|

시장보고서

상품코드

2072688

프랑스의 데이터센터 GPU 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)France Data Center GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

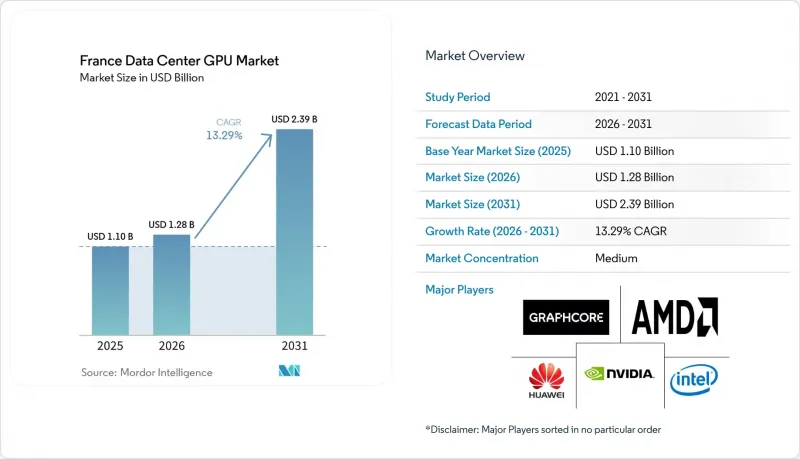

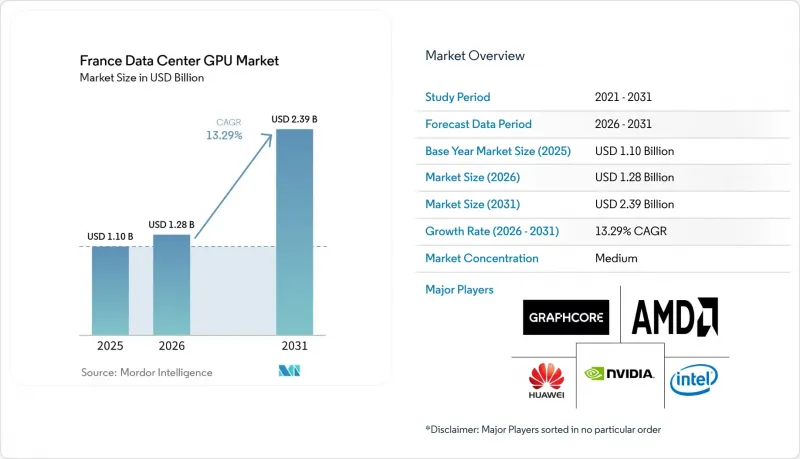

Mordor Intelligence에 의하면, 프랑스의 데이터센터 GPU 시장 규모는 2025년 11억 달러로 평가되었고, 2026년에는 12억 8,000만 달러로 추정되고, 2031년까지 23억 9,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 13.29%로 성장할 전망입니다.

본 보고서는 도입 형태별(클라우드 데이터센터, 엔터프라이즈 및 프라이빗 데이터센터 등), GPU 유형별(훈련용 GPU, 추론용 GPU), 상호 연결 방식별(PCIe 기반 GPU, 고대역폭 상호 연결 GPU), 워크로드 유형별(AI 및 ML, HPC 등), 최종 사용자별(하이퍼스케일러/CSP, 기업, 정부, 연구 기관)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

프랑스의 데이터센터 GPU 시장 동향 및 인사이트

생성형 AI 워크로드 도입이 급증하고 있습니다.

생성형 AI의 부상으로 인해, 프랑스의 GPU 조달은 시범 프로젝트 단계에서 지속 가능한 인프라 계획으로 전환되고 있습니다. 이는 기업이나 연구 기관이 모델 개발과 실제 환경에서의 서비스 제공 모두에서 고밀도 연산 능력을 필요로 하기 때문입니다. 가장 큰 수요는 은행, 보험, 의료, 국방, 통신과 같은 규제 대상 이용 사례에서 발생하고 있으며, 이러한 분야에서는 원시 벤치마크 속도와 마찬가지로 데이터의 국소성과 감사 가능한 처리가 중요하게 여겨지고 있습니다. 이에 따라, 프랑스의 데이터센터 GPU 시장은 사업자가 현지화된 관리, 세심한 서비스, 명확한 규정 준수 지원을 제공함으로써 더 높은 요금을 책정할 수 있는 '프리미엄 소버린 티어'로 향하고 있습니다. 또한, 많은 조직이 소수의 대규모 훈련 실행에만 의존하지 않고, 더 많은 소형 모델을 실제 운영 환경에 배포하고 있기 때문에 수요의 범위도 넓어지고 있습니다. 코르시카 섬에 위치한 SITEC의 AI 호스팅 플랫폼은 공공 디지털 혁신 프로그램의 일환으로, 지역 내 실험, 유연한 GPU 프로파일, 직접적인 기술 지원을 목적으로 현지 인프라가 어떻게 구축되어 있는지를 보여줍니다. 이러한 워크로드가 운영 팀 및 사업 부서에 점점 더 가까워짐에 따라, 프랑스의 데이터센터 GPU 시장은 더욱 안정적인 가동률, 재구매 증가, 그리고 지역적 추론 능력에 대한 관심 고조라는 혜택을 누리고 있습니다.

프랑스 내 하이퍼스케일 시설의 급속한 확대

대규모 캠퍼스 건설이 진행됨에 따라, 향후 10년 동안 프랑스 데이터센터 GPU 시장의 성장을 뒷받침할 물리적 기반이 확대되고 있습니다. Data4사는 노제에 위치한 PAR03 캠퍼스에 대한 투자 계획을 10억 유로(22억 6,000만 달러)에서 20억 유로(22억 6,000만 달러)로 상향 조정하고, 해당 부지의 전력 용량을 250 MW로 증설하여 약 20만 대의 GPU를 수용할 수 있도록 설계했습니다. 이는 프랑스에서 계획 중인 클러스터가 얼마나 대규모로 확대되고 있는지를 보여줍니다. 또한 이 회사는 PAR03과 기존의 마르쿠시스 캠퍼스를 상호 연결하여 더 대규모의 디지털 회랑을 구축함으로써, 파리 사크레 지역을 AI 역량의 중심지로 강화할 계획입니다. 수도권 이외 지역에서는 일리아드(Iliad)와 옵코어(OpCore)가 EDF와 공동으로 몬테로의 700MW 규모 부지에 25억 유로(28억 3,000만 달러)를 투자하기로 결정했습니다. 한편, 다른 사업자들도 보르도와 그 밖의 지방 도시에서 대규모 프로젝트를 계획하고 있습니다. 이러한 규모의 용량 확대를 통해 장비 할당 효율이 개선되고, 주요 고객의 대기 시간이 단축될 뿐만 아니라, 프랑스의 데이터센터 GPU 시장이 국가 주도의 AI 프로젝트와 상용 클라우드 수요를 동시에 지원할 수 있게 될 것입니다. 또한, 핵심인 전력 및 네트워크가 확보된다면 사업자는 단순히 부지 접근성뿐만 아니라 냉각 설계, 인증, 관리형 AI 도구 등의 측면에서 차별화를 꾀할 수 있으므로, 보다 전문적인 서비스를 제공할 여지도 생깁니다.

프랑스의 높은 전기 요금

GPU 클러스터는 높은 가동률을 직접적으로 막대한 정기 전기 요금으로 이어지게 하기 때문에 전력은 여전히 프랑스 데이터센터 GPU 시장에 있어 실질적인 제약 요인으로 남아 있습니다. 2025년에 ARENH의 규제 접근 제도가 종료됨에 따라, 장기 계약이나 강력한 협상력을 갖추지 못한 사업자들에게는 가격의 확실성이 떨어지게 되어 신규 프로젝트의 재무 계획 수립이 어려워지고 있습니다. 이러한 압박은 위험을 대규모 시설에 분산시킬 수 없는 독립형 코로케이션 제공업체, 민간 기업의 자체 부지, 그리고 지방의 시설에 가장 크게 가중되고 있습니다. 랙 밀도 증가 또한 이 문제를 더욱 심각하게 만들고 있습니다. 왜냐하면 사업자가 최신 세대의 가속기로 전환하면, 냉각 요구 사항이 증가함에 따라 전력 비용도 상승하기 때문입니다. 대규모 캠퍼스나 국가 주도의 프로젝트는 유리한 조건을 협상하거나 일시적인 가격 변동을 흡수할 여력이 있기 때문에 프랑스의 데이터센터 GPU 시장에서 초대형 구매자와 소규모 참여자 간에 격차가 발생하고 있습니다. 전력 가격이 불안정한 상태가 지속된다면, 일정 용량은 여전히 구축되겠지만, 더 많은 구매자들이 대규모의 즉각적인 도입보다는 하이브리드 이용 모델이나 단계적인 도입을 선호하게 될 것입니다.

부문별 분석

2025년에는 클라우드 데이터센터가 도입 유형별 매출의 53.47%를 차지한 것으로 평가되었으며, 멀티테넌트 활용을 통해 하드웨어 활용도 향상, 가격 책정의 유연성 강화, 교체 주기 단축이 이루어짐에 따라, 프랑스 데이터센터 GPU 시장의 주요 상업적 기반으로 계속 자리매김할 것으로 보입니다. 한편, 엣지 데이터센터 시장은 2031년까지 연평균 성장률(CAGR) 14.90%로 성장할 것으로 전망됩니다. 대규모 캠퍼스에서는 고밀도 전력 공급, 액체 냉각 및 관리형 소프트웨어 계층을 결합할 수 있지만, 기업 현장에서는 이를 동일한 속도로 재현하기 어려운 경우가 많습니다. Data4사의 PAR03 프로젝트는 이러한 규모의 우위를 명확히 보여주고 있습니다. 이 회사는 투자 계획을 20억 유로(22억 6,000만 달러)로 두 배로 늘린 후, 250MW의 전력 용량과 약 20만 대의 GPU를 수용할 수 있도록 노제(Nozay) 캠퍼스를 설계했기 때문입니다. Scaleway의 관리형 H100 서비스와 OVHcloud의 L4, L40S, H100 인스턴스 포트폴리오 확대 역시, 클라우드 사업자가 스타트업부터 규제 대상 기업에 이르기까지 수요가 다양한 광범위한 고객층에 대응할 수 있는 이유를 보여줍니다. 이 모델에 따라 워크로드의 다양화가 진행되더라도, 프랑스의 데이터센터 GPU 시장은 대규모 공유 시설을 기반으로 계속 운영될 것입니다.

엣지 데이터센터는 2031년까지 가장 빠르게 성장할 것으로 예측됩니다. 이는 추론, 산업용 분석 및 그래픽을 많이 활용하는 이용 사례에서 중앙 집중형 캠퍼스 환경에서는 항상 허용 가능한 지연 시간으로 제공할 수 없는 수준의 근접성이 요구되기 때문입니다. UltraEdge의 'Datapoles' 프로그램은 보르도, 리옹, 스트라스부르, 릴, 낭트를 포함한 9개 지역 거점에 4억 유로(4억 5,200만 달러)와 51MW를 투자하여, 자동차, 산업용 IoT, 실시간 동영상 워크로드에서 10밀리초 미만의 처리 속도를 지원하는 것을 목표로 하고 있습니다. 표준화된 모듈식 구축을 통해 납기 기간도 단축되며, 지역별 공급이 실제 수요에 더 신속하게 대응할 수 있게 됩니다. 사용자가 직접적인 제어, 안정적인 가동률, 클라우드 아웃바운드 비용 발생을 원하지 않는 상황에서는 엔터프라이즈 및 프라이빗 데이터센터의 중요성이 여전히 높습니다. 따라서 Dell이나 Lenovo와 같은 서버 공급업체들은 현재 소유형과 종량제 방식의 GPU 환경을 모두 지원하고 있습니다. 그 결과, 프랑스의 데이터센터 GPU 업계는 단일 도입 모델로 나아가는 대신, 클라우드 규모, 엣지의 응답성, 사설 환경의 주권 등 각기 다른 운영상의 과제를 해결하는 계층적 구조로 전환되고 있습니다.

2025년 프랑스 데이터센터 GPU 시장 규모에서 훈련용 GPU는 57.83%의 점유율을 차지했습니다. 이는 대규모 모델 개발이나 과학 시뮬레이션에는 여전히 고밀도 클러스터에 배포된, 고가이며 대용량 메모리를 갖춘 가속기가 필요하기 때문입니다. 한편, 추론용 GPU는 2031년까지 연평균 성장률(CAGR) 14.04%를 기록하며 가장 높은 성장세를 보일 것으로 예측됩니다. 이러한 지출 양상은 주권 AI에 대한 야망으로 인해 더욱 강화되고 있습니다. 왜냐하면, 모델 훈련을 국내에서 관리하고자 하는 조직은 고성능 하드웨어와 이를 뒷받침하는 인프라에 선행 투자를 해야 하기 때문입니다. 또한, 훈련용 클러스터는 네트워크 및 냉각 관련 비용도 많이 드는 경향이 있어, 그 결과 소규모 추론 환경에 비해 수익에서 차지하는 비중이 높아집니다. 한편, 클라우드 제공업체들이 현재 프로덕션 환경을 위해 다양한 저전력 가속기를 제공하고 있어 수요의 폭도 넓어지고 있습니다. Scaleway의 H100, L40S, L4 인스턴스 가격 정책과 OVHcloud의 월간 GPU 옵션 포트폴리오는 구매자가 가속기를 서빙, 미세 조정 및 혼합 엔터프라이즈 워크로드에 더욱 밀접하게 맞출 수 있게 되었음을 보여줍니다.

기업들이 고립된 실험 단계에서 고객 서비스, 부정 행위 감지, 추천, 문서 자동화 등의 분야로 생산 환경에 적용하는 단계로 전환함에 따라, 추론용 GPU는 2031년까지 가장 빠른 성장세를 보일 것으로 전망됩니다. 프랑스 데이터센터 GPU 시장의 이 분야는 전력 효율 향상, 시간당 단가 하락, 그리고 많은 실전 모델이 가장 고가의 훈련용 칩을 필요로 하지 않는다는 사실로부터 혜택을 보고 있습니다. AMD가 2025년 6월에 발표한 'Instinct MI350 시리즈'는 가성비(1달러당 토큰 수) 향상을 전면에 내세우고 있으며, 이로 인해 추론용 GPU의 가격 경쟁에 더욱 큰 압박이 가해지고, 선택할 수 있는 공급업체의 폭도 넓어지고 있습니다. 훈련용 GPU는 국가 차원의 계산 능력에 있어 여전히 필수적입니다. 이는 주권 사이트에서의 첨단 조사 및 하이엔드 AI 워크로드를 지원하는 'Alice Recoque' 그리고 '장 자이' 업그레이드에서 알 수 있습니다. 따라서 프랑스의 데이터센터 GPU 업계는 훈련이 기술적 위상과 고액 거래 규모를 유지하는 한편, 추론이 보다 광범위하고 안정적인 도입 곡선을 가져오는 단계에 접어들었습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the france data center GPU market size is expected to increase from USD 1.10 billion in 2025 to USD 1.28 billion in 2026 and reach USD 2.39 billion by 2031, growing at a CAGR of 13.29% over 2026-2031.

This report is Segmented by Deployment Type (Cloud Data Centers, Enterprise/Private Data Centers, and More), GPU Type (Training GPUs, Inference GPUs), Interconnect (PCIe-Based GPUs, High-Bandwidth Interconnect GPUs), Workload Type (AI and ML, HPC, and More), and End-User (Hyperscalers/CSPs, Enterprises, Government, and Research Institutions). Market Forecasts are Provided in Terms of Value (USD).

France Data Center GPU Market Trends and Insights

Surging Adoption of Generative AI Workloads

Generative AI is moving GPU procurement in France from pilot projects into sustained infrastructure planning, because enterprises and research organizations now need dense compute for both model development and production serving. The strongest demand comes from regulated use cases in banking, insurance, healthcare, defense, and telecommunications, where data locality and auditable processing matter as much as raw benchmark speed. This is pushing the France Data Center GPU Market toward a premium sovereign tier in which operators can charge more for local control, tighter service, and clearer compliance support. The demand profile is also widening because many organizations now deploy a larger number of smaller models in production instead of relying only on a few large training runs. SITEC's AI hosting platform in Corsica shows how local infrastructure is being positioned for regional experimentation, flexible GPU profiles, and direct technical support under public digital-innovation programs. As these workloads move closer to operations teams and business units, the France Data Center GPU Market benefits from steadier utilization, more repeat buying, and stronger interest in regional inference capacity.

Rapid Expansion of France-Based Hyperscale Facilities

The build-out of large campuses is increasing the physical base on which the France Data Center GPU Market can grow over the rest of the decade. Data4 raised planned investment in its PAR03 campus in Nozay from EUR 1 billion (USD 2.26 billion) to EUR 2 billion (USD 2.26 billion), lifted the site to 250 MW, and designed it to host around 200,000 GPUs, which signals how large planned clusters are becoming in France. The company also plans to interconnect PAR03 with its existing Marcoussis campus, creating a larger digital corridor that strengthens the Paris-Saclay area as a gravity center for AI capacity. Outside the capital region, Iliad and OpCore committed EUR 2.5 billion (USD 2.83 billion) to a 700 MW site in Montereau with EDF, while other operators are planning large projects in Bordeaux and other secondary locations. More capacity at this scale improves equipment allocation, shortens wait times for large customers, and helps the France Data Center GPU Market support both sovereign AI projects and commercial cloud demand at the same time. It also creates room for more specialized services, because once core power and networking are available, operators can differentiate on cooling design, certification, and managed AI tooling rather than on land access alone.

Persistently High Electricity Prices in France

Electricity remains a real constraint for the France Data Center GPU Market because GPU clusters convert high utilization directly into large recurring energy bills. The end of the ARENH regulated-access mechanism in 2025 reduced price certainty for operators that do not have long-term contracts or strong negotiating leverage, which makes financial planning harder for new projects. This pressure is strongest for independent colocation providers, private enterprise sites, and regional facilities that cannot spread risk across very large estates. Higher rack densities also compound the issue, because power costs rise together with cooling requirements once operators move into the newest accelerator generations. Large campuses and sovereign projects are better placed to negotiate favorable terms or absorb temporary volatility, which creates a gap between very large buyers and smaller participants in the France Data Center GPU Market. If power pricing remains unstable, some capacity will still be built, but more buyers will favor hybrid use models and staged deployments rather than large immediate rollouts.

Other drivers and restraints analyzed in the detailed report include:

- Government Tax Incentives for Green Data Centers

- Falling Total Cost of Ownership of GPU-Accelerated Servers

- Limited Domestic Supply Chain for Advanced Packaging

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud data centers commanded 53.47% of deployment-type revenue in 2025, and they remain the main commercial base of the France Data Center GPU Market because multi-tenant utilization supports better hardware absorption, stronger pricing flexibility, and faster refresh cycles, while edge data centers are projected to expand at 14.90% CAGR through 2031. Large campuses can combine dense power, liquid cooling, and managed software layers in ways that enterprise sites often struggle to replicate at the same speed. Data4's PAR03 project shows the scale advantage clearly, because the company designed the Nozay campus for 250 MW and around 200,000 GPUs after doubling its investment plan to EUR 2 billion (USD 2.26 billion). Scaleway's managed H100 offering and OVHcloud's widening portfolio of L4, L40S, and H100 instances also show why cloud operators can serve a broad buyer base that ranges from startups to regulated enterprises with variable demand. This model keeps the France Data Center GPU Market anchored in large shared facilities even as workload diversity increases.

Edge data centers are projected to grow fastest through 2031 because inference, industrial analytics, and graphics-heavy use cases often need proximity that centralized campuses cannot always deliver at acceptable latency. UltraEdge's Datapoles program committed EUR 400 million (USD 452 million) and 51 MW across 9 regional sites, including Bordeaux, Lyon, Strasbourg, Lille, and Nantes, to support sub-10-millisecond processing for automotive, industrial IoT, and real-time video workloads. Standardized modular builds also shorten delivery times, which makes regional supply more responsive to actual demand. Enterprise and private data centers still matter where users want direct control, stable utilization, and no cloud egress costs, and server vendors such as Dell and Lenovo now support both owned and consumption-based GPU estates for that reason. The result is a France data center GPU industry that is not moving toward a single deployment model, but toward a layered structure in which cloud scale, edge responsiveness, and private sovereignty each solve a different operating problem.

Training GPUs accounted for 57.83% share of the France Data Center GPU Market size in 2025 because large model development and scientific simulation still require expensive, high-memory accelerators deployed in dense clusters, while inference GPUs are expected to record the strongest growth at 14.04% CAGR through 2031. That spending pattern is reinforced by sovereign AI ambitions, because organizations that want domestic control over model training must commit upfront capital to powerful hardware and supporting infrastructure. Training clusters also tend to pull in higher networking and cooling spend, which raises their revenue weight relative to smaller inference deployments. At the same time, the demand profile is widening because cloud providers now offer a broader set of lower-power accelerators for production use. Scaleway's pricing for H100, L40S, and L4 instances, along with OVHcloud's portfolio of monthly GPU options, shows how buyers can now match accelerator choice more closely to serving, fine-tuning, and mixed enterprise workloads.

Inference GPUs are projected to grow fastest through 2031 because enterprises are shifting from isolated experimentation toward live deployment across customer service, fraud detection, recommendation, and document automation. This part of the France Data Center GPU Market benefits from better power efficiency, lower hourly pricing, and the fact that many production models do not need the most expensive training silicon. AMD's June 2025 positioning of the Instinct MI350 Series around stronger tokens-per-dollar economics adds more pressure to inference pricing and widens the available supplier set. Training GPUs still remain essential for national compute capability, as shown by Alice Recoque and the Jean Zay upgrade, which both support advanced research and high-end AI workloads at sovereign sites. The France data center GPU industry is therefore entering a phase in which training keeps technical prestige and high ticket sizes, while inference delivers the broader and steadier deployment curve.

Complete Report Scope:

- By Deployment Type

- Cloud Data Centers

- Enterprise / Private Data Centers

- Edge Data Centers

- By GPU Type

- Training GPUs

- Inference GPUs

- By Interconnect

- PCIe-Based GPUs

- High-Bandwidth Interconnect GPUs

- By Workload Type

- Artificial Intelligence (AI) and Machine Learning (ML)

- High-Performance Computing (HPC) (non-AI scientific computing)

- Data Analytics (database acceleration, query processing)

- Graphics and Visualization (VDI, rendering, digital twins)

- By End-User

- Hyperscalers / Cloud Service Providers

- Enterprises

- Government and Research Institutions

List of Companies Covered in this Report:

- Nvidia Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Atos SE

- Eviden

- OVH Groupe SA

- Scaleway

- Orange Business Services

- Hewlett Packard Enterprise Company

- Dell Technologies Inc.

- IBM Corporation

- Graphcore Limited

- Huawei Technologies Co., Ltd.

- Cerebras Systems Inc.

- SambaNova Systems Inc.

- Tenstorrent Inc.

- Giga Computing Technology Co., Ltd.

- Lenovo Group Limited

- Fujitsu Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Adoption of Generative AI Workloads

- 4.2.2 Rapid Expansion of France-Based Hyperscale Facilities

- 4.2.3 Government Tax Incentives for Green Data Centers

- 4.2.4 Falling Total Cost of Ownership of GPU-Accelerated Servers

- 4.2.5 Growth of Sovereign-Cloud Compliance Mandates

- 4.2.6 Emergence of Small-Scale Modular Edge Data Centers

- 4.3 Market Restraints

- 4.3.1 Persistently High Electricity Prices in France

- 4.3.2 Limited Domestic Supply Chain for Advanced Packaging

- 4.3.3 Data-Localization Rules Slowing Cross-Border Cloud Growth

- 4.3.4 Cooling Infrastructure Bottlenecks for >700 W GPUs

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitute Products or Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 Cloud Data Centers

- 5.1.2 Enterprise / Private Data Centers

- 5.1.3 Edge Data Centers

- 5.2 By GPU Type

- 5.2.1 Training GPUs

- 5.2.2 Inference GPUs

- 5.3 By Interconnect

- 5.3.1 PCIe-Based GPUs

- 5.3.2 High-Bandwidth Interconnect GPUs

- 5.4 By Workload Type

- 5.4.1 Artificial Intelligence (AI) and Machine Learning (ML)

- 5.4.2 High-Performance Computing (HPC) (non-AI scientific computing)

- 5.4.3 Data Analytics (database acceleration, query processing)

- 5.4.4 Graphics and Visualization (VDI, rendering, digital twins)

- 5.5 By End-User

- 5.5.1 Hyperscalers / Cloud Service Providers

- 5.5.2 Enterprises

- 5.5.3 Government and Research Institutions

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nvidia Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Atos SE

- 6.4.5 Eviden

- 6.4.6 OVH Groupe SA

- 6.4.7 Scaleway

- 6.4.8 Orange Business Services

- 6.4.9 Hewlett Packard Enterprise Company

- 6.4.10 Dell Technologies Inc.

- 6.4.11 IBM Corporation

- 6.4.12 Graphcore Limited

- 6.4.13 Huawei Technologies Co., Ltd.

- 6.4.14 Cerebras Systems Inc.

- 6.4.15 SambaNova Systems Inc.

- 6.4.16 Tenstorrent Inc.

- 6.4.17 Giga Computing Technology Co., Ltd.

- 6.4.18 Lenovo Group Limited

- 6.4.19 Fujitsu Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment