|

시장보고서

상품코드

2064002

북미의 기계, 전기, 배관(MEP) 서비스 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)North America Mechanical, Electrical, Plumbing (MEP) Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

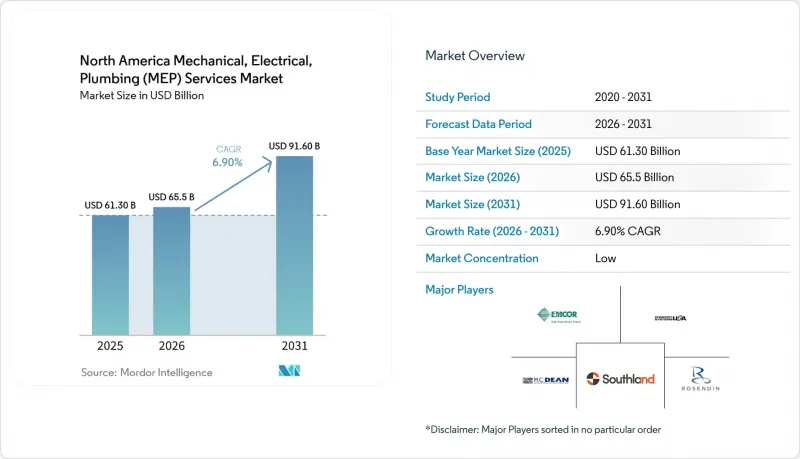

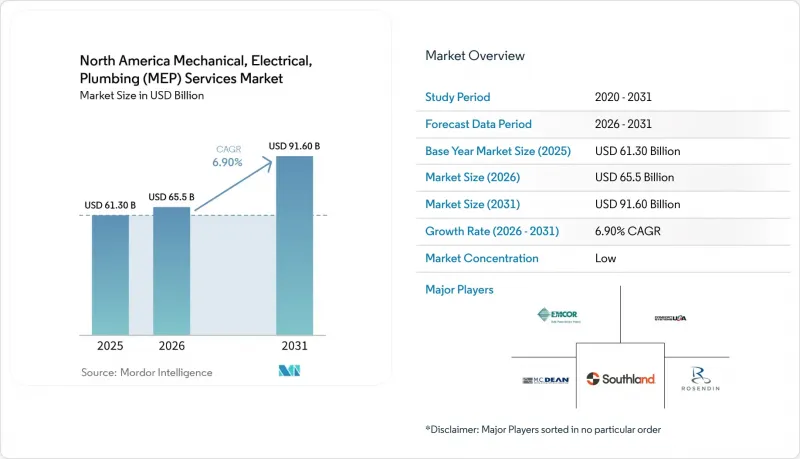

Mordor Intelligence에 의하면, 북미의 기계, 전기, 배관(MEP) 서비스 시장 규모는 2025년 613억 달러로 평가되었고, 2026년에는 655억 달러로 추정되며, 2031년까지 916억 달러에 이를 것으로 예측됩니다.

2026-2031년 연평균 성장률(CAGR) 6.90%로 성장할 것으로 전망됩니다.

본 보고서는 유형별(기계, 전기, 배관, 통합 MEP), 서비스 유형별(설계 및 엔지니어링, 설치, 시험 및 시운전, 유지보수, 수리 및 개보수, 관리형 및 성과보수형), 최종 사용자 산업별(주택, 상업, 인프라), 그리고 지역별(미국, 캐나다, 멕시코)로 분류되어 있습니다. 시장 전망치는 금액(달러) 단위로 제시되어 있습니다.

북미의 기계, 전기, 배관(MEP) 서비스 시장 동향과 인사이트

연방 및 주 정부 인프라 자금

연방 정부의 예산 배분은 대규모 기계, 전기, 배관 패키지가 포함된 프로젝트 부문을 지원하고 있어, 북미 MEP 서비스 시장에 장기적인 성장 여지를 제공합니다. IIJA(인플레이션 억제 및 투자법)에는 주요 고속도로 및 교통수단에 대한 인허가 조항이 포함되어 있으며, DOT(미국 교통부)의 데이터에 따르면 2026년 4월까지 각 프로그램 전체에서 4,902억 달러의 지출 의무가 발생했으며, 이 중 2,186억 달러가 이미 지출된 것으로 나타났습니다. 이는 지출이 발표 단계에서 실제 집행 단계로 넘어갔음을 뒷받침합니다. MEP 도급업체에게 있어 지출이 가장 큰 비중을 차지하는 분야는 교통 시설, 빗물 배수 시스템, 처리장, 펌프장 및 공공 건축물입니다. 이러한 시설에서는 배전, 제어, 배관, 환기, 방화 설비가 나중에 추가되는 것이 아니라 핵심 공사 범위에 포함되어 있습니다. EPA(미국 환경보호청)의 자금 배분 방식도 이러한 견해를 뒷받침하고 있습니다. 이 기관은 이미 1,200건 이상의 식수 순환 기금 프로젝트를 지원해 왔으며, 납으로 된 급수관 교체에 150억 달러를 배정했으나, 이는 압도적으로 배관 공사가 주를 이루는 작업입니다. 많은 도시 프로젝트에서 연방 정부가 비용의 80%를 분담함으로써, 지방자치단체의 자금 조달 과정에서 발생하는 마찰도 완화됩니다. 이를 통해 조달 주기가 단축되어, MEP 공사가 주를 이루는 유틸리티이 과거의 인프라 주기보다 신속하게 추진될 것입니다. 이러한 요인은 북미 MEP 서비스 시장의 미수주 잔고에 대한 가시성을 뒷받침하고 있습니다. 왜냐하면 공공 프로젝트는 일반적으로 설계, 조달, 설치, 시운전 등 수년에 걸친 여러 단계를 거쳐 진행되기 때문에 수익 창출 기회가 여러 계약 기간에 분산되기 때문입니다.

데이터센터 및 전기차 충전 인프라 구축

북미의 MEP 서비스 시장은 표준 상업용 건물보다 전력 소비량이 훨씬 더 많은 데이터센터와 전기차 충전 인프라의 확산에 힘입어 성장하고 있습니다. 전기실, 중전압 배전, 변전소, 개폐 장치, 직접 액체 냉각 루프, 백업 시스템, 제어 플랫폼이 현재 하이퍼스케일 프로젝트의 핵심 경로를 정의하고 있으며, 이로 인해 프로젝트 가치의 더 큰 비중이 MEP 범위로 이동하고 있습니다. 아마존은 2025년 11월, 인디애나주 북부에 위치한 데이터센터 단지에 150억 달러를 투자할 것이라고 발표했습니다. 또한, 사이러스원(CyrusOne)은 칼파인(Calpine)과 공동으로 2025년 7월 텍사스주에서 초기 용량 190MW 규모의 하이퍼스케일 데이터센터 프로젝트(12억 달러 규모)를 발표했습니다. 이 모든 것은 현재의 전력 및 냉각 요구 사항의 규모를 여실히 보여주고 있습니다. 이러한 프로젝트들은 규모를 확대할 뿐만 아니라 기술적 복잡성도 증가시키고 있습니다. 고밀도 랙과 견고한 가동 시간 목표를 달성하기 위해서는 전기 설계, 냉각, 제어, 시운전 간의 보다 긴밀한 협력이 필요하기 때문입니다. 게다가 전기차 충전이 새로운 과제를 안겨주고 있습니다. 2026년판 NEC(국가전기규정)에 따라, 상업시설 및 공공시설에서는 서비스 업그레이드, 비상 차단 조치, 그리고 건물 부하 관리 전략과의 조정이 점점 더 필요해지고 있기 때문입니다. 그 결과, 북미의 MEP 서비스 시장에서는 설치 업체뿐만 아니라, 촉박한 일정 속에서 긴밀하게 통합된 시스템의 설계, 공정 관리, 시운전을 수행할 수 있는 기업에 대한 수요가 높아지고 있습니다.

전문직 분야의 숙련된 근로자 부족

수요 증가세가 숙련된 노동력공급을 앞지르고 있기 때문에 노동력 확보는 여전히 북미 MEP 서비스 시장에서 가장 뚜렷한 단기적 제약 요인으로 남아 있습니다. 2025년 AGC와 NCCER이 실시한 인력 조사에 따르면, 기업의 92%가 시간제 숙련직 채용에 어려움을 겪고 있으며, 75% 이상이 특히 전기 기술자, 배관공, 상수도 기술자를 ‘채용하기 어렵다’고 꼽았습니다. 전미건설업협회(ABC)는 건설 업계가 2026년까지 순증으로 34만 9,000명의 신규 인력을 확보해야 한다고 밝혔으며, 이는 현재의 채용 속도만으로는 프로젝트 수요를 충족시키기에 부족함을 보여줍니다. 데이터센터 건설은 가장 경험이 풍부한 전기 기술자, 시운전 전문가, 제어 담당 인력을 고임금 프로젝트로 끌어들이고 있어 이러한 인력 부족 현상을 더욱 악화시키고 있으며, 그 결과 기존의 상업시설이나 공공시설 공사에서는 인력 부족이 심화되고 있습니다. 이러한 불균형으로 인해 입찰 프리미엄이 상승하고 공사 기간이 연장됨에 따라, 발주처들은 조립식 건축 방식을 도입하고 인재 육성 시스템을 갖춘 대형 건설사로 눈을 돌리고 있습니다. 또한, 북미의 MEP 서비스 시장에서 통합형 서비스 제공의 여지가 생기고 있습니다. 이는 발주처가 각 전문 공종의 인계·인수에 의존하기보다는 사내에서 인력 조정을 해결할 수 있는 기업을 점점 더 중요하게 여기고 있기 때문입니다.

부문별 분석

2025년 기준으로, 전기 서비스는 북미 MEP 서비스 시장 규모의 35%를 차지했으며, 매출 기준 최대의 부문이 되었습니다. 이러한 주도적 지위는 데이터센터, 상업시설의 개보수, 그리고 전기화 프로그램 모두에서 전력 배전, 제어, 보호 시스템 및 설비의 업그레이드가 프로젝트 예산의 핵심으로 자리 잡고 있다는 사실을 반영하고 있습니다. EMCOR의 미국 전기 공사 부문은 2026년 1분기에 8억 4,560만 달러의 매출을 기록하여 전년 동기 대비 12.8% 증가했습니다. 경영진은 이러한 실적이 해당 부문의 단기적인 수요 기반을 뒷받침하는 첨단 제조업 및 데이터센터의 활동에 기인한 것이라고 보고 있습니다. 2026년판 NEC(국가 전기 규정) 역시 해당 부문을 더욱 뒷받침하고 있습니다. 중전압에 관한 새로운 규정, 표시 요건의 확대, 그리고 전력 제어 시스템의 인증으로 인해 상업시설 및 공공시설 프로젝트에서의 설계 업무와 현장에서의 규정 준수 대응 업무가 증가하며, 이러한 업무가 수익으로 이어지기 때문입니다. 또한, 기존 건물들이 히트 펌프, 충전기, 에너지 저장 시스템 및 보다 정교한 디지털 제어 시스템으로 전환됨에 따라, 전기 서비스 부문은 상당한 가치 점유율을 확보하게 될 것입니다. 왜냐하면 이러한 변경 사항들이 모두 서비스 규모와 전력 배전 아키텍처에 영향을 미치기 때문입니다. 북미 MEP 서비스 시장에서 이로 인해 전기 공사의 범위는 ‘규모’와 ‘복잡성’ 두 가지 요인에 의해 주도되게 되어, 단순한 교체 수요에만 의존하는 것보다 더 견고한 입지를 확보하게 될 것입니다.

기계 설비 서비스는 여전히 2위의 규모를 차지하고 있습니다. 이는 HVAC, 소방 설비, 공정 배관 및 미션 크리티컬 냉각 시스템이 병원, 첨단 제조 공장, 데이터센터의 핵심을 이루고 있기 때문입니다. 랙 밀도가 높아짐에 따라, 또한 소유자가 표준 공기 냉각 시스템에서 액체 보조형 또는 액체 기반 냉각 전략으로 전환함에 따라 냉각 설계는 더욱 복잡해지고 있으며, 배관, 제어, 전력 및 시운전 간의 보다 긴밀한 협력이 필요해지고 있습니다. 배관 서비스는 매출 비중은 작지만, 상수도 인프라 공사나 납제 급수관 교체 프로그램과 연계된 명확한 교체 주기의 혜택을 받고 있으며, 재량권이 큰 다른 건축 분야에 비해 지자체로부터 더 안정적인 수요 기반을 확보하고 있습니다. 통합 MEP 서비스는 2031년까지 연평균 성장률(CAGR) 8.86%를 나타낼 것으로 예측되며, 이는 북미 MEP 서비스 시장의 각 부문 중 가장 빠른 성장 속도입니다. 발주자가 이 모델을 선호하는 이유는 책임 소재가 명확한 단일 도급업체가 조정상의 미비점을 줄이고, 시운전 기간을 단축하며, 복잡한 시설에서 발생할 수 있는 클레임 위험을 낮출 수 있기 때문입니다. 이러한 경향은 북미 MEP 서비스 업계에서 개별 패키지만을 제공하는 기업보다 전문 기술의 깊이와 프로그램 관리 능력을 겸비한 기업이 더 높이 평가받고 있음을 시사합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the north america mechanical, electrical, plumbing services market size is expected to increase from USD 61.30 billion in 2025 to USD 65.5 billion in 2026 and reach USD 91.60 billion by 2031, growing at a CAGR of 6.90% over 2026-2031.

This report is Segmented by Type (Mechanical, Electrical, Plumbing, Integrated MEP), Service Type (Design and Engineering, Installation, Testing and Commissioning, Maintenance, Repair and Retrofit, Managed and Performance-Based), End-User Industry (Residential, Commercial, Infrastructure), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Mechanical, Electrical, Plumbing (MEP) Services Market Trends and Insights

Federal and State Infrastructure Funding

Federal appropriations are giving the North America MEP services market a long runway because they support project categories that carry large mechanical, electrical, and plumbing packages. The IIJA includes major highway and transportation authorization, and DOT data showed USD 490.2 billion obligated and USD 218.6 billion outlaid across programs by April 2026, which confirms that spending has moved beyond announcement into active execution. For MEP contractors, spending matters most in transit facilities, stormwater systems, treatment plants, pump stations, and public buildings, where electrical distribution, controls, piping, ventilation, and fire protection are built into the core scope rather than added later. The EPA's funding pattern reinforces that view because it had already supported more than 1,200 drinking water revolving fund projects and designated USD 15 billion for lead service line replacement, which is overwhelmingly plumbing-intensive work. The 80% federal cost share on many urban projects also reduces local funding friction, which shortens procurement cycles and moves MEP-heavy public jobs forward faster than in prior infrastructure cycles. This driver supports backlog visibility in the North America MEP services market because public projects usually extend across multi-year design, procurement, installation, and commissioning phases, which spreads revenue opportunities across more than one contracting season.

Data Center and EV Charging Build-out

The North America MEP services market is also being lifted by a data center and EV charging wave that is far more power-intensive than standard commercial construction. Electrical rooms, medium-voltage distribution, substations, switchgear, direct liquid cooling loops, backup systems, and control platforms now define the critical path on hyperscale projects, which shifts a larger share of project value into MEP scope. Amazon announced a USD 15 billion investment in Northern Indiana data center campuses in November 2025, and CyrusOne, with Calpine, announced a USD 1.2 billion hyperscale data center project in Texas with 190 MW of initial capacity in July 2025, both of which illustrate the scale of current power and cooling requirements. These projects not only increase volume, but they also raise technical complexity because dense racks and resilient uptime targets demand closer integration between electrical design, cooling, controls, and commissioning. EV charging adds another layer because commercial and institutional sites increasingly need service upgrades, emergency disconnect arrangements, and coordination with building load management strategies under the 2026 NEC. The result is that the North America MEP services market is seeing stronger demand not just for installers, but also for firms that can engineer, sequence, and commission tightly integrated systems on compressed schedules.

Skilled Labor Shortages in Specialty Trades

Labor availability remains the clearest short-term constraint on the North America MEP services market because demand is rising faster than the skilled workforce pipeline. The 2025 AGC and NCCER workforce survey found that 92% of firms had difficulty filling hourly craft positions, and more than 75% specifically cited electricians, pipefitters, and plumbers as hard to recruit. Associated Builders and Contractors said the construction industry must attract 349,000 net new workers in 2026, which shows that current hiring flows are not enough to meet project demand. Data center construction worsens the strain because it pulls the most experienced electricians, commissioning specialists, and controls staff toward high-pay projects, leaving conventional commercial and institutional work with tighter labor pools. That imbalance raises bid premiums, extends schedules, and pushes owners toward larger contractors with prefabrication and workforce training systems. It also creates room for integrated delivery in the North America MEP services market because owners increasingly value firms that can solve labor coordination internally rather than depend on separate trade handoffs.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Building Performance and Energy Codes

- NEC and Utility-Driven Electrical Service Upgrades

- Switchgear, Transformer, and Copper Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electrical Services held 35% of the North America MEP services market size in 2025, which made it the largest type segment by revenue. That leadership reflects the fact that data centers, commercial retrofits, and electrification programs all place power distribution, controls, protection systems, and service upgrades near the center of project budgets. EMCOR's U.S. Electrical Construction segment generated USD 845.6 million in Q1 2026 revenue, up 12.8% year on year, and management linked that performance to high-tech manufacturing and data center activity, which supports the segment's near-term demand base. The 2026 NEC further supports the segment because new medium-voltage provisions, expanded labeling requirements, and power control system recognition raise billable design and field compliance work on commercial and institutional projects. Electrical Services also captures a large share of value when existing buildings shift toward heat pumps, chargers, storage, and more digital controls, since all of those changes affect service sizing and distribution architecture. In the North America MEP services market, that makes electrical scope both volume-led and complexity-led, which is a stronger position than relying on replacement demand alone.

Mechanical Services remains the second-largest type because HVAC, fire protection, process piping, and mission-critical cooling sit at the center of hospitals, advanced manufacturing plants, and data centers. Cooling design is becoming more complex as rack densities rise and owners move from standard air systems toward liquid-assisted or liquid-based cooling strategies, which raises the need for tighter coordination between piping, controls, power, and commissioning. Plumbing Services is smaller by revenue share, but it benefits from clear replacement cycles tied to water infrastructure work and lead service line programs, which gives it a steadier municipal demand base than many discretionary building categories. Integrated MEP Services is projected to grow at an 8.86% CAGR through 2031, the fastest pace among type segments in the North America MEP services market. Owners are leaning toward this model because one accountable delivery party reduces coordination gaps, shortens commissioning time, and lowers claims risk on complex facilities. That shift suggests the North America MEP services industry is rewarding firms that can combine trade depth with program management rather than firms that only provide isolated packages.

List of Companies Covered in this Report:

- EMCOR Group

- Comfort Systems USA

- Southland Industries

- M.C. Dean

- Rosendin Electric

- ArchKey Solutions

- TDIndustries

- Brandt

- McKinstry

- ACCO Engineered Systems

- Power Design

- Limbach Holdings

- AECOM

- WSP

- Jacobs

- Stantec

- Bowman Consulting Group

- Kimley-Horn

- Galloway & Company

- McGill Associates

- Prime Electric

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Federal and State Infrastructure Funding

- 4.2.2 Data Center and EV Charging Build-Out

- 4.2.3 Stricter Building Performance and Energy Codes

- 4.2.4 NEC and Utility-Driven Electrical Service Upgrades

- 4.2.5 Mission-Critical Cooling Redesign Complexity

- 4.2.6 Grid-Interactive Retrofit Demand in Secondary Cities

- 4.3 Market Restraints

- 4.3.1 Skilled Labor Shortages in Specialty Trades

- 4.3.2 Switchgear, Transformer, and Copper Price Volatility

- 4.3.3 Utility Interconnection Delays for Electrification-Heavy Projects

- 4.3.4 Cybersecurity Compliance Burden for Connected Building Systems

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Cost Structure Analysis

5 Market Size & Growth Forecasts (Value, in USD)

- 5.1 By Type

- 5.1.1 Mechanical Services

- 5.1.2 Electrical Services

- 5.1.3 Plumbing Services

- 5.1.4 Integrated MEP Services

- 5.2 By Service Type

- 5.2.1 Design & Engineering

- 5.2.2 Installation, Testing, and Commissioning

- 5.2.3 Maintenance, Repair, and Retrofit

- 5.2.4 Managed / Performance-based Services

- 5.3 By End-User Industry

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Infrastructure

- 5.4 By Geography

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 EMCOR Group

- 6.4.2 Comfort Systems USA

- 6.4.3 Southland Industries

- 6.4.4 M.C. Dean

- 6.4.5 Rosendin Electric

- 6.4.6 ArchKey Solutions

- 6.4.7 TDIndustries

- 6.4.8 Brandt

- 6.4.9 McKinstry

- 6.4.10 ACCO Engineered Systems

- 6.4.11 Power Design

- 6.4.12 Limbach Holdings

- 6.4.13 AECOM

- 6.4.14 WSP

- 6.4.15 Jacobs

- 6.4.16 Stantec

- 6.4.17 Bowman Consulting Group

- 6.4.18 Kimley-Horn

- 6.4.19 Galloway & Company

- 6.4.20 McGill Associates

- 6.4.21 Prime Electric

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment