|

시장보고서

상품코드

2064385

이탈리아의 컨테이너보드 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Italy Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

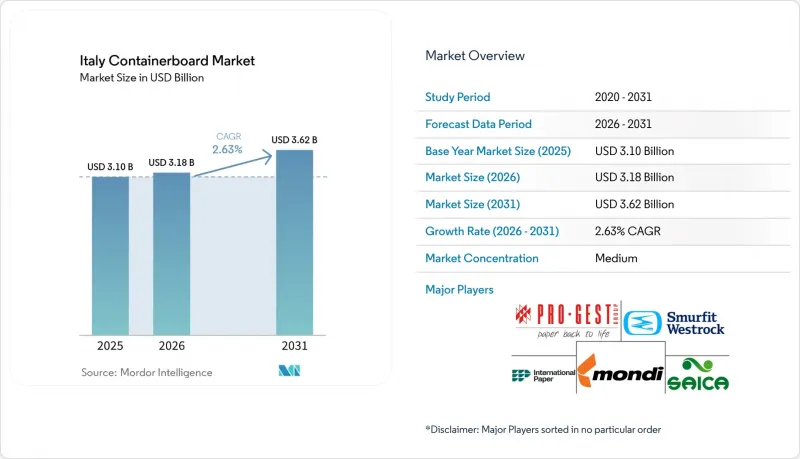

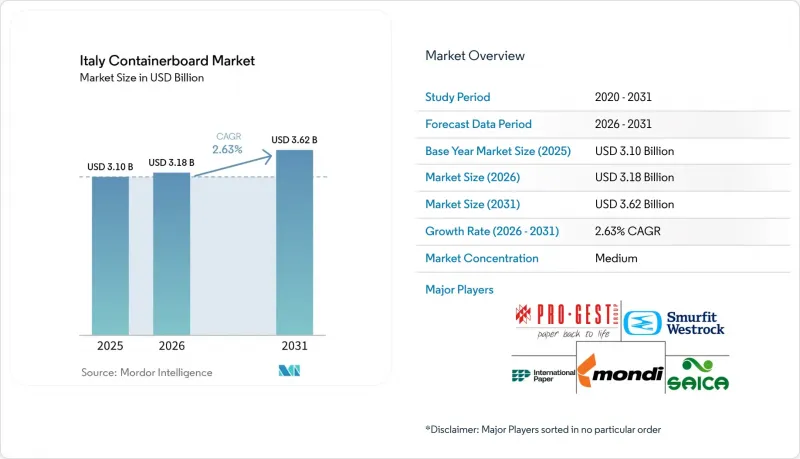

Mordor Intelligence에 의하면, 이탈리아 컨테이너보드 시장 규모는 2025년 31억 달러에서 2026년에는 31억 8,000만 달러로 확대되어 2031년까지 36억 2,000만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 2.63%로 성장할 전망입니다.

본 보고서는 원료(버진 섬유 및 재생 섬유), 제품 유형(크래프트 라이너, 테스트 라이너, 플루팅), 그리고 최종 사용자 산업(식품 및 음료, 소비재, 산업용, 기타)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

이탈리아 컨테이너보드 시장 동향과 인사이트

전자상거래 및 옴니채널에 따른 골판지 수요

2025년에 B2C 전자상거래가 계속 확대되고 모든 제품 카테고리에서 온라인 침투율이 상승함에 따라, 이탈리아의 컨테이너보드 시장은 소포 물량 증가로 인해 꾸준한 성장세를 보이고 있습니다. 이탈리아 B2C 전자상거래의 상품 부문 규모는 2025년에 400억 유로(451억 달러)에 달했으며, 소매 상품 판매에서 온라인 침투율은 전년도의 10.7%에서 11.2%로 상승했습니다. 단품 발송 방식에서는 팔레트 혼적 방식에 비해 단위당 30%에서 50% 더 많은 판지가 사용되기 때문에 상품 기준 자체의 성장률을 웃도는 속도로 판지 수요가 증가하고 있습니다. 수요는 지리적으로도 확대되어, 2026년에는 남부 지역 및 도서 지역의 성인 온라인 이용률이 60.6%에 달하며, 북부 지역과의 오랜 디지털 격차가 줄어들었습니다. 2026년 초에 발표된 조사에 따르면, 이탈리아 소비자의 75%가 소포 수령을 골판지 상자와의 주요 물리적 접점으로 인식하고 있으며, 종이 기반 배송 방식이 라스트 마일 소매에서 계속해서 핵심적인 역할을 수행하고 있습니다.

2차 포장재에서 플라스틱을 판지로 대체

이탈리아의 컨테이너보드 시장은 2차 포장 및 운송용 포장에서 플라스틱을 대체하는 광범위한 전환의 혜택도 누리고 있습니다. 특히, 재활용의 용이성이나 역물류의 간소화가 구매자에게 중요하게 여겨지는 분야에서 이러한 경향은 두드러집니다. 2026년 1월에 발표된 조사에 따르면, 이탈리아의 사용자 기업 중 51%가 연질 플라스틱을 골판지로 대체하고 있으며, 소비자의 55%는 배송되는 포장재에서 골판지가 기포 완충재나 경질 플라스틱 부품보다 더 보편화되었다고 응답했습니다. 이러한 변화는 규제 때문만은 아닙니다. 왜냐하면 골판지 포장은 분류 작업을 덜어줄 뿐만 아니라, 사용 후 종이 재활용 공정에도 더 쉽게 통합할 수 있기 때문입니다. 2차 포장을 대체할 때는 더 무겁고 강도가 높은 판지 등급이 필요한 경우가 많으며, 이로 인해 테스트 라이너나 더 높은 적재 하중을 견딜 수 있는 기타 사양의 가치가 높아집니다. 또한, 유럽연합 집행위원회의 PPWR 지침이 재활용이 용이한 포장을 권장하는 체계를 확립함에 따라, 2026년 8월부터 이탈리아에서도 적용될 예정이어서 정책적 여건도 점차 개선되고 있습니다.

전력·가스 비용 부담 증가

이탈리아의 컨테이너보드 시장은 여전히 에너지로 인한 구조적인 비용 부담에 직면해 있으며, 이러한 압박은 유럽의 주요 제지 경쟁국들보다 더 심합니다. 콘피인두스트리아(Confindustria)의 보고서에 따르면, 2025년 이탈리아의 산업용 전기 요금은 EU 평균보다 약 30% 높았으며, 독일, 프랑스, 스페인보다 높은 수준을 유지했습니다. 이는 제지 공장에 있어 매우 중요한 문제입니다. 왜냐하면 이탈리아의 제지 생산에서 에너지 비용은 역사적으로 운영 비용의 40% 이상을 차지해 왔기 때문입니다. 또한, 해당 부문의 열 수요의 95% 이상을 천연가스에 의존하고 있기 때문에 생산자들은 국내 전력 가격과 연료 가격 간의 큰 격차를 쉽게 상쇄할 수 없습니다. 업계 관계자들은 2025년 초, 이러한 격차가 70만 명의 근로자를 고용하고 있는 공급망 전체의 경쟁력을 위협하고 있다고 경고하며, 이 문제가 개별 제지 공장에만 국한되지 않는다는 점을 강조했습니다.

부문별 분석

2025년 현재, 이탈리아 컨테이너보드 시장에서 재생 섬유의 점유율은 61.13%를 차지하고 있으며, 이는 단순한 가격 선호라기보다는 인프라의 정비 수준을 반영한 것입니다. 이탈리아에서는 제지 과정에서 사용되는 섬유 배합의 63%가 재생지로 이루어져 있으며, 재생 섬유 총 소비량 면에서는 독일에 이어 유럽에서 2위를 차지하고 있습니다. 이러한 공급 기반을 바탕으로, 이탈리아의 컨테이너보드 시장은 재생 등급 부문에서 국내에서 확고한 입지를 유지하고 있습니다. 이는 성숙한 국내 수거·선별 시스템을 통해 원료를 조달할 수 있기 때문입니다. 2025년 4월에 완료된, 몬디(Mondi)사가 2억 유로(2억 1,400만 달러)를 투자한 두이노 공장 개보수 공사(재활용 골판지 연간 생산 능력 42만 톤으로 전환)는 대형 제조업체가 이탈리아의 재활용 섬유 공급망을 플래그십 프로젝트를 수행하기에 충분한 신뢰성을 갖추고 있다고 판단하고 있음을 보여줍니다.

버진 펄프는 2026년부터 2031년까지 연평균 성장률(CAGR) 2.94%를 나타낼 것으로 예측되며, 초기 규모는 작지만 가장 빠르게 확대될 원료 기반이 될 것입니다. 이탈리아 컨테이너보드 시장에서는 신선 식품 및 고급 소비재 수출업체들을 중심으로, 재생 등급 제품에서는 경량화로 인해 일관되게 제공되지 않는 더 높은 파열 강도, 우수한 인쇄 적합성, 그리고 균일한 표면 품질을 요구하는 수요가 증가하고 있습니다. 또한, 이탈리아는 수입 버진 크라프트지에 대한 의존도가 여전히 높은 상태이며, 이는 공급망의 이 부분에서 여전히 구조적인 국내 공급 부족이 존재함을 보여줍니다. 인증 기준은 이미 충분히 확립된 것으로 보입니다. 2024년에는 이탈리아 제지 공장에서 사용된 버진 섬유의 90%가 FSC 또는 PEFC 인증을 획득했으며, 이는 대규모 구매업체의 조달 과정 투명성을 높이는 데 기여하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the italy containerboard market size is expected to increase from USD 3.10 billion in 2025 to USD 3.18 billion in 2026 and reach USD 3.62 billion by 2031, growing at a CAGR of 2.63% over 2026-2031.

This report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and More). The Market Forecasts are Provided in Terms of Value (USD).

Italy Containerboard Market Trends and Insights

E-Commerce and Omnichannel Corrugated Demand

The Italian containerboard market is receiving steady support from parcel growth, as B2C e-commerce continued to expand in 2025 and online penetration rose across product categories. Italy's B2C e-commerce product segment reached EUR 40 billion (USD 45.1 billion) in 2025, while online penetration of retail product sales rose to 11.2% from 10.7% in the prior year. Single-item shipment formats use 30% to 50% more board per unit than consolidated pallet formats, allowing board demand to rise faster than the merchandise base itself. Demand is also spreading geographically, as daily online use in southern regions and the islands reached 60.6% of adults in 2026, narrowing the long-standing digital divide with the north. Research presented in early 2026 also showed that 75% of Italian consumers viewed the parcel receipt as their primary physical point of contact with corrugated cardboard, keeping paper-based shipping formats central to last-mile retail.

Plastic-to-Paperboard Substitution in Secondary Packaging

The Italy containerboard market is also benefiting from a broader switch away from plastic in secondary and transit packaging, especially where easier recycling and simpler reverse logistics matter to buyers. Research released in January 2026 showed that 51% of Italian user companies had replaced flexible plastics with corrugated cardboard, while 55% of consumers said corrugated had become more common than bubble wrap and rigid plastic components in delivered packages. This change is not tied solely to regulation, because corrugated packaging also reduces sorting friction and fits more easily into the paper recycling stream after use. Secondary packaging substitution often requires heavier, stronger board grades that support value growth in testliner and other specifications that can handle higher stacking loads. The policy backdrop is becoming more favorable as well, as the European Commission's PPWR guidance establishes a framework that favors easily recyclable packaging and will apply in Italy from August 2026.

Elevated Electricity And Gas Cost Burden

The Italy containerboard market still faces a structural cost burden from energy, and that pressure is stronger than in the main competing paper-producing countries in Europe. Confindustria reported that Italian industrial electricity prices in 2025 were around 30% above the EU average and remained higher than those in Germany, France, and Spain. This matters deeply for paper mills because energy has historically accounted for more than 40% of operating costs in Italian paper production. The sector also depends on natural gas for more than 95% of its heat requirements, so producers cannot easily absorb wide differences in national power and fuel pricing. Industry representatives warned in early 2025 that this gap threatened competitiveness across a supply chain employing 700,000 workers, underscoring that the issue extends beyond individual mills.

Other drivers and restraints analyzed in the detailed report include:

- High Recovered Fiber Collection and Recovery Rates in Italy

- Food and Beverage Export and Fresh Produce Logistics Demand

- Recovered Paper Price And Quality Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled fibers held 61.13% of Italy's containerboard market share in 2025, reflecting infrastructure depth more than simple price preference. Italy used recycled paper for 63% of its fiber mix in paper production, ranking second in Europe for total recovered fiber consumption after Germany. This supply base helps the Italy containerboard market keep a strong domestic position in recycled grades, because furnishes can be sourced through a mature national collection and sorting system. Mondi's EUR 200 million (USD 214 million) conversion of the Duino mill to 420,000 tonnes per year of recycled containerboard, completed in April 2025, showed that a major producer viewed the Italian recovered fiber chain as dependable enough for a flagship project.

Virgin fibers are forecast to grow at a CAGR of 2.94% between 2026 and 2031, which makes them the fastest-expanding material base, even from a smaller starting point. The Italy containerboard market is seeing this pull from exporters of fresh produce and premium consumer goods that need stronger burst performance, better printability, and a more uniform surface quality than recycled grades can consistently deliver at lighter weights. Italy also remained highly exposed to imported virgin kraft paper, indicating that this part of the supply chain still has a structural domestic gap. Certification standards already appear well established, because 90% of virgin fibers used in Italian mills carried FSC or PEFC certification in 2024, which supports procurement transparency for larger buyers.

List of Companies Covered in this Report:

- Pro-Gest S.p.A.

- Smurfit Westrock plc

- Mondi plc

- International Paper Italia S.r.l.

- Sociedad Anonima Industrias Celulosa Aragonesa, S.A.

- VPK Group NV

- Progroup Board S.r.l.

- Ghelfi Ondulati S.p.A.

- Ondulati Santerno S.p.A.

- LIC Packaging S.p.A.

- Ondapack Sud S.p.A.

- Box Marche S.p.A.

- Sada S.p.A.

- Antonio Sada & Figli S.p.A.

- Burgo Group S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce and Omnichannel Corrugated Demand

- 4.2.2 Plastic-to-Paperboard Substitution in Secondary Packaging

- 4.2.3 High Recovered Fiber Collection and Recovery Rates in Italy

- 4.2.4 Food and Beverage Export and Fresh Produce Logistics Demand

- 4.2.5 PPWR Readiness Favoring Recyclable Mono-Material Packs

- 4.2.6 Lightweighting Economics After New Recycled Capacity Start-Ups

- 4.3 Market Restraints

- 4.3.1 Elevated Electricity and Gas Cost Burden

- 4.3.2 Recovered Paper Price and Quality Volatility

- 4.3.3 PPWR Compliance and Documentation Costs for Smaller Converters

- 4.3.4 Imported Kraftliner Pressure in High-Performance Grades

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Pro-Gest S.p.A.

- 6.4.2 Smurfit Westrock plc

- 6.4.3 Mondi plc

- 6.4.4 International Paper Italia S.r.l.

- 6.4.5 Sociedad Anonima Industrias Celulosa Aragonesa, S.A.

- 6.4.6 VPK Group NV

- 6.4.7 Progroup Board S.r.l.

- 6.4.8 Ghelfi Ondulati S.p.A.

- 6.4.9 Ondulati Santerno S.p.A.

- 6.4.10 LIC Packaging S.p.A.

- 6.4.11 Ondapack Sud S.p.A.

- 6.4.12 Box Marche S.p.A.

- 6.4.13 Sada S.p.A.

- 6.4.14 Antonio Sada & Figli S.p.A.

- 6.4.15 Burgo Group S.p.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment