|

시장보고서

상품코드

2072690

싱가포르의 데이터센터 GPU 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Singapore Data Center GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

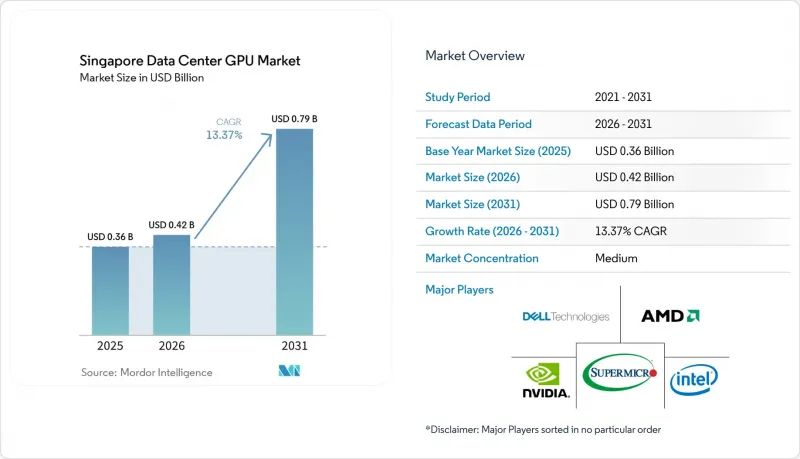

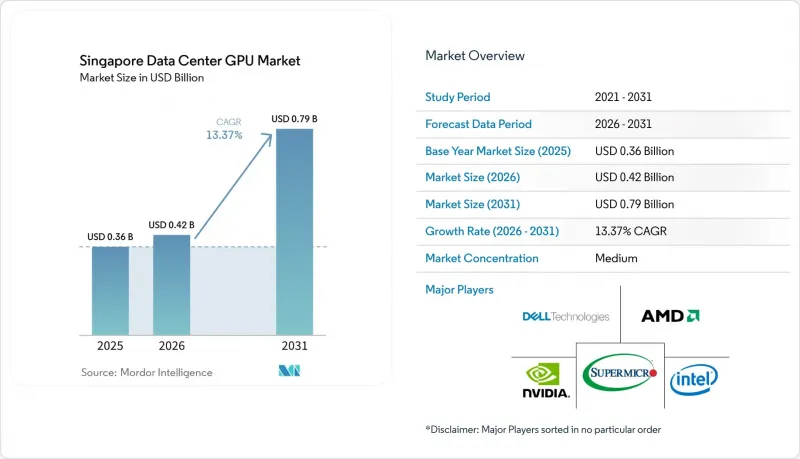

Mordor Intelligence에 의하면, 싱가포르의 데이터센터 GPU 시장 규모는 2026년에 4억 2,000만 달러로 추정되고, 2025년 3억 6,000만 달러에서 2031년까지 7억 9,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 13.37%로 성장할 전망입니다.

본 보고서는 배포 유형별(클라우드 데이터센터, 엔터프라이즈 및 프라이빗 데이터센터 등), GPU 유형별(훈련용 GPU, 추론용 GPU), 상호 연결 방식별(PCIe 기반 GPU, 고대역폭 상호 연결 GPU), 워크로드 유형별(AI 및 ML, HPC 등), 최종 사용자별(하이퍼스케일러/CSP, 기업, 정부, 연구 기관)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

싱가포르의 데이터센터 GPU 시장 동향 및 인사이트

생성형 AI 및 LLM 훈련 수요의 급증

대규모 언어 모델(LLM)의 훈련은 새로운 GPU 클러스터 도입의 가장 큰 원동력이 되고 있습니다. ASPIRE 2A+ 슈퍼컴퓨터에 탑재된 320개의 NVIDIA H100 GPU 덕분에 MERaLiON 모델의 훈련 시간이 340일에서 6일 미만으로 단축되었으며, 고밀도 가속기를 통해 생산성이 비약적으로 향상된다는 사실이 입증되었습니다. 현재, 소버린 AI 이니셔티브에서는 데이터 상주성을 유지하기 위해 온프레미스 처리 능력이 요구되고 있으며, 각 기관은 최첨단 워크로드를 처리하기 위해 B200 DGX SuperPOD 도입을 추진하고 있습니다. Firmus AI와 같은 지역 모델 개발 기업들은 수백 대의 H200 GPU를 수개월에 걸쳐 예약해 놓았으며, 이러한 수요 패턴은 현물 시장만으로는 감당할 수 없습니다. 대학 내 클러스터에서는 동영상 생성형 AI, 외과 수술 지원 AI, 재료 과학 등이 지원되고 있으며, 활용 사례는 자연어 처리의 범위를 넘어 확대되고 있습니다. 모델 규모가 커짐에 따라 상호 연결 대역폭과 메모리 용량이 아키텍처 선택에 결정적인 요인이 되면서, InfiniBand 패브릭으로의 전환이 더욱 가속화되고 있습니다.

싱가포르 내 하이퍼스케일러의 확장과 사전 확보 용량

마이크로소프트, 아마존 웹 서비스(AWS), 구글은 2024-2029년 싱가포르 내 시설 건설에 총 190억 달러 이상을 투자할 예정이며, 그 대부분은 다수의 GPU를 탑재한 가용성 구역을 대상으로 하고 있습니다. Keppel DC REIT의 하이퍼스케일러로부터의 임대료 수입은 2025 회계연도에 매출의 69.3%에 달했으며, 임대료 조정률은 45%에 이르렀습니다. 이는 클라우드 업계의 주요 기업이 수냉식 데이터센터에 대해 추가 임대료를 지불할 의사를 밝힌 것입니다. DC-CFA2 프로그램의 200메가와트 상한선과 2026년 3월의 건설 기한이 맞물리면서 토지 확보 경쟁이 촉발되었고, 각 하이퍼스케일러 기업들은 수년에 걸친 계약을 체결할 수밖에 없게 되었습니다. 기존 홀을 GPU실로 전환하는 자산 담보형 프로젝트가 가속화되고 있으며, KDC 싱가포르 7 및 8을 14억 싱가포르 달러에 인수한 사례가 그 대표적인 예입니다. 이러한 움직임으로 인해, 인근 말레이시아에 더 저렴한 용량이 있음에도 불구하고 싱가포르는 이 지역의 AI 중심지로서의 입지를 확고히 하고 있습니다.

신규 시설을 제한하는 부지 및 전력 제약

싱가포르의 건설 동결 조치는 DC-CFA2 공모를 통해 부분적으로만 해제되었지만, 확장 규모를 200메가와트로 제한하고 재생에너지 비중을 50%로 의무화하고 있어 랙 밀도를 최대 120kW까지 높여야만 하는 상황입니다. 공간 부족은 냉각, 전력, 구조상의 복잡성을 초래하여 프로젝트 일정을 지연시키고 있습니다. 사업자들은 말레이시아와 호주에서 용량을 확보함으로써 리스크를 분산하고 있지만, 지연 시간에 민감한 AI 추론은 여전히 싱가포르에 집중되어 있습니다. 국경을 넘는 재생에너지 수입은 여전히 불투명하며, 태양광 발전 생산량은 제한된 옥상 공간으로 인해 제약을 받고 있으므로, 이러한 제약은 2026년 이후에도 지속될 전망입니다.

부문별 분석

2025년, 싱가포르 데이터센터 GPU 시장 규모 중 67.42%를 클라우드 데이터센터가 차지했습니다. 이는 하이퍼스케일러의 규모의 경제성과, 수년에 걸친 재생에너지 전력 구매 계약을 체결할 수 있는 능력을 반영한 것입니다. 한편, 엣지 데이터센터는 2031년까지 연평균 성장률(CAGR)이 16.94%에 달할 전망이며, 가장 빠르게 성장이 전망되는 부문으로 꼽혔습니다. 마이크로소프트와 AWS가 향후 몇년치 GPU 용량을 확보함에 따라 시장 집중도가 더욱 심화되었고, 코로케이션 요금은월1kW당 480달러라는 높은 수준으로 치솟았습니다. 금융 서비스 업계의 데이터 거주 요건이 강화됨에 따라 엔터프라이즈급 프라이빗 클라우드가 부활했고, 각 은행들은 Tier 4 시설 내에 온프레미스 GPU 구역을 구축하기 시작했습니다. 엣지 인프라 구축은 투아스(Tuas)의 자율주행차 테스트 코스 및 10밀리초 미만의 지연 시간이 필수적인 항만에서의 라이브 스트림 분석에 힘입어 가장 급격한 성장세를 기록했습니다.

2026년, 싱가포르의 데이터센터 GPU 시장에서는 클라우드 사업자들이 기존 시설에 침지 냉각 탱크를 사후 설치하는 한편, 엣지 전문 기업들은 5G 기지국 근처에 6kW급 조립식 포드를 배치할 전망입니다. Nxera의 케이블 랜딩 통합 모델은 클라우드급 처리량으로 지역 수준의 추론 처리를 제공함으로써 코어와 엣지의 경계를 더욱 모호하게 만듭니다. 대학과 정부 산하 연구소들은 주권적 워크로드를 위해 국내 클러스터 구축을 지속하고 있으며, 절대적인 용량은 증가하는 반면 클라우드 점유율은 소폭 하락할 전망입니다.

2025년 싱가포르 데이터센터 GPU 시장에서는 고객 대상 챗봇, 부정 감지 시스템, 디지털 트윈 등이 저지연 응답을 필요로 함에 따라, 추론용 디바이스가 56.93%의 점유율을 차지하며 해당 부문을 주도했습니다. 한편, 훈련용 GPU는 예측 기간인 2031년까지 연평균 성장률(CAGR) 17.45%라는 가장 높은 성장률을 기록하고 있습니다. 각 은행은 기존 공조 덕트에 설치될 수 있도록 전력 소비 상한을 60와트로 제한한 H100 NVL 카드를 채택한 반면, 물류 기업들은 컴퓨터 비전 용도로 L40S 보드를 표준화했습니다. 그러나 대규모 언어 모델 개발자들이 H200 및 초기 Blackwell의 할당량을 확보함에 따라, 훈련용 가속기가 가장 빠른 성장세를 기록했습니다.

싱가포르 데이터센터 GPU 시장 점유율은 공공 부문 구매자들이 국가 안보용 언어 모델을 위해 DGX SuperPOD를 발주함에 따라 훈련용으로 기울어졌습니다. 멀티테넌트 제약으로 인해 프라이빗 클라우드는 추론 전용 랙으로만 제한되어 왔으나, GB200급 시스템에 탑재된 새로운 분리 기능을 통해 2027년 이후부터는 혼합 워크로드 클러스터 구성이 가능해집니다. 또한, 교육 수요는 통합 메모리 클러스터의 도입을 촉진할 것이며, 두 유형의 GPU가 경쟁하기보다는 점점 더 공존하게 될 것으로 확실시되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

제8장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the singapore data center GPU market size was valued at USD 0.42 billion in 2026 and is estimated to grow from USD 0.36 billion in 2025 to reach USD 0.79 billion by 2031, advancing at a 13.37% CAGR over 2026-2031.

This report is Segmented by Deployment Type (Cloud Data Centers, Enterprise/Private Data Centers, and More), GPU Type (Training GPUs, Inference GPUs), Interconnect (PCIe-Based GPUs, High-Bandwidth Interconnect GPUs), Workload Type (AI and ML, HPC, and More), and End-User (Hyperscalers/CSPs, Enterprises, Government, and Research Institutions). Market Forecasts are Provided in Terms of Value (USD).

Singapore Data Center GPU Market Trends and Insights

Surge in Generative AI and LLM Training Demand

Large language model training has become the single biggest catalyst for new GPU clusters. The ASPIRE 2A+ supercomputer's 320 NVIDIA H100 GPUs cut the MERaLiON model's training time from 340 days to under 6 days, proving the productivity leap enabled by dense accelerators. Sovereign AI initiatives now require on-premises capacity to maintain data residency, prompting agencies to deploy B200 DGX SuperPODs for frontier workloads. Regional model builders such as Firmus AI reserve hundreds of H200 GPUs for months, a demand pattern spot markets cannot match.University clusters support video generative AI, surgical intelligence, and materials science, broadening use cases beyond natural language processing. As model sizes swell, interconnect bandwidth and memory capacity dictate architectural choices, reinforcing the shift to InfiniBand fabrics.

Hyperscaler Expansion and Pre-Committed Capacity in Singapore

Microsoft, Amazon Web Services, and Google have collectively earmarked more than USD 19 billion for Singapore builds between 2024 and 2029, with a disproportionate share targeting GPU-dense availability zones. Keppel DC REIT's hyperscaler rent climbed to 69.3% of revenue in fiscal 2025, and rental reversions reached 45%, signaling that cloud giants will pay premiums for liquid-cooled halls. The DC-CFA2 program's 200-megawatt cap, coupled with a March 2026 build deadline, triggered a land rush that locked hyperscalers into multi-year commitments. Asset-backed conversions of legacy halls into GPU rooms accelerated, highlighted by KDC Singapore 7 and 8's SGD 1.4 billion purchase. These moves cement Singapore as the region's AI gravity center despite more affordable capacity in neighboring Malaysia.

Land and Power Caps Limiting New Facilities

Singapore's moratorium, lifted only partially through the DC-CFA2 call, restricts expansion to 200 megawatts and mandates 50% renewable energy, forcing rack densities up to 120 kilowatts. Space scarcity drives cooling, electrical, and structural complexities that lengthen project timelines. Operators hedge by securing capacity in Malaysia and Australia, but latency-sensitive AI inference still gravitates to Singapore. Cross-border renewable imports remain uncertain, and solar yield is capped by limited rooftop real estate, sustaining the constraint beyond 2026.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives for Green Data Centers

- Rapid Enterprise Adoption of AI Workloads

- Global GPU Supply Constraints and Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud data centers captured 67.42% of the Singapore data center GPU market size in 2025, reflecting hyperscaler scale economics and their ability to sign multi-year renewable power purchase agreements, while edge data centers were identified as the fastest-growing segment through at 16.94% CAGR through 2031. The concentration deepened as Microsoft and AWS reserved GPU halls years in advance, pushing colocation rates toward the upper end of USD 480 per kilowatt per month. Enterprise-class private clouds mounted a comeback once data residency clauses tightened in financial services, leading banks to carve out on-premises GPU zones inside Tier 4 facilities. Edge builds recorded the sharpest growth, driven by autonomous vehicle testing tracks in Tuas and live-stream analytics at the port, where sub-10-millisecond latency is mandatory.

In 2026, the Singapore data center GPU market sees cloud operators retrofit existing halls with immersion tanks while edge specialists deploy prefabricated 6-kilowatt pods near 5G base stations. Nxera's cable-landing integration model further blurs lines between core and edge by offering regional inference at cloud-class throughput. Universities and government labs continue to build in-country clusters for sovereign workloads, ensuring that the cloud's share edges down slightly even as absolute capacity rises.

Inference devices led the segment with 56.93% share of the Singapore data center GPU market in 2025 as customer-facing chatbots, fraud detectors, and digital twins demanded low-latency responses, whereas training GPUs are registering the highest growth at 17.45% CAGR through 2031 momentum across the forecast window. Banks opted for H100 NVL cards configured for 60-watt power caps to fit within legacy air corridors, while logistics firms standardized on L40S boards for computer vision. Training-class accelerators, however, posted the quickest growth as large language model developers locked in H200 and early Blackwell allocations.

The Singapore data center GPU market share tilted toward training when public-sector buyers ordered DGX SuperPODs for national security language models. Multi-tenancy constraints limited private clouds to inference-only racks, but new isolation features in GB200-class systems will allow mixed-workload clusters from 2027 onward. Training demand also spurred the adoption of unified memory clusters, ensuring that the two GPU types increasingly coexist rather than compete.

Complete Report Scope:

- By Deployment Type

- Cloud Data Centers

- Enterprise / Private Data Centers

- Edge Data Centers

- By GPU Type

- Training GPUs

- Inference GPUs

- By Interconnect

- PCIe-Based GPUs

- High-Bandwidth Interconnect GPUs

- By Workload Type

- Artificial Intelligence and Machine Learning

- High-Performance Computing (non-AI scientific computing)

- Data Analytics (database acceleration, query processing)

- Graphics and Visualization (VDI, rendering, digital twins)

- By End-User

- Hyperscalers / Cloud Service Providers

- Enterprises

- Government and Research Institutions

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Lenovo Group Limited

- Super Micro Computer, Inc.

- ASUStek Computer Inc.

- GIGABYTE Technology Co., Ltd.

- Inspur Electronic Information Industry Co., Ltd.

- Fujitsu Limited

- Huawei Technologies Co., Ltd.

- xFusion Digital Technologies Co., Ltd.

- Equinix, Inc.

- Digital Realty Trust, Inc.

- ST Telemedia Global Data Centres

- Keppel DC REIT

- Singtel Group (Nxera)

- Amazon Web Services, Inc.

- Microsoft Corporation

- Google LLC

- Aethir Pte. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Generative AI and LLM Training Demand

- 4.2.2 Hyperscaler Expansion and Pre-Committed Capacity in Singapore

- 4.2.3 Government Incentives for Green Data Centers

- 4.2.4 Rapid Enterprise Adoption of AI Workloads

- 4.2.5 Decentralized GPUaaS Platforms Filling Capacity Gaps

- 4.2.6 Integrated Cable-Landing Data Centers Lowering Latency

- 4.3 Market Restraints

- 4.3.1 Land and Power Caps Limiting New Facilities

- 4.3.2 Global GPU Supply Constraints and Price Volatility

- 4.3.3 Skilled Workforce Shortage in Liquid-Cooling Operations

- 4.3.4 Water-Use Scrutiny Impacting Facility Permits

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 Cloud Data Centers

- 5.1.2 Enterprise / Private Data Centers

- 5.1.3 Edge Data Centers

- 5.2 By GPU Type

- 5.2.1 Training GPUs

- 5.2.2 Inference GPUs

- 5.3 By Interconnect

- 5.3.1 PCIe-Based GPUs

- 5.3.2 High-Bandwidth Interconnect GPUs

- 5.4 By Workload Type

- 5.4.1 Artificial Intelligence and Machine Learning

- 5.4.2 High-Performance Computing (non-AI scientific computing)

- 5.4.3 Data Analytics (database acceleration, query processing)

- 5.4.4 Graphics and Visualization (VDI, rendering, digital twins)

- 5.5 By End-User

- 5.5.1 Hyperscalers / Cloud Service Providers

- 5.5.2 Enterprises

- 5.5.3 Government and Research Institutions

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Dell Technologies Inc.

- 6.4.5 Hewlett Packard Enterprise Company

- 6.4.6 Lenovo Group Limited

- 6.4.7 Super Micro Computer, Inc.

- 6.4.8 ASUStek Computer Inc.

- 6.4.9 GIGABYTE Technology Co., Ltd.

- 6.4.10 Inspur Electronic Information Industry Co., Ltd.

- 6.4.11 Fujitsu Limited

- 6.4.12 Huawei Technologies Co., Ltd.

- 6.4.13 xFusion Digital Technologies Co., Ltd.

- 6.4.14 Equinix, Inc.

- 6.4.15 Digital Realty Trust, Inc.

- 6.4.16 ST Telemedia Global Data Centres

- 6.4.17 Keppel DC REIT

- 6.4.18 Singtel Group (Nxera)

- 6.4.19 Amazon Web Services, Inc.

- 6.4.20 Microsoft Corporation

- 6.4.21 Google LLC

- 6.4.22 Aethir Pte. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

- 7.1.1 Fujitsu Limited

- 7.1.2 Amazon Web Services, Inc. (Annapurna Labs)

- 7.1.3 Google LLC

- 7.1.4 Samsung Electronics Co., Ltd.

- 7.1.5 EVGA Corporation

- 7.1.6 Xilinx, Inc. (AMD)

- 7.1.7 Arm Ltd.

- 7.1.8 Tyan Computer Corporation

- 7.1.9 Synopsys, Inc.

8 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 8.1 White-Space and Unmet-Need Assessment