|

시장보고서

상품코드

2064395

인도의 컨테이너보드 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)India Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

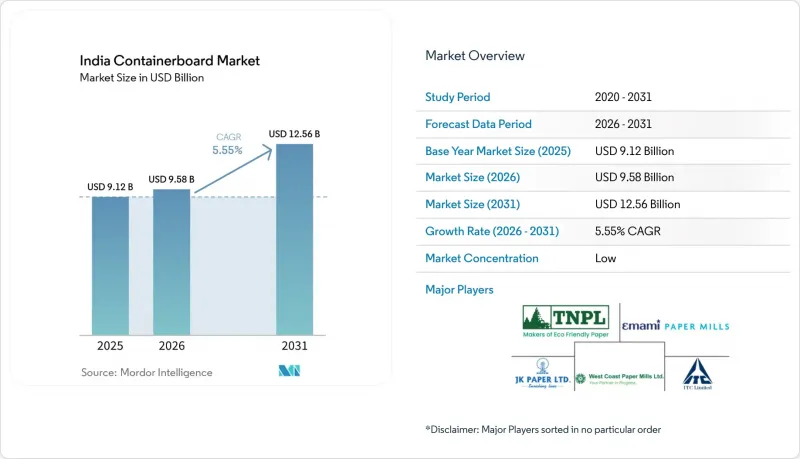

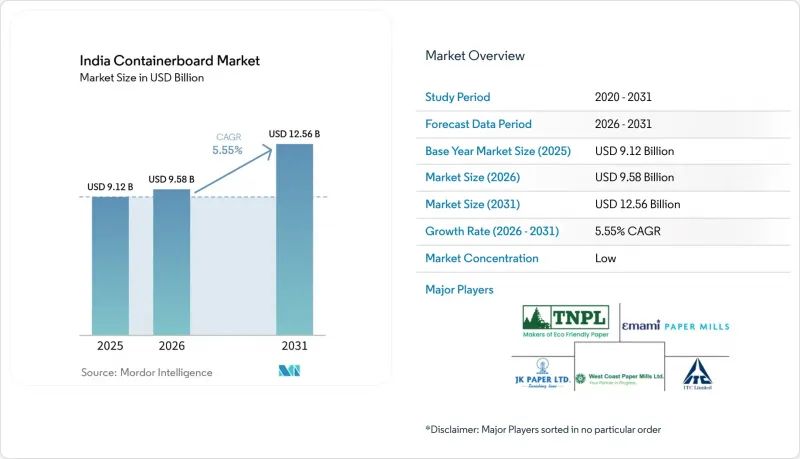

Mordor Intelligence에 의하면, 인도 컨테이너보드 시장 규모는 2025년 91억 2,000만 달러에서 2026년에는 95억 8,000만 달러로 확대되어 2031년까지 125억 6,000만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 5.55%로 성장할 전망입니다.

본 보고서는 원료(버진 섬유 및 재생 섬유), 제품 유형(크래프트 라이너, 테스트 라이너, 플루팅), 그리고 최종 사용자 산업(식품 및 음료, 소비재, 산업용 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

인도 컨테이너보드 시장 동향 및 인사이트

전자상거래 및 퀵커머스로 인한 골판지 수요 증가

인도의 퀵 커머스 부문은 2024년에 총 상품 가치(GMV)가 33억 5,000만 달러에 달할 것으로 예상되며, 2028년까지 연평균 성장률(CAGR) 27.42%를 기록하며 88억 3,000만 달러로 성장할 것으로 전망되고 있어, 이로 인해 도시 지역의 전체 물류 네트워크 전반에 걸친 포장 수요 양상이 급변하고 있습니다. 2025년, Blinkit은 100개 이상의 도시에서 1,500개 이상의 다크 스토어를 운영하고 있으며, Zepto와 Swiggy Instamart도 밀집된 다크 스토어 네트워크로 확장했습니다. 이로 인해 단주기 골판지 소비의 잠재 시장이 확대되었습니다. 이러한 네트워크에서는 단순히 상자의 수만 요구되는 것이 아니라, 피킹부터 발송까지의 과정에서 반복되는 가로 방향의 취급에도 견딜 수 있는 콤팩트하고 적절한 크기의 골판지 포장이 요구됩니다. 이러한 요건으로 인해 구매자들은 파열 강도(버스트 팩터)의 임계값에만 의존하지 않고, 단기간의 압축이나 에지 크래시(가장자리 찌그러짐)에 대한 요구 사항을 보다 일관되게 충족시키는 테스트 라이너 및 플루팅 등급으로 전환하고 있습니다. 여전히 주로 저가 재활용 제품으로 경쟁하고 있는 제지 업체들은 사양 관리의 향상을 요구받고 있습니다. 왜냐하면, 자동화된 단기 납기 배송 시스템에서는 기존의 소매 채널보다 더 신속하게 구조적 취약성이나 압축 성능의 편차가 드러나기 때문입니다. 이러한 변화는 인도의 컨테이너보드 시장에 있어 중요한 의미를 지닙니다. 왜냐하면 대량 생산되고 가격에 민감한 포장 형태라 하더라도, 기술적으로 신뢰성이 높은 테크니컬 등급으로 수요가 점차 이동하고 있기 때문입니다.

식품 및 음료 포장의 고급화

인도의 식품 가공 및 음료 밸류체인에서는 조직화된 소매, 식품 안전 요건, 그리고 재활용 가능한 형태에 대한 노력이 모두 같은 방향으로 나아가고 있기 때문에 포장 규정이 꾸준히 강화되고 있습니다. 코카콜라, 펩시코, 펄 아그로 등의 브랜드 소유주들은 포장 포트폴리오를 재활용 가능한 형태로 조정하고 있으며, 그 결과 조직화된 유통 채널에서 단일 소재 및 섬유 기반의 2차 포장 사용이 증가하고 있습니다. 또한 식품 가공업체들도 라이너의 평량(坪量)을 150g/m²에서 120g/m²로 낮춤으로써 포장 중량을 줄이는 한편, 더욱 견고한 섬유 설계와 우수한 판지 공학을 통해 압축 성능을 유지하기 위해 노력하고 있습니다. 2026년 4월, 인도 식품안전기준청(FSSAI)은 판 마살라 및 담배 포장재에 대해 종이, 판지, 셀룰로오스 또는 기타 천연 유래 소재의 사용을 제안하는 고시 초안을 발표했습니다. 이로 인해 오랫동안 다층 플라스틱 구조에 의존해 온 분야에서도 섬유계 소재에 대한 규제상의 지원이 확대되었습니다. 이 변경 사항이 중요한 이유는 인도 남부 및 서부 지역에서는 이미 이러한 제품 카테고리에 대한 수요 밀도가 높기 때문에 포장 형태의 전환이 테스트 라이너 및 크라프트 등급에 대한 지역적 수요로 신속하게 파급될 가능성이 있기 때문입니다. 인도의 컨테이너보드 시장에서 이러한 프리미엄화 추세는 식품 관련 골판지 포장 전반에 걸쳐 인쇄 품질, 압축 강도의 균일성, 그리고 재활용성에 대한 기본적인 기대치를 높이고 있습니다.

폐지 및 수입 펄프의 가격 변동

인도에서는 재생 보드 원료의 상당 부분을 여전히 해상 운송을 통해 공급되는 재생 섬유에 의존하고 있으며, 이러한 높은 의존도 때문에 많은 생산자들이 수입 폐지(OCC) 및 기타 원료의 급격한 가격 변동에 취약한 상황에 놓여 있습니다. 이러한 위험은 환율 변동에 따라 더욱 커집니다. 왜냐하면, 달러 표시 국제 섬유 가격이 안정된 것처럼 보일지라도, 루피화 약세가 수입 비용을 상승시킬 가능성이 있기 때문입니다. 이로 인해 자사 펄프나 조림지를 통해 지원을 받는 통합형 기업과, 수입 원료에 대한 의존도가 높고 조달 주기가 짧은 재생섬유 공장 간의 격차가 확대되고 있습니다. 중소규모 공장은 특히 취약합니다. 수입 여건이 악화되었을 때 재고 완충 장치를 마련할 수 있는 재정적 유연성이 부족하기 때문에 갑작스러운 생산 감축이나 현지 가격 인상을 감수해야 할 가능성이 있기 때문입니다. 또한, 이러한 압력은 조달 활동에도 변화를 가져옵니다. 고순도 재생 원료를 필요로 하는 공장들은 국내 혼합 스크랩에 의존하기보다는 프리미엄 등급 원료를 놓고 보다 직접적으로 경쟁하게 될 것이기 때문입니다. 인도 컨테이너보드 시장에서 섬유 가격의 변동성은 통합 체제나 규모를 갖추지 못한 생산자들에게 여전히 가장 시급한 수익성 위험 요인으로 남아 있습니다.

부문별 분석

2025년 시점에서 인도의 컨테이너보드 시장에서 재생 섬유가 차지하는 비중은 64.53%였습니다. 이는 경쟁력을 유지하기 위해 여전히 재생 섬유에 크게 의존하고 있는 생산 거점의 비용 구조를 반영한 것입니다. 인도에서는 사용 후 종이 및 골판지의 50%가 재활용되고 있지만, 선진국에서는 85%에 달하고 있어, 국내 수거 효율이 제지 공장의 원료 수요를 완전히 충당하는 데 필요한 수준에는 아직 한참 못 미칩니다는 것을 알 수 있습니다. 이러한 격차는 공급량과 품질 모두에 영향을 미치고 있습니다. 수거 시스템의 취약성으로 인해 국내 재생섬유 공급이 불안정해지면서, 많은 제지 공장이 수입 폐지(OCC)에 의존할 수밖에 없기 때문입니다. 버진 섬유 부문은 여전히 소규모 시장이지만, 브랜드의 프리미엄화 및 수입 대체에 대한 투자가 고성능 크래프트 라이너 수요를 뒷받침함에 따라 2031년까지 연평균 성장률(CAGR) 6.02%로 성장할 것으로 전망됩니다. 따라서 인도의 컨테이너보드 시장에서는 원자재 전환이 양극화되고 있습니다. 재생 등급이 여전히 수량 면에서 우위를 점하고 있는 반면, 더 높은 압축 강도, 매끄러운 표면, 그리고 높은 균일성이 요구되는 용도에서는 버진 등급의 매력이 커지고 있습니다.

또한 버진 그레이드는 무역 조치의 혜택도 받고 있습니다. 무역구제총국이 중국의 원지에는 톤당 152.27달러, 칠레의 원지에는 톤당 123.18달러의 반덤핑 관세를 권고했기 때문입니다. 이러한 조치가 유지된다면, 국내 제지 업체들의 수익성이 개선될 가능성이 있습니다. FSC 인증 및 EPR(생산자 책임 확대) 준수는 인도 컨테이너보드 업계에서 특히 FMCG(일용소비재) 및 의약품 수출업체에게 시장 진입의 필수 요건으로 자리 잡고 있습니다. 이 기업들은 현재 추적성 및 지속가능성과 관련된 실적에 대해 포장 공급업체를 더욱 엄격하게 심사하고 있습니다. 파스와라 페이퍼스사는 이 부문에서 균형 감각이 얼마나 중요한지를 보여주고 있습니다. 이 회사는 크라프트지와 크라프트 라이너의 비율을 60대 40에서 라이너 중심의 생산 구조로 전환하는 동시에, 혼합 등급의 재생 펄프보다 미국에서 수입하는 고품질 DSOCC(탈산 처리된 단섬유)를 우선적으로 사용하고 있습니다. 이러한 움직임은 중견 제조업체들조차 범용 재활용 제품과 고사양 등급의 제품을 구분하기 시작했음을 보여줄 뿐만 아니라, 저등급 제품의 국내 회수량이 완만한 개선에 그치는 경우에도 고품질 수입 재생 펄프에 대한 수요는 견조한 추세를 유지할 수 있음을 시사합니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the india containerboard market size is expected to increase from USD 9.12 billion in 2025 to USD 9.58 billion in 2026 and reach USD 12.56 billion by 2031, growing at a CAGR of 5.55% over 2026-2031.

This report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and More). The Market Forecasts are Provided in Terms of Value (USD).

India Containerboard Market Trends and Insights

Rising E-Commerce And Quick-Commerce Corrugated Demand

India's quick-commerce sector reached USD 3.35 billion in gross merchandise value in 2024 and is projected to grow to USD 8.83 billion by 2028 at a 27.42% CAGR, which is reshaping packaging demand across urban fulfillment networks. Blinkit operated more than 1,500 dark stores across more than 100 cities in 2025, while Zepto and Swiggy Instamart had also scaled to dense dark-store networks, which widened the addressable base for short-cycle corrugated consumption. These networks do not just need more boxes; they need compact and right-sized corrugated packs that can withstand repeated lateral handling from picking to dispatch. That requirement is pushing buyers toward testliner and fluting grades that meet short-span compression and edge-crush needs with greater consistency, rather than relying only on burst-factor thresholds. Mills that still compete mainly on low-cost recycled output are under pressure to upgrade their specification control, because automated, fast-turn delivery systems are exposing weak formations and uneven compression performance more quickly than traditional retail channels did. This change is important for the India containerboard market because it is shifting demand toward technically dependable grades even within high-volume, price-sensitive packaging formats.

Food And Beverage Packaging Premiumization

India's food processing and beverage value chains are steadily tightening packaging specifications as organized retail, food safety requirements, and commitments to recyclable formats all move in the same direction. Brand owners such as Coca-Cola, PepsiCo, and Parle Agro have been aligning their packaging portfolios toward recyclable formats, thereby increasing the use of mono-material and fiber-based secondary packaging in organized distribution channels. Food processors are also reducing pack weights by moving liner grammages from 150 GSM toward 120 GSM while still trying to preserve compression performance through stronger fiber design and better board engineering. In April 2026, the Food Safety and Standards Authority of India issued a draft notification proposing paper, paperboard, cellulose, or other naturally derived materials for pan masala and tobacco packaging, extending the regulatory push for fiber-based formats into a category that had long relied on multi-layer plastic structures. That change matters because southern and western India already has high demand density for these product categories, so that any format migration can flow quickly into regional requirements for testliner and kraft grades. For the India containerboard market, this premiumization trend is raising the baseline expectation for print quality, compression consistency, and recyclability across food-linked corrugated packaging.

Wastepaper And Imported Fiber Price Volatility

India still relies on seaborne recovered fiber for a meaningful share of recycled-board furnish, and that dependence leaves many producers exposed to sudden cost swings in imported OCC and other feedstock streams. The risk is amplified by currency movement, because INR weakness can push landed costs higher even when dollar-denominated international fiber prices appear stable. This creates a widening gap between integrated players with captive pulp or plantation support and recycled-fiber mills that depend heavily on imported furnish and short procurement cycles. Smaller mills are especially vulnerable because they lack the financial flexibility to build inventory buffers when import conditions turn unfavorable, which can force abrupt production cuts or local price increases. The pressure also changes sourcing behavior, as mills seeking higher-purity recovered inputs compete more directly for premium grades rather than relying on mixed domestic scrap streams. For the India containerboard market, fiber volatility remains the most immediate profitability risk for producers that lack integration and scale.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push Toward Recyclable Fiber-Based Packaging

- Manufacturing And Export Logistics Expansion

- Power, Fuel, And Freight Cost Inflation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled fibers accounted for 64.53% of the India containerboard market in 2025, reflecting the cost logic of a manufacturing base that still depends heavily on recovered fiber to remain competitive. India recycled 50% of used paper and boards, compared with 85% in developed economies, which shows that domestic recovery efficiency is still far below the level needed to fully support mill furnish needs. That gap affects both availability and quality, because weaker collection systems produce a more uneven domestic recovered-fiber stream and keep many mills dependent on imported OCC. Virgin fiber grades remained the smaller material segment, but they are projected to grow at a 6.02% CAGR through 2031, as brand premiumization and investment in import substitution support higher-performance kraftliner demand. The India containerboard market is therefore seeing a two-speed material transition, where recycled grades still dominate volume while virgin grades are becoming more attractive for applications that require higher compression strength, smoother surfaces, and greater consistency.

Virgin grades are also benefiting from trade action, as the Directorate General of Trade Remedies recommended anti-dumping duties of USD 152.27 per metric ton on Chinese virgin paperboard and USD 123.18 per metric ton on Chilean virgin paperboard, which could improve the economics for domestic mills if those measures hold. FSC certification and EPR compliance are becoming commercial entry requirements in the Indian containerboard industry, especially for FMCG and pharmaceutical exporters, who are now screening packaging suppliers more closely for traceability and sustainability credentials. Paswara Papers illustrates the balancing act within the segment, as it has shifted from a 60:40 kraft-to-kraftliner mix toward a more liner-led output profile while prioritizing high-quality DSOCC imports from the United States over mixed-grade recovered fiber. That move shows how even mid-tier producers are separating commodity recycled output from higher-specification grades, and it also suggests that demand for premium imported recovered fiber can remain firm even if there is only a slow improvement in lower-grade domestic collection.

List of Companies Covered in this Report:

- ITC Limited

- JK Paper Limited

- West Coast Paper Mills Limited

- Tamil Nadu Newsprint and Papers Limited

- Emami Paper Mills Limited

- B&B Triplewall Containers

- Pakka Limited

- N R Agarwal Industries Limited

- Khanna Paper Mills Limited

- Paswara Papers Limited

- Bell Multi Kraft Private Limited

- Laxmi Board and Paper Mills Private Limited

- Apollo Papers LLP

- Venkraft Paper Mills Private Limited

- Aryan Paper Mills Private Limited

- Ruchira Papers Limited

- Star Paper Mills Limited

- Shree Ajit Pulp and Paper Limited

- Caliber Papers LLP

- Gauranga Papers LLP

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising E-Commerce and Quick-Commerce Corrugated Demand

- 4.2.2 Food and Beverage Packaging Premiumization

- 4.2.3 Regulatory Push Toward Recyclable Fiber-Based Packaging

- 4.2.4 Manufacturing and Export Logistics Expansion

- 4.2.5 Lightweighting and Strength Engineering for Automated Corrugation

- 4.2.6 Premium Kraftliner Import Substitution

- 4.3 Market Restraints

- 4.3.1 Wastepaper and Imported Fiber Price Volatility

- 4.3.2 Power, Fuel, and Freight Cost Inflation

- 4.3.3 Quality Variability in Domestic Recovered Fiber Streams

- 4.3.4 Post-2027 EU Waste Shipment Regulation Exposure

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ITC Limited

- 6.4.2 JK Paper Limited

- 6.4.3 West Coast Paper Mills Limited

- 6.4.4 Tamil Nadu Newsprint and Papers Limited

- 6.4.5 Emami Paper Mills Limited

- 6.4.6 B&B Triplewall Containers

- 6.4.7 Pakka Limited

- 6.4.8 N R Agarwal Industries Limited

- 6.4.9 Khanna Paper Mills Limited

- 6.4.10 Paswara Papers Limited

- 6.4.11 Bell Multi Kraft Private Limited

- 6.4.12 Laxmi Board and Paper Mills Private Limited

- 6.4.13 Apollo Papers LLP

- 6.4.14 Venkraft Paper Mills Private Limited

- 6.4.15 Aryan Paper Mills Private Limited

- 6.4.16 Ruchira Papers Limited

- 6.4.17 Star Paper Mills Limited

- 6.4.18 Shree Ajit Pulp and Paper Limited

- 6.4.19 Caliber Papers LLP

- 6.4.20 Gauranga Papers LLP

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment