|

시장보고서

상품코드

2064376

아시아태평양의 기계, 전기, 배관(MEP) 서비스 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Asia-Pacific Mechanical, Electrical, And Plumbing (MEP) Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

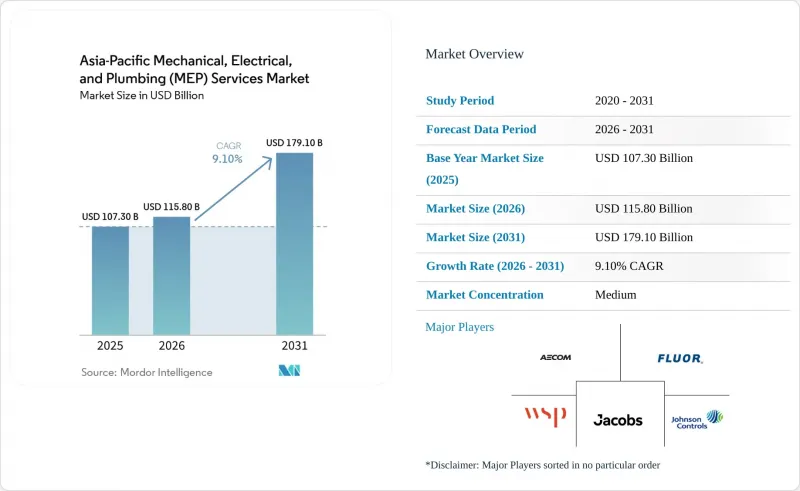

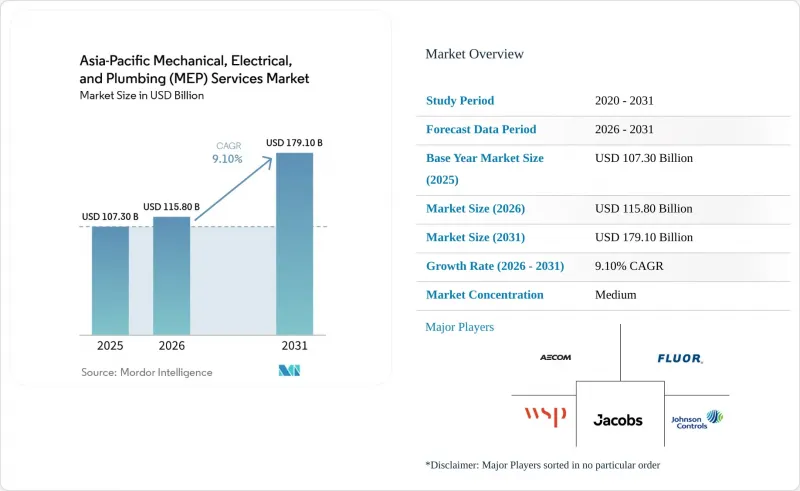

Mordor Intelligence에 의하면, 아시아태평양의 기계, 전기, 배관(MEP) 서비스 시장 규모는 2025년에 1,073억 달러로 평가되었고, 2026년에 1,158억 달러로 추정되며, 2031년까지 1,791억 달러에 이를 것으로 예측됩니다.

2026-2031년 연평균 성장률(CAGR) 9.10%로 성장할 것으로 전망됩니다.

본 보고서는 유형별(기계, 전기, 배관, 통합 MEP), 서비스 유형별(설계 및 엔지니어링, 설치, 시험 및 시운전, 유지보수 및 수리 등), 최종 사용자 산업별(주택, 상업, 인프라), 지역별(중국, 인도, 일본, 한국, 호주, 인도네시아, 기타 아시아태평양)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

아시아태평양의 기계, 전기, 배관(MEP) 서비스 시장 동향 및 고찰

교통 주도형 도시 메가 프로젝트에 대한 지출

민간 건설 사이클의 기세가 주춤해지고 있음에도 불구하고, 정부의 인프라 계획은 계속해서 아시아태평양의 MEP 서비스 시장을 지탱하고 있습니다. 베트남은 2025년에 라오카이-하노이-하이퐁 구간의 표준궤 철도를 승인했으나, 이 프로젝트에는 174개의 교량과 55개의 터널이 포함되어 있어 시공 단계에서 터널 환기, 방화·방재·안전, 견인 전력 및 관련 시스템이 필요합니다. 대규모 교통 인프라 프로젝트에서는 공종별로 작업을 분할하는 것이 아니라, 단일 범위 내에서 여러 시스템을 조율할 수 있는 도급업체가 유리합니다. 이는 철도 등급 인증, 노선 전체에 걸친 시스템 도입 경험, 그리고 확실한 시운전 실적을 갖춘 기업을 뒷받침하는 것으로, 특히 그러한 인력이 여전히 부족한 아세안 일부 지역에서 두드러지게 나타납니다. 그 결과, 대중교통에 대한 지출은 호주, 베트남, 태국, 인도에 걸친 아시아태평양의 MEP 서비스 시장에서 계속해서 고부가가치 비즈니스 기회를 창출하고 있습니다.

데이터센터 및 반도체 시설의 건설 확대

미션 크리티컬 시설은 아시아태평양의 MEP 서비스 시장에서 여전히 가장 뚜렷한 성장 분야 중 하나입니다. AI 지원 데이터센터는 기존 서버실보다 고밀도의 전력, 냉각, 백업 및 제어 아키텍처가 필요하기 때문에 시공사는 표준 사무실용 MEP 템플릿을 그대로 적용하는 대신 서비스 레이아웃 전체를 재설계해야 합니다. 존슨 컨트롤스는 2026년 싱가포르 혁신 센터 확장을 위해 향후 5년간 최대 6,000만 달러를 투자하기로 결정했습니다. 이 센터는 지역 내 데이터센터 수요에 부응하기 위해 첨단 냉각 및 열 관리에 중점을 두고 있습니다. 반도체 프로젝트도 이와 병행하여 수요를 견인하고 있습니다. 클린룸의 공조 설비, 초순수 배관, 고가용성 전기 시스템은 일반 상업용 빌딩보다 더 엄격한 성능 기준이 요구되기 때문입니다. 아세안(ASEAN) 투자 보고서에서는 TSMC의 43억 달러 규모 싱가포르 공장, 인피니언의 54억 달러 규모 말레이시아 실리콘 카바이드(SiC) 생산 확대, 그리고 유나이티드 마이크로일렉트로닉스의 50억 달러 규모 싱가포르 시설 등 주요 제조 프로젝트들도 주목받고 있습니다. 이에 따라 아시아태평양의 MEP 서비스 시장은 더욱 전문적인 엔지니어링, 더욱 엄격한 시운전, 그리고 더욱 강력한 통합형 제공 역량을 향해 나아가고 있습니다.

숙련 기술자 부족과 임금 상승

아시아태평양 지역의 MEP 서비스 시장에서 인력 확보는 여전히 가장 두드러진 공급 제약 요인 중 하나입니다. 전기 기술자, 공조 기술자, 배관 작업원, 방화 설비 전문가 등은 특히 운송, 에너지, 산업, 건축 분야의 각 프로젝트가 동시에 진행되는 시기에는 해당 지역에서 가장 활기를 띠는 거점에서 확보하기 어렵습니다. 인력 부족 상황은 인건비 증가와 초과근무 시간 증가를 초래하며, 도급업체가 외국인 근로자나 전문 하도급 팀에 대한 의존도를 높이는 요인이 되고 있습니다. 더 큰 문제는 계약 시점에 있습니다. 대부분의 프로젝트에서는 현장 시공이 시작되기 훨씬 전에 가격이 결정되기 때문입니다. 이러한 불일치로 인해 고정 가격 계약이 이익률 하락을 초래할 가능성이 있으며, 수요가 견조한 상황에서도 아시아태평양 MEP 서비스 시장 전체의 생산 능력 확대를 지연시키는 요인이 되고 있습니다.

부문별 분석

2025년, 아시아태평양의 MEP 서비스 시장 점유율 중 41%를 기계 설비 서비스가 차지했으며, 이에 따라 냉각 및 환기 공사가 이 지역의 프로젝트 지출에서 여전히 핵심을 차지했습니다. 수요가 가장 높은 곳은 여전히 인구 밀도가 높은 도시 시장이며, 이곳에서는 HVAC, 냉수 루프, 지역 냉방 시스템이 건물 설치 비용에서 큰 비중을 차지하고 있습니다. 또한, 에너지 개보수는 일반적으로 외관 개보수가 아닌 칠러, 펌프, 공기 측 시스템, 제어 시스템부터 시작되기 때문에 기계 설비의 범위는 규정 준수 측면에서도 여전히 핵심적인 위치를 차지하고 있습니다. 전기 설비 서비스와 배관 설비 서비스가 그 뒤를 잇는 주요 카테고리로, 이 두 분야 모두 신뢰성이 높은 전력 및 급수 시스템을 필요로 하는 데이터센터, 산업 시설, 고층 빌딩 프로젝트에 의해 뒷받침되고 있습니다.

개발업체들이 복잡한 시설에서 일괄 도급 방식으로 전환함에 따라, 아시아태평양의 MEP 서비스 시장 규모 구성에서 통합 MEP 서비스는 2031년까지 연평균 성장률(CAGR) 11.65%로 성장할 것으로 전망됩니다. 이는 여러 전문 업체가 각기 다른 업무 범위에서 작업을 수행할 때 발생하는 조정 위험, 재작업 및 공정 지연에 대한 우려를 반영한 것입니다. 아시아태평양의 MEP 서비스 업계에서는 BIM 대응 능력, 간섭 검출 기능, 그리고 전 공정에 걸친 실행 능력을 갖춘 기업이 단일 전문 분야만 제공하는 기업에 비해 우위를 점하고 있습니다. 이러한 장점은 서비스 밀도가 높고, 후기 단계에서 변경 시 막대한 비용이 소요되는 교통 시스템, 데이터센터, 반도체 시설에서 특히 두드러집니다. 따라서 최종 패키지 내의 기계, 전기, 배관 분야의 전문성은 여전히 중요하지만, 아시아태평양의 MEP 서비스 시장은 인터페이스를 줄이고 대규모 통합형 프로젝트로 전환되고 있습니다.

기타 혜택 :

- Excel 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the asia-Pacific mechanical, electrical, and plumbing services market size is projected to be USD 107.30 billion in 2025, USD 115.80 billion in 2026, and reach USD 179.10 billion by 2031, growing at a CAGR of 9.10% from 2026 to 2031.

This report is Segmented by Type (Mechanical, Electrical, Plumbing, Integrated MEP), Service Type (Design & Engineering, Installation Testing & Commissioning, Maintenance & Repair Among Others), End-User Industry (Residential, Commercial, Infrastructure), and Geography (China, India, Japan, South Korea, Australia, Indonesia, Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Mechanical, Electrical, And Plumbing (MEP) Services Market Trends and Insights

Transit-Led Urban Megaproject Spending

Government infrastructure pipelines continue to support the Asia-Pacific MEP services market, even as private construction cycles lose momentum. Vietnam approved the Lao Cai to Hanoi to Hai Phong standard-gauge railway in 2025, and the project includes 174 bridges and 55 tunnels that will require tunnel ventilation, fire-life-safety, traction power, and related systems during delivery. Large transit packages also favor contractors that can coordinate multiple systems within one scope instead of splitting the work trade by trade. That supports firms with railway-grade certifications, linewide systems experience, and proven commissioning depth, especially in parts of ASEAN where that talent pool remains limited. The result is that public transport spending continues to create high-value opportunities in the Asia-Pacific MEP services market across Australia, Vietnam, Thailand, and India.

Data-Center and Semiconductor Facility Build-Out

Mission-critical facilities remain one of the clearest growth pockets in the Asia-Pacific MEP services market. AI-ready data centers require denser power, cooling, backup, and control architectures than legacy server rooms, so contractors must redesign entire service layouts rather than repeating standard office MEP templates. Johnson Controls committed up to USD 60 million over 5 years in 2026 to expand its Singapore Innovation Center, with the site focused on advanced cooling and thermal management to meet regional data center demand. Semiconductor projects add a parallel stream because cleanroom HVAC, ultra-pure water plumbing, and high-availability electrical systems require tighter performance standards than ordinary commercial buildings. ASEAN investment reporting also highlighted major manufacturing projects, including TSMC's USD 4.3 billion Singapore fab, Infineon's USD 5.4 billion Malaysian silicon carbide expansion, and United Microelectronics' USD 5 billion Singapore facility. This is pushing the Asia-Pacific MEP services market toward more specialized engineering, tighter commissioning, and stronger integrated delivery capability.

Skilled-Trade Shortages and Wage Inflation

Labor availability remains one of the clearest delivery limits in the Asia-Pacific MEP services market. Electrical installers, HVAC technicians, plumbing crews, and fire-protection specialists are difficult to secure in the region's busiest hubs, especially when transport, energy, industrial, and building programs move forward at the same time. Tight labor conditions raise wage bills, increase overtime exposure, and push contractors to rely more heavily on imported labor or specialist subcontract crews. The larger problem is contract timing because many jobs are priced well before site execution begins. That mismatch can turn fixed-price work into margin loss and it slows capacity expansion across the Asia-Pacific MEP services market even when demand conditions are strong.

Other drivers and restraints analyzed in the detailed report include:

- Green-Building and Refrigerant Compliance Tightening

- Industrial Relocation into ASEAN and India

- Copper, Switchgear, and HVAC Component Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mechanical Services held 41% of Asia-Pacific MEP services market share in 2025, which kept cooling and ventilation work at the center of regional project spend. Demand remains strongest in dense urban markets where HVAC, chilled-water loops, and district cooling systems account for a large share of installed building value. Mechanical scope also stays central to compliance because energy retrofits usually begin with chillers, pumps, air-side systems, and controls rather than with cosmetic upgrades. Electrical Services and Plumbing Services followed as the next-largest categories, both supported by data centers, industrial facilities, and high-rise projects that require reliable power and water systems.

Integrated MEP Services is projected to grow at 11.65% CAGR within the Asia-Pacific MEP services market size mix through 2031 as developers shift toward single-package awards on complex facilities. This reflects concern over coordination risk, rework, and schedule slippage when multiple trade contractors operate under separate scopes. In the Asia-Pacific MEP services industry, firms with BIM capability, clash detection, and full-cycle execution are gaining ground on companies that supply only one trade. That advantage is strongest on transit systems, data centers, and semiconductor facilities, where service density is great and late-stage changes are expensive. The Asia-Pacific MEP services market is therefore moving toward fewer interfaces and larger integrated mandates, even though mechanical, electrical, and plumbing specialization still matter within the final package.

List of Companies Covered in this Report:

- AECOM

- WSP Global

- Jacobs

- Fluor Corporation

- Johnson Controls

- Honeywell Building Solutions

- Siemens Smart Infrastructure

- Larsen & Toubro Construction

- Voltas Limited

- Sterling and Wilson

- Shinryo Corporation

- Meinhardt Group

- Surbana Jurong

- Arup

- Aurecon

- Mott MacDonald

- Tata Projects

- Beca Group

- Nippon Koei

- Obayashi Corporation

- Gammon Construction

- Kinden Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Transit-Led Urban Megaproject Spending

- 4.2.2 Data-Center and Semiconductor Facility Build-Out

- 4.2.3 Green-Building and Refrigerant Compliance Tightening

- 4.2.4 Industrial Relocation into ASEAN and India

- 4.2.5 Public-Project BIM Mandates and Prefab MEP Adoption

- 4.2.6 District Cooling and Heat-Pump Retrofit Acceleration

- 4.3 Market Restraints

- 4.3.1 Skilled-Trade Shortages and Wage Inflation

- 4.3.2 Copper, Switchgear, and HVAC Component Volatility

- 4.3.3 Cross-Border Code Fragmentation and Local-Content Rules

- 4.3.4 Utility-Connection Bottlenecks for Mission-Critical Projects

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Cost Structure Analysis

5 Market Size & Growth Forecasts (Value, in USD)

- 5.1 By Type

- 5.1.1 Mechanical Services

- 5.1.2 Electrical Services

- 5.1.3 Plumbing Services

- 5.1.4 Integrated MEP Services

- 5.2 By Service Type

- 5.2.1 Design & Engineering

- 5.2.2 Installation, Testing, and Commissioning

- 5.2.3 Maintenance & Repair

- 5.2.4 Managed / Performance-based Services

- 5.3 By End-User Industry

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Infrastructure

- 5.4 By Geography

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 South Korea

- 5.4.5 Australia

- 5.4.6 Indonesia

- 5.4.7 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 AECOM

- 6.4.2 WSP Global

- 6.4.3 Jacobs

- 6.4.4 Fluor Corporation

- 6.4.5 Johnson Controls

- 6.4.6 Honeywell Building Solutions

- 6.4.7 Siemens Smart Infrastructure

- 6.4.8 Larsen & Toubro Construction

- 6.4.9 Voltas Limited

- 6.4.10 Sterling and Wilson

- 6.4.11 Shinryo Corporation

- 6.4.12 Meinhardt Group

- 6.4.13 Surbana Jurong

- 6.4.14 Arup

- 6.4.15 Aurecon

- 6.4.16 Mott MacDonald

- 6.4.17 Tata Projects

- 6.4.18 Beca Group

- 6.4.19 Nippon Koei

- 6.4.20 Obayashi Corporation

- 6.4.21 Gammon Construction

- 6.4.22 Kinden Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment