|

시장보고서

상품코드

2065755

인도의 통합 시설 관리 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)India Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

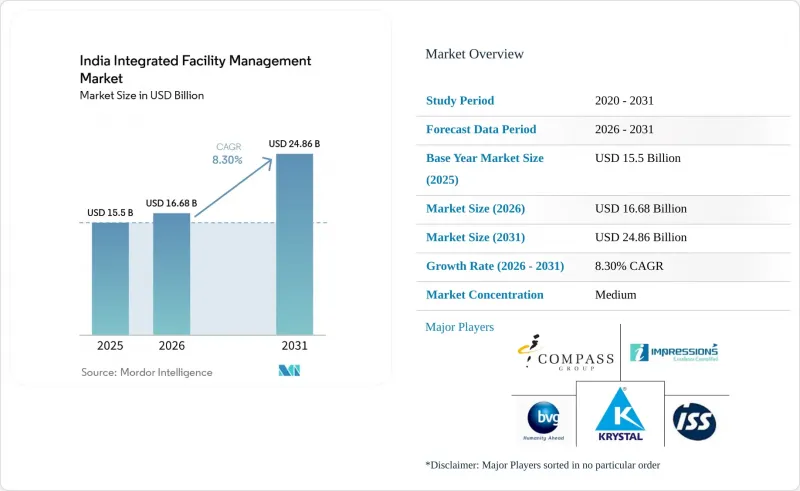

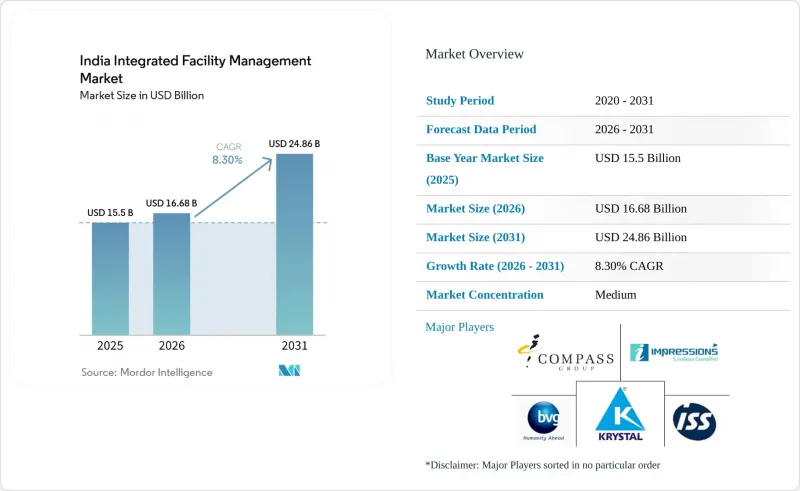

Mordor Intelligence에 의하면, 인도의 통합 시설 관리 시장 규모는 2025년에 155억 달러로 평가되었고, 2026년에 166억 8,000만 달러로 추정되고, 2031년까지 248억 6,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 8.30%로 성장할 전망입니다.

본 보고서는 서비스 유형별(하드 시설 관리(자산 관리, MEP 및 HVAC 서비스 등), 소프트 시설 관리(사무 지원 및 보안, 청소 서비스, 케이터링 서비스 등]) 및 최종 사용자별(상업시설, 호스피탈리티, 공공기관 및 공공 인프라, 의료시설 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

인도의 통합 시설 관리 시장 동향 및 인사이트

A급 오피스 및 복합 용도 캠퍼스의 확대

인도의 A급 오피스 시장은 2025년에 사상 최고 실적을 기록했으며, 주요 8개 도시의 순흡수 면적은 6,140만 제곱피트에 달하고, 전년 대비 25% 증가했습니다. 이로 인해 지속적인 운영 지원이 필요한 전문적으로 관리되는 부동산의 규모가 직접적으로 확대되었습니다. 또한, 2026년 아시아태평양에서 공급될 6,130만 제곱피트의 신규 A급 오피스 공급량의 40%를 인도가 차지할 것으로 예상되며, 이에 따라 인도의 통합 시설 관리 시장에서 신규 프로젝트 파이프라인은 활발한 상태를 유지할 것으로 보입니다. 공급량의 구성과 마찬가지로, 품질의 구성도 중요합니다. 2026년 신규 공급 물량의 80%가 친환경 인증을 획득할 것으로 예상되며, 이에 따라 에너지 관리, 물 사용량 모니터링, 실내 공기질 관리, 그리고 감사에 대응할 수 있는 보고와 관련된 서비스 기준이 높아질 것이기 때문입니다. 또한 복합 용도 캠퍼스에서는 사무실, 소매, 숙박, 외식 서비스 등의 기능이 단일 관리 체계 하에 통합되어 있으며, 이에 따라 소유주는 여러 서비스 분야에 걸쳐 단일한 책임 있는 운영 사업자를 지정하는 경향이 강해지고 있습니다. 이러한 규모, 기술적 요건 및 소유주의 선호도가 복합적으로 작용함에 따라, 하드 FM과 소프트 FM의 균형을 갖춘 전문성을 보유한 통합형 서비스 제공업체가 계속해서 우위를 점하고 있으며, 이는 인도의 통합 시설 관리 시장에서 보다 종합적인 IFM 계약으로의 전환을 촉진하고 있습니다.

통합형 및 성과 기반 계약에 대한 공급업체 통합

인도의 통합 시설 관리 시장은 인력 수에 의존하는 계약 방식에서 단순한 인력 배치가 아닌 가동률, 에너지 효율, 위생 품질, 사용자 경험을 측정하는 SLA(서비스 수준 계약) 연계형 비즈니스 모델로 전환되고 있습니다. 5개 이상의 서비스 범주에 걸쳐 단일 IFM 파트너를 활용하고 있는 기업들은 벤더 관리에 드는 간접비가 평균 18% 감소했다고 보고하고 있으며, 이를 통해 조달 팀은 통합을 통한 직접적인 비용 절감과 관리 효율화 근거를 확보하고 있습니다. 이러한 변화는 하드 FM의 전략적 가치도 높이고 있습니다. 왜냐하면 HVAC 가동률, 전기 시스템의 신뢰성, 전력 사용 효율과 같은 기술적 지표는 입찰 단계에서 많은 소프트 서비스의 산출물보다 검증 및 관리가 용이하기 때문입니다. 인도 사무실 부동산 전반에 걸쳐 기관 투자자의 소유 비중이 확대되고 있으며, REIT 전환 가능성이 있는 A급 공간은 3억 8,000만 제곱피트 이상에 달할 전망입니다. 이러한 소유주들은 지역별로 개별적인 운영 체제를 갖추기보다는 분산된 포트폴리오 전체에 일관된 기준을 적용하는 것을 선호합니다. 이 모델이 표준화됨에 따라, 전국적인 확장 능력, 데이터 시스템, 규정 준수 대응 역량이 부족한 소규모 기업들은 비록 지역 차원에서 가격 경쟁력을 유지하고 있다 하더라도, 인도의 통합 시설 관리 시장에서 점유율을 잃을 가능성이 높을 것입니다.

비조직적인 공급업체에 의한 가격 주도형 경쟁

비조직적인 공급업체들이 주도하는 가격 경쟁은 여전히 인도 통합 시설 관리 시장에서 가장 뚜렷한 구조적 걸림돌로 남아 있습니다. 소규모 공급업체들은 적립 기금, 근로자 주 보험 및 최저임금 의무를 회피함으로써, 조직화된 기업보다 15%에서 20% 더 저렴한 가격을 책정하고 있습니다. 이러한 압박은 청소, 하우스키핑, 경비 분야에서 가장 심하며, 이는 해당 분야에서 인건비가 주요 비용 요인인 데다, 조달 시 구매자가 서비스 품질을 객관적으로 평가하기 어려운 경우가 많기 때문입니다. 이 문제는 계약 체결로 끝나지 않습니다. 왜냐하면, 그 시점에서 드러난 가격 차이가 계약 갱신 협상에 영향을 미쳐, 조직화된 기업들이 법규를 준수한 서비스 제공 모델에서 더 낮은 요금을 수용하도록 새로운 압력을 가하게 되기 때문입니다. 인도의 노동법 통합으로 인해 향후 경쟁 균형이 개선될 가능성은 있지만, 주 차원에서의 이행 상황에는 여전히 편차가 있어 지역에 따라 법 집행 결과에 일관성이 없습니다. 그럼에도 불구하고, 대기업의 구매 담당자들은 최저가 결정에서 총소유비용(TCO) 검토로 점차 전환하고 있으며, 이로 인해 인도의 통합 시설 관리 시장에서 품질의 균형이 서서히 개선될 것으로 보입니다.

부문별 분석

하드 시설 관리(FM) 시장은 2031년까지 연평균 성장률(CAGR) 9.47%로 확대될 것으로 예상되며, 이는 시장 전체의 성장률을 상회하는 수치로, 인도의 통합 시설 관리(IFM) 시장에서 서비스 부문의 가장 강력한 성장 동력으로 자리 잡고 있습니다. 이러한 성장 가속화는 A급 자산의 기술 집약도 향상 및 데이터센터 확장과 밀접한 관련이 있으며, 국내 데이터센터용량은 2025년 말 약 1.7 GW에서 2030년도까지 4GW 이상으로 증가할 것으로 예측됩니다. 이러한 확장에 따라 MEP 서비스, HVAC 관리, 전력 공급의 신뢰성 확보, 전원 백업 지원, 그리고 일반 서비스 사업자가 쉽게 규모를 확대할 수 없는 24시간 365일 기술 인력 배치에 대한 수요가 높아지고 있습니다. 또한, REIT 주도의 포트폴리오와 GCC 캠퍼스가 정기적인 유지보수 주기에서 라이프사이클 계획, 교체 관리, 설비 투자(Capex)와 연계된 관리 방식으로 전환됨에 따라 자산 관리 서비스의 역할도 확대되고 있습니다.

2025년 현재, 인도의 IFM 시장 규모 중 소프트 FM이 67.19%의 점유율을 차지했으며, 이는 인도의 상업, 호텔 및 관광, 의료, 공공시설에서 청소, 급식, 사무 지원, 경비 업무에 필요한 막대한 노동력을 반영한 것입니다. 이 부문은 일상적인 입주 경험과 직결되며, 대규모 임차인이 여러 거점으로 구성된 포트폴리오 전체에서 이를 자체적으로 처리하기 어렵기 때문에 많은 서비스 제공업체에게 여전히 주요 수익원입니다. 그렇긴 하지만, 통합 계약 내의 서비스 구성은 서서히 변화하고 있습니다. 이는 하드 서비스의 경우 평방피트당 부가가치가 높고, 노동 집약적인 소프트 서비스에 비해 SLA(서비스 수준 계약)에 기반한 성과를 측정하기가 더 쉽기 때문입니다. 청소 업무는 기계화 및 로봇을 활용한 바닥 관리의 혜택을 누리고 있는 반면, 사무 지원 및 경비 기능은 AI를 활용한 감시 및 지능형 방문자 관리를 통해 고도화가 진행되고 있습니다. 이를 통해 인도의 IFM 업계는 치열한 가격 경쟁 환경 속에서도 서비스 품질을 유지할 수 있게 되었습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSH 26.06.24According to Mordor Intelligence, the india integrated facility management market size is projected to be USD 15.5 billion in 2025, USD 16.68 billion in 2026, and reach USD 24.86 billion by 2031, growing at a CAGR of 8.30% from 2026 to 2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), and End User (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, and More). The Market Forecasts are Provided in Terms of Value (USD).

India Integrated Facility Management Market Trends and Insights

Expansion Of Grade A Offices and Mixed-use Campuses

India's Grade A office market delivered its strongest year on record in 2025, with net absorption of 61.4 million sq ft across the top 8 cities, up 25% year over year, thereby directly expanding the professionally managed estate that requires continuous operating support. India is also expected to account for 40% of Asia-Pacific's 61.3 million sq ft of new Grade A office supply in 2026, which keeps the onboarding pipeline active for the India integrated facility management market. The quality mix matters as much as the quantity mix, because 80% of the new 2026 supply is expected to be green-certified, and that raises the service threshold for energy management, water monitoring, indoor air quality control, and audit-ready reporting. Mixed-use campuses are also bringing office, retail, hospitality, and food service functions into a single managed environment, which makes owners more likely to appoint one accountable operator across multiple service lines. This combination of scale, technical requirements, and ownership preference continues to favour integrated providers with balanced Hard FM and Soft FM depth, which supports the move toward fuller IFM contracts within the India integrated facility management market.

Vendor Consolidation into Integrated and Outcome-based Contracts

The India integrated facility management market is moving away from headcount-driven contracts and toward SLA-linked commercial models that measure uptime, energy efficiency, hygiene quality, and user experience rather than just labour deployment. Enterprises that use a single IFM partner across 5 or more service categories have reported an average 18% reduction in vendor management overhead, which gives procurement teams a direct cost and control argument for consolidation. This shift also lifts the strategic value of Hard FM, because technical metrics such as HVAC uptime, electrical reliability, and power usage performance are easier to verify and govern than many soft-service outputs at the bid stage. Institutional ownership is expanding across India's office stock, with more than 380 million sq ft of Grade A space carrying REIT potential, and these owners prefer consistent standards across distributed portfolios rather than separate local operating arrangements. As this model becomes standard, smaller firms without national reach, data systems, and compliance depth are likely to lose share in the India integrated facility management market even when they remain locally competitive on price.

Price-led Competition from Unorganized Vendors

Price-led competition from unorganized vendors remains the clearest structural brake on the India integrated facility management market, with smaller operators undercutting organized firms by 15% to 20% by bypassing Provident Fund, Employees' State Insurance, and minimum wage obligations. The pressure is strongest in cleaning, housekeeping, and security, where labour is the main cost input and output quality is often harder for buyers to benchmark objectively during procurement. The problem does not end at contract award, because the visible price gap then shapes renewal discussions and creates fresh pressure on organized firms to accept lower rates on compliant delivery models. India's labour code consolidation could improve the competitive balance over time, but state-level implementation remains uneven, and that keeps enforcement outcomes inconsistent across locations. Even so, large enterprise buyers are slowly shifting from lowest-bid decisions toward total-cost-of-ownership reviews, which should gradually improve the quality mix in the India integrated facility management market.

Other drivers and restraints analyzed in the detailed report include:

- Wider Adoption of Smart Buildings and Predictive Maintenance

- Sustainability-led Demand for Energy, Water and Waste Optimization

- Skilled Workforce Attrition and Wage Inflation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hard facility management (FM) is forecast to expand at a 9.47% CAGR through 2031, which places it ahead of the overall growth rate and makes it the strongest service-side growth engine in the India integrated facility management (IFM) market. This acceleration is closely tied to higher technical density in Grade A assets and to data center expansion, with national capacity projected to rise from nearly 1.7 GW at the end of 2025 to more than 4 GW by FY30. That buildout increases demand for MEP services, HVAC management, electrical reliability, power backup support, and 24/7 technical staffing that general service operators cannot easily scale. Asset management services are also gaining a larger role as REIT-led portfolios and GCC campuses shift from periodic maintenance cycles toward lifecycle planning, replacement tracking, and capex-linked stewardship.

Soft FM held 67.19% share of the India IFM market size in 2025, which reflects the large labour base needed for cleaning, catering, office support, and security across India's commercial, hospitality, healthcare, and institutional estate. The segment remains the revenue anchor for many providers because it touches daily occupancy experience and is difficult for large occupiers to internalize across multi-site portfolios. Even so, the service mix inside integrated contracts is gradually shifting, because hard services carry higher value per square foot and support more measurable SLA outcomes than many labour-heavy soft lines. Cleaning is benefiting from mechanization and robotic floor care, while office support and security functions are being upgraded through AI-assisted surveillance and intelligent visitor management, which helps the India IFM industry defend service quality in a price-sensitive environment.

List of Companies Covered in this Report:

- BVG India Limited

- SIS Limited

- Sodexo India Services Private Limited

- Updater Services Limited

- Bluspring Enterprises Limited

- ISS Facility Services India Private Limited

- Krystal Integrated Services Limited

- CBRE South Asia Private Limited

- Jones Lang LaSalle Property Consultants (India) Private Limited

- Cushman & Wakefield India Private Limited

- Compass Group India (Compass Group PLC)

- Colliers International (India) Property Services Private Limited

- Knight Frank (India) Private Limited

- Tenon Facility Management India Private Limited

- Dusters Total Solutions Services Private Limited

- Property Solutions (India) Private Limited

- OCS India

- SMS Integrated Facility Services Private Limited

- Impressions Services Private Limited

- ServiceMax Facility Management Private Limited

- Supreme Facility Management Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Grade A Offices and Mixed-use Campuses

- 4.2.2 Vendor Consolidation Into Integrated and Outcome-based Contracts

- 4.2.3 Wider Adoption of Smart Buildings and Predictive Maintenance

- 4.2.4 Sustainability-led Demand for Energy, Water and Waste Optimization

- 4.2.5 Global Capability Centre Expansion Beyond Tier-1 Hubs

- 4.2.6 Data Centre and Mission-critical Infrastructure Buildout

- 4.3 Market Restraints

- 4.3.1 Price-led Competition From Unorganized Vendors

- 4.3.2 Skilled Workforce Attrition and Wage Inflation

- 4.3.3 Working-capital Stress From Delayed Receivables

- 4.3.4 Utility Reliability and Water-stress Exposure in Critical Assets

- 4.4 Industry Value Chain Analysis

- 4.5 Technology Analysis

- 4.6 Regulatory Landscape

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 By End User

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 BVG India Limited

- 6.4.2 SIS Limited

- 6.4.3 Sodexo India Services Private Limited

- 6.4.4 Updater Services Limited

- 6.4.5 Bluspring Enterprises Limited

- 6.4.6 ISS Facility Services India Private Limited

- 6.4.7 Krystal Integrated Services Limited

- 6.4.8 CBRE South Asia Private Limited

- 6.4.9 Jones Lang LaSalle Property Consultants (India) Private Limited

- 6.4.10 Cushman & Wakefield India Private Limited

- 6.4.11 Compass Group India (Compass Group PLC)

- 6.4.12 Colliers International (India) Property Services Private Limited

- 6.4.13 Knight Frank (India) Private Limited

- 6.4.14 Tenon Facility Management India Private Limited

- 6.4.15 Dusters Total Solutions Services Private Limited

- 6.4.16 Property Solutions (India) Private Limited

- 6.4.17 OCS India

- 6.4.18 SMS Integrated Facility Services Private Limited

- 6.4.19 Impressions Services Private Limited

- 6.4.20 ServiceMax Facility Management Private Limited

- 6.4.21 Supreme Facility Management Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment