|

시장보고서

상품코드

2065493

동남아시아의 GPU 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Southeast Asia GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

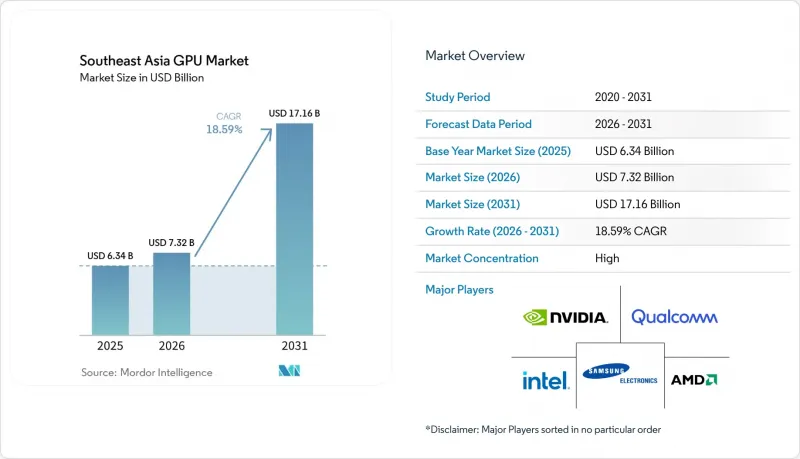

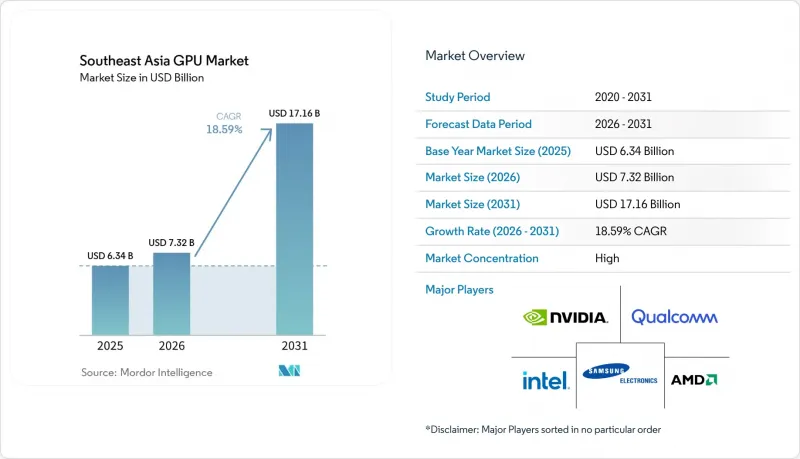

Mordor Intelligence에 의하면, 동남아시아의 GPU 시장 규모는 2026년 73억 2,000만 달러로 추정되고, 2031년까지 171억 6,000만 달러로 확대될 전망이며, 2026-2031년 CAGR 18.59%를 나타낼 것으로 예측되고 있습니다.

본 보고서는 통합형별(통합형 GPU, 디스크리트 GPU) 및 기기 용도별(모바일 기기 및 태블릿, PC 및 워크스테이션, 서버 및 데이터센터용 가속기, 게임기 및 휴대용 기기, 자동차 및 ADAS, 기타 임베디드 및 엣지 기기)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

동남아시아의 GPU 시장 동향 및 인사이트

데이터센터에서 고성능 컴퓨팅에 대한 수요 증가

각 하이퍼스케일러 기업들은 데이터 상주 요건을 충족하고 생성형 AI 추론의 지연 시간을 줄이기 위해 컴퓨팅 클러스터의 현지화를 시작하고 있습니다. 마이크로소프트 애저(Microsoft Azure)는 2025년에 말레이시아와 인도네시아에서 ND GB200-v6 인스턴스를 출시했으며, 구글 클라우드(Google Cloud)도 같은 해 H100 GPU를 탑재한 A3 노드를 갖춘 방콕 리전을 개설했습니다. YTL Power International은 조호르 주에 500 MW 규모의 AI 캠퍼스 건설에 착수했으며, 2027년 완공을 목표로 하고 있습니다. 또한, 지역 내 각 코로케이션 제공업체들은 시설에 액체 냉각 시스템을 도입하는 개보수 작업을 진행하고 있습니다. 이러한 움직임에 힘입어 동남아시아는 싱가포르를 거점으로 하는 ‘스포크’가 아닌, 일류 추론 허브로서의 위상을 확립해 가고 있습니다.

클라우드 게임과 온라인 e스포츠의 급속한 확산

FTTH(Fiber-to-the-home)의 보급과 전국적인 5G 커버리지 덕분에, 구독형 클라우드 게임 서비스에서 20밀리초 미만의 게임 플레이가 가능해졌습니다. Radian Arc와 Singtel-Razer가 진행한 시범 사업은 2024년부터 2025년에 걸쳐 시험 운영을 거쳐 상용 서비스로 전환되었으며, 월 10달러 미만의 가격 책정이 사업 규모 확대에 있어 매우 중요하다는 사실이 밝혀졌습니다. 2025년 동남아시아 경기대회에서 e스포츠가 메달 종목으로 채택됨에 따라, 공공 부문의 GPU를 갖춘 훈련 센터에 대한 투자가 촉진되면서 태국과 필리핀 전역에서 워크스테이션급 그래픽 카드의 단기 구매가 활발해지고 있습니다.

세계 GPU 공급망의 혼란과 칩 부족

HBM3E 메모리는 2025년 내내 공급 부족 상태가 지속되었으며, NVIDIA와 AMD는 다년 계약을 체결한 하이퍼스케일러 기업들에 대한 플래그십 가속기 공급을 제한할 수밖에 없었습니다. 지역 클라우드 서비스 제공업체에 대한 납기 기간은 6개월 이상에 달했으며, TSMC의 CoWoS 패키징 가동률은 90%를 넘어섰습니다. 미국의 수출 규제로 인해 2025년부터 2027년에 걸쳐 인도네시아로 출하되는 데이터센터용 GPU에 5만 대의 상한선이 설정됨에 따라, 기업들은 훈련보다는 추론을 중시할 수밖에 없게 되었습니다.

부문별 분석

2025년, 동남아시아 GPU 시장에서 디스크리트 GPU가 67.85%의 점유율을 차지했습니다. 이 입지는 NVIDIA H200 및 AMD MI325X 가속기를 핵심으로 하는 데이터센터 클러스터 구축을 통해 더욱 공고해졌습니다. 각 하이퍼스케일러 기업들이 수년에 걸친 공급 계약을 체결함에 따라, 동남아시아의 디스크리트 GPU 시장 규모는 2031년까지 연평균 성장률(CAGR) 19.11%로 성장할 전망입니다. YTL Power International사의 500 MW 조호르 시설만 해도 수만 장의 GPU 카드를 도입할 계획이며, 한편 볼보 등 자동차 OEM 제조업체들은 차량 1대당 254 TOPS를 구현하는 듀얼 Drive AGX Orin 보드를 탑재하고 있습니다.

규모는 작지만 성장세가 두드러지는 통합형 GPU는 스마트폰과 AI PC의 출하 대수에 힘입어 성장하고 있습니다. MediaTek의 9500s는 하드웨어 레이 트레이싱 기능을 갖춘 Immortalis-G925 코어를 내장하고 있어, 보급형 디스크리트 그래픽 카드와의 성능 격차를 좁히고 있습니다. 퀄컴의 스냅드래곤 8 Gen 3와 미디어텍의 8500은 인기 모바일 게임에서 60fps를 유지하고 있으며, 이는 과거에는 전용 그래픽 카드에만 맡겨졌던 작업 부하를 현재는 통합 칩이 처리할 수 있게 되었음을 보여줍니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSH 26.06.24According to Mordor Intelligence, the southeast asia gPU market size is expected to increase from USD 7.32 billion in 2026 to USD 17.16 billion by 2031, growing at a CAGR of 18.59% over 2026-2031.

This report is Segmented by Integration Type (Integrated GPUs, Discrete GPUs), and Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive and ADAS, Other Embedded and Edge Devices). The Market Forecasts are Provided in Terms of Value (USD).

Southeast Asia GPU Market Trends and Insights

Rising Demand for High-Performance Computing in Data Centers

Hyperscalers have started localizing compute clusters to satisfy data-residency mandates and reduce latency for generative AI inference. Microsoft Azure rolled out ND GB200-v6 instances in Malaysia and Indonesia in 2025, while Google Cloud launched a Bangkok region with A3 nodes powered by H100 GPUs the same year. YTL Power International broke ground on a 500 MW AI campus in Johor, scheduled for 2027 completion, and regional colocation providers are retrofitting halls with liquid cooling. These moves establish Southeast Asia as a first-tier inference hub rather than a spoke served out of Singapore.

Rapid Adoption of Cloud Gaming and Online Esports

Fiber-to-the-home penetration and nationwide 5G coverage have enabled sub-20 ms gameplay for subscription-based cloud gaming services. Radian Arc and Singtel-Razer pilots moved from trial to commercial launch during 2024-2025, with monthly pricing under USD 10 proving critical for scale. Esports' inclusion as a medal event in the Southeast Asian Games 2025 triggered public-sector investment in GPU-equipped training centers, spurring near-term purchases of workstation-class cards across Thailand and the Philippines.

Global GPU Supply Chain Disruptions and Chip Shortages

HBM3E memory remained constrained through 2025, compelling NVIDIA and AMD to ration flagship accelerators to hyperscalers on multi-year contracts. Lead times for regional cloud providers stretched beyond six months, and CoWoS packaging capacity at TSMC exceeded 90% utilization. U.S. export controls imposed a 50,000-unit ceiling on datacenter GPUs shipped to Indonesia for 2025-2027, forcing enterprises to emphasize inference over training.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of AI-Powered Content Creation for Social Commerce

- Growth of Mobile Gaming Ecosystem in Southeast Asia

- Rising Average Selling Prices Limiting Entry-Level Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Discrete units controlled 67.85% of the Southeast Asia GPU market in 2025, a position amplified by datacenter clusters built around NVIDIA H200 and AMD MI325X accelerators. The Southeast Asia GPU market size for discrete units is on track to expand at a 19.11% CAGR through 2031 as hyperscalers lock in multi-year supply agreements. YTL Power International's 500 MW Johor facility alone plans to host tens of thousands of cards, while automotive OEMs such as Volvo integrate dual Drive AGX Orin boards that deliver 254 TOPS per vehicle.

Smaller but rising, integrated GPUs ride smartphone and AI PC shipments. MediaTek's 9500s embeds an Immortalis-G925 core with hardware ray tracing, trimming the gap with entry-level discrete boards. Qualcomm's Snapdragon 8 Gen 3 and MediaTek's 8500 sustain 60 fps on popular mobile titles, underscoring that integrated silicon now handles workloads once reserved for add-in cards.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Qualcomm Technologies, Inc.

- Samsung Electronics Co., Ltd.

- MediaTek Inc.

- ARM Holdings plc

- Imagination Technologies Limited

- Apple Inc.

- Huawei Technologies Co., Ltd.

- Lenovo Group Limited

- ASUSTeK Computer Inc.

- Micro-Star International Co., Ltd.

- Gigabyte Technology Co., Ltd.

- Acer Incorporated

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- EVGA Corporation

- Zotac Technology Limited

- Colorful Technology Company Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Adoption of Cloud Gaming and Online Esports

- 4.2.2 Rising Demand for High-Performance Computing in Data Centers

- 4.2.3 Growth of Mobile Gaming Ecosystem in Southeast Asia

- 4.2.4 Increasing Graphics Requirements for AAA PC and Console Titles

- 4.2.5 Government Incentives for Local Semiconductor Packaging and Testing

- 4.2.6 Expansion of AI-Powered Content Creation for Social Commerce

- 4.3 Market Restraints

- 4.3.1 Global GPU Supply Chain Disruptions and Chip Shortages

- 4.3.2 Rising Average Selling Prices Limiting Entry-Level Adoption

- 4.3.3 Energy Cost Sensitivity of Emerging Country Data Centers

- 4.3.4 Regulatory Scrutiny on Cryptocurrency Mining in Key Markets

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Intensity of Competitive Rivalry

- 4.8.2 Threat of New Entrants

- 4.8.3 Threat of Substitutes

- 4.8.4 Bargaining Power of Suppliers

- 4.8.5 Bargaining Power of Buyers

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Integration Type

- 5.1.1 Integrated GPUs (iGPU)

- 5.1.2 Discrete GPUs (dGPU)

- 5.2 By Device Application

- 5.2.1 Mobile Devices and Tablets

- 5.2.2 PCs and Workstations

- 5.2.3 Servers and Datacenter Accelerators

- 5.2.4 Gaming Consoles and Handhelds

- 5.2.5 Automotive / ADAS

- 5.2.6 Other Embedded and Edge Devices

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Qualcomm Technologies, Inc.

- 6.4.5 Samsung Electronics Co., Ltd.

- 6.4.6 MediaTek Inc.

- 6.4.7 ARM Holdings plc

- 6.4.8 Imagination Technologies Limited

- 6.4.9 Apple Inc.

- 6.4.10 Huawei Technologies Co., Ltd.

- 6.4.11 Lenovo Group Limited

- 6.4.12 ASUSTeK Computer Inc.

- 6.4.13 Micro-Star International Co., Ltd.

- 6.4.14 Gigabyte Technology Co., Ltd.

- 6.4.15 Acer Incorporated

- 6.4.16 Dell Technologies Inc.

- 6.4.17 Hewlett Packard Enterprise Company

- 6.4.18 EVGA Corporation

- 6.4.19 Zotac Technology Limited

- 6.4.20 Colorful Technology Company Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment