|

시장보고서

상품코드

2073261

통합 GPU 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Integrated GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

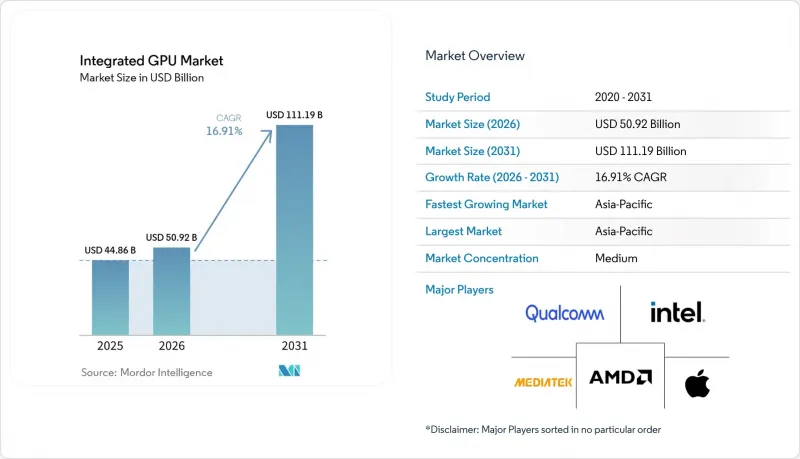

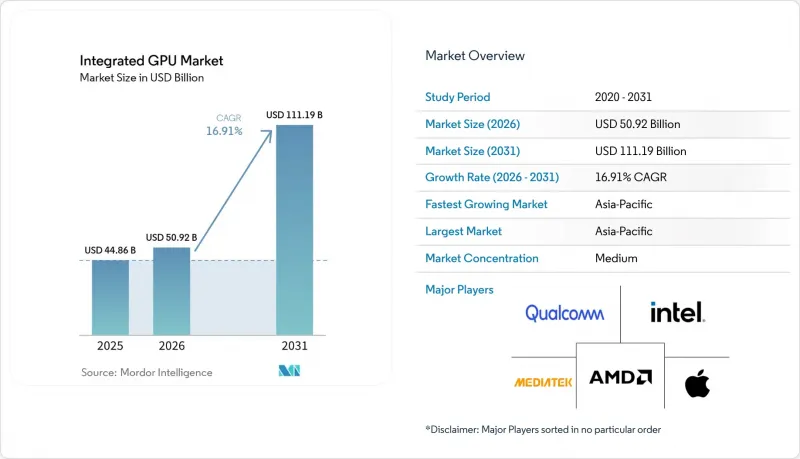

Mordor Intelligence에 의하면, 통합 GPU 시장 규모는 2025년 448억 6,000만 달러에서 2026년에는 509억 2,000만 달러로 확대되어 2031년까지 1,111억 9,000만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 16.91%로 성장할 전망입니다.

본 보고서는 디바이스(데스크톱 및 노트북용 프로세서, 모바일 SoC, 임베디드·산업용 SoC, 통합 그래픽이 탑재된 서버·데이터센터용 프로세서), 성능 수준(엔트리 레벨, 메인스트림, 퍼포먼스, 하이 퍼포먼스), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 통합 GPU 시장 동향과 인사이트

AI PC의 교체 주기와 온디바이스 AI 도입

통합 GPU 시장은 AI 기반 퍼스널 컴퓨팅으로의 광범위한 전환에 힘입어 성장하고 있습니다. 현재 주류 시스템에서는 그래픽스 블록이 이미지 보정, 로컬 모델 실행 및 미디어 처리를 지원하도록 되어 있습니다. 벤더들은 통합 GPU를 더 이상 부수적인 기능으로 취급하지 않습니다. 왜냐하면 통합 GPU는 현재 기업 및 일반 소비자 구매자들에게 중요한 공유 워크로드에서 CPU 및 NPU와 연동하여 작동하게 되었기 때문입니다. 인텔은 Core Ultra Series 3를 통해 이러한 변화를 명확히 제시했습니다. 이 시리즈는 Intel 18A 프로세서의 단일 패키지에 최대 12개의 Xe3 GPU 코어와 50 TOPS의 NPU를 통합하고 있습니다. 이러한 설계 선택을 통해 별도의 그래픽 카드를 추가하지 않고도 AI PC의 기본 그래픽 성능을 향상시켜, 통합 GPU 시장을 뒷받침하고 있습니다. 또한, 이러한 접근 방식을 통해 비교적 가벼운 AI 작업을 NPU로 오프로드하는 동시에, 통합 GPU가 비주얼 파이프라인 및 지속적인 그래픽스 처리를 계속 담당할 수 있으므로 시스템의 균형도 향상됩니다. 이에 따라 통합 GPU 시장은 기업의 교체 주기와 프리미엄 노트북의 포지셔닝 측면에서 더욱 중요한 역할을 수행하게 되었습니다.

모바일 SoC에서의 그래픽스 통합 확대

통합 GPU 시장에서 가장 많은 판매량을 차지하고 있는 분야는 모바일 SoC 분야입니다. 이 분야에서는 그래픽스 블록이 단순한 프레임 렌더링의 범위를 넘어, 보다 광범위한 연산 기능과 AI를 활용한 이미지 처리 기능으로 진화하고 있습니다. MediaTek은 “Dimensity 9500”를 통해 그 성능 범위를 확대했습니다. 이 칩은 Arm G1-Ultra GPU를 통합하고 있으며, 새로운 “GPU 동적 캐시 아키텍처”를 추가함으로써 최고 성능을 33% 향상시켰으며, 이전 세대에 비해 전력 효율을 42% 개선했습니다. 삼성 역시 2nm GAA 칩인 ‘Exynos 2600”을 통해 프리미엄 스마트폰에 대한 기대감을 높였습니다. 이 칩은 Xclipse 960 GPU와 자체 개발한 열 관리 기술을 결합하여, 이전 모델보다 뛰어난 레이 트레이싱 성능을 구현하고 있습니다. 퀄컴 역시 Snapdragon X2 Elite 제품군을 통해 PC급 모바일 반도체 분야에서 이와 같은 방향성을 강화했습니다. 이 제품군에 탑재된 Adreno X2-90 통합 GPU는 DirectX 12.2 Ultimate 및 Vulkan 1.4를 지원하며, 동등한 전력 소비 수준에서 더 높은 성능을 구현합니다. 이러한 변화는 통합 GPU 시장에 있어 중요한 의미를 지닙니다. 왜냐하면 스마트폰, 태블릿, 상시 연결형 PC 등 이미 매우 대량으로 출하되고 있는 SoC의 성능 한계를 한층 더 넓혀주기 때문입니다. 또한 메모리 처리, 캐시 설계, 그래픽스 효율이 단순한 보조 기능이 아니라 통합 GPU 시장에서 핵심적인 제품 차별화 요소로 작용하고 있음을 보여줍니다.

AAA 타이틀 및 전문가용 워크로드에서 디스크리트 GPU와의 성능 격차

통합 GPU 시장은 장시간 렌더링, 전문적인 컨텐츠 제작, 혹은 높은 설정에서 진행되는 고사양 게임 플레이가 필요한 워크로드에서 여전히 뚜렷한 한계에 직면해 있습니다. 아키텍처상의 발전이 있더라도, 통합형 설계는 시스템 메모리 및 열 설계상의 제약을 계속 공유하는 반면, 디스크리트 GPU는 전용 메모리 풀과 독립적인 전력 예산을 확보하고 있습니다. 인텔의 현재 로드맵은 통합 그래픽스가 얼마나 발전했는지를 보여주고 있지만, 이 회사의 최신 클라이언트 플랫폼조차도 강력한 통합 그래픽스를 전문가용 독립형 하드웨어를 완전히 대체하는 수단이 아니라, 보다 광범위한 패키지 설계의 일부로 자리매김하고 있습니다. 따라서 통합 GPU 시장은 크리에이터용 워크스테이션, 하이엔드 데스크톱, 그리고 고부하 3D 제작 환경에서 발생하는 모든 비즈니스 기회를 포착할 수는 없습니다. 또한, 소프트웨어 인증 상황도 대체 작업의 진전을 늦추고 있습니다. 전문 구매자들은 전문적인 렌더링 및 시각화 워크플로우 분야에서 오랜 실적을 쌓아온 하드웨어를 계속해서 지정하는 경우가 많기 때문입니다. 그 결과, 통합 GPU 시장은 계속 확대될 것이지만, 예측 기간 동안 가장 요구 사항이 까다로운 그래픽스 분야에서는 그 보급이 제한적인 수준에 그칠 가능성이 높습니다.

부문별 분석

2025년, 모바일 SoC는 통합 GPU 시장에서 49.32%의 점유율을 차지하며, 이 부문은 전 세계 출하 대수에서 여전히 중심적인 위치를 차지하고 있습니다. 통합 GPU 시장 규모의 상당 부분은 스마트폰 및 태블릿에서 비롯됩니다. 이는 그래픽 IP가 애플리케이션 프로세서에 직접 내장되어 있으며, 이러한 프로세서들이 폭넓은 소비자 가격대에서 매우 대량으로 출하되고 있기 때문입니다. 통합 GPU 업계의 이 분야에서는 각 벤더들이 단순한 원시 연산 능력뿐만 아니라 게임 반응성, 화질, AI를 활용한 미디어 기능, 그리고 전력 효율을 놓고 경쟁하고 있습니다. 미디어텍은 “Dimensity 9500”를 통해 이 카테고리를 강화했습니다. 이 제품은 주류 상용 SoC에 Arm G1-Ultra GPU를 탑재하여 그래픽 성능의 최고치를 높이고, 전력 효율을 개선하며, 120 fps의 하드웨어 레이 트레이싱을 구현합니다. 또한, 삼성도 “Exynos 2600”를 통해 프리미엄 모바일 그래픽 성능을 강화했습니다. 이 제품은 Xclipse 960 GPU와 2nm GAA 공정을 특징으로 하며, 플래그십 기기에서 더욱 강력한 시각적 성능을 지원합니다.

통합 그래픽을 탑재한 서버 및 데이터센터용 프로세서는 2031년까지 연평균 성장률(CAGR) 17.62%를 나타낼 것으로 예측되며, 통합 GPU 시장에서 가장 빠르게 성장하는 디바이스 카테고리가 될 것입니다. 이러한 성장은 엣지 AI 및 소형 서버 플랫폼에 대한 수요를 반영한 것으로, 이러한 환경에서는 별도의 추가 카드 없이도 경량 추론 및 오케스트레이션을 실행할 수 있습니다. 데스크톱 및 노트북용 프로세서는 클라이언트 컴퓨팅 분야에서 x86 및 Arm 기반 프로세서가 계속해서 대량으로 채택되고 있으며, 통합 그래픽 기능도 향상됨에 따라 매출 기준 2위 기기 카테고리를 유지하고 있습니다. 인텔의 “Core Ultra 시리즈 3” 및 “Core 시리즈 3”는 더욱 강력한 그래픽스 블록과 첨단 AI 지원 기능을 갖추고 있으며, 프리미엄 및 가성비 노트북 라인 모두에서 통합 GPU 시장이 어떻게 전개되고 있는지를 보여줍니다. 임베디드 및 산업용 SoC는 여전히 매출 규모가 가장 작은 부문이지만, 비주얼 인터페이스, 엣지 비전, 커넥티드 제어 시스템 분야에서 고성능 SoC 설계가 채택됨에 따라 통합 GPU 시장의 잠재 고객 기반은 계속해서 확대되고 있습니다.

지역별 분석

아시아태평양은 2025년에 통합 GPU 시장 점유율의 43.93%를 차지하고 2031년까지 지역별 가장 높은 연평균 성장률(CAGR)인 17.89%를 나타낼 것으로 전망됩니다. 해당 지역이 통합 GPU 시장을 주도하고 있는 것은 SoC 제조의 고도화, 대규모 전자제품 조립, 그리고 스마트폰, 노트북, 소비자용 전자기기에 걸친 막대한 최종 기기 수요가 복합적으로 작용하고 있기 때문입니다. 중국은 기기 조립 규모가 크고, 국내 반도체 역량 강화를 위한 노력을 기울이고 있어 이 지역에서 여전히 최대 수요 거점으로 자리 잡고 있습니다. 지역 내 각 벤더들은 프리미엄 통합 그래픽 기능에 대한 투자를 계속하고 있습니다. 한국은 첨단 모바일 칩 개발을 통해 부가가치를 창출하고 있으며, 삼성의 ‘Exynos 2600”는 해당 지역의 주요 벤더들이 프리미엄 통합 그래픽스 기능에 지속적으로 투자하고 있음을 보여줍니다. 인도 및 동남아시아 역시 5G 보급 확대, 스마트폰 사용 증가, 그리고 일상적인 컴퓨팅에 GPU 탑재 제품을 도입하는 디바이스 액세스 프로그램을 통해 통합 GPU 시장을 확대되고 있습니다.

북미는 통합 GPU 시장에서 두 번째로 큰 지역 매출 기준을 차지하고 있으며, 이는 기업용 PC의 교체 수요, 프리미엄 소비자 수요, 그리고 AI 지원 기기의 보급 확대에 힘입은 결과입니다. 2026년 1월에 시행된 “제232조”에 근거한 반도체 관세는 수입 칩의 조달 경제성을 변화시켜, 일부 구매자들에게는 국내산 또는 관세 면제 공급원의 매력을 높였습니다. 이러한 정책적 배경은 특히 통합 플랫폼이 자재명세서(BOM)의 복잡성을 완화할 수 있는 경우, 미국을 거점으로 한 설계 및 제조 전략을 뒷받침하고 있습니다. 캐나다와 멕시코는 보다 광범위한 북미 공급망에서 주로 조립, 물류, 유통의 역할을 통해 기여하고 있습니다.

유럽은 통합 GPU 시장에서 수요의 중심지일 뿐만 아니라, 전략적인 제조 투자 거점으로서도 지속적으로 발전하고 있습니다. 이 지역 수요는 내장형 그래픽 기능에 의존하는 상용 PC, 산업용 시스템 및 자동차용 전자기기에 의해 뒷받침되고 있습니다. 남미는 통합 GPU 시장에서 규모는 작지만 지속적인 성장을 보이고 있는 지역이며, 그 수요는 중급형 스마트폰 및 모바일 데이터의 보급 확대와 밀접한 관련이 있습니다. 중동 및 아프리카에서도 디지털 전환 프로그램, 스마트 시티 구축, 그리고 커넥티드 감시 시스템의 보급에 힘입어 그래픽 기능을 갖춘 임베디드 및 산업용 SoC에 대한 수요가 증가함에 따라, 소규모 기반에서 지속적으로 성장하고 있습니다. 두 지역 모두에서 통합 GPU 시장은 현지 칩 생산보다는 수입 장치공급 상황과 가격 책정에 여전히 크게 좌우되고 있습니다. 따라서 수요는 환율 변동, 무역 정책, 그리고 주요 반도체 생산 거점에서 공급 부족으로 인한 가격 변동의 영향을 받기 쉬워지고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the integrated GPU market size is expected to increase from USD 44.86 billion in 2025 to USD 50.92 billion in 2026 and reach USD 111.19 billion by 2031, growing at a CAGR of 16.91% over 2026-2031.

This report is Segmented by Device Category (Desktop and Laptop Processors, Mobile SoCs, Embedded and Industrial SoCs, and Server and Data Center Processors With Integrated Graphics), Performance Tier (Entry-Level, Mainstream, Performance, and High-Performance), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Integrated GPU Market Trends and Insights

AI PC Refresh Cycle and On-Device AI Adoption

The integrated GPU market is benefiting from the broader move toward AI-capable personal computing, where graphics blocks now support image enhancement, local model execution, and media processing in mainstream systems. Platform vendors are no longer treating the integrated GPU as a secondary feature, because it now works alongside the CPU and NPU in shared workloads that matter to enterprise and consumer buyers. Intel clearly positioned this shift with the Core Ultra Series 3, which combines up to 12 Xe3 GPU cores and a 50 TOPS NPU in a single package on Intel 18A. That design choice supports the integrated GPU market by raising the baseline graphics capability in AI PCs without adding a separate graphics card. The same approach also improves system balance, as lighter AI tasks can be offloaded to the NPU while the integrated GPU continues to handle visual pipelines and sustained graphics activity. This is helping the integrated GPU market gain a stronger role in commercial refresh cycles and premium notebook positioning.

Rising Graphics Integration Across Mobile SoCs

The integrated graphics processing unit (GPU) market continues to draw its largest unit base from mobile SoCs, where graphics blocks are moving beyond frame rendering and into broader compute and AI-assisted imaging functions. MediaTek expanded that performance range with the Dimensity 9500, which integrates the Arm G1-Ultra GPU, adds a new GPU Dynamic Cache Architecture, delivers 33% higher peak performance, and improves power efficiency by 42% from the prior generation. Samsung also raised expectations in premium smartphones with the Exynos 2600, a 2nm GAA chip that pairs the Xclipse 960 GPU with in-house thermal management and higher ray-tracing capability than the prior model. Qualcomm reinforced the same direction in PC-class mobile silicon with the Snapdragon X2 Elite family, where the Adreno X2-90 integrated GPU supports DirectX 12.2 Ultimate, Vulkan 1.4, and higher performance at the same power level. These changes matter to the integrated GPU market because they widen the performance ceiling of SoCs that already ship at very high volume across phones, tablets, and always-connected PCs. They also show that memory handling, cache design, and graphics efficiency have become core product differentiators in the integrated GPU market rather than supporting features.

Performance Gap Versus Discrete GPUs in AAA and Professional Workloads

The integrated GPU market still faces a clear ceiling in workloads that need long-duration rendering, professional content creation, or advanced gaming at high settings. Even with architectural gains, integrated designs still share system memory and thermal limits, while discrete GPUs keep dedicated memory pools and separate power budgets. Intel's current roadmap shows how far integrated graphics have advanced, but even its newest client platforms position strong integrated graphics within broader package designs rather than as full substitutes for professional discrete hardware. This keeps the integrated GPU market from capturing the entire opportunity in creator workstations, high-end desktops, and heavy 3D production environments. Software certification patterns also slow substitution, because professional buyers often continue to specify hardware that has a longer history in specialist rendering and visualization workflows. As a result, the integrated GPU market will continue to expand, but it is likely to remain limited in the most demanding graphics segments over the forecast period.

Other drivers and restraints analyzed in the detailed report include:

- Unified-Memory Designs Enabling Local AI Inference

- Demand for Power-Efficient Thin-and-Light Computing

- Thermal and Shared-Memory Constraints in Sustained Loads

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mobile SoCs held a 49.32% share of the integrated GPU market in 2025, keeping the category at the center of global shipment volume. The integrated GPU market draws much of its scale from smartphones and tablets because graphics IP is embedded directly into application processors that ship in very large numbers across consumer price bands. In this part of the integrated GPU industry, vendors compete on gaming response, imaging quality, AI-assisted media features, and power efficiency rather than on raw compute power alone. MediaTek strengthened this category with the Dimensity 9500, which added the Arm G1-Ultra GPU, higher peak graphics performance, better power efficiency, and 120 fps hardware ray tracing in a mainstream commercial SoC. Samsung also reinforced premium mobile graphics with the Exynos 2600, which features the Xclipse 960 GPU and a 2nm GAA process, supporting stronger visual performance in flagship devices.

Server and Data Center Processors with Integrated Graphics are projected to expand at a 17.62% CAGR through 2031, making them the fastest-growing device category in the integrated GPU market. This growth reflects demand for edge AI and compact server platforms where lightweight inference and orchestration can run without a separate add-in card. Desktop and Laptop Processors remain the second-largest device category by value, as client computing continues to absorb large volumes of x86 and Arm-based processors, with improving integrated graphics capabilities. Intel's Core Ultra Series 3 and Core Series 3 show how the integrated GPU market is moving across both premium and value notebook lines with stronger graphics blocks and higher AI readiness. Embedded and Industrial SoCs remain the smallest revenue segment, but they continue to widen the addressable base of the integrated GPU market as visual interfaces, edge vision, and connected control systems adopt more capable SoC designs.

Complete Report Scope:

- By Device Category

- Desktop and Laptop Processors

- Mobile SoCs (Smartphones and Tablets)

- Embedded and Industrial SoCs

- Server and Data Center Processors with Integrated Graphics

- By Performance Tier

- Entry-Level (< USD 50)

- Mainstream (USD 50 - USD 150)

- Performance (USD 150 - USD 300)

- High-Performance (> USD 300)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Southeast Asia

- Rest of Asia-Pacific

- South America

- Middle East and Africa

- North America

Geography Analysis

Asia-Pacific held 43.93% of the integrated GPU market share in 2025 and is expected to post the fastest regional CAGR of 17.89% through 2031. The region leads the integrated GPU market because it combines SoC manufacturing depth, high-volume electronics assembly, and very great end-device demand across smartphones, notebooks, and consumer electronics. China remains the largest regional demand center due to its scale in device assembly and its push to strengthen domestic semiconductor capabilities. Regional vendors continue to invest in premium integrated graphics capabilities. South Korea adds value through advanced mobile chip development, and Samsung's Exynos 2600 shows how leading vendors in the region continue to invest in premium integrated graphics capability. India and Southeast Asia are also expanding the integrated GPU market through wider 5G adoption, rising smartphone use, and device access programs that bring more GPU-equipped products into everyday computing.

North America represents the second-largest regional revenue base in the integrated GPU market, supported by enterprise PC replacement, premium consumer demand, and wider adoption of AI-ready devices. The January 2026 Section 232 semiconductor tariffs changed procurement economics for imported chips, increasing the appeal of domestic or tariff-exempt supply for some buyers. That policy backdrop favors US-based design and manufacturing strategies, especially when integrated platforms can help reduce bill-of-material complexity. Canada and Mexico contribute mainly through assembly, logistics, and distribution roles within the broader North American supply chain.

Europe continues to develop as both a demand center and a strategic manufacturing investment location for the integrated graphics processing unit (GPU) market. Regional demand is supported by commercial PCs, industrial systems, and automotive electronics that rely on embedded graphics capability. South America remains a smaller but growing part of the integrated GPU market, with demand tied closely to mid-range smartphones and broader mobile data adoption. The Middle East and Africa are also expanding from a smaller base as digital transformation programs, smart city deployments, and connected surveillance systems increase demand for embedded and industrial SoCs with graphics capability. Across both regions, the integrated GPU market is still shaped more by the availability and pricing of imported devices than by local chip production. This leaves demand sensitive to currency movements, trade policy, and pricing effects stemming from supply tightness in major semiconductor manufacturing hubs.

- Intel Corporation

- Advanced Micro Devices, Inc.

- Apple Inc.

- Qualcomm Incorporated

- MediaTek Inc.

- Samsung Electronics Co., Ltd.

- Arm Limited

- Imagination Technologies Group plc

- UNISOC Technologies Co., Ltd.

- NXP Semiconductors N.V.

- Renesas Electronics Corporation

- Texas Instruments Incorporated

- VeriSilicon Holdings Co., Ltd.

- HiSilicon Technologies Co., Ltd.

- Rockchip Electronics Co., Ltd.

- Allwinner Technology Co., Ltd.

- Loongson Technology Corporation Limited

- Shanghai Zhaoxin Semiconductor Co., Ltd.

- Google LLC

- VIA Technologies, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI PC Refresh Cycle and On-Device AI Adoption

- 4.2.2 Demand for Power-Efficient Thin-and-Light Computing

- 4.2.3 Rising Graphics Integration Across Mobile SoCs

- 4.2.4 Architectural Gains in Mainstream Integrated Graphics

- 4.2.5 Unified-Memory Designs Enabling Local AI Inference

- 4.2.6 Tariff- and Memory-Driven Substitution Away From Entry Discrete GPUs

- 4.3 Market Restraints

- 4.3.1 Performance Gap Versus Discrete GPUs in AAA and Professional Workloads

- 4.3.2 Thermal and Shared-Memory Constraints in Sustained Loads

- 4.3.3 Advanced-Node and LPDDR Supply Allocation Constraints

- 4.3.4 AI PC Spec Inflation Versus Real Memory-Bandwidth Needs

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Supply Chain Analysis

- 4.7 Regulatory Landscape

- 4.8 Technological Outlook

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Category

- 5.1.1 Desktop and Laptop Processors

- 5.1.2 Mobile SoCs (Smartphones and Tablets)

- 5.1.3 Embedded and Industrial SoCs

- 5.1.4 Server and Data Center Processors with Integrated Graphics

- 5.2 By Performance Tier

- 5.2.1 Entry-Level (< USD 50)

- 5.2.2 Mainstream (USD 50 - USD 150)

- 5.2.3 Performance (USD 150 - USD 300)

- 5.2.4 High-Performance (> USD 300)

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 South Korea

- 5.3.3.4 India

- 5.3.3.5 Southeast Asia

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.5 Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Intel Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Apple Inc.

- 6.4.4 Qualcomm Incorporated

- 6.4.5 MediaTek Inc.

- 6.4.6 Samsung Electronics Co., Ltd.

- 6.4.7 Arm Limited

- 6.4.8 Imagination Technologies Group plc

- 6.4.9 UNISOC Technologies Co., Ltd.

- 6.4.10 NXP Semiconductors N.V.

- 6.4.11 Renesas Electronics Corporation

- 6.4.12 Texas Instruments Incorporated

- 6.4.13 VeriSilicon Holdings Co., Ltd.

- 6.4.14 HiSilicon Technologies Co., Ltd.

- 6.4.15 Rockchip Electronics Co., Ltd.

- 6.4.16 Allwinner Technology Co., Ltd.

- 6.4.17 Loongson Technology Corporation Limited

- 6.4.18 Shanghai Zhaoxin Semiconductor Co., Ltd.

- 6.4.19 Google LLC

- 6.4.20 VIA Technologies, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment