|

시장보고서

상품코드

2073251

중국의 폐기물 유래 재생 가스 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)China Renewable Gas From Waste - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

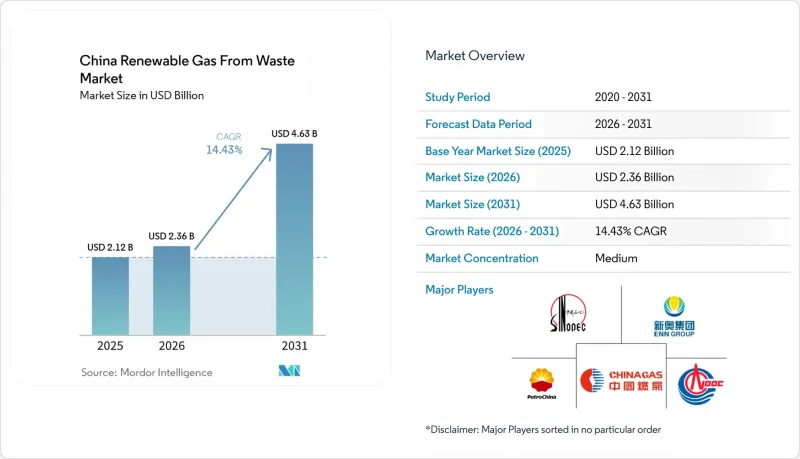

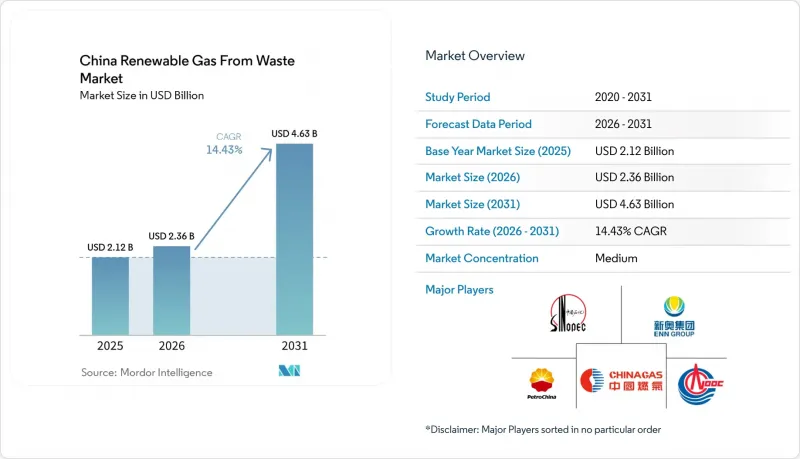

Mordor Intelligence에 의하면, 중국의 폐기물 유래 재생 가스 시장 규모는 2025년 21억 2,000만 달러로 평가되었습니다. 2026년 23억 6,000만 달러에서 2031년까지 46억 3,000만 달러로 확대되며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 14.43%를 나타낼 전망입니다.

본 보고서는 원료별(도시 고형 폐기물, 농업 잔여물, 식품 폐기물 등), 기술별(가스화, 열분해 등), 가스 유형별(바이오가스, 합성가스 등), 용도별(발전, 계통 연계 등), 구성 요소별(가스 회수, 소화조·발효 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

중국의 폐기물 유래 재생 가스 시장 동향 및 인사이트

'이산화탄소 배출 정점'라고 '탄소 중립'의 목표가 바이오 천연가스와 관련된 정책 요건을 가속화하고 있습니다.

중국의 탄소 배출 정점 및 탄소 중립 관련 의제는 현재 단순한 광범위한 정책 신호에 그치지 않고, 규정, 측정 시스템 및 프로젝트 차원의 준수 요건을 통해 중국의 폐기물 유래 재생 가스 시장을 형성하고 있습니다. 국가발전개혁위원회(NDRC)가 수립한 2024년 탄소 배출 정점 및 탄소 중립 기준에 관한 행동 계획은 재생 가스 프로젝트가 기업 차원에서 배출량 성과를 문서화하기 위해 필요한 측정 및 검증 기반을 강화했습니다. 이러한 변화가 중요한 이유는 개발 사업자가 전력 회사나 산업계로부터 프로젝트 인수 확약을 얻기 전에, 더 높은 데이터 품질과 자금 조달에 유리한 보고 체계를 갖추어야 하기 때문입니다. 또한, 검증된 모니터링 시스템이나 공식적인 보고 능력을 갖추지 못한 중소기업의 경우, 진입 장벽이 높아지게 됩니다. 실제로 중국의 폐기물 유래 재생 가스 시장은 규모 확대를 실현하기 위해서는 법적 승인, 탄소 회계, 인프라 접근성이 유기적으로 연계되어 기능해야 하는 분야로 점차 발전하고 있습니다.

바이오메탄 통합을 강화하는 에너지법

『중화인민공화국 에너지법』이 2025년 1월 1일에 시행됨에 따라, 바이오 천연가스는 국가 에너지 시스템 내에서 보다 명확한 법적 지위를 확보하게 되었습니다. 이 법은 지역의 실정에 맞는 바이오매스 에너지 이용을 장려하는 한편, 에너지 시스템에 대해 재생에너지의 수용 및 배분 능력 향상을 요구하고 있습니다. 이번 법 개정을 통해, 도시가스 공급 사업자가 그동안 바이오메탄 송배전망에 대한 접근을 거부하기 위해 이용해 온 모호한 부분이 해소되었습니다. 프로젝트 개발자들은 현재, 2025년 이전의 중국의 폐기물 유래 재생 가스 시장보다 더 견고한 제도적 뒷받침을 바탕으로 장기 공급 계약을 협상할 수 있게 되었습니다. 그 결과, 도시가스 네트워크가 구축된 주에서는 가스망 공급 프로젝트의 상업적 전망을 더 쉽게 예측할 수 있게 되었습니다.

전국적인 바이오메탄 생산 보조금 체계의 부재가 사업의 실현 가능성을 저해하고 있습니다.

중국의 폐기물 유래 재생 가스 시장에는 여전히 전국적인 단위당 생산 보조금이 부족하여, 많은 프로젝트가 지역별 가스 가격, 제품별 판매, 그리고 탄소 수익에 의존할 수밖에 없는 상황입니다. 이는 유통망이 취약하여 개발업체가 도시 지역의 프리미엄 판매 경로에 의존할 수 없는 지역에서 특히 큰 문제가 됩니다. 환경보호부(MEE)가 2025년 12월에 발표한, 양돈장의 분뇨에서 바이오가스를 회수하고 농업 폐기물을 집중 처리하는 것에 관한 새로운 CCER(중국 탄소 배출 감축 단위) 조사 기법은 수익 구조의 일부를 보완하는 데 도움이 될 것입니다. 그렇다고는 해도, 이것이 직접적인 생산 지원 메커니즘을 대체하는 것은 아닙니다. 전국적인 보조금이 없다면, 견고한 재무 기반이 여전히 큰 경쟁 우위가 되어, 중소 개발업체보다 국영 기업이나 대형 환경 기업이 유리해질 것입니다. 그 결과, 자원 기반이 풍부한 경우에도 프로젝트의 전개는 여전히 선별적인 수준에 그치고 있습니다.

부문별 분석

2025년, 중국의 폐기물 유래 재생 가스 시장에서 농업 잔여물은 시장 점유율의 31.50%를 차지하며, 해당 부문에서 가장 큰 원료 공급원이 되었습니다. 이러한 우위는 작물 생산 규모가 크고, 주요 농업부 전역에 걸쳐 볏짚 및 관련 잔여물이 풍부하게 공급되고 있는 상황을 반영하고 있습니다. 실무적으로 볼 때, 이러한 원료 공급원은 수집 시스템이 이미 구축된 현 단위의 공장에서 필요한 처리량을 확보하고 있습니다. 또한, 중국의 폐기물 유래 재생 가스 시장은 농업 잔여물이 더 광범위한 농촌 지역의 폐기물 처리 및 자원 활용 목표와 부합한다는 점에서도 혜택을 보고 있습니다.

식품 폐기물은 2031년까지 연평균 14.32%의 성장률을 보일 것으로 예상되며, 시장 내에서 가장 빠르게 성장하는 원료 부문이 될 전망입니다. 가축 분뇨, 산업계 유기 폐기물, 하수 슬러지, 매립 폐기물은 중국의 폐기물 유래 재생 가스 시장에서 각각 서로 다른 규제 준수 및 처리 요구 사항에 대응하고 있습니다. 가축 분뇨는 특히 중요하며, 많은 지역에서 가축 폐기물 처리가 더 이상 선택 사항이 아니게 된 데다, 농업농촌가 전국적으로 80% 이상의 종합 이용률을 추진하고 있기 때문입니다. 이러한 성장은 도시 지역에서의 분리수거 의무화, 보다 깨끗한 원료공급, 그리고 유기성 폐기물 흐름에서 집중형 바이오가스 처리의 수익성을 높이는 새로운 CCER(탄소 크레딧) 조사 기법을 반영한 것입니다.

2025년, 중국의 폐기물 유래 재생 가스 시장 규모 중 혐기성 소화 방식이 43.60%를 차지하며, 농업 폐기물 및 도시 폐기물 프로젝트 전반에 걸쳐 주요 기술 플랫폼으로 자리매김했습니다. 이러한 우위는 오랜 기간의 운영 실적, 기존 플랜트에 대한 숙련도, 그리고 가축 분뇨 및 혼합 유기 원료를 중심으로 구축된 광범위한 도입 실적에서 비롯됩니다. 또한, 현재 진행 중인 프로젝트의 상당수가 어떠한 정제 공정을 거치기 전, 우선 정제되지 않은 바이오가스 생산부터 시작되고 있기 때문에 이 기술은 여전히 핵심적인 위치를 차지하고 있습니다. 이에 따라 새로운 기술이 부상하고 있는 상황에서도, 혐기성 소화는 중국의 폐기물 유래 재생 가스 시장에서 기초적인 역할을 수행하고 있습니다.

가스화 시장은 2031년까지 연평균 15.10%의 성장률이 예상되며, 예측 기간 동안 가장 빠르게 성장하는 기술 분야가 될 것입니다. 바이오가스 정제 시스템, 매립지 가스 회수, 열분해 및 모니터링 시스템은 모두 더욱 광범위하고 고도화되는 기술 스택을 뒷받침하고 있습니다. 중국 광대환경이 안후이성 샤오현에서 시행한 첫 번째 바이오매스 가스화 프로젝트는 열화학적 변환이 시범 단계를 넘어 소화 처리에 적합하지 않은 건조한 재료까지 원료 범위를 확대할 수 있음을 보여주었습니다. 이 점은 중요합니다. 왜냐하면 중국의 폐기물 산업에서 재생 가스는 도시, 농업, 산업에서 발생하는 모든 유기성 폐기물을 처리하기 위해 여러 가지 전환 과정을 거쳐야 하기 때문입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the china renewable gas from waste market size is projected to expand from USD 2.12 billion in 2025 and USD 2.36 billion in 2026 to USD 4.63 billion by 2031, registering a CAGR of 14.43% between 2026 to 2031.

This report is Segmented by Feedstock (Municipal Solid Waste, Agricultural Residues, Food Waste, and More), by Technology (Gasification, Pyrolysis, and More), by Gas Type (Biogas, Syngas, and More), by Application (Electricity Generation, Grid Injection, and More), and by Component (Gas Collection, Digesters & Fermentation, and More). The Market Forecasts are Provided in Terms of Value (USD).

China Renewable Gas From Waste Market Trends and Insights

Dual Carbon Goals Accelerating Bio-Natural Gas Policy Mandates

China's carbon peak and carbon neutrality agenda is now shaping the China renewable gas from waste market through rules, measurement systems, and project-level compliance expectations rather than broad policy signaling alone. The National Development and Reform Commission (NDRC) 2024 action plan on carbon peak and carbon neutrality standards strengthened the measurement and verification base that renewable gas projects need to document emissions outcomes at the enterprise level. That shift matters because developers now need stronger data quality and more bankable reporting before projects can secure offtake confidence from utilities and industries. It also raises entry barriers for smaller firms that lack verified monitoring systems and formal reporting capabilities. In practice, the China renewable gas from waste market is moving closer to sectors where legal recognition, carbon accounting, and access to infrastructure must work together before scale can follow.

Energy Law Strengthening Biomethane Integration

The Energy Law of the People's Republic of China took effect on January 1, 2025, and gave bio-natural gas a clearer statutory position within the national energy system. The law encourages the use of biomass energy according to local conditions and also requires the energy system to improve its ability to accept and allocate renewable energy. That legal change reduces the ambiguity that city gas distributors previously used to resist access to the biomethane grid. Project developers can now negotiate long-term supply arrangements with better institutional backing than the China renewable gas from waste market had before 2025. The result is a more predictable commercial path for grid injection projects in provinces with dense municipal gas networks.

Absence of a National Biomethane Production Subsidy Framework Undermining Viability

The China renewable gas from waste market still lacks a national per-unit production subsidy, leaving many projects dependent on local gas prices, by-product sales, and carbon revenues. This matters most in regions where distribution networks are weaker, and developers cannot rely on premium urban offtake channels. The MEE's December 2025 release of new CCER methodologies for pig farm manure biogas recovery and agricultural waste centralized processing helps part of the revenue stack. Still, it does not replace a direct production support mechanism. Without a national subsidy, stronger balance sheets remain a major competitive advantage, favoring SOEs and large environmental firms over smaller developers. As a result, project deployment remains selective even when the resource base is large.

Other drivers and restraints analyzed in the detailed report include:

- State-Owned Enterprise Entry Validating and Scaling the Biomethane Sector

- Mandatory Urban Food Waste Sorting Expanding Centralized Feedstock Supply

- High Feedstock Logistics Costs Limiting Viable Project Geographies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Agricultural residues accounted for 31.50% of the China renewable gas from waste market share in 2025, making them the largest feedstock base in the sector. Their lead reflects the scale of crop output and the wide availability of straw and related residues across major farming provinces. In practical terms, these streams provide the volume needed for county-level plants where collection systems are already in place. The China renewable gas from waste market also benefits from the fact that agricultural residues align with broader rural waste treatment and resource-use goals.

Food waste is forecast to expand at 14.32% through 2031, making it the fastest-growing feedstock category in the market. Animal manure, industrial organic waste, sewage sludge, and landfill waste serve different compliance and disposal needs within the China renewable gas from waste market. Manure is especially important because livestock waste treatment is no longer optional in many areas, and the Ministry of Agriculture and Rural Affairs has pushed for nationwide comprehensive utilization rates of 80% or more. This growth reflects mandatory urban sorting, cleaner incoming feedstock, and new CCER methodologies that improve the revenue potential of centralized biogas processing from organic waste streams.

Anaerobic digestion accounted for 43.60% of the China renewable gas from waste market size in 2025, making it the leading technology platform across agricultural and urban waste projects. Its dominance stemmed from a long operating history, familiarity with existing plants, and a broad installed base built around manure and mixed organic feedstocks. The technology also remains central because most current projects still begin with raw biogas production before any upgrading step. This gives anaerobic digestion a foundational role in the China renewable gas from waste market, even as newer pathways gain ground.

Gasification is projected to grow at 15.10% through 2031, which makes it the fastest-growing technology category in the forecast period. Biogas upgrading systems, landfill gas recovery, pyrolysis, and monitoring systems all support a broader, increasingly sophisticated technology stack. China Everbright Environment's first biomass gasification project in Xiao County, Anhui, showed that thermochemical conversion can move beyond pilot status and widen the usable feedstock base to drier materials that are less suitable for digestion. That matters because renewable gas from the waste industry in China requires multiple conversion routes to process the full range of municipal, agricultural, and industrial organic waste.

Complete Report Scope:

- By Feedstock

- Municipal Solid Waste (MSW)

- Agricultural Residues

- Animal Manure

- Industrial Organic Waste

- Sewage Sludge

- Food Waste

- Others

- By Technology

- Anaerobic Digestion

- Landfill Gas Recovery

- Gasification

- Pyrolysis

- Biogas Upgrading Systems

- Others

- By Gas Type

- Biogas

- Biomethane / Renewable Natural Gas (RNG)

- Syngas

- By Application

- Electricity Generation

- Combined Heat & Power (CHP)

- Grid Injection

- Transportation Fuel

- Industrial Heating

- Residential & Commercial Heating

- Others

- By Component

- Gas Collection Systems

- Digesters & Fermentation Systems

- Gas Processing & Upgrading Units

- Compressors & Storage Systems

- Power Generation Equipment

- Monitoring & Control Systems

- Others

List of Companies Covered in this Report:

- PetroChina Company Limited

- China Petroleum & Chemical Corporation (Sinopec Corp.)

- CNOOC Refining and Petrochemical Co., Ltd.

- China Gas Holdings Limited

- ENN Energy Holdings Limited

- Towngas China Company Limited

- China Everbright Environment Group Limited

- Beijing Enterprises Holdings Limited

- China Resources Gas Group Limited

- Shenergy Environment Technology Co., Ltd.

- China Tianying Inc.

- China Conch Venture Holdings Limited

- Shanghai SUS Environment Co., Ltd.

- Grandblue Environment Co., Ltd.

- China Energy Conservation and Environmental Protection Group (CECEP)

- Anhui Province Natural Gas Development Co., Ltd.

- China Three Gorges Corporation

- Shenzhen Gas Corporation Ltd.

- Zheneng Jinjiang Environment Holding Company Limited

- Beijing Capital Eco-Environment Protection Group Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Dual Carbon Goals Accelerating Bio-Natural Gas Policy Mandates

- 4.2.2 Energy Law Strengthening Biomethane Integration

- 4.2.3 State-Owned Enterprise Entry Validating and Scaling the Biomethane Sector

- 4.2.4 Mandatory Urban Food Waste Sorting Expanding Centralized Feedstock Supply

- 4.2.5 National Carbon Market and SOE Emission Disclosure Driving Industrial Biomethane Offtake

- 4.2.6 Agricultural Waste Management Crisis Creating Policy-Driven Feedstock Push

- 4.3 Market Restraints

- 4.3.1 Absence of a National Biomethane Production Subsidy Framework Undermining Viability

- 4.3.2 High Feedstock Logistics Costs Limiting Viable Project Geographies

- 4.3.3 Fragmented Multi-Ministry Regulatory Structure Causing Approval Delays

- 4.3.4 Mass Abandonment of Household Digesters Eroding Distributed Production Base

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Digital Feedstock Management and Process Optimization Improving Renewable Gas Plant Efficiency

- 4.9 Organic Waste Diversion and Segregation Policies Supporting Feedstock Supply Growth

- 4.10 Impact of Geopolitical Events on the Market

5 Market Size & Growth Forecasts

- 5.1 By Feedstock

- 5.1.1 Municipal Solid Waste (MSW)

- 5.1.2 Agricultural Residues

- 5.1.3 Animal Manure

- 5.1.4 Industrial Organic Waste

- 5.1.5 Sewage Sludge

- 5.1.6 Food Waste

- 5.1.7 Others

- 5.2 By Technology

- 5.2.1 Anaerobic Digestion

- 5.2.2 Landfill Gas Recovery

- 5.2.3 Gasification

- 5.2.4 Pyrolysis

- 5.2.5 Biogas Upgrading Systems

- 5.2.6 Others

- 5.3 By Gas Type

- 5.3.1 Biogas

- 5.3.2 Biomethane / Renewable Natural Gas (RNG)

- 5.3.3 Syngas

- 5.4 By Application

- 5.4.1 Electricity Generation

- 5.4.2 Combined Heat & Power (CHP)

- 5.4.3 Grid Injection

- 5.4.4 Transportation Fuel

- 5.4.5 Industrial Heating

- 5.4.6 Residential & Commercial Heating

- 5.4.7 Others

- 5.5 By Component

- 5.5.1 Gas Collection Systems

- 5.5.2 Digesters & Fermentation Systems

- 5.5.3 Gas Processing & Upgrading Units

- 5.5.4 Compressors & Storage Systems

- 5.5.5 Power Generation Equipment

- 5.5.6 Monitoring & Control Systems

- 5.5.7 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 PetroChina Company Limited

- 6.4.2 China Petroleum & Chemical Corporation (Sinopec Corp.)

- 6.4.3 CNOOC Refining and Petrochemical Co., Ltd.

- 6.4.4 China Gas Holdings Limited

- 6.4.5 ENN Energy Holdings Limited

- 6.4.6 Towngas China Company Limited

- 6.4.7 China Everbright Environment Group Limited

- 6.4.8 Beijing Enterprises Holdings Limited

- 6.4.9 China Resources Gas Group Limited

- 6.4.10 Shenergy Environment Technology Co., Ltd.

- 6.4.11 China Tianying Inc.

- 6.4.12 China Conch Venture Holdings Limited

- 6.4.13 Shanghai SUS Environment Co., Ltd.

- 6.4.14 Grandblue Environment Co., Ltd.

- 6.4.15 China Energy Conservation and Environmental Protection Group (CECEP)

- 6.4.16 Anhui Province Natural Gas Development Co., Ltd.

- 6.4.17 China Three Gorges Corporation

- 6.4.18 Shenzhen Gas Corporation Ltd.

- 6.4.19 Zheneng Jinjiang Environment Holding Company Limited

- 6.4.20 Beijing Capital Eco-Environment Protection Group Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment