|

시장보고서

상품코드

2065480

필리핀의 컨테이너보드 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Philippines Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

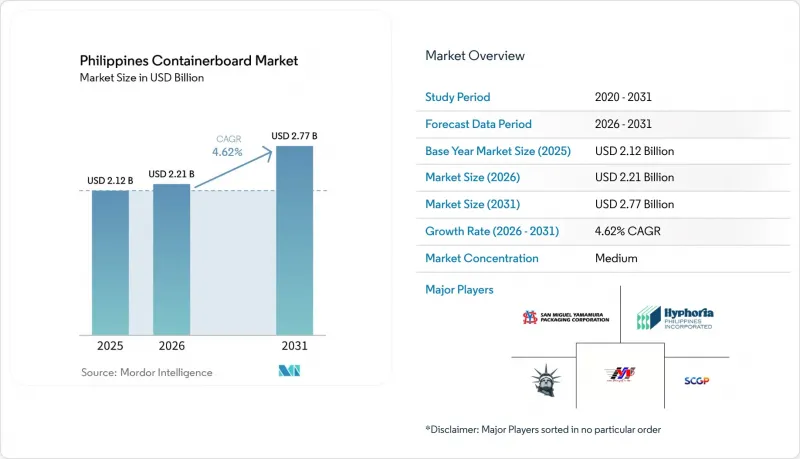

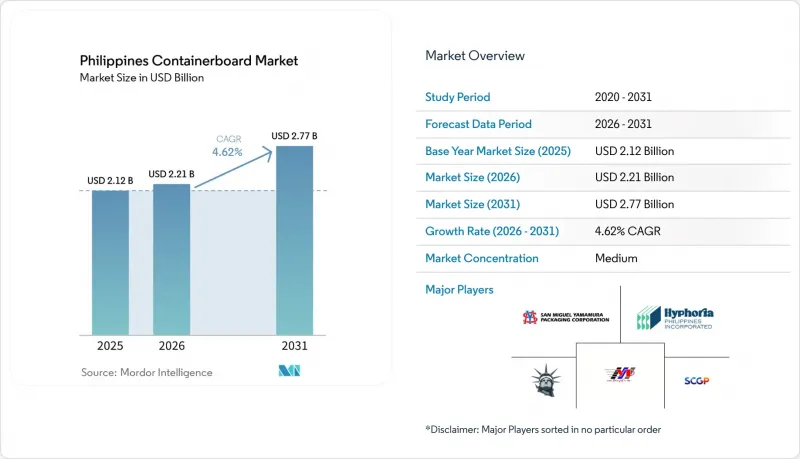

필리핀의 컨테이너보드 시장 규모는 2025년 21억 2,000만 달러로 평가되었고, 2026년 22억 1,000만 달러로 추정되고, 2031년까지 27억 7,000만 달러로 확대될 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR)은 4.62%를 나타낼 전망입니다.

본 보고서는 원료별(버진 섬유 및 재생 섬유), 제품 유형별(크래프트 라이너, 테스트 라이너, 플루팅), 그리고 최종 사용자 산업별(식품 및 음료, 소비재, 공업용 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

필리핀의 컨테이너보드 시장 동향 및 분석

포장 식품 및 음료의 생산 확대

포장 식품 및 음료의 생산은 도시, 지방, 그리고 섬들을 가로지르는 유통 채널에서 지속적인 운송 수요를 창출하기 때문에 필리핀의 컨테이너보드 시장에 있어 여전히 가장 강력한 수요의 주축으로 자리 잡고 있습니다. 필리핀 통계청의 보고에 따르면, 식품 생산량 지수는 2025년 5월에 전년 동월 대비 15.7% 상승했으며, 이후 산업 활동 전반의 성장세가 둔화되는 상황 속에서도 2026년 2월에는 3.4% 증가했습니다. 이는 식품 제조업이 다른 많은 제조업 분야에 비해 더 견고한 모습을 보이고 있음을 보여줍니다. 미국 농무부(USDA) 해외농업국도 2026년에 이어 성장이 지속될 것으로 전망하고 있으며, 그 요인 중 하나로 식품 가공업체의 물류상의 마찰을 완화하기 위한 정부의 이니셔티브을 꼽고 있습니다. 바랑가이가 주도하는 소매 모델은 상자 수요를 더욱 끌어올리는 요인이 될 것입니다. 이는 슈퍼마켓 중심의 시스템에 비해 상품의 운송 단위가 작고 보충 주기가 빈번하기 때문에 판매되는 제품 단위당 상자 소비량이 증가하기 때문입니다. 이러한 경향은 전체 산업 생산이 둔화되고 있는 상황에서도 필리핀 골판지 시장이 식품 용도로부터 지속적인 수요를 뒷받침받고 있는 이유와, 일용소비재 관련 가공업체들이 주로 선택적 소비재 분야에 의존하는 기업들보다 안정적인 수주 기반을 바탕으로 사업을 전개하는 경향이 있는 이유를 설명하는 한 가지 요인이 되고 있습니다.

전자상거래 소포 처리량 증가

전자상거래는 소포 배송 및 반품 처리에 사용되는 ‘일회용’을 전제로 한 골판지 포장 형태로 수요가 이동함에 따라, 필리핀의 골판지 시장을 지속적으로 재편하고 있습니다. 온라인 소매의 흐름은 기존의 도매 유통과는 다릅니다. 주문이 소량 발송으로 분할됨에 따라 골판지 사양이 변화하고, 취급 물량이 증가함에 따라, 경량이면서도 안정적인 품질을 갖춘 골판지 등급에 대한 지속적인 수요가 발생하고 있습니다. 이로 인해 모든 용도에서 수출용 등급의 판지를 필요로 하지 않게 되었으며, 소포 배송에 적합한 재생 테스트라이너와 경량 플루트 구조에 대한 수요가 뒷받침되고 있습니다. 이러한 혜택을 가장 크게 누리고 있는 것은 소셜 커머스나 마켓플레이스 채널을 이용하는 사업자를 대상으로 소량 생산, 다양한 치수, 신속한 납기에 대응할 수 있는 현지 가공업체들입니다. 그 결과, 포장 수요가 대형 계약 구매자에 그치지 않고 국내 판매업체, 물류업체, 택배업체 관련 고객 등 더 폭넓은 계층으로 확대됨에 따라 필리핀의 컨테이너보드 시장의 고객 기반이 확대되고 있습니다.

수입 골판지가 지역 제지 회사에 미치는 가격 압박

수입 골판지 원지는 여전히 필리핀 골판지 원지 시장에 심각한 제약 요인으로 작용하고 있습니다. 이는 현지 제지 제조업체들이 더 뛰어난 규모의 경제와 낮은 운영 비용을 갖춘, 더 대규모의 지역 생산 시스템을 갖춘 공급업체들과 경쟁할 수밖에 없기 때문입니다. 투자위원회(BOI)에 따르면, 국내 제지 부문에는 22개의 비통합형 제지 제조업체가 있으며, 이들의 총 생산 능력은 연간 165만 메트르톤에 달할 전망입니다. 이는 현지 시장으로서는 상당한 규모이지만, 지역의 유력 기업들과 비교하면 여전히 세분화되어 있습니다. 또한, 2026년 1월 관세위원회가 '인도네시아산 골판지 원지의 수입은 심각한 피해를 초래하지 않았다'는 판단을 내렸고, 그 후, 무역산업성이 최종 세이프가드 관세 적용을 요구하는 청구를 기각하고, 수입업체에 대한 현금 보증금 반환을 명령함에 따라 무역 정책을 통한 지원도 약화되었습니다. 그 결과, 특히 국내 생산자들이 구형 기계에 의존하고 있거나 높은 운영 비용에 직면해 있는 경우, 외국산 골판지 원지가 범용 등급 시장에서 보다 자유롭게 경쟁할 수 있는 여지가 다시 생겼습니다. 이러한 압박은 필리핀의 컨테이너보드 시장에서 특히 중요한 의미를 지닙니다. 왜냐하면 가공업체들은 수입품을 현지 제지업체의 가격 책정에 대한 협상 카드로 활용할 수 있기 때문에 최종 소비자 수요가 견조한 경우에도 국내 이익률이 압박을 받기 때문입니다.

부문별 분석

2025년에는 재생 섬유가 시장의 67.83%를 차지했으며, 이는 필리핀의 컨테이너보드 시장이 OCC(폐신문) 및 혼합 폐지를 원료로 얼마나 깊이 의존하고 있는지를 보여줍니다. 투자위원회(BOI)의 PAPELS 조사에 따르면, 필리핀 제지 생산에서 재생 섬유의 함유율은 95-100%에 달하며, 이러한 상황은 단순한 상업적 선호라기보다는 인프라의 현실을 반영한다고 할 수 있습니다. 실제로 필리핀에는 상업 규모의 버진 펄프용 조림지가 없기 때문에 이 나라의 골판지 산업은 현지 제지 공장이 폐지를 원료로 사용하는 모델을 중심으로 구축되어 있습니다. 따라서 재생 골판지는 안정적인 공급량을 확보하고 있으며, 그 수요는 최종 사용자의 포장재 선택 변화뿐만 아니라 수거 효율, 지자체 수거 시스템, 그리고 국내산 폐지 품질과도 밀접하게 연관되어 있습니다.

버진 섬유 시장은 2026-2031년 연평균 성장률(CAGR) 5.37%를 나타낼 것으로 예측되며, 규모는 작지만 가장 빠르게 성장하는 소재 분야가 될 것입니다. 이러한 기회는 특정 의약품 포장, 고급 소비재, 더 높은 청정도를 요구하는 섬유 등급이나 인증된 섬유 등급이 필요한 식품 용도 등, 재생 소재의 사용이 선호되지 않는 분야에서 비롯됩니다. 평판이 좋은 버진 크래프트 공급업체로부터 수입함으로써, 컨버터는 이러한 원자재를 확보할 수 있게 됩니다. 즉, 국내에서 펄프 산업의 통합이 이루어지지 않더라도 부가가치가 높은 수요는 확대될 수 있다는 것입니다. 이로 인해 필리핀의 컨테이너보드 업계에는 ‘양극화’ 구조가 형성되고 있습니다. 총 톤수 기준으로는 재생 원료가 여전히 주류를 이루고 있는 반면, 버진 펄프의 용도는 더 좁은 범위에서 사양을 중시하는 부문에서 부가가치를 창출하고 있습니다. SCGP가 동남아시아 전역의 섬유 포장 설비 업그레이드를 위해 수립한 2026년까지 130억 바트(3억 5,400만 달러) 규모의 투자 계획은 필리핀을 네트워크 전략에 포함시킨 지역 기업들에게 있어 고부가가치 포지셔닝이 점점 더 중요해지고 있음을 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the philippines containerboard market size is projected to expand from USD 2.12 billion in 2025 and USD 2.21 billion in 2026 to USD 2.77 billion by 2031, registering a CAGR of 4.62% between 2026 to 2031.

This report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and More). The Market Forecasts are Provided in Terms of Value (USD).

Philippines Containerboard Market Trends and Insights

Packaged Food And Beverage Output Expansion

Packaged food and beverage production remains the strongest demand anchor for the Philippines containerboard market because it creates recurring shipping needs across urban, provincial, and inter-island distribution channels. The Philippine Statistics Authority reported that the volume of production index for food products rose 15.7% year over year in May 2025, then increased 3.4% in February 2026 even as wider industrial activity stayed less even, which shows that food manufacturing has been more defensive than many other factory categories. The USDA Foreign Agricultural Service also projected continued expansion in 2026 and linked part of that support to government efforts aimed at reducing logistics friction for food processors. The barangay-led retail model adds another layer of box demand because goods often move in smaller shipment formats and more frequent replenishment cycles than in supermarket-heavy systems, which raises box conversion intensity per unit of product sold. That pattern helps explain why the Philippines containerboard market draws durable support from food applications even when headline industrial production softens and why converters tied to everyday consumer staples tend to operate with a steadier order base than firms exposed mainly to discretionary categories.

E-Commerce Parcel Volume Growth

E-commerce continues to reshape the Philippines containerboard market by shifting more packaging demand toward single-trip corrugated formats used in parcel delivery and return handling. Online retail flows differ from traditional wholesale movement because orders are broken into smaller shipments, which changes box specifications, increases the number of units handled, and creates repeat demand for light but consistent corrugated grades. This has supported demand for recycled testliners and lighter fluting structures that suit parcel shipping without requiring export-grade board in every application. The benefit is strongest for local converters that can handle short production runs, varied dimensions, and quick turnaround times for merchants serving social commerce and marketplace channels. The result is a broader customer base for the Philippines containerboard market because packaging demand is spreading beyond large contract buyers and into a wider pool of domestic sellers, fulfillment operators, and courier-linked accounts.

Imported Board Price Pressure On Local Mills

Imported containerboard remains a serious constraint on the Philippines containerboard market because local mills compete against suppliers from larger regional production systems with better economies of scale and lower operating costs. The Board of Investments noted that the domestic paper sector includes 22 non-integrated mills with combined capacity of 1.65 million metric tons per year, which is sizable for the local market but still fragmented compared with regional heavyweights. Trade policy support also weakened after the Tariff Commission's January 2026 finding that Indonesian corrugating medium imports did not cause serious injury, and the Department of Trade and Industry later rejected the petition for definitive safeguard duties and ordered cash bond refunds to importers. That outcome reopened room for foreign board to compete more freely in commodity grades, especially where domestic producers rely on older machines or face higher operating costs. The pressure is especially relevant in the Philippines containerboard market because converters can use imports as a negotiating check on local mill pricing, which compresses domestic margins even when end-user demand remains healthy.

Other drivers and restraints analyzed in the detailed report include:

- Electronics And Industrial Export Packaging Demand

- Better Domestic Wastepaper Recovery And Reuse

- High Electricity Costs Versus ASEAN Peers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled fibers held 67.83% of the market in 2025, which shows how deeply the Philippines containerboard market depends on OCC and mixed wastepaper as its operating base. The Board of Investments PAPELS study stated that recycled fiber content in Philippine paper production runs at 95-100%, which means this position reflects infrastructure reality more than a simple commercial preference. In practice, the Philippines containerboard industry is built around a feedstock model where local mills work with recovered paper because commercial-scale virgin pulp plantations are not available in the country. That gives recycled board a stable volume role and keeps its demand closely linked to collection efficiency, municipal recovery systems, and the quality of domestically sourced wastepaper rather than only to shifts in end-user packaging choice.

Virgin fibers are projected to grow at a 5.37% CAGR from 2026 to 2031, which makes them the fastest-moving material niche even from a small base. The opportunity comes from applications where recycled content is less favored, including select pharmaceutical packaging, premium consumer goods, and food uses that require cleaner or certified fiber grades. Imports from established virgin kraft suppliers give converters access to these substrates, which means value-added demand can grow even without domestic pulp integration. This creates a two-speed structure in the Philippines containerboard industry, where recycled inputs remain dominant in tonnage while virgin-fiber applications capture incremental value in narrower, specification-driven segments. SCGP's 2026 investment plan of THB 13,000 million, or USD 354 million, for fiber packaging upgrades across Southeast Asia reinforces that higher-value positioning is becoming more important for regional players that include the Philippines in their network strategy.

List of Companies Covered in this Report:

- United Pulp and Paper Co., Inc.

- San Miguel Yamamura Packaging Corporation

- Valenzuela Packaging Container Corporation

- Hyphoria Philippines Inc.

- Papercon (Phils.) Inc.

- 3D Container and Packaging Phils. Corp.

- Total Packaging Solutions and Manufacturing, Inc.

- Mina Moto Packaging Corp.

- Corbox Corporation

- Liberty Corrugated Boxes Mfg. Corp.

- Davao Fibreboard Packaging Plant Inc.

- Duraboard Packaging Corp.

- Goldrich Industrial Packaging Corporation

- Malinta Corrugated Boxes Manufacturing Corporation

- Tenaga Pack Solution Inc.

- Cr8tive Boxes and Labels Corporation

- SBC Packaging OPC

- GagMax Packaging Solutions Inc.

- STC Paper and Plastic Packaging Solutions

- SuperPack Enterprises

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Packaged Food and Beverage Output Expansion

- 4.3.2 E-Commerce Parcel Volume Growth

- 4.3.3 Electronics and Industrial Export Packaging Demand

- 4.3.4 Better Domestic Wastepaper Recovery and Reuse

- 4.3.5 Corrugating Medium Safeguard Action Supporting Local Utilization

- 4.3.6 ISO 14001:2026 Adoption Favoring Traceable Fiber Packaging

- 4.4 Market Restraints

- 4.4.1 Imported Board Price Pressure on Local Mills

- 4.4.2 High Electricity Costs Versus ASEAN Peers

- 4.4.3 Recycling-Center Scarcity Outside Major Urban Hubs

- 4.4.4 Port Congestion and Elevated Container Freight Costs

- 4.5 Industry Value Chain Analysis

- 4.6 Supply Chain Analysis

- 4.7 Regulatory Landscape

- 4.8 Technological Outlook

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Bargaining Power of Buyers

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 United Pulp and Paper Co., Inc.

- 6.4.2 San Miguel Yamamura Packaging Corporation

- 6.4.3 Valenzuela Packaging Container Corporation

- 6.4.4 Hyphoria Philippines Inc.

- 6.4.5 Papercon (Phils.) Inc.

- 6.4.6 3D Container and Packaging Phils. Corp.

- 6.4.7 Total Packaging Solutions and Manufacturing, Inc.

- 6.4.8 Mina Moto Packaging Corp.

- 6.4.9 Corbox Corporation

- 6.4.10 Liberty Corrugated Boxes Mfg. Corp.

- 6.4.11 Davao Fibreboard Packaging Plant Inc.

- 6.4.12 Duraboard Packaging Corp.

- 6.4.13 Goldrich Industrial Packaging Corporation

- 6.4.14 Malinta Corrugated Boxes Manufacturing Corporation

- 6.4.15 Tenaga Pack Solution Inc.

- 6.4.16 Cr8tive Boxes and Labels Corporation

- 6.4.17 SBC Packaging OPC

- 6.4.18 GagMax Packaging Solutions Inc.

- 6.4.19 STC Paper and Plastic Packaging Solutions

- 6.4.20 SuperPack Enterprises

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Future Outlook