|

시장보고서

상품코드

2066510

반려동물 케어 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Pet Care - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

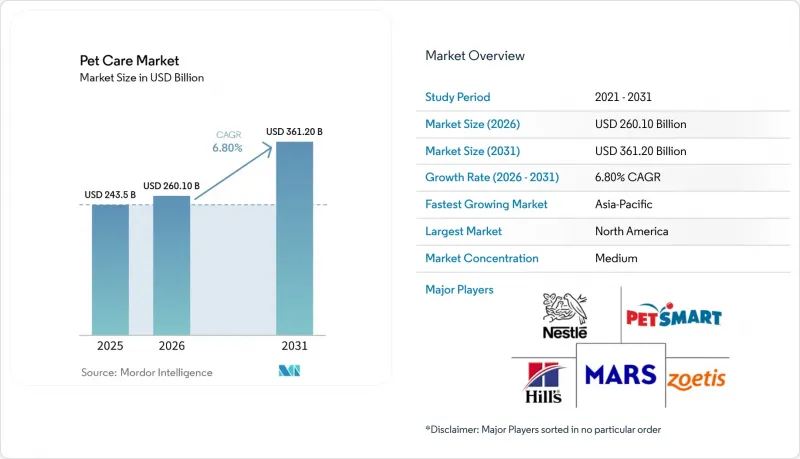

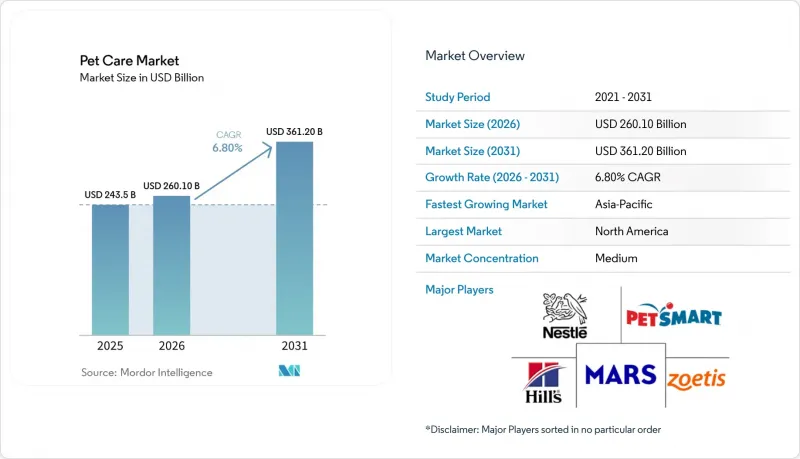

Mordor Intelligence에 의하면, 반려동물 케어 시장 규모는 2025년에 2,435억 달러로 평가되었고, 2026년 2,601억 달러로 추정되고, 2031년까지 3,612억 달러로 성장할 전망이며, 2026-2031년 CAGR 6.80%를 나타낼 것으로 예측됩니다.

본 보고서는 제품 유형별(반려동물 사료, 반려동물 건강 관리, 반려동물 미용 제품, 반려동물 용품, 반려동물 서비스), 동물 유형별(개, 고양이, 기타 동물), 유통 채널별(오프라인 소매, 온라인 소매) 및 지역별(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 반려동물 케어 시장 동향 및 인사이트

반려동물의 ‘인간화’와 ‘프리미엄화’

반려동물의 ‘인간화’와 ‘프리미엄화’가 반려동물 케어 시장의 장기적인 성장을 이끌고 있습니다. 이는 소비자들이 반려동물을 점점 더 가족의 일원으로 여기고, 건강 증진에 중점을 둔 제품 및 서비스에 대한 지출을 늘리고 있기 때문입니다. 미국 반려동물 제품 협회(American Pet Products Association)에 따르면, 2025년 미국의 반려견 보유율은 전년의 51%에서 53%로 증가할 것으로 예상되며, 이는 프리미엄 영양 식품, 예방 의료, 진단, 미용 및 환경 풍부화 관련 반려동물 관리 제품에 대한 수요가 증가하고 있음을 여실히 보여주고 있습니다. 또한, 반려동물에 대한 정서적 애착이 높아짐에 따라 만성 질환 관리, 전문적인 치료, 노화에 따른 의료 서비스에 대한 지출이 증가하고 있으며, 이는 반려동물 케어 시장의 지속적인 가치 성장에 기여하고 있습니다.

예방 의료와 반려동물 보험의 보급

예방 의료와 반려동물 보험의 보급이 반려동물 케어 시장의 성장을 이끌고 있습니다. 보험 적용 범위가 확대됨에 따라 진단, 치료 및 정기적인 수의학 서비스에 대한 지출이 증가하고 있기 때문입니다. 북미 반려동물 건강보험협회(NAPHIA)에 따르면, 북미의 보험료 수입 총액은 2023년 42억 달러에서 2024년에는 52억 달러에 달했습니다. 반려동물 보험 가입률 증가는 예방 의료, 만성 질환 관리 및 첨단 수의학 서비스에 대한 접근성을 높이고 있습니다. 또한, 반려동물 주인들이 사랑하는 반려동물을 위해 더 높은 수준의 임상 치료와 웰니스 서비스를 찾게 되는 동기가 되고 있습니다.

원자재 및 포장 비용의 변동

원자재 및 포장 비용의 변동은 여전히 펫케어 시장에 있어 큰 제약 요인으로 작용하고 있습니다. 단백질 원료, 포장 자재, 운송비, 에너지 가격의 변동은 제조 원가와 소비자 가격에 직접적인 영향을 미치고 있습니다. Zoetis Inc.의 2025년 연차 보고서에 따르면, 거시경제적 압박과 가계 지출 감소가 동물병원 방문 동향과 반려동물용 헬스케어 각 부문의 구매 행태에 영향을 미치고 있습니다. 반려동물 주인들의 비용 의식이 높아짐에 따라, 각 기업은 반려동물 케어 업계에서 이익률을 유지하기 위해 공급망 관리 강화, 조달 전략 최적화, 그리고 업무 효율 향상을 최우선 과제로 삼고 있습니다.

부문별 분석

2025년, 반려동물 케어 시장에서 반려동물 사료 부문의 점유율은 52.6%로 가장 높은 비중을 차지했습니다. 반려동물사료는 구매 빈도가 정기적이고, 제품을 구하기 쉬우며, 프리미엄 제품이나 기능성 영양 제품에 대한 소비자의 선호도가 높아지고 있는 점 등으로 인해 여전히 주요 카테고리로 자리 잡고 있습니다. 수요는 소화기 건강, 체중 관리, 연령별 영양 요구를 충족시키는 신선·냉장, 그레인 프리, 수의사가 추천하는 제품으로 이동하고 있습니다. 각 제조업체들은 지속 가능한 원료와 맞춤형 사료 솔루션을 도입함으로써 프리미엄 제품 라인업을 확대되고 있습니다. 슈퍼마켓, 반려동물 전문점, 동물병원, 전자상거래 플랫폼을 통한 소매망의 강력한 확산이 전 세계 선진국 및 신흥국의 반려동물 케어 시장에서 안정적인 소비자 지출을 지속적으로 뒷받침하고 있습니다.

반려동물 케어 시장 중 반려동물 서비스 분야 시장 규모는 2026-2031년 연평균 성장률(CAGR) 10.0%라는 가장 높은 성장률을 기록하며 확대될 것으로 전망됩니다. 이러한 성장은 수의학, 미용, 데이케어, 펫 호텔, 보험, 예방 의료 서비스에 대한 지출 증가에 힘입어 이루어지고 있습니다. 소비자들은 반려동물의 건강 관리와 정기적인 의료 서비스를 자유재량 지출이 아닌 필수적인 가계비로 인식하기 시작했습니다. 또한, 도시 지역 시장에서는 정액제 수의학 플랜, 원격 진료, 진단, 행동 지원 서비스도 급속히 확대되고 있습니다. 또한, 반려동물의 고령화와 예방 치료에 대한 인식이 높아짐에 따라, 반려동물 의료 생태계 내에서 정기적인 진료와 건강 유지에 중점을 둔 반려동물 서비스에 대한 장기적인 수요가 계속해서 주도하고 있습니다.

지역별 분석

2025년, 북미의 반려동물 케어 시장 점유율은 33.5%로 가장 높은 비중을 차지했습니다. 이러한 선도적인 위상은 높은 반려동물 사육률, 선진적인 수의의료 인프라, 예방의료 서비스의 광범위한 보급, 그리고 프리미엄 반려동물 영양·웰니스 제품에 대한 소비자들의 막대한 지출에 기인합니다. 이 지역은 동물병원 네트워크의 확대, 진단 및 만성 질환 관리에 대한 수요 증가, 그리고 구독형 반려동물 의료 서비스 이용 증가의 혜택을 누리고 있습니다. 또한, 미국과 캐나다에서는 반려동물 보험 가입률이 상승하고 예방 의료에 대한 관심이 높아지면서, 수의학 서비스, 의약품, 영양, 웰니스 등 각 분야의 지출을 견인하고 있습니다.

아시아태평양 시장 규모는 2026-2031년 연평균 성장률(CAGR) 9.6%라는 가장 높은 성장률을 기록하며 확대될 것으로 전망됩니다. 도시화, 가구 규모 축소, 출산 연령 상승, 가처분 소득 증가 등이 중국, 인도, 일본, 한국 및 동남아시아 국가들의 반려동물 사육 수 증가에 기여하고 있습니다. 소비자들은 반려동물을 위한 프리미엄 영양 식품, 예방 의료, 미용, 진단, 웰니스 서비스에 더 많은 자원을 할애하고 있습니다. 또한, 디지털 커머스 및 앱 기반 반려동물 관리 플랫폼 덕분에 대도시권에서 제품 및 수의사 상담 서비스에 대한 접근성이 향상되고 있습니다. 국내외 기업들은 급속히 성장하는 지역 반려동물 케어 시장에서 입지를 강화하기 위해 프리미엄 제품 포트폴리오와 옴니채널 유통 전략에 투자하고 있습니다.

유럽은 반려동물 사육이 정착된 추세와 수준 높은 수의학 서비스, 그리고 예방 의료 및 웰니스에 대한 지출이 중시되고 있는 점으로 미루어 볼 때, 여전히 중요한 지역 시장으로 자리 잡고 있습니다. 영국보험협회(Association of British Insurers)에 따르면, 영국의 반려동물 보험 계약 건수는 2023년 440만 건에서 2024년에는 460만 건에 달했으며, 이는 보험을 통한 수의학 치료 및 예방 의료 서비스 이용이 확대되고 있음을 반영하고 있습니다. 또한, 이 지역에서는 프리미엄 반려동물사료, 진단, 의약품, 웰니스 제품에 대한 꾸준한 수요가 계속해서 호재로 작용하고 있습니다. 구독형 수의학 서비스와 옴니채널 소매의 확대 역시 유럽 주요 시장에서 반려동물을 위한 헬스케어에 대한 지속적인 지출을 더욱 촉진하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the pet care market size was valued at USD 243.50 billion in 2025 and is projected to grow from USD 260.10 billion in 2026 to USD 361.20 billion by 2031, registering a CAGR of 6.80% from 2026 to 2031.

This report is Segmented by Product Type (Pet Food, Pet Healthcare, Pet Grooming Products, Pet Accessories, and Pet Services), by Animal Type (Dogs, Cats, and Other Animals), by Distribution Channel (Offline Retail and Online Retail), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Pet Care Market Trends and Insights

Pet Humanization and Premiumization

Pet humanization and premiumization are driving long-term growth in the pet care market, as consumers increasingly view companion animals as family members and allocate more spending toward wellness-focused products and services. According to the American Pet Products Association, dog ownership reached 53% of United States households in 2025, up from 51% the previous year, highlighting the growing demand for premium nutrition, preventive healthcare, diagnostics, grooming, and enrichment-related pet care products. Additionally, the rising emotional attachment to pets is fostering increased expenditure on chronic care management, specialty treatments, and age-related healthcare services, contributing to sustained value growth in the pet care market.

Preventive Care and Insurance Adoption

Preventive care and the adoption of pet insurance are driving growth in the pet care market, as insurance coverage promotes increased spending on diagnostics, treatments, and routine veterinary services. According to the North American Pet Health Insurance Association (NAPHIA), the total written premium in North America reached USD 5.2 billion in 2024, up from USD 4.2 billion in 2023. The rising adoption of pet insurance is enhancing access to preventive healthcare, chronic disease management, and advanced veterinary procedures. It also motivates pet owners to seek higher-value clinical care and wellness services for their companion animals.

Raw Material and Packaging Cost Volatility

Volatility in raw material and packaging costs continues to be a significant restraint on the pet care market. Fluctuations in the prices of protein ingredients, packaging materials, freight, and energy directly impact manufacturing expenses and consumer pricing. According to Zoetis Inc.'s 2025 Annual Report, macroeconomic pressures and reduced household spending have influenced veterinary visit trends and purchasing behavior across companion animal healthcare categories. Increasing cost sensitivity among pet owners is prompting companies to enhance supply chain management, optimize sourcing strategies, and prioritize operational efficiency to sustain margins within the pet care industry.

Other drivers and restraints analyzed in the detailed report include:

- Veterinary Clinic Corporatization and Care-Plan Cross-Sell

- Novel Proteins and Functional Ingredient Approvals

- Veterinary Labor Shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The pet care market share for the pet food segment accounted for the largest 52.6% in 2025. Pet food remains the dominant category due to its recurring purchase frequency, wide product availability, and increasing consumer preference for premium and functional nutrition products. Demand is shifting toward fresh, refrigerated, grain-free, and veterinary-recommended formulations that address digestive health, weight management, and age-specific nutrition needs. Manufacturers are expanding premium offerings by incorporating sustainable ingredients and personalized feeding solutions. Strong retail penetration across supermarkets, pet specialty stores, veterinary clinics, and e-commerce platforms continues to support stable consumer spending in both developed and emerging companion animal care markets globally.

The pet care market size for the pet services segment is projected to grow at the fastest 10.0% CAGR from 2026 to 2031. This growth is driven by increasing expenditure on veterinary care, grooming, daycare, boarding, insurance, and preventive healthcare services. Consumers increasingly consider pet wellness and routine medical care as essential household expenses rather than discretionary spending. Subscription-based veterinary plans, telehealth consultations, diagnostics, and behavioral support services are also expanding rapidly in urban markets. Additionally, the aging pet population and rising awareness of preventive treatments continue to drive long-term demand for recurring clinical and wellness-focused pet service offerings within the companion animal healthcare ecosystem.

Geography Analysis

The pet care market share for North America held the largest 33.5% in 2025. This leading position is attributed to high pet ownership rates, advanced veterinary infrastructure, widespread adoption of preventive healthcare services, and substantial consumer spending on premium pet nutrition and wellness products. The region benefits from the expansion of veterinary clinic networks, growing demand for diagnostics and chronic disease management, and increased use of subscription-based pet healthcare services. Additionally, the rising adoption of companion animal insurance and a stronger emphasis on preventive care are driving spending across veterinary services, pharmaceuticals, nutrition, and wellness categories in the United States and Canada.

The Asia-Pacific market size is projected to grow at the fastest CAGR at 9.6% from 2026 to 2031. Urbanization, smaller household sizes, delayed parenthood, and rising disposable incomes are contributing to increased pet ownership in countries such as China, India, Japan, South Korea, and across Southeast Asia. Consumers are allocating more resources to premium nutrition, preventive healthcare, grooming, diagnostics, and wellness services for their pets. Additionally, digital commerce and app-based pet care platforms are enhancing access to products and veterinary consultation services in metropolitan areas. Both domestic and international companies are investing in premium product portfolios and omnichannel distribution strategies to strengthen their presence in the rapidly developing regional pet care markets.

Europe remains a key regional market because of established pet ownership trends, advanced veterinary services, and strong emphasis on preventive care and wellness spending. According to the Association of British Insurers, pet insurance coverage in the United Kingdom reached 4.6 million policies in 2024, compared with 4.4 million policies in 2023, reflecting rising adoption of insurance-backed veterinary care and preventive healthcare services. The region also continues benefiting from strong demand for premium pet nutrition, diagnostics, pharmaceuticals, and wellness products. Subscription-based veterinary services and omnichannel retail expansion are further supporting recurring companion animal healthcare spending across major European markets.

- Mars, Incorporated

- Nestle Purina PetCare Company (Nestle S.A.)

- Hill's Pet Nutrition, Inc. (Colgate-Palmolive Company)

- The J. M. Smucker Company

- Blue Buffalo Company, Ltd. (General Mills, Inc.)

- Spectrum Brands Holdings, Inc.

- Central Garden & Pet Company

- Freshpet, Inc.

- Unicharm Corporation

- Zoetis Inc.

- Elanco Animal Health Incorporated

- Virbac S.A.

- Dechra Pharmaceuticals PLC

- IDEXX Laboratories, Inc.

- PetSmart LLC (BC partners)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Pet humanization and premiumization

- 4.2.2 Rising millennial and Generation Z pet ownership

- 4.2.3 Online retail and autoship expansion

- 4.2.4 Preventive care and insurance adoption

- 4.2.5 Veterinary clinic corporatization and care-plan cross-sell

- 4.2.6 Novel proteins and functional ingredient approvals

- 4.3 Market Restraints

- 4.3.1 Raw material and packaging cost volatility

- 4.3.2 Labeling and claims compliance tightening

- 4.3.3 Veterinary labor shortages

- 4.3.4 Cold-chain and last-mile economics for fresh diets

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Pet Food

- 5.1.2 Pet Healthcare

- 5.1.3 Pet Grooming Products

- 5.1.4 Pet Accessories

- 5.1.5 Pet Services

- 5.2 By Animal Type

- 5.2.1 Dogs

- 5.2.2 Cats

- 5.2.3 Others

- 5.3 By Distribution Channel

- 5.3.1 Offline Retail

- 5.3.1.1 Supermarkets and Hypermarkets

- 5.3.1.2 Pet Specialty Stores

- 5.3.1.3 Veterinary Clinics

- 5.3.2 Online Retail

- 5.3.1 Offline Retail

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Chile

- 5.4.2.4 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 Australia

- 5.4.4.5 South Korea

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Turkey

- 5.4.5.4 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Mars, Incorporated

- 6.4.2 Nestle Purina PetCare Company (Nestle S.A.)

- 6.4.3 Hill's Pet Nutrition, Inc. (Colgate-Palmolive Company)

- 6.4.4 The J. M. Smucker Company

- 6.4.5 Blue Buffalo Company, Ltd. (General Mills, Inc.)

- 6.4.6 Spectrum Brands Holdings, Inc.

- 6.4.7 Central Garden & Pet Company

- 6.4.8 Freshpet, Inc.

- 6.4.9 Unicharm Corporation

- 6.4.10 Zoetis Inc.

- 6.4.11 Elanco Animal Health Incorporated

- 6.4.12 Virbac S.A.

- 6.4.13 Dechra Pharmaceuticals PLC

- 6.4.14 IDEXX Laboratories, Inc.

- 6.4.15 PetSmart LLC (BC partners)