|

시장보고서

상품코드

2064378

유럽의 기계, 전기, 배관(MEP) 서비스 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Europe Mechanical, Electrical, And Plumbing (MEP) Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

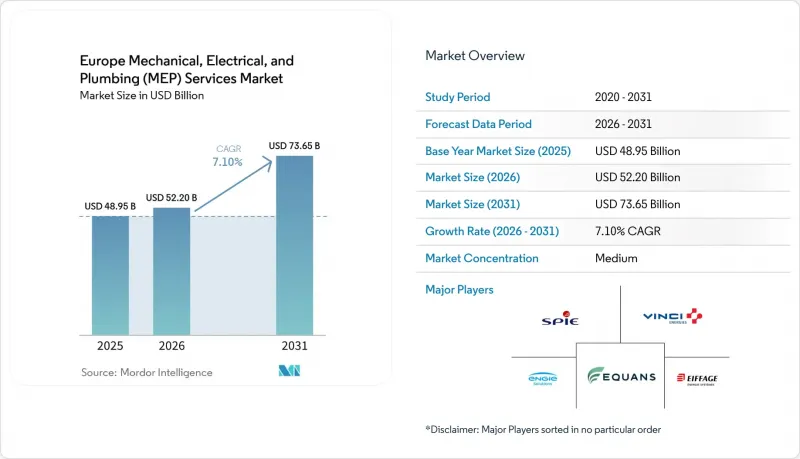

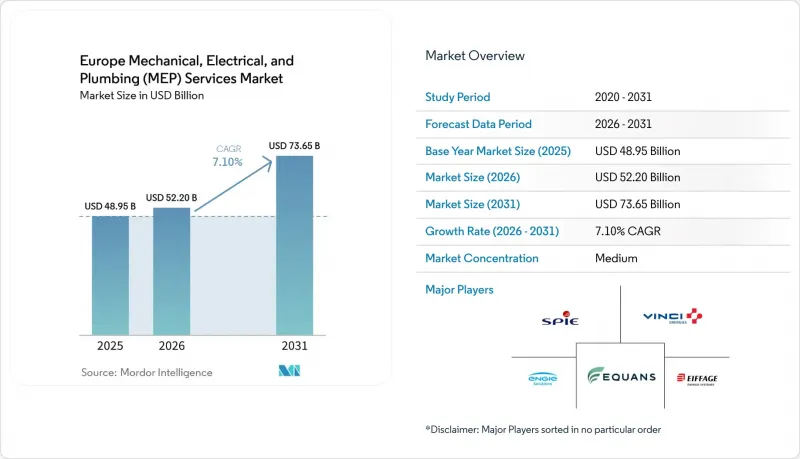

Mordor Intelligence에 의하면, 유럽의 기계, 전기, 배관(MEP) 서비스 시장 규모는 2025년에 489억 5,000만 달러로 평가되었고, 2026년 522억 달러로 추정되고, 2031년까지 736억 5,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 7.10%를 나타낼 전망입니다.

본 보고서는 유형별(기계, 전기, 배관, 통합 MEP), 서비스 유형별(설계 및 엔지니어링, 설치 및 시운전, 유지보수 및 개보수, 매니지드 서비스), 최종 사용자별(주거, 상업, 인프라), 지역별(독일, 영국, 프랑스, 스페인, 이탈리아, 네덜란드, 스웨덴, 덴마크, 노르웨이, 기타 유럽)로 분류되어 있습니다. 예상치는 금액(달러)으로 표시되어 있습니다.

유럽의 기계, 전기, 배관(MEP) 서비스 시장 동향 및 고찰

EPBD 개정 및 최소 에너지 성능 기준

개정된 EPBD는 현재 사이클에서 유럽의 기계, 전기, 배관(MEP) 서비스 시장에 있어 여전히 가장 강력한 정책적 촉진요인으로 작용하고 있습니다. 이에 따르면, 에너지 성능이 가장 낮은 비주거용 건축물의 16%를 2030년까지, 26%를 2033년까지 개보수해야 하며, 한편 주거용 건축물의 경우 1차 에너지 사용량의 평균을 2030년까지 16%, 2035년까지 20%에서 22%까지 감축해야 합니다. 가맹국들은 2025년 12월 31일까지 ‘국가 건축물 개보수 계획’ 초안을 제출해야 하며, 최종 계획은 2026년 12월 31일까지 제출될 예정이므로, 이를 통해 시공사 및 엔지니어링 기업들은 향후 업무량에 대해 보다 명확한 전망을 얻을 수 있게 됩니다. 이 규정 세트는 각국의 건축물 중 성능이 가장 낮은 부분부터 우선적으로 개선하도록 지시하고 있으며, MEP 분야에서 대규모 개입이 필요한 건축물이 집중적으로 발생하기 때문에 이전의 정책 주기보다 더욱 목표를 명확히 한 것입니다. 또한, 2021-2027년 EU의 에너지 효율화 자금도 대폭 확대되어 1,447억 유로(1,563억 달러)가 배정되었으며, 그중 794억 유로(858억 달러)에 해당하는 ‘회복·탄력성 기금(RRF)’ 자금이 건축물 분야에 배정되었습니다. 이로 인해 지역 전체 프로젝트의 자금 조달 가능성이 높아지고 있습니다. 이로 인해 유럽의 기계, 전기, 배관(MEP) 서비스 시장은 단기적인 신축 주기에 대한 의존도를 낮추고, 기존 자산의 규제 준수를 목적으로 한 개보수 공사에 대한 의존도를 높이게 될 것입니다.

화석 연료 보일러 중심의 개조를 대체하는 전기화

개정된 EPBD 제17조(15)에 따라 2025년 1월 1일부터 독립형 화석연료 보일러에 대한 재정 지원이 종료됨에 따라, 전기화가 유럽의 기계, 전기, 배관(MEP) 서비스 시장을 재편하고 있습니다. EU 내 히트펌프 판매 대수는 2024년 211만 대에서 2025년에는 234만 대로 회복되었으며, EU 회원국 13개국의 속보 데이터에 따르면 2025년 시장 성장률이 11%에 달한 것으로 나타났습니다. 이러한 변화로 인해 개보수 공사의 범위와 성격도 달라지고 있습니다. 왜냐하면 시공업체는 단순히 보일러를 교체하는 것뿐만 아니라, 전기 설비 업그레이드, 수력 균형 조정, 제어 시스템 통합 및 시운전이 필요하기 때문입니다. 독일이 계획하고 있는 GModG 체계는 현대화 규정을 더욱 엄격하게 하고, 저탄소 건축물에 대한 의무를 확대함으로써 한 차원 더 발전시키고 있습니다. 이를 통해 기술의 선택지가 발전하더라도, 개량 활동은 활발한 상태를 유지할 것입니다. EU 열펌프 가속화 플랫폼과 향후 도입될 건축물 대상 ETS2 제도는 이러한 방향성에 대한 추가적인 정책 지원을 제공할 것입니다. 유럽의 기계, 전기, 배관(MEP) 서비스 시장에 있어, 이는 수요가 더욱 복잡하고 고부가가치의 개보수 패키지로 이동하고 있음을 의미합니다.

인증 보수 기술자 부족

유럽의 기계, 전기, 배관(MEP) 서비스 시장에서 인력 확보는 여전히 가장 뚜렷한 공급 제약 요인으로 남아 있습니다. 유럽연합 집행위원회는 최소 75만 명의 열펌프 설치 기술자가 추가로 필요할 것이며, 현재 설치 기술자의 최소 50%는 열펌프 작업을 위해 재교육을 받아야할 것으로 추산하고 있습니다. 해당 정책 체계에서는 기술적 장벽과 원스톱 서비스 체계의 부재 또한 개보수 공사 시행에 있어 중대한 장애물로 인식되고 있으며, 이러한 제약이 제도적 측면과 운영적 측면 모두에 존재함을 보여주고 있습니다. 개보수 공사의 범위가 전기, 기계, 급배수 설비, 자동화, 제어 등 각 작업을 단일 프로젝트로 통합하는 경향이 강해지고 있어, 인력 부족 문제는 현재 더욱 심각해지고 있습니다. 또한, 자격 제도는 적격한 도급업체의 기반을 좁히기 때문에 기술적 품질은 향상되겠지만, 복잡한 규정 준수 중심의 프로젝트에 입찰할 수 있는 기업의 수는 줄어들 것입니다. 이로 인해 수요 자체는 유지되고 있지만, 유럽의 기계, 전기, 배관(MEP) 서비스 시장 전체에서 정책에 따른 수요가 수주 수익으로 전환되는 속도는 둔화되고 있습니다.

부문별 분석

2025년, 기계 설비 서비스는 유럽의 기계, 전기, 배관(MEP) 서비스 시장 점유율의 37%를 차지했으며, 해당 지역에서 가장 큰 부문이 되었습니다. 이러한 1위 순위는 현재의 정책 조합 하에서 HVAC 교체 주기, 히트펌프 도입, 지역 난방 개보수 공사가 모두 증가 추세를 보이고 있음을 반영하고 있습니다. 전기 및 배관 서비스는 현재 대부분의 에너지 효율 개선 공사에서 전력 설비 업그레이드, 제어 배선, 수력 균형 조정 및 급배수 설비 공사가 동일한 패키지에 포함되기 때문에 여전히 중요한 관련 분야로 남아 있습니다. 또한, 배관 서비스는 히트 펌프 및 저온 시스템으로의 재설계 전환으로부터도 혜택을 받고 있으며, 이 과정에서 물 측의 최적화는 핵심적인 엔지니어링 범위의 일부를 차지하고 있습니다. 이로 인해 유럽의 기계, 전기, 배관(MEP) 서비스 시장은 개별 장비 교체가 아닌 시스템 전체의 개보수와 밀접하게 연계된 상태를 유지하고 있습니다.

통합 MEP 서비스는 2031년까지 연평균 성장률(CAGR) 9.09%를 나타낼 것으로 예측되며, 이 부문에서 유럽의 기계, 전기, 배관(MEP) 서비스 시장 규모는 설계, 설치, 자동화, 시운전에 대해 단일 창구를 통한 책임을 요구하는 구매자가 늘어나고 있기 때문에 더욱 빠르게 확대되고 있습니다. 유럽의 기계, 전기, 배관(MEP) 서비스 업계에서 이러한 변화는 데이터센터, 생명과학 분야, 그리고 인터페이스 리스크가 비용 증가로 이어지는 기술적으로 고도의 공공 프로젝트에서 가장 두드러지게 나타납니다. 또한, 독일의 현대화 체계에 따라 자동화, 균형 조정, 성능 기준 준수를 하나의 계약에 통합한 종합적인 서비스 범위에 대한 수요가 증가하고 있습니다. VINCI Energies가 2025년에 독일의 Zimmer &Halbig 및 R+S를 인수한 사례는 주요 기업들이 단일 분야의 확장에만 의존하는 것이 아니라, 보다 심층적인 통합형 서비스 제공 역량을 구축하고 있음을 보여줍니다.

기타 혜택 :

- Excel 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the europe mechanical, electrical, and plumbing services market size was valued at USD 48.95 billion in 2025 and is estimated to grow from USD 52.20 billion in 2026 to reach USD 73.65 billion by 2031, at a CAGR of 7.10% during the forecast period (2026-2031).

This report is Segmented by Type (Mechanical, Electrical, Plumbing, Integrated MEP), Service Type (Design & Engineering, Installation & Commissioning, Maintenance & Retrofit, Managed Services), End-User (Residential, Commercial, Infrastructure), and Geography (Germany, UK, France, Spain, Italy, Netherlands, Sweden, Denmark, Norway, Rest of Europe). Forecasts are Provided in Terms of Value (USD).

Europe Mechanical, Electrical, And Plumbing (MEP) Services Market Trends and Insights

EPBD Recast and Minimum Energy Performance Standards

The recast EPBD remains the strongest policy driver for the Europe Mechanical, Electrical, and Plumbing (MEP) Services market in the current cycle. It requires renovating the worst-performing 16% of non-residential buildings by 2030 and 26% by 2033, while residential buildings must reduce average primary energy use by 16% by 2030 and by 20% to 22% by 2035. Member states were required to submit draft National Building Renovation Plans by December 31, 2025, and final plans are due by December 31, 2026, providing contractors and engineering firms with clearer visibility into future workloads. The rule set is more targeted than earlier policy cycles because it directs countries toward the worst-performing part of the stock first, creating a concentrated pool of buildings requiring deep MEP intervention. EU energy efficiency funding also expanded sharply for 2021 to 2027, with EUR 144.7 billion (USD 156.3 billion) allocated and EUR 79.4 billion (USD 85.8 billion) of Recovery and Resilience Facility funding directed to buildings, which improves project bankability across the region. This makes the Europe Mechanical, Electrical, and Plumbing (MEP) Services market less dependent on short new-build cycles and more dependent on compliance-led upgrades across existing assets.

Electrification Replacing Fossil Boiler-Led Retrofits

Electrification is reshaping the Europe Mechanical, Electrical, and Plumbing (MEP) Services market because financial support for stand-alone fossil fuel boilers ended from January 1, 2025 under Article 17(15) of the recast EPBD. Heat pump sales in the EU recovered to 2.34 million units in 2025 from 2.11 million units in 2024, and preliminary data from 13 EU member states pointed to 11% market growth in 2025. This shift changes the nature of retrofit scopes because contractors now need electrical upgrades, hydraulic balancing, controls integration, and commissioning rather than simple boiler replacements. Germany's planned GModG framework adds another layer by tightening modernization rules and expanding obligations for low-emission buildings, which keeps retrofit activity active even as technology choices evolve. The EU Heat Pump Accelerator Platform and the future ETS2 regime for buildings add further policy support to this direction of travel. For the Europe Mechanical, Electrical, and Plumbing (MEP) Services market, this means demand is shifting toward more complex, higher-value retrofit packages.

Shortage of Certified Retrofit Technicians

Labor availability remains the clearest delivery constraint for the Europe Mechanical, Electrical, and Plumbing (MEP) Services market. The European Commission estimates that at least 750,000 additional heat pump installers are needed, and at least 50% of current installers will need reskilling for heat pump work. The same policy framework also recognizes skills barriers and one-stop-shop gaps as material obstacles to renovation delivery, indicating that the constraint is both institutional and operational. Shortages matter more now because retrofit scopes increasingly combine electrical, mechanical, wet-services, automation, and controls work in a single project. Qualification schemes also narrow the eligible contractor base, thereby improving technical quality but reducing the number of firms that can bid for complex compliance-led projects. This keeps demand intact but slows conversion of policy demand into booked revenue across the Europe Mechanical, Electrical, and Plumbing (MEP) Services market.

Other drivers and restraints analyzed in the detailed report include:

- Building Automation and Digital EPC Rollout

- District and One-Stop-Shop Renovation Programs

- High Capex Across Fragmented Legacy Building Stock

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mechanical Services held 37% of the Europe Mechanical, Electrical, and Plumbing (MEP) Services market share in 2025, which made it the largest type segment in the region. This lead reflects HVAC replacement cycles, heat pump adoption, and district heating retrofit work that are all moving higher under the current policy mix. Electrical Services and Plumbing Services remain important adjacent volumes because most energy upgrades now involve power upgrades, controls wiring, hydraulic balancing, and wet-services work in the same package. Plumbing Services also benefits from the move toward heat pump and low-temperature system redesign, where water-side optimization becomes part of the core engineering scope. This keeps the Europe Mechanical, Electrical, and Plumbing (MEP) Services market firmly tied to whole-system retrofits rather than isolated equipment replacements.

Integrated MEP Services is projected to grow at a 9.09% CAGR through 2031, and the Europe Mechanical, Electrical, and Plumbing (MEP) Services market size for this segment is expanding faster because buyers want single-point responsibility for design, installation, automation, and commissioning. Within the Europe Mechanical, Electrical, and Plumbing (MEP) Services industry, this shift is most visible in data centers, life sciences, and technically demanding public projects where interface risk is costly. Germany's modernization framework is also increasing the need for bundled scopes that combine automation, balancing, and performance compliance in the same contract. VINCI Energies' 2025 acquisitions of Zimmer & Halbig and R+S in Germany show how major players are building deeper integrated delivery capacity rather than relying on single-trade expansion.

List of Companies Covered in this Report:

- SPIE

- VINCI Energies

- Equans

- ENGIE Solutions

- Eiffage Energie Systemes

- Bilfinger

- Exyte

- Ramboll

- Cundall

- Arup

- WSP

- AtkinsRealis

- AECOM

- Jacobs

- Mott MacDonald

- Stantec

- Mercury Engineering

- Dornan

- Bouygues Energies & Services

- Hochtief Engineering

- Arcadis

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EPBD Recast and Minimum Energy Performance Standards

- 4.2.2 Electrification Replacing Fossil Boiler-Led Retrofits

- 4.2.3 Building Automation and Digital EPC Rollout

- 4.2.4 District And One-Stop-Shop Renovation Programs

- 4.2.5 Smart Readiness Upgrades in Large Tertiary Buildings

- 4.2.6 Whole-Life Carbon Reporting Driving System Redesign

- 4.3 Market Restraints

- 4.3.1 Shortage of Certified Retrofit Technicians

- 4.3.2 High Capex Across Fragmented Legacy Building Stock

- 4.3.3 Split Incentives Between Landlords and Tenants

- 4.3.4 Data and Interoperability Compliance Burden for BACS

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Cost Structure Analysis

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Type

- 5.1.1 Mechanical Services

- 5.1.2 Electrical Services

- 5.1.3 Plumbing Services

- 5.1.4 Integrated MEP Services

- 5.2 By Service Type

- 5.2.1 Design & Engineering

- 5.2.2 Installation, Testing, and Commissioning

- 5.2.3 Maintenance, Repair, and Retrofit

- 5.2.4 Managed / Performance-based Services

- 5.3 By End-User Industry

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Infrastructure

- 5.4 By Geography

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Spain

- 5.4.5 Italy

- 5.4.6 Netherlands

- 5.4.7 Sweden

- 5.4.8 Denmark

- 5.4.9 Norway

- 5.4.10 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 SPIE

- 6.4.2 VINCI Energies

- 6.4.3 Equans

- 6.4.4 ENGIE Solutions

- 6.4.5 Eiffage Energie Systemes

- 6.4.6 Bilfinger

- 6.4.7 Exyte

- 6.4.8 Ramboll

- 6.4.9 Cundall

- 6.4.10 Arup

- 6.4.11 WSP

- 6.4.12 AtkinsRealis

- 6.4.13 AECOM

- 6.4.14 Jacobs

- 6.4.15 Mott MacDonald

- 6.4.16 Stantec

- 6.4.17 Mercury Engineering

- 6.4.18 Dornan

- 6.4.19 Bouygues Energies & Services

- 6.4.20 Hochtief Engineering

- 6.4.21 Arcadis

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment