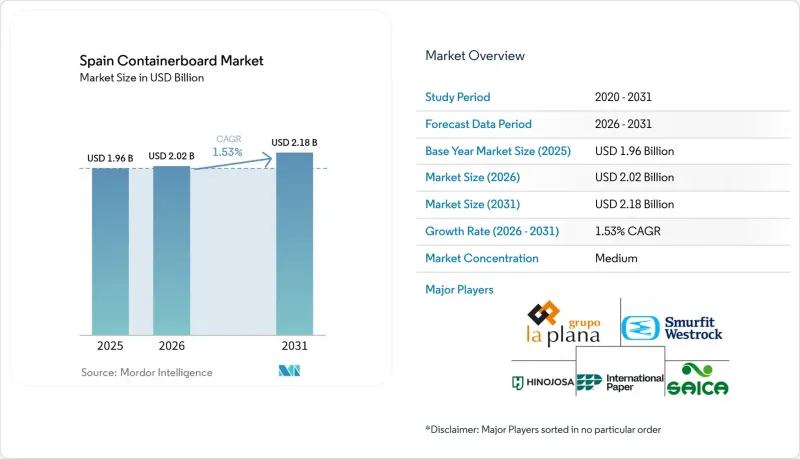

Mordor Intelligence에 의하면, 스페인 컨테이너보드 시장 규모는 2025년에 19억 6,000만 달러로 평가되었고 2026년 20억 2,000만 달러에서 2031년까지 21억 8,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 1.53%를 나타낼 전망입니다.

본 보고서는 원료(버진 섬유 및 재생 섬유), 제품 유형(크래프트 라이너, 테스트 라이너, 플루팅), 그리고 최종 사용자 산업(식품 및 음료, 소비재, 산업용, 기타)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

스페인 컨테이너보드 시장 동향 및 인사이트

식품 수출 및 신선식품용 골판지 수요

스페인의 농산물·식품 수출 기반 덕분에, 스페인의 컨테이너보드 시장은 신선식품의 무역 흐름과 밀접하게 연결되어 있습니다. 2025년에는 신선 과일 및 채소의 수출액이 186억 6,600만 유로(202억 달러)에 달했습니다. 이는 출하량이 4% 감소했음에도 불구하고 달성된 성과로, 고부가가치 품목이 운송 단위당 포장 가치 밀도를 끌어올렸음을 보여줍니다. 2025년, 안달루시아 주는 국내 과일 및 채소 수출량의 33%를 차지하고, 발렌시아 주는 28%를 차지하고 있어, 두 지역은 골판지 수요의 핵심 발주 거점이 되고 있습니다. 수출업체들이 저부가가치 농산물에서 베리류, 핵과류, 특산 채소로 전환함에 따라 포장 규격이 엄격해지고 있으며, 평균적인 골판지 등급도 상승하고 있습니다. 2024년, 스페인의 중국으로의 농산물·식품 수출액은 77억 달러에 달했습니다. 이로 인해 물류 거리가 길어지면서, 수출용 골판지 제품에 대한 내압성 및 적재성 요구 사항이 높아지고 있습니다. 2024년 12월에 서명된 EU-메르코수르 협정은 스페인의 무역 규모를 0.6%-1.4% 끌어올릴 것으로 예상되며, 이는 복합 운송에 적합한 수출용 골판지에 대한 추가적인 수요를 뒷받침할 것으로 전망됩니다. 이로 인해 스페인의 컨테이너보드 시장은 수출량뿐만 아니라, 스페인이 해외로 수출하는 상품의 가치 구성 변화에도 영향을 받게 될 것입니다.

전자상거래 소포와 적정 크기화의 성장

소포 처리량은 스페인 컨테이너 보드 시장에 있어 가공 보드에 대한 꾸준한 수요 증가를 가져오고 있습니다. 스페인에서는 2024년에 사상 최대인 13억 300만 건의 전자상거래 배송을 처리했으며, 이는 2019년의 5억 3,800만 건에 비해 240% 증가한 수치입니다. 한편, 2026년 물류 택배 처리량은 하루 평균 330만 건에 달하고 있습니다. ICEX는 2025년 전자상거래 성장률을 5.4%로 전망하고 있으며, 이는 당기 소포 처리량이 지속적으로 증가할 것임을 뒷받침하고 있습니다. 물류 네트워크가 소포 보관함이나 자동 이송 라인에 적합한, 적정 크기에 형태가 가변적인 포장 방식으로 전환됨에 따라, 변화는 상자 수뿐만 아니라 형태의 정밀도에도 미치고 있습니다. 스페인의 물류 업체들은 경로 최적화와 창고 자동화를 빠르게 도입하고 있으며, 이에 따라 자동 주문 처리 및 효율적인 공간 활용을 지원할 수 있는 포장 자재가 선호되고 있습니다. 수요는 식료품 및 퀵커머스 채널로도 확대되고 있으며, 인구 밀도가 높은 도시 지역의 배송 네트워크에서는 골판지로 만든 2차 포장이 여전히 표준적인 운송 수단으로 자리 잡고 있습니다. 이러한 추세에 따라 스페인의 컨테이너보드 시장은 단순한 상품으로서의 물량뿐만 아니라 부가가치가 높은 가공 형태를 통해서도 더 많은 지지를 얻고 있습니다.

재생 섬유와 에너지 비용의 변동

스페인 컨테이너보드 시장의 주요 위험 요인은 최종 수요의 급감보다는 비용 전가에 있습니다. 2025년 수요 중 재생 섬유가 60.18%를 차지하고 있으며, 이는 시장의 상당 부분이 폐지(OCC) 가격이나 에너지 비용 변동의 영향을 받기 쉬운 상태가 지속되고 있음을 보여줍니다. 유럽의 OCC 벤치마크 가격은 2025년 초가을 톤당 120유로(135.4달러)에서 연말에는 톤당 105유로(118.5달러)로 하락했습니다. 이는 하류 수요의 부진, 중국의 건식 재생 펄프 수입 중단, 그리고 서유럽의 재고 과잉을 반영한 것입니다. 이번 가격 하락으로 인해 위험이 해소된 것은 아닙니다. 섬유 가격의 변동성이 지속되면서, 비통합형 제조업체의 이익률 계획과 재고 전략에 계속해서 혼란을 초래하고 있기 때문입니다. 에너지에 대한 의존도 또한 또 다른 우려 요인으로 대두되고 있습니다. EU 내 재생 골판지 생산에 소비되는 에너지의 68%는 천연가스에서 비롯되며, 가스 가격이 1MWh당 10유로(11.2달러) 상승하면 재생 포장지의 변동 생산 비용은 1톤당 최대 20유로(22.5달러)까지 상승합니다. 스페인의 컨테이너보드 시장에서 이러한 압박은 자체 발전 설비, 바이오매스 지원, 또는 장기적인 에너지 헤지 수단을 갖추지 못한 재생지 등급 제지 공장에서 가장 크게 느껴집니다.

부문별 분석

2025년, 스페인의 컨테이너보드 시장에서 재생 섬유는 60.18%를 차지했으며, 이 부문은 원료 구성에서 주도적인 위치를 차지했습니다. 이러한 점유율은 스페인의 확고한 제지 공장 기반, 높은 골판지 회수율, 그리고 많은 표준 용도에서 수입 버진 크라프트지보다 재생지를 조달하는 것이 비용 면에서 유리하다는 점을 반영하고 있습니다. 엘 부르고 데 에브로에 위치한 사이카(Saika)사의 PM9는 100% 재생 섬유로 연간 40만 톤 이상의 경량 재생 골판지를 생산하고 있으며, 이 기계는 효율성과 지속가능성을 높이기 위해 2026년 3월에 계획되었던 업그레이드를 완료했습니다. 스페인의 90%에 달하는 골판지 회수율은 안정적인 원료 공급을 뒷받침하고 있지만, 자체 회수망을 갖추지 않은 제지 공장은 2025년에 예상되는 톤당 105-120유로(118-135달러) 범위 내에서 OCC 가격이 변동할 경우 여전히 영향을 받기 쉬운 상황에 놓여 있습니다.

버진 펄프는 2031년까지 연평균 성장률(CAGR) 1.79%를 기록하며 성장할 것으로 예상되며, 초기 규모는 작지만 더 빠르게 성장하는 원료 기반이 될 전망입니다. 이러한 성장은 고급 신선식품 수출 및 전자상거래 분야 수요 증가를 반영한 것으로, 이러한 분야에서는 파열 강도 및 내압성 면에서 여전히 고성능 섬유 원료가 선호되고 있습니다. 부문별로 살펴보면, 버진 섬유는 스페인 컨테이너보드 시장에서 성장세가 두드러지는 분야이며, 이 분야에서는 원자재 비용보다 성능 사양이 더 중요하게 여겨지고 있습니다. 엔세사가 아스 폰테스에 건설을 계획하고 있는 표백 재생 섬유 바이오 플랜트는 정부로부터 2,470만 유로(2,780만 달러)의 임시 자금을 지원받았으며, 2025년 8월에 발급된 통합 환경 허가도 취득한 상태이며, 이는 생산자가 재생 섬유와 버진 스타일 등급 간의 성능 격차를 줄이려 하고 있음을 보여줍니다. 따라서 스페인의 컨테이너보드 업계는 여전히 재생 섬유가 주도하고 있지만, 더 강인하고 전문성이 높은 등급에 대한 상업적 수요가 증가함에 따라, 버진 펄프를 원료로 하는 솔루션이 소폭이나마 성장 우위를 점하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the spain containerboard market size was valued at USD 1.96 billion in 2025 and estimated to grow from USD 2.02 billion in 2026 to reach USD 2.18 billion by 2031, at a CAGR of 1.53% during the forecast period (2026-2031).

This report is Segmented by Material (Virgin Fibers and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and More). The Market Forecasts are Provided in Terms of Value (USD).

Spain Containerboard Market Trends and Insights

Food Export And Fresh-Produce Corrugated Demand

Spain's agrifood export base keeps the Spain containerboard market closely linked to fresh-produce trade flows. Fresh fruit and vegetable exports generated EUR 18.666 billion in 2025 (USD 20.2 billion), even as shipped volume declined by 4%, indicating that higher-value categories lifted packaging value intensity per unit moved. Andalusia accounted for 33% of national fruit and vegetable export volume in 2025, while the Valencian Community contributed 28%, making both regions central ordering points for corrugated demand. As exporters shift from lower-value produce to berries, stone fruits, and specialty vegetables, packaging specifications become tighter and average board grades rise. Spain's agrifood exports to China reached USD 7.7 billion in 2024, which lengthens logistics distances and raises crush resistance and stacking requirements for corrugated formats serving export chains. The EU-Mercosur agreement, signed in December 2024, is expected to boost Spain's trade by 0.6%-1.4%, supporting further demand for export-ready boards suited to multi-modal handling. This keeps the Spain containerboard market tied not only to export volumes, but also to the changing value mix of what Spain ships abroad.

E-Commerce Parcel And Right-Sizing Growth

Parcel activity is providing the Spain containerboard market with a steady source of incremental demand for converted board. Spain handled a record 1.303 billion e-commerce shipments in 2024, up 240% from 538 million in 2019, while logistics package volumes are running at 3.3 million per day in 2026. ICEX projected 5.4% e-commerce growth for 2025, which supports continuing parcel throughput into the current period. The material change is not only in box count but also in format precision, as logistics networks move toward right-sized, variable-geometry packaging that better fits parcel lockers and automated handling lines. Spanish logistics operators have adopted route optimization and warehouse automation at high rates, which favors packaging inputs that can support automated fulfillment and efficient cube utilization. Demand is also broadening into grocery and quick-commerce channels, where corrugated secondary packaging remains the standard transport choice across dense urban distribution networks. That pattern gives the Spain containerboard market more support from value-added converted formats than from simple commodity volume alone.

Recovered Fiber And Energy Cost Volatility

The main risk to the Spain containerboard market remains cost transmission rather than a collapse in end demand. Recycled fibers accounted for 60.18% of demand in 2025, indicating that a large part of the market remains exposed to swings in OCC prices and energy costs. European OCC benchmark prices moved down from EUR 120 (USD 135.4) per tonne in early autumn 2025 to EUR 105 (USD 118.5) per tonne by year-end, reflecting weak downstream demand, China's suspension of dry-ground recycled pulp imports, and excess inventories in Western Europe. That price decline did not eliminate risk, as unstable fiber pricing continues to disrupt margin planning and inventory strategy for non-integrated producers. Energy exposure adds another layer, with 68% of energy consumed in EU recycled containerboard production derived from natural gas, and a EUR 10 (USD 11.2) per MWh rise in gas prices lifting variable production costs by up to EUR 20 (USD 22.5) per tonne for recycled packaging paper. For the Spain containerboard market, this pressure is strongest at recycled-grade mills that lack captive power, biomass support, or long-term energy hedging.

Other drivers and restraints analyzed in the detailed report include:

- Recyclability Rules Favor Fiber Packaging

- Strong Recovered-Fiber And Recycling Infrastructure

- Reusable Transport Packaging Mandates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled fibers accounted for 60.18% of the Spain containerboard market in 2025, giving this segment the leading position across the feedstock mix. That share reflects Spain's established paper mill base, high corrugated recovery rates, and the cost advantage of recovered-paper sourcing over imported virgin kraft in many standard applications. Saica's PM9 at El Burgo de Ebro produces more than 400,000 metric tons per year of lightweight recycled containerboard from 100% recovered fiber, and the machine completed a planned upgrade in March 2026 to improve efficiency and sustainability. Spain's 90% corrugated recovery rate supports stable feedstock access, although mills without captive collection remain exposed when OCC prices fluctuate within the EUR 105-120 (USD 118-135) per tonne range seen in 2025.

Virgin fibers are forecast to grow at a 1.79% CAGR through 2031, making them the faster-growing feedstock base even from a smaller starting point. That growth reflects stronger demand from premium fresh-produce exports and e-commerce applications, where burst strength and crush resistance still favor higher-performance fiber inputs. In segment terms, virgin fibers are the faster-moving part of the Spanish containerboard market size, where performance specifications matter more than raw material cost alone. Ence's planned bleached-recycled-fiber bioplant at As Pontes, backed by EUR 24.7 million (USD 27.8 million) in provisional government funding and supported by an integrated environmental authorization issued in August 2025, shows how producers are trying to narrow the performance gap between recycled and virgin-style grades. The Spain containerboard industry therefore remains led by recycled fiber, but the commercial pull toward stronger and more specialized grades is giving virgin-linked solutions a modest growth edge.

List of Companies Covered in this Report:

- SAICA Pack, S.L.

- Smurfit Westrock plc

- International Paper Company

- Hinojosa Packaging Group, S.L.

- Cartonajes de la Plana, S.L.U.

- Cartonajes Santorroman, S.A.

- Ondupack, S.A.U.

- Papresa, S.A.

- Klingele Paper & Packaging SE & Co. KG

- Cartonajes Europa, S.A.

- Cartondis, S.A.

- Vegabaja Packaging, S.L.

- Cartonajes International, S.A.

- Macopa, S.A.

- INECO, S.A.

- Avance Carton Ondulado, S.L.

- Cartonajes Valles Gasset, S.A.

- Cartonajes Arregui, S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Food Export and Fresh-Produce Corrugated Demand

- 4.2.2 E-Commerce Parcel and Right-Sizing Growth

- 4.2.3 Recyclability Rules Favor Fiber Packaging

- 4.2.4 Strong Recovered-Fiber and Recycling Infrastructure

- 4.2.5 Automation-Ready Packaging Demand in Iberian Logistics

- 4.2.6 Agricultural-Residue Nanocellulose for Stronger Recycled Linerboard

- 4.3 Market Restraints

- 4.3.1 Recovered Fiber and Energy Cost Volatility

- 4.3.2 Reusable Transport Packaging Mandates

- 4.3.3 Fresh-Produce Shift Toward Reusable Plastic Crates

- 4.3.4 Mill-Outage Risk in Spain's Recycled Containerboard Base

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAICA Pack, S.L.

- 6.4.2 Smurfit Westrock plc

- 6.4.3 International Paper Company

- 6.4.4 Hinojosa Packaging Group, S.L.

- 6.4.5 Cartonajes de la Plana, S.L.U.

- 6.4.6 Cartonajes Santorroman, S.A.

- 6.4.7 Ondupack, S.A.U.

- 6.4.8 Papresa, S.A.

- 6.4.9 Klingele Paper & Packaging SE & Co. KG

- 6.4.10 Cartonajes Europa, S.A.

- 6.4.11 Cartondis, S.A.

- 6.4.12 Vegabaja Packaging, S.L.

- 6.4.13 Cartonajes International, S.A.

- 6.4.14 Macopa, S.A.

- 6.4.15 INECO, S.A.

- 6.4.16 Avance Carton Ondulado, S.L.

- 6.4.17 Cartonajes Valles Gasset, S.A.

- 6.4.18 Cartonajes Arregui, S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment