|

시장보고서

상품코드

2072689

인도의 데이터센터 GPU 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)India Data Center GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

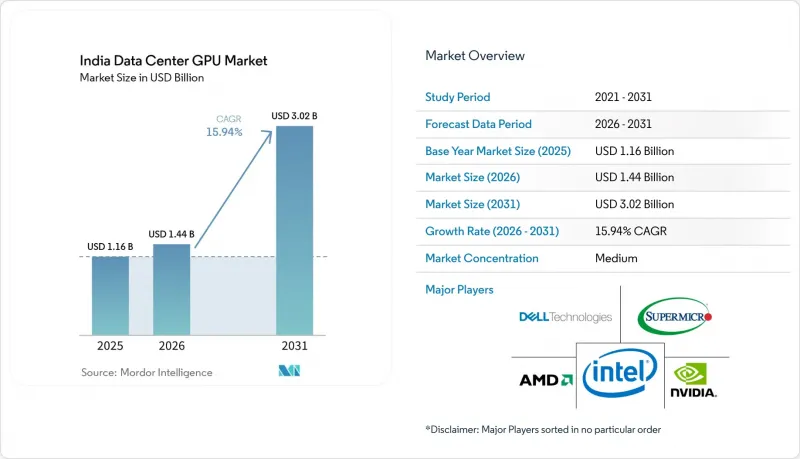

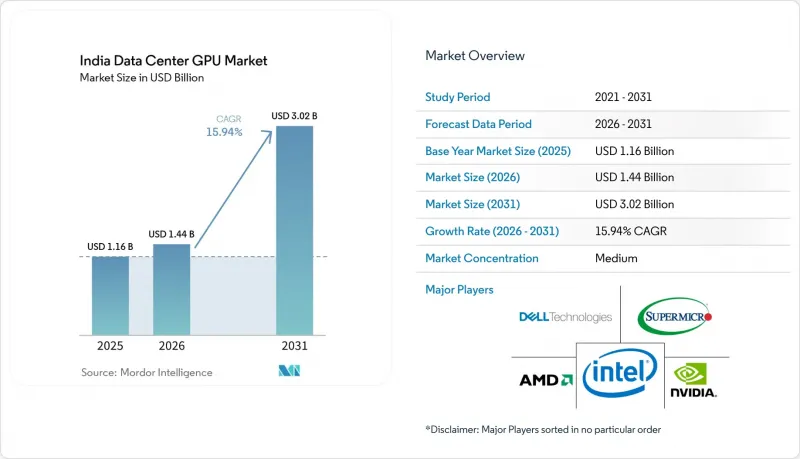

Mordor Intelligence에 의하면, 인도의 데이터센터 GPU 시장 규모는 2025년 11억 6,000만 달러로 평가되었고, 2026년에는 14억 4,000만 달러로 추정되고, 2031년까지 30억 2,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 15.94%로 성장할 전망입니다.

본 보고서는 배포 유형별(클라우드 데이터센터, 엔터프라이즈 및 프라이빗 데이터센터 등), GPU 유형별(훈련용 GPU, 추론용 GPU), 상호 연결 방식별(PCIe 기반 GPU, 고대역폭 상호 연결 GPU), 워크로드 유형별(AI 및 ML, HPC 등), 최종 사용자별(하이퍼스케일러/CSP, 기업, 정부 및 연구 기관)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

인도의 데이터센터 GPU 시장 동향 및 분석

인도 내 하이퍼스케일 클라우드 리전의 급속한 확대

아마존 웹 서비스(Amazon Web Services), 구글 클라우드(Google Cloud), 마이크로소프트(Microsoft), Oracle(Oracle)의 전례 없는 설비 투자를 통해 신규 용량 구축 주기가 24개월 미만으로 단축되었으며, 2028년까지 인도 데이터센터 GPU 시장의 총 GPU 재고량은 2배 이상 증가할 것으로 확실시되고 있습니다. AWS만 해도 하이데라바드에 70억 달러를 투자한 반면, 구글이 150억 달러 규모로 투자한 비사카파트남 지역에서는 해저 케이블 상륙과 H100 클러스터를 결합하여 다국어 추론 워크로드를 처리하고 있습니다. 이러한 투자 열풍에 힘입어 인도 SaaS 제공업체의 왕복 지연 시간이 200-300밀리초에서 50밀리초 미만으로 단축되었으며, 이러한 개선은 추천 엔진의 고객 전환율을 직접적으로 향상시킵니다. 이러한 투자에 따른 일자리 창출 프로그램은 10만 명의 AI 개발자를 양성하는 것을 목표로 하고 있으며, 인재 풀의 확대가 GPU 활용도 향상으로 이어지는 선순환을 강화하고 있습니다. 하이퍼스케일러의 구매 규모는 NVIDIA와 AMD로부터 조기 할당량을 확보함으로써, 전 세계적인 공급 부족으로부터 국내 공급망을 보호하고 있습니다.

'디지털 인디아' 및 데이터 현지화 기준에 따른 정부의 인센티브

10,372 카롤 루피(12억 4,000만 달러) 규모의 'IndiaAI 미션'에 따라 3만 8,000대의 GPU를 시간당 65루피의 보조 가격으로 이용할 수 있도록 배정하고 있으며, 이를 통해 프로토타입 훈련 실행에 드는 경제적 장벽이 일반 클라우드 가격에 비해 70% 낮아졌습니다. 동시에 시행되고 있는 데이터 현지화 관련 법령에 따라 은행, 보험사, 병원은 규제 대상 데이터를 인도 국내에 보관해야 할 의무가 있으며, 이러한 요건으로 인해 자사 전용 및 코로케이션형 GPU 클러스터 모두에 대한 새로운 설비 투자가 촉진되고 있습니다. 증분 매출의 4-6%를 보상하는 생산 연동형 인센티브를 통해 현지 시스템 통합사업자의 총 시스템 비용을 절감함으로써, 브랜드 OEM 제조업체보다 15-20% 저렴한 가격 책정이 가능해집니다. 이 제도에 인도 표준국(BIS)의 인증이 결합됨으로써, 기존 화이트박스 하드웨어에 대한 품질 관련 우려가 해소됩니다. 정부 기관 및 BFSI(은행 및 금융 및 보험) 분야의 워크로드에 대한 조기 도입으로 인해, 엔터프라이즈용 GPU 랙 임대 계약이 전년 대비 40% 증가를 기록하며 수요의 지속성을 보여주고 있습니다.

GPU가 탑재된 데이터센터의 막대한 설비 투자

H100 GPU 8개를 탑재한 1랙당 비용은 부동산 비용과 전력 공급 비용을 제외하더라도 40만-50만 달러에 달할 전망입니다. 이 때문에 중견 시장 참여자들은 성숙한 경제권에서 볼 수 있는 25-30%라는 기준에 비해, 프로젝트 파이낸스 거래에서 40-50%의 자기자본을 배정할 수밖에 없는 실정입니다. 고밀도 AI 클러스터에 필수적인 액체 냉각 시스템의 사후 설치 공사는 랙 1대당 5만-8만 달러의 추가 비용을 발생시키며, 탄소 배출량 공개 규제가 강화되는 가운데 에너지 소비량을 더욱 증가시키고 있습니다. 대출 기관들은 여전히 전용 하드웨어의 잔존 가치 리스크를 경계하고 있으며, 그 결과 금리 스프레드는 기존의 데이터센터 프로젝트에 비해 최대 250베이시스포인트까지 확대되었습니다. Tier 2 부지의 경우, 전력 공급 가동률이 99.99%에 미치지 못하기 때문에 개발사는 디젤 발전기나 배터리 스트링을 과도하게 설치할 수밖에 없으며, 이로 인해 총 건설 비용이 20-25% 더 상승합니다. 전력 사용 효율(PUE) 개선을 장려하는 대상을 선별한 그린 파이낸스 수단이 없다면, 대도시권 클러스터 외부의 신규 시장 진출기업들은 터무니없이 높은 비용 곡선에 직면하게 될 것입니다.

부문별 분석

2025년, 인도의 데이터센터 GPU 시장 점유율의 63.28%를 클라우드 데이터센터가 차지했으며, 이는 하이퍼스케일러가 워크로드를 집약하고 세분화된 이용 계층을 통해 GPU로 수익을 창출할 수 있는 능력을 여실히 보여주었습니다. 한편, 엣지 데이터센터는 2031년까지 연평균 성장률(CAGR)이 16.94%로, 가장 빠르게 성장하는 부문으로 꼽혔습니다. 현재 인도의 데이터센터 GPU 시장에서는 AWS, Microsoft Azure, Google Cloud가 데이터 상주 요건을 준수한 지역 한정 H100 인스턴스를 출시하고 있으며, 이러한 정책 전환은 은행 및 생명과학 기업들로부터 지지를 얻고 있습니다. 기업들은 이러한 인프라를 활용하여 설비 투자(Capex) 부담 없이 단기 교육 업무를 수행함으로써, 대차대조표상의 리스크를 운영 비용(OpEx)으로 전환하고 있습니다. 엣지 시설(대부분 5G 기지국에 연결된 100kW급 포드)은 자율주행 로봇이나 스마트 시티 카메라에서 추론 지연 시간을 10밀리초 미만으로 단축할 수 있어, 가장 빠르게 성장하고 있는 노드 범주로 자리 잡고 있습니다.

이러한 변화를 뒷받침하고 있는 것은 인도 전역 400개 도시에 걸친 5G 구축입니다. 이를 통해 지원 가능한 엣지의 범위가 확대되었으며, 확정적인 지연 시간 보장이 확립되었습니다. Bharti Airtel 등의 통신 사업자들은 NVIDIA와의 제휴를 활용해 추론에 최적화된 GPU를 사전 설치함으로써, OTT 미디어, 물류, 소매 분야의 고객을 대상으로 업셀링이 가능한 자산 기반을 구축하고 있습니다. 규제가 엄격한 업계에서는 사설 데이터센터의 중요성이 여전히 높습니다. FDA의 감사 추적 대상이 되는 의약품 수출업체나 기밀 데이터 취급 규정에 구속되는 방위 관련 기업들은 계속해서 격리된 GPU 클러스터를 도입하고 있습니다. 그 결과, 인도의 데이터센터 GPU 시장 규모는 단일 모델에 집중되기보다는 클라우드, 코로케이션, 엣지로 분산된 하이브리드 토폴로지가 형성되고 있습니다.

2025년, 인도의 데이터센터 GPU 시장 규모 중 58.37%를 추론용 GPU가 차지했습니다. 이는 높은 처리량과 뛰어난 전력 효율을 갖춘 실리콘을 필요로 하는 상용 챗봇, 상품 추천 엔진, 그리고 실시간 부정 행위 감지 모델이 주도한 결과입니다. NVIDIA의 L4 및 L40S 모듈은 와트당 쿼리 수가 뛰어나며, 도시 지역의 코로케이션 시설에서 전력 공급 상한선이 더욱 엄격해지는 추세와 부합하는 특성을 지니고 있어 시장을 독점하고 있습니다. 한편, 훈련용 GPU는 예측 기간인 2031년까지 연평균 성장률(CAGR) 17.45%라는 가장 높은 성장률을 기록하고 있습니다. 훈련용 GPU는 출하 대수는 적지만 평균 판매 가격이 높으며, 인도계 언어 및 멀티모달 컨텐츠용 독자 모델이 정책적 지원을 받음에 따라 급속히 확대되고 있습니다.

Sarvam AI의 4,096대 H100 도입 사례는 거시적 차원의 정책 목표가 고밀도 훈련 전용 클러스터로 자본을 유도하고 있는 실태를 보여줍니다. 동시에, 각 클라우드 벤더들은 모델을 처음부터 구축하는 대신, 오픈 웨이트 모델을 미세 조정하려는 팀들이 더 쉽게 접근할 수 있도록 온디맨드 방식의 8개 GPU 슬라이스 제공을 시작했습니다. 기업에서는 정기적인 재훈련용 H100 클러스터와 일상적인 추론용 L40S 플릿을 함께 사용하는 경우가 많으며, 이를 통해 설비 투자 제약과 지연 시간 목표 사이에서 사내 균형을 맞추고 있습니다. 이러한 혼합 함대 전략은 수요 곡선의 미묘한 뉘앙스를 부각시키고 있습니다. 즉, 인도의 데이터센터 GPU 시장은 훈련용 고대역폭의 밀접하게 결합된 패브릭과, 추론용 PCIe 기반의 저전력 카드, 이 두 가지 모두를 지원해야 합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 전개 유형별

제7장 GPU 유형별

제8장 상호 접속별

제9장 워크로드 유형별

제10장 최종 사용자별

제11장 경쟁 구도

제12장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the india data center GPU market size is expected to increase from USD 1.16 billion in 2025 to USD 1.44 billion in 2026 and reach USD 3.02 billion by 2031, growing at a CAGR of 15.94% over 2026-2031.

This report is Segmented by Deployment Type (Cloud Data Centers, Enterprise/Private Data Centers, and More), GPU Type (Training GPUs, Inference GPUs), Interconnect (PCIe-Based GPUs, High-Bandwidth Interconnect GPUs), Workload Type (AI and ML, HPC, and More), and End-User (Hyperscalers/CSPs, Enterprises, Government and Research Institutions). Market Forecasts are Provided in Terms of Value (USD).

India Data Center GPU Market Trends and Insights

Rapid Expansion of Hyperscale Cloud Regions in India

Unprecedented capital expenditure by Amazon Web Services, Google Cloud, Microsoft, and Oracle is compressing build cycles for new capacity to under 24 months, ensuring that aggregate GPU inventory in the India data center GPU market will more than double before 2028.AWS alone earmarked USD 7 billion for Hyderabad, while Google's USD 15 billion Visakhapatnam region is pairing subsea cable landings with H100 clusters to serve multilingual inference workloads. This wave of investment shortens round-trip latency for Indian SaaS providers from 200-300 milliseconds to sub-50 milliseconds, a gain that directly raises customer conversion rates for recommendation engines. Job creation programs attached to these investments aim to certify 100,000 AI developers, reinforcing a virtuous cycle where a larger talent pool drives higher GPU utilization. Hyperscalers' purchasing scale also secures early allocations from NVIDIA and AMD, shielding the domestic supply stack from global shortages.

Government Incentives Under Digital India and Data Localization Norms

The INR 10,372 crore (USD 1.24 billion) IndiaAI Mission reserves 38,000 GPUs for subsidized usage at INR 65 per hour, lowering the economic barrier for prototype training runs by 70% relative to retail cloud pricing. Parallel data-localization statutes compel banks, insurers, and hospitals to retain regulated data inside India, a mandate that steers fresh capex toward both captive and colocation GPU clusters. Production-linked incentives covering 4-6% of incremental sales reduce total system costs for local integrators, letting them undercut branded OEMs by 15-20%. When combined with Bureau of Indian Standards certification, the scheme removes quality concerns traditionally associated with white-box hardware. Early adoption in government and BFSI workloads has already produced a 40% year-over-year jump in enterprise GPU rack leases, signaling durable demand.

High Capital Expenditure for GPU-Equipped Data Centers

A single rack populated with eight H100 GPUs costs USD 400,000-500,000, excluding real estate and power provisioning, which forces mid-market operators to allocate 40-50% equity in project finance deals versus the 25-30% norms observed in mature economies. Liquid cooling retrofits, now indispensable for dense AI clusters, add another USD 50,000-80,000 per rack and push energy footprints higher at a time when carbon disclosure mandates are tightening. Lenders remain wary of residual-value risk on specialized hardware, making interest spreads up to 250 basis points wider than for traditional data-center projects. In Tier-2 locations, the absence of 99.99% utility uptime obliges developers to oversize diesel gensets and battery strings, lifting all-in build costs by an additional 20-25%. Without targeted green-financing instruments that reward improved power usage effectiveness, new entrants outside the metro clusters face a prohibitive cost curve.

Other drivers and restraints analyzed in the detailed report include:

- Rising AI Startup Ecosystem Demand for GPU-Accelerated Compute

- Surge in Video Streaming, Gaming and AR/VR Requiring GPU-Based Transcoding and Rendering

- Limited Domestic Manufacturing Capacity Leading to Import Dependency

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud data centers accounted for 63.28% of the India data center GPU market share in 2025, underscoring hyperscalers' ability to aggregate workloads and monetize GPUs via granular usage tiers, while edge data centers were identified as the fastest-growing segment through at 16.94% CAGR through 2031. The India data center GPU market now sees AWS, Microsoft Azure, and Google Cloud touting region-locked H100 instances that comply with data-residency statutes, a pivot that resonates with banks and life-sciences firms. Enterprises piggyback on these footprints, spinning up short-lived training jobs without committing capex and thereby shifting balance-sheet exposure to opex. Edge facilities, often 100-kilowatt pods attached to 5G base stations, are the fastest-growing node category because they reduce inference latency to sub-10 milliseconds for autonomous mobile robots and smart-city cameras.

The shift is powered by India's 5G rollout across 400 cities, which is widening the addressable edge radius and establishing deterministic latency guarantees. Telecom operators such as Bharti Airtel leverage partnerships with NVIDIA to pre-install inference-optimized GPUs, creating an asset base that can be upsold to over-the-top media, logistics, and retail clients. Private data centers remain relevant for regulated verticals: pharmaceutical exporters subject to FDA audit trails and defense contractors bound by classified-data handling rules continue to procure isolated GPU clusters. The result is a hybrid topology in which the India data center GPU market size gets distributed across cloud, colocation, and edge rather than gravitating toward a single archetype.

Inference GPUs secured 58.37% of the India data center GPU market size in 2025, driven by commercial chatbots, product-recommendation engines, and real-time fraud-detection models that require high-throughput yet power-efficient silicon. NVIDIA's L4 and L40S modules dominate because they deliver superior queries-per-watt, an attribute that dovetails with tightening power-availability caps in urban colocation campuses, whereas training GPUs are registering the highest growth at 17.45% CAGR through 2031 momentum across the forecast window. Training GPUs, while smaller in volume, command higher average selling prices and are expanding quickly as sovereign models for Indic languages and multimodal content gain policy backing.

Sarvam AI's 4,096-H100 deployment illustrates how macro-level policy ambitions funnel capital into dense, training-only clusters. Concurrently, cloud vendors have launched on-demand eight-GPU slices that democratize access for teams looking to fine-tune open-weights models instead of building from scratch. Enterprises often pair H100 clusters for periodic retraining with L40S fleets for day-to-day inference, striking an internal equilibrium between capex constraints and latency targets. This mixed-fleet strategy underlines a nuanced demand curve: the India data center GPU market must accommodate both high-bandwidth, tightly coupled fabrics for training and PCIe-centric, power-sipping cards for inference.

Complete Report Scope:

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- ASUSTeK Computer Inc.

- Dell Technologies Inc.

- Super Micro Computer, Inc.

- Giga-Computing Technology Co., Ltd. (GIGABYTE)

- Lenovo Group Limited

- Cisco Systems, Inc.

- Hewlett Packard Enterprise Company

- Reliance Industries Limited (Jio Platforms)

- Bharti Airtel Limited (Nxtra Data)

- Sify Technologies Limited

- CtrlS Datacenters Ltd.

- STT Global Data Centres India Pvt. Ltd.

- Yotta Infrastructure Solutions LLP

- AdaniConneX Private Limited

- NTT Global Data Centers and Cloud Infrastructure India Pvt. Ltd.

- Amazon Web Services, Inc.

- Microsoft Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Expansion of Hyperscale Cloud Regions in India

- 4.2.2 Government Incentives Under Digital India and Data Localization Norms

- 4.2.3 Rising AI Startup Ecosystem Demand for GPU-Accelerated Compute

- 4.2.4 Surge in Video Streaming, Gaming and AR/VR Requiring GPU-Based Transcoding and Rendering

- 4.2.5 Deployment of 5G and Edge Computing Driving Micro Data Centers With GPUs

- 4.2.6 Declining Cost per TFLOP of Data Center GPUs Enabling Broader Adoption

- 4.3 Market Restraints

- 4.3.1 High Capital Expenditure for GPU-Equipped Data Centers

- 4.3.2 Limited Domestic Manufacturing Capacity Leading to Import Dependency

- 4.3.3 Power and Cooling Infrastructure Constraints in Tier-2/3 Indian Cities

- 4.3.4 Supply-Chain Volatility in Advanced Packaging Components (HBM, Interposers)

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

6 By Deployment Type

- 6.1 Cloud Data Centers

- 6.2 Enterprise / Private Data Centers

- 6.3 Edge Data Centers

7 By GPU Type

- 7.1 Training GPUs

- 7.2 Inference GPUs

8 By Interconnect

- 8.1 PCIe-Based GPUs

- 8.2 High-Bandwidth Interconnect GPUs

9 By Workload Type

- 9.1 Artificial Intelligence (AI) and Machine Learning (ML)

- 9.2 High-Performance Computing (HPC) (non-AI scientific computing)

- 9.3 Data Analytics (database acceleration, query processing)

- 9.4 Graphics and Visualization (VDI, rendering, digital twins)

10 By End-User

- 10.1 Hyperscalers / Cloud Service Providers

- 10.2 Enterprises

- 10.3 Government and Research Institutions

11 COMPETITIVE LANDSCAPE

- 11.1 Market Concentration

- 11.2 Strategic Moves

- 11.3 Market Share Analysis

- 11.4 Company Profiles (Each profile includes: Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 11.4.1 NVIDIA Corporation

- 11.4.2 Advanced Micro Devices, Inc.

- 11.4.3 Intel Corporation

- 11.4.4 ASUSTeK Computer Inc.

- 11.4.5 Dell Technologies Inc.

- 11.4.6 Super Micro Computer, Inc.

- 11.4.7 Giga-Computing Technology Co., Ltd. (GIGABYTE)

- 11.4.8 Lenovo Group Limited

- 11.4.9 Cisco Systems, Inc.

- 11.4.10 Hewlett Packard Enterprise Company

- 11.4.11 Reliance Industries Limited (Jio Platforms)

- 11.4.12 Bharti Airtel Limited (Nxtra Data)

- 11.4.13 Sify Technologies Limited

- 11.4.14 CtrlS Datacenters Ltd.

- 11.4.15 STT Global Data Centres India Pvt. Ltd.

- 11.4.16 Yotta Infrastructure Solutions LLP

- 11.4.17 AdaniConneX Private Limited

- 11.4.18 NTT Global Data Centers and Cloud Infrastructure India Pvt. Ltd.

- 11.4.19 Amazon Web Services, Inc.

- 11.4.20 Microsoft Corporation

12 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 12.1 White-Space and Unmet-Need Assessment