|

시장보고서

상품코드

2073244

유럽의 폐기물 유래 재생 가스 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Renewable Gas From Waste - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

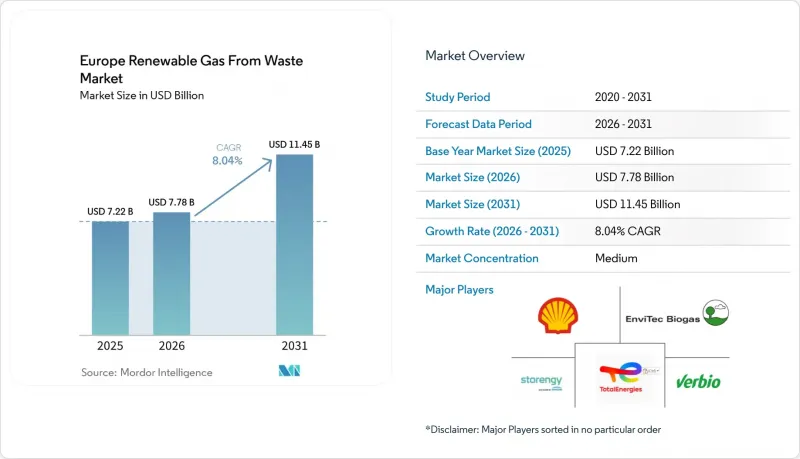

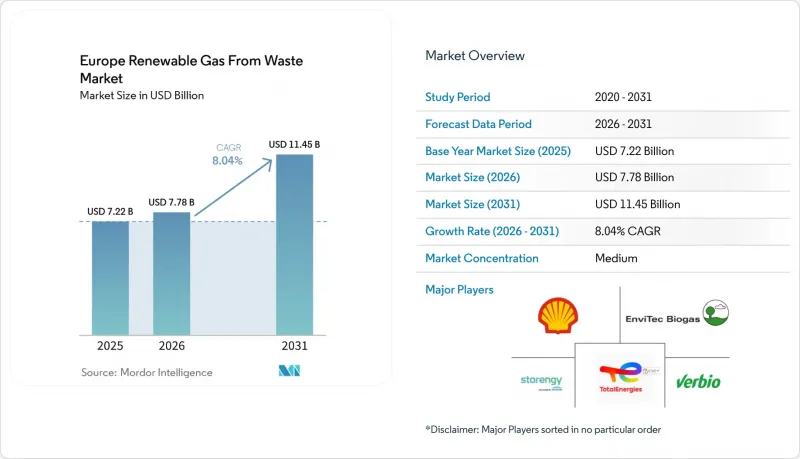

Mordor Intelligence에 의하면, 유럽의 폐기물 유래 재생 가스 시장 규모는 2025년에 72억 2,000만 달러로 평가되었습니다. 2026년 77억 8,000만 달러에서 2031년까지 114억 5,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 8.04%를 나타낼 전망입니다.

본 보고서는 원료(식품 폐기물, 가축 분뇨 등), 기술(가스화, 열분해 등), 가스 유형(바이오가스 등), 용도(발전, 계통 연계 등), 구성 요소(가스 회수, 발전 설비 등) 및 지역(독일 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

유럽의 폐기물 유래 재생 가스 시장 동향 및 인사이트

REPowerEU의 법적 구속력이 있는 바이오메탄 목표가 폐기물 유래 가스에 대한 투자를 주도하고 있습니다.

REPowerEU 계획에서는 2030년까지 35 bcm의 바이오메탄 생산 목표가 설정됨에 따라, 유럽 내 재생 가스 투자에 대한 정책적 확실성이 크게 높아졌습니다. 이 목표는 기존의 정책 전망을 크게 상회하는 것으로, 유럽의 폐기물 유래 재생 가스 시장에 더욱 대규모적이고 지속적인 수요 전망을 제시하고 있습니다. 관련 투자 수요는 370억 유로(435억 달러)로 추산되며, 이는 공공 정책이 단계적인 시범 사업 주도의 확대가 아닌, 인프라 차원의 확장을 상정하고 있음을 보여줍니다. 유럽 바이오가스 협회는 2026년 4월, 가축 분뇨, 농업 잔여물, 산업 폐수가 합쳐서 유럽의 기술적으로 달성 가능한 바이오메탄 잠재량의 81%를 차지한다고 보고했으며, 이는 프로젝트의 경제성 측면에서 폐기물 유래 원료에 대한 접근이 얼마나 중요한지를 여실히 보여주고 있습니다. 이에 따라 투자자들이 투자 기회를 선정하는 방식도 변화하게 됩니다. 왜냐하면 폐기물 흐름에 대한 확실한 접근권을 가진 개발 사업자는 여전히 일반 시장에서 바이오매스를 조달하는 사업자보다 더 신속하게 사업을 추진할 수 있기 때문입니다. 또한, 2030년 목표를 자금 지원 및 인허가 지원으로 구체화하는 각국의 정책에 따라, 향후 몇 년 동안 유럽의 폐기물 유래 재생 가스 시장 내 프로젝트 결정이 앞당겨질 가능성이 높다는 것을 의미합니다.

유럽연합(EU)의 음식물 쓰레기 매립 금지 조치가 혐기성 소화용 원료 공급을 확대

유럽연합(EU)의 “폐기물 기본 지침”이에 따라 2024년 1월 1일부터 회원국 전역에서 바이오 폐기물의 분리 수거가 의무화되었으며, 이를 통해 혐기성 소화 프로젝트의 공식적인 공급 기반이 확대되었습니다. 이는 유럽의 폐기물 유래 재생 가스 시장에 있어 중요한 의미를 지닙니다. 왜냐하면 원료 확보가 작물의 생산량이나 농산물 가격의 계절적 변동에 덜 영향을 받기 때문입니다. 또한, ‘바이오메탄 실행 계획’따라서, 바이오 폐기물의 매립을 피하는 것이 두 가지 이점으로 이어진다고 평가되고 있습니다. 즉, 매립 처분을 피한 1톤당 메탄 및 CO2 환산 배출량을 줄이면서, 동시에 이용 가능한 가스를 생산할 수 있는 것입니다. 유럽 바이오가스 협회는 독일, 프랑스, 이탈리아, 폴란드, 영국을 활용 가능한 바이오메탄 잠재력이 집중된 주요 지역으로 지목하고 있으며, 이들 국가에서의 수집 품질이 향후 공급에 지대한 영향을 미칠 것으로 보입니다. EU는 2030년까지 도시 쓰레기의 매립 처리율을 10% 이하로 낮추겠다는 목표를 향해, 매립 처리에 대한 의존도가 계속해서 낮아질 것으로 여전히 전망하고 있기 때문에 매립 처리에 관한 규제는 더욱 강화되고 있습니다. 규제 준수가 더욱 엄격해짐에 따라, 유럽의 폐기물 유래 재생 가스 시장은 분리 수거된 유기성 폐기물의 보다 안정적이고 규제가 잘 갖춰진 공급 흐름으로부터 혜택을 받게 될 것입니다.

도매 천연가스에 비해 여전히 지속되고 있는 생산 비용의 불리함

유럽에서 혐기성 소화 방식을 통한 바이오메탄 생산 비용은 여전히 1MWh당 50-175유로(1MWh당 58.8-205.9달러) 수준이며, 예측 기간의 대부분 동안 도매 천연가스 가격을 상회하는 상태를 유지하고 있습니다. 옥스퍼드 에너지 연구소는 2026년 1월, 2010년대에 비해 생산 비용이 유의미하게 감소했다는 증거는 여전히 제한적이며, 그로 인해 많은 프로젝트에서 여전히 보조금에 의존하고 있다고 밝혔습니다. 이러한 제약은 태양광이나 풍력 발전의 경우보다 해결하기가 더 어렵습니다. 왜냐하면 원료 운송 비용, 생물학적 전환의 한계, 그리고 송전망에 전력을 공급하는 데 드는 비용은 제조된 하드웨어만큼 빠르게 감소하지 않기 때문입니다. 원산지 보증(GO)이나 고정가격 임베디드 제도(FIT)와 같은 지원책은 이러한 격차를 줄이는 데 도움이 되지만, 그 가치는 국가마다 여전히 크게 달라 상업적 조건에 편차가 발생하고 있습니다. 가스 가격 하락은 특히 지원이 더욱 선별적으로 이루어지고 있는 국가들에서 보조금에 의존하지 않는 프로젝트의 실현을 더욱 어렵게 만들 것입니다. 그 결과, 유럽의 폐기물 유래 재생 가스 시장은 2031년까지 보조금 없이 대규모로 확대될 수 있는 명확한 방향을 아직 찾지 못하고 있습니다.

부문별 분석

2025년, 유럽의 폐기물 유래 재생 가스 시장에서 도시 고형 폐기물은 34.8%를 차지하며, 해당 지역에서 가장 큰 원료 그룹이 되었습니다. 이러한 1위 순위는 독일, 프랑스, 네덜란드, 영국에서 수집, 선별, 처리 시스템의 성숙도를 반영하고 있습니다. 이처럼 확립된 도시 폐기물 흐름은 보다 제한적인 농업 및 산업 유래 원료 공급원에 비해 프로젝트 개발자에게 더 안정적이고 확실한 공급 기반을 제공합니다. 농업 잔여물 및 가축 분뇨는 여전히 두 번째로 큰 원료 부문이며, RED III(재생에너지 지침 III)에 따라 운송용 연료 용도에서 이중 산입 대상이 되기 때문에 분뇨는 계속해서 규제상 우위를 누리고 있습니다. 산업 유기 폐기물 및 하수 슬러지는 특히 하수 인프라가 이미 소화 및 가스 회수 프로젝트의 자본 부담을 경감시키고 있는 지역에서 중요한 중견 부문으로 자리매김하고 있습니다.

유럽의 폐기물 유래 재생 가스 시장에서 식품 폐기물은 2026년부터 2031년까지 연평균 성장률(CAGR) 9.9%라는 가장 빠른 성장세를 보일 것으로 전망됩니다. 이러한 성장 추세는 EU의 생물성 폐기물 분리 수거 의무와 밀접한 관련이 있으며, 이 조치로 인해 자원화할 수 있는 분리 수거된 식품 폐기물의 양이 꾸준히 증가하고 있습니다. 또한, 이러한 정책 지원은 도시 폐기물이나 일반 폐기물을 원료로 하는 가스 시설을 건설하는 개발자들에게 원료 공급에 대한 장기적인 전망을 개선하는 데에도 기여합니다. 매립 폐기물은 여전히 중요한 위치를 차지하고 있으며, 특히 구형 매립지의 경우 매립 및 배출 규제가 강화됨에 따라 메탄 회수가 환경 규제 준수 및 에너지 회수라는 두 가지 목표 달성에 기여하고 있습니다. 따라서 원료 구성은 규제 대상인 유기물의 흐름을 관리할 수 있는 폐기물 처리 사업자로 전환되고 있으며, 이는 유럽의 폐기물 유래 재생 가스 시장 전체에서 이들의 입지를 강화하고 있습니다.

2025년, 혐기성 소화는 유럽의 폐기물 유래 재생 가스 시장 점유율의 45.1%를 차지하며, 해당 지역 전체에서 주요 기술 플랫폼으로서의 위상을 유지했습니다. 이러한 지위는 오랜 운영 실적, 확립된 규제 체계, 그리고 도시, 농업, 산업에서 유래한 유기 원료와의 폭넓은 호환성을 바탕으로 합니다. 또한, 이 기술은 소화 잔여물을 생산한다는 장점도 있어, 바이오 비료에 대한 수요가 있을 경우 플랜트의 경제성을 뒷받침할 수 있습니다. 매립가스 회수는 여전히 두 번째로 중요한 경로이며, 그린필드에 혐기성 소화 시설을 건설할 필요 없이 기존 매립 시설을 재생 가스 생산 거점으로 전환할 수 있다는 상업적 실현 가능성에 기반을 두고 있습니다. 이 모델은 유럽의 여러 시장에서 매립지에 직접 설치된 컨테이너형 업그레이딩 유닛을 통해 그 효과가 입증되었습니다. 가스화 및 열분해는 상용화 과정에서 아직 초기 단계에 있지만, 건조된 잔류 폐기물 흐름이 소화 처리에 적합하지 않은 지역에서는 여전히 주목을 받고 있습니다.

바이오가스 정제 시스템은 2031년까지 연평균 성장률(CAGR) 9.3%로 확대될 것으로 예상되며, 유럽의 폐기물 유래 재생 가스 시장에서 가장 빠르게 성장하는 기술 부문이 될 전망입니다. 주요 촉진요인은 특히 독일에서 보조금 종료 후 시설들이 새로운 수익원을 모색하는 과정에서 구형 바이오가스 플랜트를 바이오메탄 대응 시설로 전환하는 움직임입니다. 이 전환 경로는 발전 프로세스가 이미 구축되어 있고, 많은 시설이 이미 송전망에 연결되어 있기 때문에 신규 개발(그린필드 개발)보다 자본 효율성이 뛰어납니다. 또한, 단순히 전력을 생산하는 것에서 벗어나 부가가치가 더 높은 가스 주입이나 운송용 연료로의 활용으로 전환하는 보다 광범위한 추세와도 부합합니다. 유럽 전역의 폐기물 유래 재생 가스 업계에서는 이러한 추세에 따라 막 시스템, 스크러빙 장치, 압축 패키지 및 개조 엔지니어링 서비스에 대한 수요가 증가하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the europe renewable gas from waste market size was valued at USD 7.22 billion in 2025 and is estimated to grow from USD 7.78 billion in 2026 to reach USD 11.45 billion by 2031, at a CAGR of 8.04% during the forecast period (2026-2031).

This report is Segmented by Feedstock (Food Waste, Animal Manure, and More), by Technology (Gasification, Pyrolysis, and More), by Gas Type (Biogas, and More), by Application (Electricity Generation, Grid Injection, and More), by Component (Gas Collection, Power Generation Equipment, and More), and by Geography (Germany, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe Renewable Gas From Waste Market Trends and Insights

REPowerEU Binding Biomethane Target Driving Waste-to-Gas Investment

The REPowerEU plan set a target of 35 bcm of biomethane production by 2030, sharply raising policy certainty for renewable gas investment in Europe. That target is materially higher than earlier policy expectations, so it has given the Europe renewable gas from waste market a larger and more durable demand horizon. The related investment need was estimated at EUR 37 billion (USD 43.5 billion), indicating that public policy expects infrastructure-scale deployment rather than a gradual, pilot-led expansion. The European Biogas Association reported in April 2026 that animal manure, agricultural residues, and industrial wastewater together account for 81% of Europe's technically achievable biomethane potential, underscoring the importance of waste-linked feedstock access to project economics. This changes how investors screen opportunities, because developers with reliable access to waste streams can move faster than players still dependent on open-market biomass procurement. It also means national schemes that translate the 2030 target into funding and permitting support are likely to pull forward project decisions in the Europe renewable gas from waste market over the next several years.

European Union Biowaste Landfill Ban Expanding Anaerobic Digestion Feedstock Supply

The European Union Waste Framework Directive required separate biowaste collection across member states from January 1, 2024, which expanded the formal supply base for anaerobic digestion projects. This matters for the Europe renewable gas from waste market because feedstock access becomes less exposed to seasonal swings in crop output and agricultural commodity pricing. The Biomethane Action Plan also linked biowaste diversion to dual benefits: each tonne diverted from landfill can reduce methane and CO2-equivalent emissions while producing usable gas. The European Biogas Association identified Germany, France, Italy, Poland, and the United Kingdom as the main concentration of mobilizable biomethane potential, so collection quality in those countries will have an outsized effect on future supply. The landfill framework adds further pressure because the EU still expects landfill dependence to decline toward the 2030 target of no more than 10% of municipal waste. As compliance tightens, the Europe renewable gas from waste market stands to benefit from a steadier, more regulated flow of segregated organic waste.

Persistent Production Cost Disadvantage Relative to Wholesale Natural Gas

Biomethane production from anaerobic digestion in Europe still costs EUR 50 to EUR 175 per MWh (USD 58.8 to USD 205.9 per MWh), which remains above wholesale natural gas pricing for much of the forecast period. The Oxford Institute for Energy Studies stated in January 2026 that there is still limited evidence of meaningful reductions in production costs compared with the 2010s, which keeps subsidy dependence in place for many projects. This constraint is harder to solve than it was in solar or wind, because feedstock transport, biological conversion limits, and grid injection costs do not decline as quickly as manufactured hardware. Support instruments such as Guarantees of Origin and feed-in premiums help narrow the gap, but their value still varies widely across countries, creating uneven commercial conditions. Lower gas prices would further complicate the case for unsubsidized projects, especially in countries where support has become more selective. As a result, the Europe renewable gas from waste market is still not on a clear path to large-scale subsidy-free expansion by 2031.

Other drivers and restraints analyzed in the detailed report include:

- Declining Dispatchable Power Capacity Boosting Demand for Storable Renewable Gas

- German EEG Tariff Expiry Triggering Mass Biogas-to-Biomethane Conversion

- Fragmented National Permitting Frameworks Delaying Project Commissioning

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Municipal solid waste accounted for 34.8% of the Europe renewable gas from waste market in 2025, making it the largest feedstock group in the region. Its lead reflects the maturity of collection, sorting, and processing systems across Germany, France, the Netherlands, and the United Kingdom. These established municipal waste flows give project developers a more stable and visible supply base than several narrower agricultural or industrial streams. Agricultural residues and animal manure remained the next major feedstock block, and manure continues to benefit from a regulatory edge because RED III gives it double-counting status in transport fuel applications. Industrial organic waste and sewage sludge remained important middle-tier categories, especially where wastewater infrastructure already lowers the capital burden for digestion and gas recovery projects.

Food waste is projected to record the fastest growth at 9.9% CAGR from 2026 to 2031 in the Europe renewable gas from waste market. This trajectory is closely tied to the EU requirement for separate biowaste collection, which has steadily increased the volume of segregated food waste available for valorization. That policy support also improves long-term visibility into feedstocks for developers building urban and municipal waste-based gas assets. Landfill waste remains relevant, particularly at legacy sites, where methane capture serves both environmental compliance and energy recovery goals under tighter landfill and emissions rules. The feedstock mix is therefore moving toward waste-stream operators with control over regulated organic flows, which strengthens their position across the Europe renewable gas from waste market.

Anaerobic digestion held 45.1% of the Europe renewable gas from waste market share in 2025, keeping it as the leading technology platform across the region. Its position rests on a long operating history, an established regulatory framework, and broad compatibility with municipal, agricultural, and industrial organic feedstocks. The technology also benefits from digestate output, which can support plant economics where biofertilizer demand is present. Landfill gas recovery remained the second key route, supported by the commercial viability of converting existing landfill assets into renewable gas production sites without requiring greenfield anaerobic digestion development, a model demonstrated by containerized upgrading units deployed directly at landfill sites across several European markets. Gasification and pyrolysis remained earlier in the commercial cycle, but they continue to attract interest where dry residual waste streams are less suitable for digestion.

Biogas upgrading systems are projected to expand at 9.3% CAGR through 2031, making them the fastest-growing technology segment in the Europe renewable gas from waste market. The main driver is the conversion of older biogas plants into biomethane-capable assets, especially in Germany, as post-subsidy facilities seek new revenue pathways. This conversion route is more capital-efficient than greenfield development because the digestion process is already in place, and many sites already have grid access. It also fits the broader shift from electricity-only generation toward higher-value gas injection and transport fuel use. Across Europe, in the renewable gas from waste industry, that trend is improving demand for membrane systems, scrubbing units, compression packages, and retrofit engineering services.

Complete Report Scope:

- By Feedstock

- Municipal Solid Waste (MSW)

- Agricultural Residues

- Animal Manure

- Industrial Organic Waste

- Sewage Sludge

- Food Waste

- Others

- By Technology

- Anaerobic Digestion

- Landfill Gas Recovery

- Gasification

- Pyrolysis

- Biogas Upgrading Systems

- Others

- By Gas Type

- Biogas

- Biomethane / Renewable Natural Gas (RNG)

- Syngas

- By Application

- Electricity Generation

- Combined Heat & Power (CHP)

- Grid Injection

- Transportation Fuel

- Industrial Heating

- Residential & Commercial Heating

- Others

- By Component

- Gas Collection Systems

- Digesters & Fermentation Systems

- Gas Processing & Upgrading Units

- Compressors & Storage Systems

- Power Generation Equipment

- Monitoring & Control Systems

- Others

- By Geography

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Benelux (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

List of Companies Covered in this Report:

- Shell Plc

- EnvITec Biogas AG

- Verbio SE

- Storengy SAS

- TotalEnergies SE

- Waga Energy SA

- SUEZ SA

- Veolia Environnement S.A.

- Attero B.V.

- BALANCE Erneuerbare Energien GmbH

- Biogen (UK) Limited

- BTS Biogas Srl

- Gasum Oyj

- PlanET Biogas Group GmbH

- Enagas, S.A.

- Naturgy Energy Group, S.A.

- Archaea Energy

- Andion CH4 Holding BV

- Future Biogas Ltd

- SARIA SE & Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 REPowerEU Binding Biomethane Target Driving Waste-to-Gas Investment

- 4.2.2 European Union Biowaste Landfill Ban Expanding Anaerobic Digestion Feedstock Supply

- 4.2.3 Declining Dispatchable Power Capacity Boosting Demand for Storable Renewable Gas

- 4.2.4 German EEG Tariff Expiry Triggering Mass Biogas-to-Biomethane Conversion

- 4.2.5 RED III Double-Counting Provisions Enhancing Commercial Viability in Transport

- 4.2.6 Rising ETS Carbon Prices Accelerating Industrial Fossil Gas Substitution

- 4.3 Market Restraints

- 4.3.1 Persistent Production Cost Disadvantage Relative to Wholesale Natural Gas

- 4.3.2 Fragmented National Permitting Frameworks Delaying Project Commissioning

- 4.3.3 Incompatible Guarantee of Origin Registries Obstructing Cross-Border Trade

- 4.3.4 Organic Waste Feedstock Competition Constraining Biomass Availability

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Impact of Artificial Intelligence-Powered Waste Collection on Service Providers Revenue Growth

- 4.9 Consumer Behavior Shifts Toward Zero-Waste Lifestyles Influencing Service Demand

- 4.10 Impact of Geopolitical Events on the Market

5 Market Size & Growth Forecasts

- 5.1 By Feedstock

- 5.1.1 Municipal Solid Waste (MSW)

- 5.1.2 Agricultural Residues

- 5.1.3 Animal Manure

- 5.1.4 Industrial Organic Waste

- 5.1.5 Sewage Sludge

- 5.1.6 Food Waste

- 5.1.7 Others

- 5.2 By Technology

- 5.2.1 Anaerobic Digestion

- 5.2.2 Landfill Gas Recovery

- 5.2.3 Gasification

- 5.2.4 Pyrolysis

- 5.2.5 Biogas Upgrading Systems

- 5.2.6 Others

- 5.3 By Gas Type

- 5.3.1 Biogas

- 5.3.2 Biomethane / Renewable Natural Gas (RNG)

- 5.3.3 Syngas

- 5.4 By Application

- 5.4.1 Electricity Generation

- 5.4.2 Combined Heat & Power (CHP)

- 5.4.3 Grid Injection

- 5.4.4 Transportation Fuel

- 5.4.5 Industrial Heating

- 5.4.6 Residential & Commercial Heating

- 5.4.7 Others

- 5.5 By Component

- 5.5.1 Gas Collection Systems

- 5.5.2 Digesters & Fermentation Systems

- 5.5.3 Gas Processing & Upgrading Units

- 5.5.4 Compressors & Storage Systems

- 5.5.5 Power Generation Equipment

- 5.5.6 Monitoring & Control Systems

- 5.5.7 Others

- 5.6 By Geography

- 5.6.1 Germany

- 5.6.2 United Kingdom

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Russia

- 5.6.7 Benelux (Belgium, Netherlands, and Luxembourg)

- 5.6.8 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.6.9 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Shell Plc

- 6.4.2 EnviTec Biogas AG

- 6.4.3 Verbio SE

- 6.4.4 Storengy SAS

- 6.4.5 TotalEnergies SE

- 6.4.6 Waga Energy SA

- 6.4.7 SUEZ SA

- 6.4.8 Veolia Environnement S.A.

- 6.4.9 Attero B.V.

- 6.4.10 BALANCE Erneuerbare Energien GmbH

- 6.4.11 Biogen (UK) Limited

- 6.4.12 BTS Biogas Srl

- 6.4.13 Gasum Oyj

- 6.4.14 PlanET Biogas Group GmbH

- 6.4.15 Enagas, S.A.

- 6.4.16 Naturgy Energy Group, S.A.

- 6.4.17 Archaea Energy

- 6.4.18 Andion CH4 Holding BV

- 6.4.19 Future Biogas Ltd

- 6.4.20 SARIA SE & Co. KG

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment