|

시장보고서

상품코드

2064372

싱가포르의 통합 시설 관리 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Singapore Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

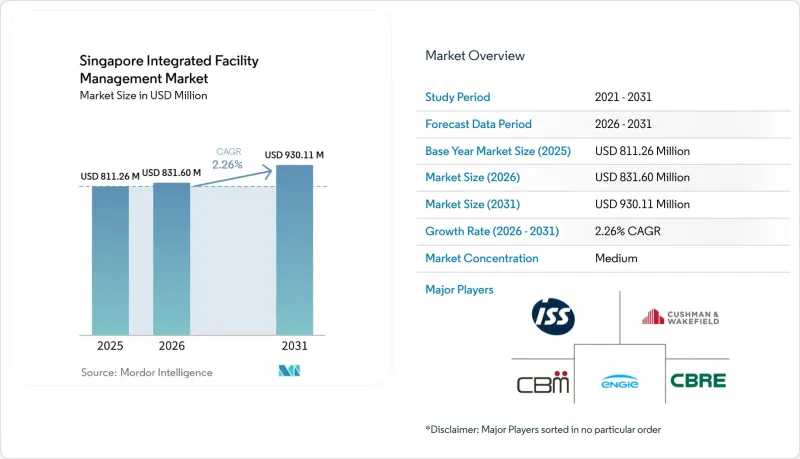

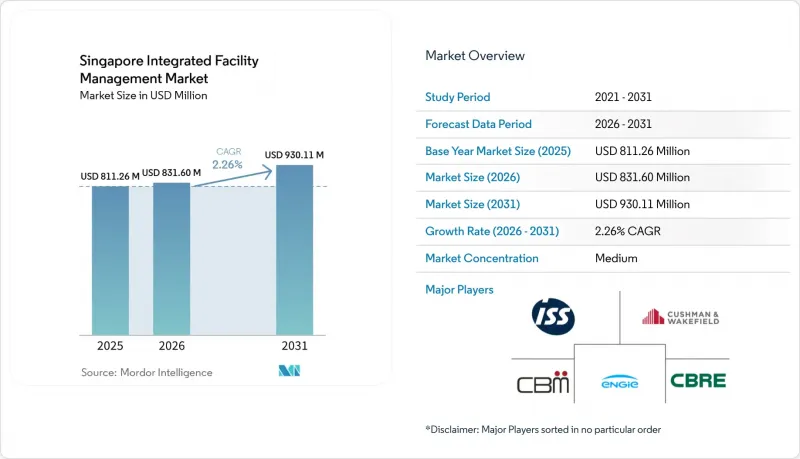

Mordor Intelligence에 의하면, 싱가포르의 통합 시설 관리 시장 규모는 2025년 8억 1,126만 달러로 평가되었고, 2026년 8억 3,160만 달러로 추정되고, 2031년까지 9억 3,011만 달러로 확대될 전망이며, 2026-2031년 CAGR 2.26%를 나타낼 것으로 예측됩니다.

본 보고서는 서비스 유형별(하드 설비 관리(자산 관리, MEP 및 HVAC 서비스 등), 소프트 설비 관리별(사무 지원 및 보안, 청소 서비스, 케이터링 서비스 등)) 및 최종 사용자별(상업, 호텔 및 관광, 의료, 산업 및 공정 부문 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

싱가포르의 통합 시설 관리 시장 동향 및 인사이트

스마트 그린 빌딩을 위한 정부의 추진 강화

싱가포르의 통합 시설 관리 시장은 기존 건물의 에너지 효율 향상을 위한 정부의 직접적인 추진 정책의 혜택을 받고 있습니다. 싱가포르의 건축 부문은 국내 이산화탄소 배출량의 20% 이상을 차지하고 있으며, 이로 인해 에너지 효율은 정책 과제로서 지속적으로 중요시되고 있어, 측정 가능한 성과를 제공할 수 있는 기술 서비스 제공업체에 대한 장기적인 수요를 뒷받침하고 있습니다. ‘건축 규제(기존 건축물의 환경 지속가능성 조치)(개정) 규칙 2025’가 2025년 9월 30일에 시행됨에 따라, 사무실에는 200 kWh/m²/년, 소매 시설에는 495 kWh/m²/년, 병원에는 360 kWh/m²/년의 에너지 사용 원단위 기준치가 설정되었습니다. 이 기준치를 초과하는 건물은 자격을 갖춘 에너지 감사관을 선임하고, 에너지 효율 개선 계획을 제출하며, 3년 이내에 10% 감축을 달성해야 합니다. 이를 통해 FM 계약의 기술적 범위가 확대되고, 지속적인 전문 업무가 촉진될 것입니다. 또한, ‘기존 건축물 대상 그린마크 인센티브 제도 2.0’에서는 개보수 비용의 최대 50%를 지원함으로써 개보수 공사의 재정적 장벽을 낮추고 있으며, 이를 통해 소유주가 성과 연계형 FM 계약을 도입하기가 더 쉬워졌습니다. 싱가포르에서는 2026년 5월까지 건축 물량의 61%가 친환경화되고, 2030년까지 80%라는 목표를 달성하기까지 남은 격차는 싱가포르의 통합 시설 관리(IFM) 시장에서 단기적으로 리모델링 관련 서비스 수요를 확실히 발생시킬 것임을 시사합니다.

예방적 유지보수의 의무화 요건과 HSE 규정

싱가포르의 IFM 시장은 예방적 유지보수를 미루기 어렵게 만드는 엄격한 규제 환경의 이점도 누리고 있습니다. 건물 소유주는 작업장 안전, 화재 안전 인증, 엘리베이터 유지보수, 에스컬레이터 유지보수, 냉방 시스템 정비에 이르는 중복된 의무를 관리해야 하므로, 이러한 일련의 업무를 단일 운영 모델 하에서 조정할 수 있는 통합 서비스 제공업체의 매력이 높아지고 있습니다. BCA FM01의 사업 책임자 체계는 공공 부문 유지보수 계약의 적격 후보를 선별하고 있습니다. M1 클래스 신청자는 200만 싱가포르 달러(150만 달러)의 납입 자본금과, 최소 4,000만 싱가포르 달러(3,000만 달러)에 상당하는 검증된 IFM 프로젝트 실적을 보유하고 있어야 하기 때문입니다. 이러한 선별 효과는 싱가포르의 통합 시설 관리 시장에서 특히 고객사가 최저가 입찰보다 신뢰성을 중시하는 경우, 대규모 인증 사업자의 이익률 관리를 뒷받침하고 있습니다. 정부의 입찰 요건도 이러한 추세를 뒷받침하고 있습니다. 왜냐하면, 공인된 안전 기준을 충족하지 못하는 사업자는 고액의 예방 정비 업무 자격을 얻기 어렵기 때문입니다. 실제로, 이를 통해 여러 규제 당국, 기술적 업무, 보고 의무를 차질 없이 처리할 수 있는 입지를 다진 기업에게는 규정 준수 대응 일정이 지속적인 수익원이 됩니다.

자격을 갖춘 FM 인력 부족이 서비스 확장성을 제한하고 있습니다.

노동력은 싱가포르의 통합 시설 관리(IFM) 시장이 어느 정도의 속도로 성장할 수 있을지에 있어 여전히 가장 뚜렷한 구조적 제약 요인으로 남아 있습니다. 싱가포르 노동 시장에서는 2025년 12월 구인 대 실업자 비율이 1.58을 기록했으며, 고용주의 24.3%가 업무 부담을 가중시키고 서비스 품질에 영향을 미치는 기술 격차를 보고하고 있습니다. 시설 관리 분야에서는 인건비가 운영 비용의 40%에서 50%를 차지하는 데다, 많은 하드 FM 계약에서 대체하기 어려운 공인 기술자, 기계 엔지니어, 에너지 감사인이 필요하기 때문에 그 압박은 더욱 심각합니다. 국내 기술 인력의 고령화와 젊은 층의 기술직 진출이 주춤해지면서 문제가 더욱 심각해지고 있는 반면, 외국인 노동자 수용 제한으로 인해 대규모 인력 보충도 어려워지고 있습니다. 이러한 요인들이 겹치면서, 수요가 존재하더라도 신규 사업자가 흡수할 수 있는 규모는 제한됩니다. 왜냐하면 계약 이행은 단순한 영업 능력뿐만 아니라 자격을 갖춘 인력을 확보하는 데 달려 있기 때문입니다. BCA 아카데미의 전문 연수 프로그램은 중기적인 인재 공급망을 뒷받침하고 있지만, 싱가포르의 통합 시설 관리 시장이 직면한 단기적인 인력 부족을 완전히 해소해 주지는 못합니다.

부문별 분석

하드 시설 관리(FM)는 싱가포르의 통합 시설 관리(IFM) 시장에서 가장 빠르게 성장하고 있는 서비스 분야이며, 이 부문의 싱가포르 IFM 시장 규모는 2026-2031년 연평균 성장률(CAGR) 2.88%로 성장할 전망입니다. 이러한 성장 속도는 2025년 9월에 시행될 MEI 제도와 밀접한 관련이 있습니다. 이 제도에 따라 에너지 성능은 단순한 선택적 개선 대상에서 연면적 5,000제곱미터를 초과하는 대규모 건물에 대한 기한이 정해진 준수 요건으로 전환됩니다. 건물이 정해진 에너지 강도 기준치를 초과한 경우, 소유주는 자격을 갖춘 전문가를 선임하여 개선 조치를 문서화해야 합니다. 이에 따라 하드 FM 제공업체는 감사, 기계 설비 최적화, 시스템 조정 및 후속 보고에서 지속적인 역할을 담당하게 됩니다. 싱가포르에서 KONE의 커넥티드 엘리베이터 서비스는 도입 후 2년 동안 예측 유지보수를 통해 고장 감지율을 70% 향상시켰으며, 현장 출동 횟수를 40% 줄였습니다. 이는 기술 분야 운영 담당자들이 정기 점검에서 자산당 수익을 증대시키는 지속적인 모니터링 계약으로 전환하고 있음을 보여줍니다. 또한, 싱가포르의 통합 시설 관리(IFM) 업계는 현지 운영 환경의 이점도 누리고 있습니다. 높은 습도와 연중 긴 냉방 가동 시간으로 인해, 쾌적성, 효율성 및 건물의 규정 준수 사항에 영향을 미치지 않으면서 HVAC 유지보수를 미루는 것은 어렵기 때문입니다.

소프트 FM은 계속해서 최대 점유율을 유지하며, 2025년 싱가포르 IFM 시장 점유율의 61.75%를 차지했습니다. 이러한 우위는 거의 모든 자산군에서 볼 수 있는 청소, 경비, 조경, 해충 방제, 컨시어지 및 관련 현장 서비스에 걸친 업무의 폭을 반영하고 있습니다. 싱가포르의 통합 시설 관리 업계에서 이 서비스 그룹은 매일 꾸준한 운영이 요구되는 상업용 건물, 공공 공간, 물류 시설 및 위생 관리가 중요한 환경에 깊이 뿌리내리고 있습니다. 그러나 비용 구조는 변화하고 있습니다. 청소 및 경비 분야의 임금 규제로 인해 사업자들은 단순히 노동력을 늘리는 것뿐만 아니라, 로봇 기술 도입, 프로세스 재설계, 성과 기반 가격 책정을 통해 이익률을 유지해야 하는 상황에 놓여 있기 때문입니다. OCS 싱가포르가 2024년 11월에 소프트뱅크 로보틱스와 체결한 제휴와 ‘환경 서비스 산업 혁신 로드맵 2025’는 모두 이러한 방향성을 보여주고 있으며, 생산성, 자동화, 노동 효율성이 소프트 FM 분야의 차기 경쟁 구도를 형성하게 될 것입니다.

기타 혜택 :

- Excel 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the singapore integrated facility management market size is projected to expand from USD 811.26 million in 2025 and USD 831.60 million in 2026 to USD 930.11 million by 2031, registering a CAGR of 2.26% between 2026 to 2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), and End User (Commercial, Hospitality, Healthcare, Industrial and Process Sector, and More). The Market Forecasts are Provided in Terms of Value (USD).

Singapore Integrated Facility Management Market Trends and Insights

Growing Government Push for Smart Green Buildings

The Singapore integrated facility management market is benefiting from the government's direct push to improve the energy performance of existing buildings. Singapore's building sector accounted for more than 20% of national carbon emissions, which keeps energy efficiency high on the policy agenda and supports long-term demand for technical service providers that can deliver measurable outcomes. The Building Control (Environmental Sustainability Measures for Existing Buildings) (Amendment) Regulations 2025 took effect on September 30, 2025, and imposed Energy Use Intensity thresholds of 200 kWh/m2/year for offices, 495 kWh/m2/year for retail, and 360 kWh/m2/year for hospitals. Buildings that exceed those thresholds must appoint a qualified energy auditor, submit an Energy Efficiency Improvement Plan, and deliver a 10% reduction within 3 years, which expands the technical scope of FM contracts and supports recurring specialist work. The Green Mark Incentive Scheme for Existing Buildings 2.0 also lowers the financial barrier for retrofit activity by co-funding up to 50% of retrofit capital expenditure, which makes performance-linked FM contracts easier for owners to adopt. Singapore had greened 61% of its building stock by May 2026, and the remaining gap to the 80% target by 2030 leaves a clear near-term pipeline for retrofit-linked service mandates in the Singapore integrated facility management (IFM) market.

Mandatory Preventive Maintenance Requirements and HSE Regulations

The Singapore IFM market also benefits from a stringent regulatory environment that makes preventive maintenance difficult to defer. Building owners must manage overlapping obligations covering workplace safety, fire safety certification, lift servicing, escalator servicing, and cooling system maintenance, which increases the appeal of a single integrated provider that can coordinate those routines under one operating model. The BCA FM01 work head framework narrows the eligible pool for public sector maintenance contracts because M1-grade applicants must hold SGD 2 million (USD 1.5 million) in paid-up capital and at least SGD 40 million (USD 30 million) in a verified IFM project track record. That screening effect supports margin discipline for larger accredited operators in the Singapore integrated facility management market, especially where clients value reliability over lowest-cost bidding. Government tender requirements also reinforce that pattern because operators that cannot meet recognized safety standards are less likely to qualify for high-value preventive maintenance work. In practice, this turns compliance calendars into a recurring revenue base for established firms that can handle multiple regulators, technical trades, and reporting obligations without disruption.

Shortage Of Qualified FM Workforce Limiting Service Scalability

Labor remains the clearest structural limit on how fast the Singapore integrated facility management (IFM) market can scale. Singapore's labour market recorded a vacancy-to-unemployed ratio of 1.58 in December 2025, and 24.3% of employers reported skills gaps that increased workloads and affected service quality. In facility management, the pressure is sharper because labour accounts for 40% to 50% of operating costs, and many hard FM contracts require certified technicians, mechanical engineers, and energy auditors who are not easy to replace. The aging domestic technical workforce and weaker entry of younger workers into trade roles are adding to the problem, while foreign worker limits make large-scale staffing responses difficult. That combination restrains how much new business providers can absorb, even when demand is present, because contract mobilization depends on qualified people rather than only sales capacity. BCA Academy's specialist training programs support the medium-term pipeline, but they do not fully relieve the near-term staffing constraint facing the Singapore integrated facility management market.

Other drivers and restraints analyzed in the detailed report include:

- Corporate ESG Push Driving Outsourcing of Facility Services

- AI And IoT Integration for Predictive Maintenance

- Data Privacy and Cybersecurity Risks in Smart Building Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hard Facility Management (FM) is the fastest-growing service line in the Singapore integrated facility management (IFM) market, with the Singapore IFM market size for this segment set to rise at a 2.88% CAGR from 2026 to 2031. That pace is tied to the September 2025 MEI regime, which turns energy performance from a discretionary upgrade topic into a timed compliance requirement for large buildings above 5,000 m2 gross floor area. Once buildings cross prescribed energy intensity thresholds, owners must engage qualified specialists and document improvement actions, which gives hard FM providers a recurring role in audits, mechanical optimization, system tuning, and follow-up reporting. KONE's connected elevator services in Singapore, which improved proactive fault identification by 70% and reduced callouts by 40% in the first 2 years of deployment, show how technical operators are moving from scheduled visits toward continuous monitoring contracts that increase revenue per asset. The Singapore integrated facility management industry also benefits from local operating conditions because high humidity and long annual cooling hours make HVAC upkeep difficult to defer without affecting comfort, efficiency, and building compliance.

Soft FM remained the volume leader and held 61.75% of the Singapore IFM market share in 2025. Its lead reflects the breadth of work covered across cleaning, security, landscaping, pest control, concierge, and related site services that appear in almost every asset class. In the Singapore integrated facility management industry, this service group remains deeply embedded in commercial buildings, public spaces, logistics facilities, and hygiene-sensitive environments that require steady execution every day. The cost profile is changing, however, because wage regulation in cleaning and security is pushing operators to defend margins through robotics, process redesign, and outcome-based pricing rather than through higher labour deployment alone. OCS Singapore's November 2024 arrangement with SoftBank Robotics and the Environmental Services Industry Transformation Map 2025 both point in that direction, with productivity, automation, and labour efficiency shaping the next phase of competition in soft FM.

List of Companies Covered in this Report:

- C&W Services

- ISS A/S

- CBM Pte Ltd

- CBRE Group, Inc.

- Jones Lang LaSalle Incorporated

- ENGIE Services Singapore Pte Ltd.

- Atalian Global Services

- Knight Frank Pte Ltd.

- Keppel Infrastructure Holdings Pte Ltd.

- SMM Pte Ltd

- Colliers International Group Inc.

- Sodexo SA

- DTZ Facilities & Engineering (S) Limited

- Certis Group

- AETOS Holdings Pte Ltd.

- Surbana Jurong Pte Ltd.

- UEMS Solutions Pte Ltd.

- Mapletree Facilities Services Pte Ltd.

- OCS Group International Ltd.

- BMS Engineering and Trading Pte Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Government Push for Smart, Green Buildings

- 4.2.2 Mandatory Preventive Maintenance Norms Under BCA Regulations

- 4.2.3 Corporate ESG Targets Driving Outsourcing of Facility Operations

- 4.2.4 5G-Enabled IoT Adoption for Predictive Maintenance

- 4.2.5 Expansion of Integrated Resorts and Mixed-Use Mega Projects

- 4.2.6 Shift Toward Outcome-Based FM Contracts in Public Sector

- 4.3 Market Restraints

- 4.3.1 Shortage of Skilled Technicians for High-Tech Building Systems

- 4.3.2 Squeezed Margins Due to Rising Manpower Costs

- 4.3.3 Data-Security Concerns in Cloud-Based FM Platforms

- 4.3.4 Volatility in Commercial Real-Estate Demand Post-Pandemic

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 By End User Industry

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 C&W Services

- 6.4.2 ISS A/S

- 6.4.3 CBM Pte Ltd

- 6.4.4 CBRE Group, Inc.

- 6.4.5 Jones Lang LaSalle Incorporated

- 6.4.6 ENGIE Services Singapore Pte Ltd.

- 6.4.7 Atalian Global Services

- 6.4.8 Knight Frank Pte Ltd.

- 6.4.9 Keppel Infrastructure Holdings Pte Ltd.

- 6.4.10 SMM Pte Ltd

- 6.4.11 Colliers International Group Inc.

- 6.4.12 Sodexo SA

- 6.4.13 DTZ Facilities & Engineering (S) Limited

- 6.4.14 Certis Group

- 6.4.15 AETOS Holdings Pte Ltd.

- 6.4.16 Surbana Jurong Pte Ltd.

- 6.4.17 UEMS Solutions Pte Ltd.

- 6.4.18 Mapletree Facilities Services Pte Ltd.

- 6.4.19 OCS Group International Ltd.

- 6.4.20 BMS Engineering and Trading Pte Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment