|

시장보고서

상품코드

2064004

남미의 기계, 전기, 배관(MEP) 서비스 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)South America Mechanical, Electrical, And Plumbing (MEP) Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

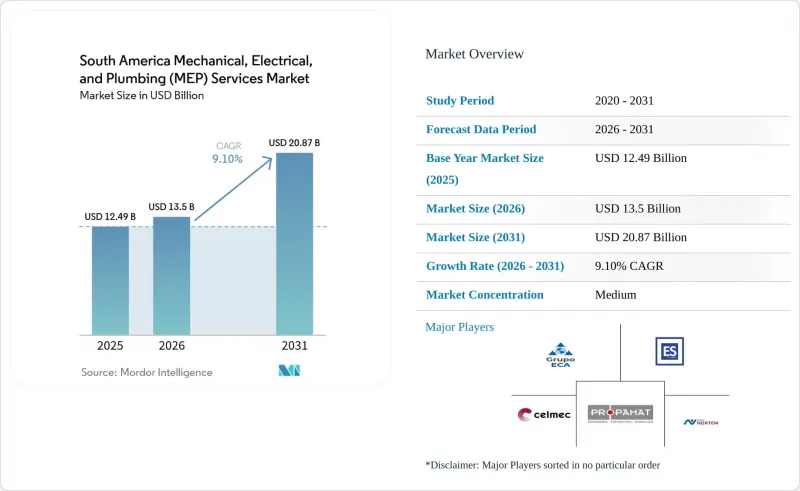

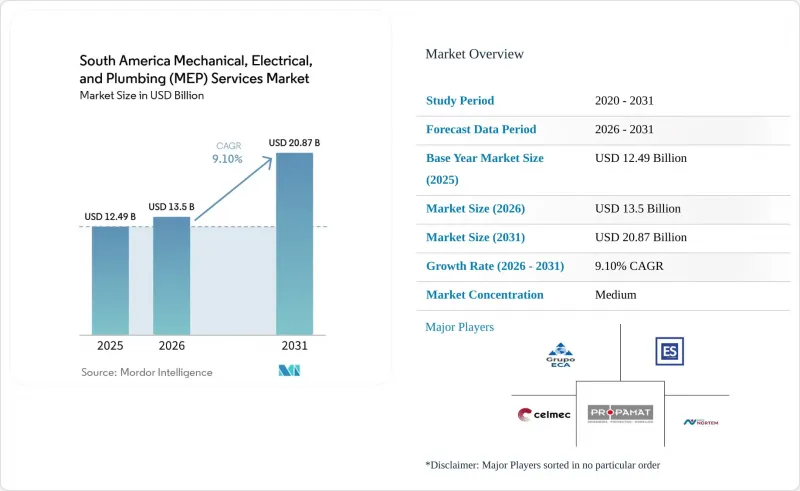

Mordor Intelligence에 의하면, 남미의 기계, 전기, 배관(MEP) 서비스 시장 규모는 2025년 124억 9,000만 달러로 평가되었고, 2026년에는 135억 달러로 추정되고, 2026-2031년 CAGR 9.10%로 성장을 지속할 전망이며, 2031년까지 208억 7,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 유형별(기계, 전기, 배관, 통합 MEP), 서비스 유형별(설계 및 엔지니어링, 설치, 시험 및 시운전, 유지보수, 수리 및 개보수, 관리형 및 성과보수형), 최종 사용자 산업별(주택, 상업, 인프라), 지역별(브라질, 아르헨티나, 칠레, 콜롬비아, 페루, 기타 남미 국가)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

남미의 기계, 전기, 배관(MEP) 서비스 시장 동향 및 인사이트

상업시설 및 인프라의 현대화

남미의 기계, 전기, 배관(MEP) 서비스 시장은 해당 지역의 교통, 의료, 상수도, 도시 자산 분야에서 진행 중인 광범위한 현대화 주기에 힘입어 꾸준한 성장을 이어가고 있습니다. 브라질의 건설 부문은 GDP의 6%에 가까운 비중을 차지하고 있으며, PAC-3는 교통, 에너지, 상수도, 도시 이동성에 3,330억 달러를 투자하겠다고 약속하고 있어, 이는 병원, 공항, 지하철 시스템 및 위생 시설 분야에서 다년간에 걸친 MEP 하도급 기회로 이어지고 있습니다. 브라질 이외의 지역에서도 비슷한 추세가 나타나고 있으며, 2024년에는 AECOM의 합작 회사가 페루 보건부로부터 선정되어 피우라와 토루히요에 위치한 두 곳의 주요 지역 병원의 관리를 맡게 되었습니다. 이 회사는 BIM 중심의 모델에 따라 MEP의 전체 수명 주기에 걸친 책임을 맡고 있습니다. 또한, LEED 인증을 획득한 건물 수에서 브라질이 세계 상위 5위권에 든 것은 감사 가능한 MEP 성능의 중요성을 더욱 부각시키고 있습니다. 왜냐하면 인증은 더 이상 단순한 설비 설치 완료에 그치는 것이 아니라, 시스템의 성과에 좌우되게 되었기 때문입니다. 이에 따라 남미의 기계, 전기, 배관(MEP) 서비스 시장에서 계약 기간이 연장됨에 따라, 인도 후에도 모니터링, 재시운전, 에너지 최적화를 통해 지속적으로 관여할 수 있는 기업의 가치가 높아지고 있습니다. 또한, 남미의 기계, 전기, 배관(MEP) 서비스 시장이 일회성 건설 주기에 얽매이는 경우가 줄어들고, 지속적인 건물 성능 의무와 더욱 밀접하게 연계되어 있음을 의미합니다.

데이터센터 및 물류 시설의 확장

남미의 기계, 전기, 배관(MEP) 서비스 시장은 브라질과 칠레에서 진행 중인 데이터센터 단지 및 현대식 물류 시설의 확장에 힘입어 성장하고 있습니다. 칠레의 ‘2024년부터 2030년까지의 국가 데이터센터 계획’은 해당 부문의 규모를 3배로 확대하는 것을 목표로 하고 있으며, 2025년 이후 하이퍼스케일러들의 투자액은 80억 달러를 넘어설 것으로 예측됩니다. 이로 인해 냉각, 전력 품질, 비상 발전 및 소화 시스템 패키지에 대한 지속적인 수요가 창출될 것입니다. AI를 중시하는 데이터센터에서는 랙당 10kW였던 기존의 설계 조건에서 랙당 100kW의 밀도로 전환되고 있으며, 이를 위해서는 액체 냉각 루프, 고전압 버스웨이, N+1 중복 구성이 적용된 칠러가 필요합니다. 이러한 변화로 인해 고밀도 기계 및 전기 패키지를 제공하면서 성능상의 문제 없이 시운전을 완료할 수 있는 도급업체의 수가 줄어들고 있습니다. 그 결과, 남미의 기계, 전기, 배관(MEP) 서비스 시장에서는 일반 공급업체와 고밀도 디지털 캠퍼스에 대응할 수 있는 전문 시공업체 간의 격차가 확대되고 있습니다. 이와 유사한 변화는 인접한 물류 시설로도 확산되고 있으며, 사업자들 사이에서는 시운전 시 장애 내성이 뛰어난 전력 시스템, 첨단 환기 시스템, 그리고 자동화에 대응할 수 있는 서비스 프레임워크를 요구하는 목소리가 점점 더 커지고 있습니다.

환율 변동과 인플레이션 압력

환율 변동성과 자금 조달 비용은 남미의 기계, 전기, 배관(MEP) 서비스 시장에서 여전히 사업 운영에 큰 걸림돌이 되고 있습니다. 브라질의 세릭 금리는 2025년 5월 14.8%에 달했으며, OECD는 점진적인 완화만 예상하고 있어 고객의 차입 비용은 높은 수준을 유지하고 있으며, 수입 장비에 의존하는 고정 가격 프로젝트에서 시공사들의 이익률을 압박하고 있습니다. PVC 파이프 가격은 2026년 2월까지의 12개월 동안 이미 16.3% 상승했으며, 건설 비용 인플레이션으로 인해 2026년 INCC(건설 비용 지수)는 9.7%에 달할 가능성이 있습니다. 이로 인해, 해당 자재 가격이 상승하기 전에 체결된 계약에 추가적인 압박이 가해질 것입니다. 이러한 영향은 달러에 연동되는 부품이나 헤지 비용에 의존하는 재생에너지, 디지털 인프라, 기타 MEP 비중이 높은 프로젝트에서 특히 두드러집니다. 남미의 기계, 전기, 배관(MEP) 서비스 시장에서 조달 팀이 비용 변동을 신속하게 전가하지 못할 경우, 공사 지연, 공사 범위 축소 또는 입찰 조건의 강화로 이어질 가능성이 있습니다. 아르헨티나에서는 통화 가치 하락으로 인해 기존 솔루션에 비해 높은 자본 지출(CAPEX)이 필요한 MEP 시스템의 현지 비용이 급격히 상승하고 있어, 이러한 압박이 더욱 심화되고 있습니다. 이로 인해 구매자들은 업그레이드가 아닌 도입 연기를 선택할 가능성이 높아질 수 있습니다.

부문별 분석

2025년, 남미의 기계, 전기, 배관(MEP) 서비스 시장에서 기계 서비스는 37%의 점유율을 차지했으며, 서비스 유형별로는 가장 큰 부문을 형성했습니다. 이러한 위상은 상업용 빌딩, 의료시설, 디지털 인프라 전반에 걸쳐 공조(HVAC), 냉동 및 산업용 공정 냉각 설비의 도입 기반이 광범위하게 마련되어 있음을 반영합니다. 남미의 기계, 전기, 배관(MEP) 서비스 시장은 브라질의 열대 기후에 따른 운영 조건과 고가용성 시설의 냉각 수요로 인해 열 관리가 프로젝트 설계 및 유지보수의 핵심으로 자리 잡고 있어, 계속해서 기계 분야에 중점을 두고 있습니다. 또한, 브라질에서는 여전히 위생 시설의 격차가 심각하며, 인구의 47%가 하수도망에 연결되어 있지 않기 때문에 상수도 및 하수도 관련 개보수 및 네트워크 공사에 대한 수요가 지속되고 있어, 배관 서비스도 계속해서 중요한 위치를 차지하고 있습니다. 통합형 MEP 서비스는 가장 빠르게 성장하는 분야로, 고객이 기계, 전기, 배관 각 분야의 도급업체를 개별적으로 조율하는 데 드는 비용과 위험을 줄여감에 따라 2031년까지 연평균 성장률(CAGR) 11.7%로 확대될 것으로 전망됩니다.

남미의 기계, 전기, 배관(MEP) 서비스 업계에서 통합 계약의 부상은 다양한 분야의 현장 팀을 동원하여 설계, 설치, 시험, 시운전을 단일 계약 범위 내에서 일관되게 관리할 수 있는 기업에 이점을 가져다주고 있습니다. 이러한 변화는 데이터센터 사업 분야에서 더욱 두드러지게 나타나고 있으며, 고밀도 홀의 경우 개별 패키지 납품이 아닌 냉각 루프, 배전, 수처리 시스템의 동시 재설계가 요구되고 있습니다. 또한, 빌딩 소유주들도 통합형 계약을 활용하여 인터페이스 관련 분쟁을 줄이고, 인계 주기를 단축하며, 3개사가 아닌 1개공급업체로부터 성능 보증을 확보하고자 하고 있습니다. 이로 인해 남미의 기계, 전기, 배관(MEP) 서비스 시장에서 라이프사이클 대응 능력을 갖춘 기업과 개별 시공 패키지만으로 경쟁하는 기업 간의 격차가 확대되고 있습니다. 그 결과, 기계 설비의 전문성, 전기 설비의 신뢰성, 배관 설비의 통합, 그리고 정식 시운전 체계를 하나의 체계적인 제안으로 결합할 수 있는 시공사에게 더 유리한 성장의 길이 열리고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the south america mechanical, electrical, and plumbing services market size is expected to grow from USD 12.49 billion in 2025 to USD 13.5 billion in 2026 and is forecast to reach USD 20.87 billion by 2031 at 9.10% CAGR over 2026-2031.

This report is Segmented by Type (Mechanical, Electrical, Plumbing, Integrated MEP), Service Type (Design & Engineering, Installation/Testing/Commissioning, Maintenance/Repair/Retrofit, Managed/Performance-based), End-User Industry (Residential, Commercial, Infrastructure), and Geography (Brazil, Argentina, Chile, Colombia, Peru, Rest of South America). The Market Forecasts are in Terms of Value (USD).

South America Mechanical, Electrical, And Plumbing (MEP) Services Market Trends and Insights

Commercial and Infrastructure Modernization

The South America mechanical, electrical, and plumbing (MEP) services market is drawing steady support from the region's wider modernization cycle in transport, health, water, and urban assets. Brazil's construction sector contributes close to 6% of GDP, and PAC-3 has committed USD 333 billion across transport, energy, water, and urban mobility, which is converting into multi-year MEP subcontract opportunities in hospitals, airports, metro systems, and sanitation plants. The same pattern is visible outside Brazil, where AECOM's joint venture was selected by Peru's Ministry of Health in 2024 to manage two major regional hospitals in Piura and Trujillo with responsibility across the MEP lifecycle under a BIM-led model. Brazil's position among the top five countries globally for LEED-certified buildings is also deepening the role of auditable MEP performance, because certification now depends on system outcomes rather than simple installation completion. This is extending the life of contracts in the South America mechanical, electrical, and plumbing (MEP) services market and raising the value of firms that can stay involved after handover through monitoring, recommissioning, and energy optimization. It also means that the South America mechanical, electrical, and plumbing (MEP) services market is becoming less tied to one-time construction cycles and more linked to ongoing building performance obligations.

Data Center and Logistics Facility Expansion

The South America mechanical, electrical, and plumbing (MEP) services market is gaining from the expansion of data center campuses and modern logistics facilities in Brazil and Chile. Chile's National Data Center Plan for 2024 to 2030 aims to triple the size of the sector, and projected hyperscaler investment from 2025 onward exceeds USD 8 billion, creating a sustained pipeline for cooling, power quality, backup generation, and fire suppression packages. These facilities are no longer being designed around traditional 10 kW per rack conditions, as AI-oriented halls are moving toward 100 kW per rack densities that require liquid-cooling loops, higher-voltage busways, and N+1 redundant chillers. That change is narrowing the pool of contractors capable of delivering dense mechanical and electrical packages and completing commissioning without performance failures. The South America mechanical, electrical, and plumbing (MEP) services market is therefore seeing a wider gap between standard installation vendors and specialized contractors that can work on high-density digital campuses. The same shift is spilling into adjacent logistics facilities, where operators increasingly want resilient power systems, advanced ventilation, and automation-ready service frameworks at commissioning.

FX Volatility and Inflation Pressure

FX volatility and financing costs remain a major operational brake on the South America mechanical, electrical, and plumbing (MEP) services market. Brazil's Selic rate reached 14.8% in May 2025 and the OECD expects only gradual easing, which keeps borrowing costs high for clients and compresses contractor returns on fixed-price projects that rely on imported equipment. PVC pipe prices were already up 16.3% in the 12 months to February 2026, and construction cost inflation could push the INCC to 9.7% in 2026, which puts further pressure on contracts signed before those inputs moved higher. The effect is especially visible in renewables, digital infrastructure, and other MEP-heavy projects that depend on dollar-linked components and hedging costs. In the South America mechanical, electrical, and plumbing (MEP) services market, this can lead to delayed starts, smaller scopes, or tighter bid discipline when procurement teams cannot pass cost changes through quickly. Argentina intensifies the pressure because depreciation sharply increases the local cost of high-CAPEX MEP systems relative to legacy solutions, which can shift buyers toward deferral rather than upgrade.

Other drivers and restraints analyzed in the detailed report include:

- Outsourcing of Hard Services and Lifecycle Maintenance

- Chile and Brazil Power-Linked Campus Development

- Labor Informality and Uneven Execution Quality

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mechanical Services held 37% of the South America mechanical, electrical, and plumbing (MEP) services market share in 2025, which made it the largest service cluster by type. That position reflects the large installed base of HVAC, refrigeration, and industrial process cooling equipment across commercial buildings, healthcare facilities, and digital infrastructure. The South America mechanical, electrical, and plumbing (MEP) services market continues to lean toward mechanical scopes because tropical operating conditions in Brazil and the cooling demands of high-availability facilities keep thermal management at the center of project design and maintenance. Plumbing services also retain solid relevance because Brazil still faces a major sanitation gap, with 47% of the population not connected to the sewage system, which sustains demand for water and wastewater-related retrofits and network work. Integrated MEP Services is the fastest-growing type and is projected to expand at 11.7% CAGR through 2031 as clients reduce the cost and risk of coordinating separate mechanical, electrical, and plumbing contractors.

Within the South America mechanical, electrical, and plumbing (MEP) services industry, the rise of integrated contracts is rewarding firms that can mobilize multi-discipline site teams and keep design, installation, testing, and commissioning aligned under one scope. The shift is becoming more visible in data center work, where high-density halls require simultaneous redesign of cooling loops, electrical distribution, and water management systems rather than isolated package delivery. Building owners are also using integrated contracts to reduce interface disputes, shorten handover cycles, and secure performance guarantees from one provider instead of three. That is widening the gap between firms with lifecycle capability and those that only compete on discrete installation packages in the South America mechanical, electrical, and plumbing (MEP) services market. The result is a more favorable growth path for contractors that can combine mechanical depth, electrical reliability, plumbing integration, and formal commissioning discipline in one managed offer.

List of Companies Covered in this Report:

- Grupo ECA

- ES4Q

- Propamat

- CELMEC

- Grupo Nortem

- MEPSIS

- JIC Ingenieria

- Semaica

- AECOM

- WSP

- Jacobs

- Arup

- Stantec

- Mott MacDonald

- Hatch

- Techint Engineering & Construction

- ACCIONA

- Equans Brasil

- ENGIE Solutions Brasil

- VINCI Energies Brasil

- Fluor

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Commercial and Infrastructure Modernization

- 4.2.2 Data Center and Logistics Facility Expansion

- 4.2.3 Outsourcing of Hard Services and Lifecycle Maintenance

- 4.2.4 Chile and Brazil Power-Linked Campus Development

- 4.2.5 ESG-Driven Energy and Refrigerant Audit Scopes

- 4.2.6 Water Resilience and Closed-Loop Cooling Retrofits

- 4.3 Market Restraints

- 4.3.1 FX Volatility and Inflation Pressure

- 4.3.2 Labor Informality and Uneven Execution Quality

- 4.3.3 Fragmented Building and Fire-Code Enforcement

- 4.3.4 Grid Interconnection Delays Near Digital Clusters

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Cost Structure Analysis

5 Market Size & Growth Forecasts (Value, in USD)

- 5.1 By Type

- 5.1.1 Mechanical Services

- 5.1.2 Electrical Services

- 5.1.3 Plumbing Services

- 5.1.4 Integrated MEP Services

- 5.2 By Service Type

- 5.2.1 Design & Engineering

- 5.2.2 Installation, Testing, and Commissioning

- 5.2.3 Maintenance, Repair, and Retrofit

- 5.2.4 Managed / Performance-based Services

- 5.3 By End-User Industry

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Infrastructure

- 5.4 By Geography

- 5.4.1 Brazil

- 5.4.2 Argentina

- 5.4.3 Chile

- 5.4.4 Colombia

- 5.4.5 Peru

- 5.4.6 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Grupo ECA

- 6.4.2 ES4Q

- 6.4.3 Propamat

- 6.4.4 CELMEC

- 6.4.5 Grupo Nortem

- 6.4.6 MEPSIS

- 6.4.7 JIC Ingenieria

- 6.4.8 Semaica

- 6.4.9 AECOM

- 6.4.10 WSP

- 6.4.11 Jacobs

- 6.4.12 Arup

- 6.4.13 Stantec

- 6.4.14 Mott MacDonald

- 6.4.15 Hatch

- 6.4.16 Techint Engineering & Construction

- 6.4.17 ACCIONA

- 6.4.18 Equans Brasil

- 6.4.19 ENGIE Solutions Brasil

- 6.4.20 VINCI Energies Brasil

- 6.4.21 Fluor

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment