|

시장보고서

상품코드

2064379

중동 및 북아프리카의 기계, 전기, 배관(MEP) 서비스 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Middle East And North Africa Mechanical, Electrical, And Plumbing (MEP) Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

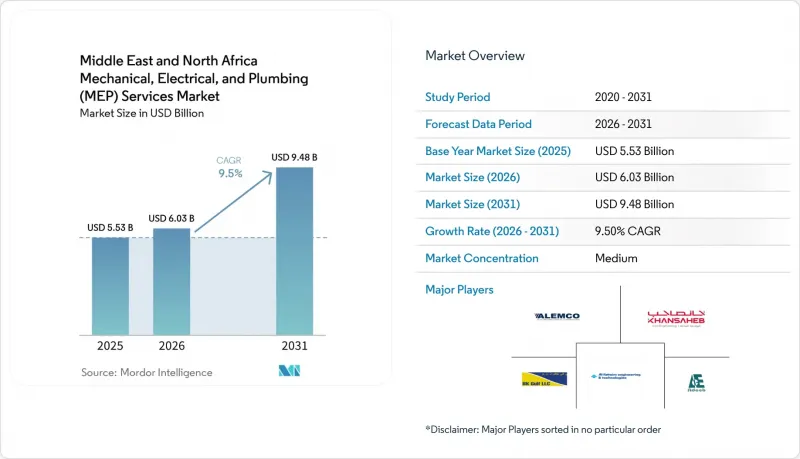

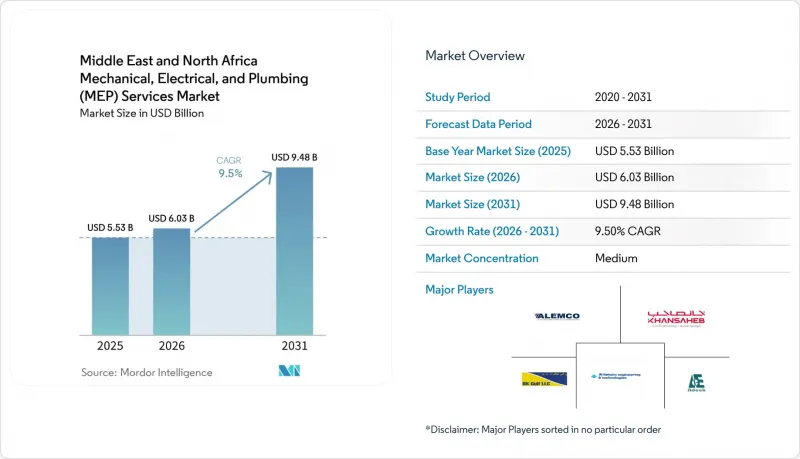

Mordor Intelligence에 의하면, 중동 및 북아프리카(MENA)의 기계, 전기, 배관(MEP) 서비스 시장 규모는 2025년에 55억 3,000만 달러로 평가되었고, 2026년에 60억 3,000만 달러로 추정되고, 2031년까지 94억 8,000만 달러에 이를 것으로 예측됩니다.

2026-2031년 연평균 성장률(CAGR) 9.5%로 성장할 것으로 전망됩니다.

본 보고서는 유형별(기계, 전기, 배관, 통합 MEP 서비스), 서비스 유형별(설계 및 엔지니어링, 설치, 시험 및 시운전, 유지보수 및 수리, 기타), 최종 사용자 산업별(주택, 상업, 인프라), 지역별(사우디아라비아, UAE, 이집트, 튀르키예, 모로코, 기타 MENA 국가)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

중동 및 북아프리카의 기계, 전기, 배관(MEP) 서비스 시장 동향 및 고찰

사우디아라비아의 기가 프로젝트와 UAE의 복합 애플리케이션 개발 확대

사우디아라비아의 기가 프로젝트 활동은 프로젝트 소유주가 매우 대규모인 프로그램 전체에 걸쳐 더욱 엄격한 공정 관리와 실현 가능성 검증을 수행하고 있음에도 불구하고, MENA 지역의 MEP 서비스 시장에서 여전히 가장 큰 수요 원천으로 자리 잡고 있습니다. 2030년 리야드 엑스포와 2034년 FIFA 월드컵으로 인해 단기 계약 패키지는 명확한 납기 마일스톤과 연계되어 있으며, 그 결과 진행 중인 프로젝트는 ‘표제’ 중심이라기보다는 ‘실행’ 중심의 경향이 강해지고 있습니다. UAE에서는 복합 용도 및 목적지 프로젝트에 힘입어 MENA 지역의 MEP 서비스 시장이 상업, 레저, 호텔 및 관광, 주거 등 다양한 형태로 확대되고 있으며, 단일 프로젝트 유형에 대한 의존도가 낮아지고 있습니다. 또한, 사우디아라비아의 고객사는 국내 부가가치 창출 요건을 더욱 적극적으로 적용하고 있으며, 이에 따라 경쟁 구도는 국내 생산 능력, 인재 양성 능력, 그리고 프로젝트 수행 역량을 갖춘 시공사 쪽으로 이동하고 있습니다. 이 시장 분야에서는 여전히 규모가 중요하지만, 현재는 발표된 프로젝트의 규모보다 실행력에 대한 신뢰성이 더 중요시되고 있습니다.

데이터센터, 지역 냉방 및 미션 크리티컬 수요

데이터센터, 지역 냉방 및 기타 미션 크리티컬 프로젝트는 초기 설계 단계부터 보다 심층적인 시스템 통합을 필요로 하기 때문에 MENA 지역의 MEP 서비스 시장 내 사업 구성을 변화시키고 있습니다. 랙 밀도가 높아짐에 따라 설계자들은 기존의 상업용 건물에서 일반적으로 요구되는 것보다 더 복잡한 전원 이중화, 액체 냉각 전략 및 백업 시스템을 마련해야 합니다. 이에 따라 가치는 조달 결정이 확정된 후 설치 단계에서 수정하는 데 의존하기보다는 조기에 기계 및 전기 분야의 범위를 조정할 수 있는 엔지니어나 도급업체로 전환되고 있습니다. 또한, 지역 냉방 플랜트와 네트워크 배관은 대규모 기계 설비가 유틸리티 및 공공 인프라와 병행하여 도입되는 종합적인 도시 개발 계획과 MENA 지역의 MEP 서비스 시장을 연결하고 있습니다. 이러한 수요 흐름은 디지털 인프라, 유틸리티 계획, 도시 서비스 플랫폼과 연동되어 있기 때문에 단기적인 부동산 시장 동향의 영향을 덜 받는 경향이 있습니다.

숙련된 노동자와 엔지니어링 인력 부족

숙련된 노동자와 엔지니어링 인력의 부족은 MENA 지역의 MEP 서비스 시장에서 여전히 구조적인 제약 요인으로 남아 있습니다. 이는 복잡한 시스템을 관리하고 구축할 수 있도록 훈련받은 인력 공급이 프로젝트 물량 증가를 따라가지 못하고 있기 때문입니다. 이 지역에서는 감독자, 프로젝트 매니저, 시운전 전문가, 공인 설치 기술자 등이 필요하지만, 이러한 인재를 양성하는 데는 시간이 걸리기 때문에 프로젝트 일정이 촉박해지면 쉽게 대체할 수 없습니다. MEP 하도급업체가 예정대로 현장에 인력을 배치하지 못할 경우, 원청업체는 일정 지연을 감수할 수밖에 없게 되며, 이는 프로젝트 체인 전반에 걸쳐 클레임 위험의 확대로 이어지게 됩니다. 또한 일부 시장에서는 HVAC 및 관련 직종에서 설치 업체의 자격 요건이 완전히 표준화되지 않아, 기술력의 편차가 품질상의 문제로 대두되고 있습니다. 사내 연수 센터나 현장에서 표준화된 프로세스에 투자하는 기업은 위험을 줄일 수 있지만, MENA 지역의 MEP 서비스 시장 전체적으로는 여전히 심각한 인력 부족이 지속되고 있습니다.

부문별 분석

2025년, 기계 설비 서비스는 MENA 지역의 MEP 서비스 시장 점유율의 48.3%를 차지했으며, 다른 부문들을 크게 앞지르며 최대 부문이 되었습니다. 해당 지역의 지속적인 냉방 수요로 인해 상업용 빌딩, 주택 단지, 호텔, 교통 인프라, 공공시설에서 HVAC 관련 작업이 필수적이며, 이는 신축 및 리모델링 양쪽 사이클을 통해 대규모 기계 설비 패키지에 대한 수요를 뒷받침하고 있습니다. 데이터센터, 스마트 빌딩 시스템, 비상 전원 시스템 및 저전압 네트워크가 신규 프로젝트에서 시스템 전체의 복잡성을 가중시키고 있기 때문에 전기 서비스 부문은 여전히 2위 자리를 유지했습니다. 배관 서비스는 해수 담수화 관련 네트워크, 절수 의무, 그리고 기존 자산에서의 처리수 재이용 확산에 힘입어 수요가 뒷받침되며 안정적인 추세를 보였습니다.

통합 MEP 서비스는 2026-2031년 연평균 성장률(CAGR) 12.1%를 나타낼 것으로 예측되며, 이는 MENA 지역 MEP 서비스 업계의 각 부문 중 가장 빠른 성장 속도입니다. 복합 용도 시설, 호텔·리조트 시설, 인프라 및 기가 프로젝트 분야에서 마스터 개발사는 기계, 전기, 배관 각 분야에 걸친 단일 계약을 통한 책임 체계를 점점 더 선호하는 추세입니다. 이는 특정 시스템의 조정 실패가 인계 시점에 다른 여러 시스템의 지연을 초래할 가능성이 있기 때문입니다. 미션 크리티컬 시스템, 지능형 저전압 설비, 신속한 납품을 지원할 수 있는 전문 팀을 보유한 공급업체는 이러한 변화로 인해 혜택을 볼 수 있는 유리한 위치에 있습니다. 특히, 프로젝트 소유자가 인터페이스 축소나 보다 엄격한 일정 관리를 요구하는 경우입니다. 또한, 통합형 배송 방식은 더욱 엄격해진 에너지 성능에 대한 기대에도 부응합니다. 왜냐하면 시스템 전반에 걸친 모델링, 시험, 시운전은 단일 주계약자 하에서 관리하는 편이 더 쉽기 때문입니다.

기타 혜택 :

- Excel 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the middle east and north africa mechanical, electrical, and plumbing services market size is projected to be USD 5.53 billion in 2025, USD 6.03 billion in 2026, and reach USD 9.48 billion by 2031, growing at a CAGR of 9.5% from 2026 to 2031.

This report is Segmented by Type (Mechanical, Electrical, Plumbing, Integrated MEP Services), Service Type (Design & Engineering, Installation Testing & Commissioning, Maintenance & Repair, Other), End-User Industry (Residential, Commercial, Infrastructure), and Geography (Saudi Arabia, UAE, Egypt, Turkey, Morocco, Rest of MENA). The Market Forecasts are Provided in Terms of Value (USD).

Middle East And North Africa Mechanical, Electrical, And Plumbing (MEP) Services Market Trends and Insights

Saudi Giga-Projects and UAE Mixed-Use Expansion

Saudi giga-project activity remains the largest demand engine in the MENA MEP services market, even as project owners apply tighter sequencing and feasibility checks across very large programs. Expo 2030 Riyadh and the 2034 FIFA World Cup keep near-term packages tied to visible delivery milestones, which makes the active pipeline more execution-led than headline-led. In the UAE, mixed-use and destination projects keep the MENA MEP services market broad across commercial, leisure, hospitality, and residential formats, which reduces dependence on a single project class. Saudi clients are also applying in-country value requirements more actively, and that is shifting competition toward contractors with local manufacturing, training capacity, and delivery depth inside the Kingdom. Scale still matters in this part of the market, but execution credibility now matters more than announced project value.

Data-Center, District-Cooling, and Mission-Critical Demand

Data-center, district-cooling, and other mission-critical projects are changing the mix of work in the MENA MEP services market because they require deeper system integration from the first design stage. Higher rack densities are pushing designers toward more complex power redundancy, liquid-cooling strategies, and backup systems than conventional commercial buildings usually require. This shifts value toward engineers and contractors that can coordinate mechanical and electrical scopes early, rather than rely on late installation fixes after procurement decisions are already locked in. District-cooling plants and network pipework also keep the MENA MEP services market tied to master-planned urban developments where large mechanical packages move in parallel with utilities and public infrastructure. These demand streams are less exposed to short-term real estate sentiment because they are linked to digital infrastructure, utility planning, and urban service platforms.

Skilled-Labor and Engineering Talent Shortages

Skilled labor and engineering shortages remain a structural limit on the MENA MEP services market because project volume is rising faster than the supply of trained people who can manage and install complex systems. The regional pipeline needs more supervisors, project managers, commissioning specialists, and certified installers, but that workforce takes time to build and is not easily replaced once project schedules compress. When MEP subcontractors cannot staff work fronts on time, main contractors absorb schedule slippage and wider claims exposure across the full project chain. Skill inconsistency is also a quality issue because some markets still lack fully standardized installer qualification requirements across HVAC and related trades. Companies that invest in internal training centers and repeatable site processes are better protected, but the workforce gap remains material across the MENA MEP services market.

Other drivers and restraints analyzed in the detailed report include:

- Energy-Efficiency Retrofits in Cooling-Intensive Buildings

- BIM-Led Design Coordination and Modular MEP Uptake

- Material Lead Times and Aggressive Price Competition

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mechanical Services held 48.3% of the MENA MEP services market share in 2025, which made it the largest type segment by a wide margin. The region's sustained cooling load keeps HVAC-related work essential across commercial buildings, residential compounds, hotels, transport assets, and public facilities, which supports large mechanical packages through both new build and retrofit cycles. Electrical Services remained the second-largest segment because data centers, smart-building systems, backup power architecture, and low-voltage networks are expanding overall system complexity in new projects. Plumbing Services stayed steady, with demand supported by desalination-linked networks, water-efficiency mandates, and wider adoption of treated-water reuse in built assets.

Integrated MEP Services is projected to grow at a 12.1% CAGR from 2026 to 2031, the fastest pace among type segments in the MENA MEP services industry. Master developers increasingly prefer single-contract accountability across mechanical, electrical, and plumbing scopes on mixed-use, hospitality, infrastructure, and giga-project programs, because coordination failures on one system can delay several others at handover. Providers with specialist teams across mission-critical systems, intelligent low-voltage work, and fast-track delivery are well positioned to benefit from this shift, particularly where project owners want fewer interfaces and tighter schedule control. Integrated delivery also aligns with stricter energy-performance expectations because cross-system modeling, testing, and commissioning are easier to manage under one lead contractor.

List of Companies Covered in this Report:

- BK Gulf

- ALEMCO

- Al-Futtaim Engineering & Technologies

- Khansaheb MEP

- Adeeb Group

- AG Engineering

- Al Shafar United

- Menasco Mechanical Contracting

- Voltas Limited

- Orascom Construction

- International Electromechanical Services

- Drake & Scull Engineering

- ETA Engineering

- KEO International Consultants

- Dar Al-Handasah

- Jacobs

- AECOM

- WSP Global

- AtkinsRealis

- Cundall

- Buro Happold

- Khatib & Alami

- Johnson Controls Arabia

- JLW Middle East

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Saudi Giga-Projects and UAE Mixed-Use Expansion

- 4.2.2 Data-Center, District-Cooling, and Mission-Critical Demand

- 4.2.3 Energy-Efficiency Retrofits in Cooling-Intensive Buildings

- 4.2.4 BIM-Led Design Coordination and Modular MEP Uptake

- 4.2.5 Airport, Tourism, and New-City Build-Outs in North Africa

- 4.2.6 Water Reuse, Desalination Linkage, and High-Efficiency Plumbing Needs

- 4.3 Market Restraints

- 4.3.1 Skilled-Labor and Engineering Talent Shortages

- 4.3.2 Material Lead Times and Aggressive Price Competition

- 4.3.3 Payment-Certification Delays and Claims-Management Risk

- 4.3.4 Geopolitical and Security Volatility in Select Markets

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Cost Structure Analysis

5 Market Size & Growth Forecasts (Value, in USD)

- 5.1 By Type

- 5.1.1 Mechanical Services

- 5.1.2 Electrical Services

- 5.1.3 Plumbing Services

- 5.1.4 Integrated MEP Services

- 5.2 By Service Type

- 5.2.1 Design & Engineering

- 5.2.2 Installation, Testing, and Commissioning

- 5.2.3 Maintenance & Repair

- 5.2.4 Other Services

- 5.3 By End-User Industry

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Infrastructure

- 5.4 By Geography

- 5.4.1 Saudi Arabia

- 5.4.2 United Arab Emirates

- 5.4.3 Egypt

- 5.4.4 Turkey

- 5.4.5 Morocco

- 5.4.6 Rest of Middle East and North Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 BK Gulf

- 6.4.2 ALEMCO

- 6.4.3 Al-Futtaim Engineering & Technologies

- 6.4.4 Khansaheb MEP

- 6.4.5 Adeeb Group

- 6.4.6 AG Engineering

- 6.4.7 Al Shafar United

- 6.4.8 Menasco Mechanical Contracting

- 6.4.9 Voltas Limited

- 6.4.10 Orascom Construction

- 6.4.11 International Electromechanical Services

- 6.4.12 Drake & Scull Engineering

- 6.4.13 ETA Engineering

- 6.4.14 KEO International Consultants

- 6.4.15 Dar Al-Handasah

- 6.4.16 Jacobs

- 6.4.17 AECOM

- 6.4.18 WSP Global

- 6.4.19 AtkinsRealis

- 6.4.20 Cundall

- 6.4.21 Buro Happold

- 6.4.22 Khatib & Alami

- 6.4.23 Johnson Controls Arabia

- 6.4.24 JLW Middle East

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment