|

시장보고서

상품코드

2072784

싱가포르의 카톤 보드 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Singapore Cartonboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

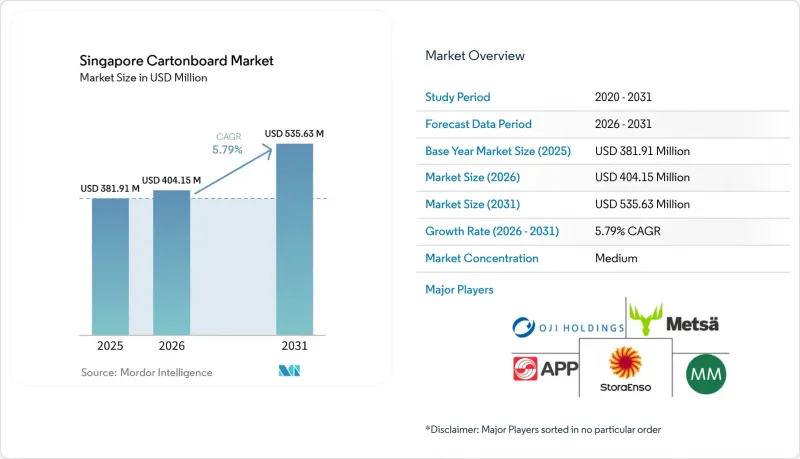

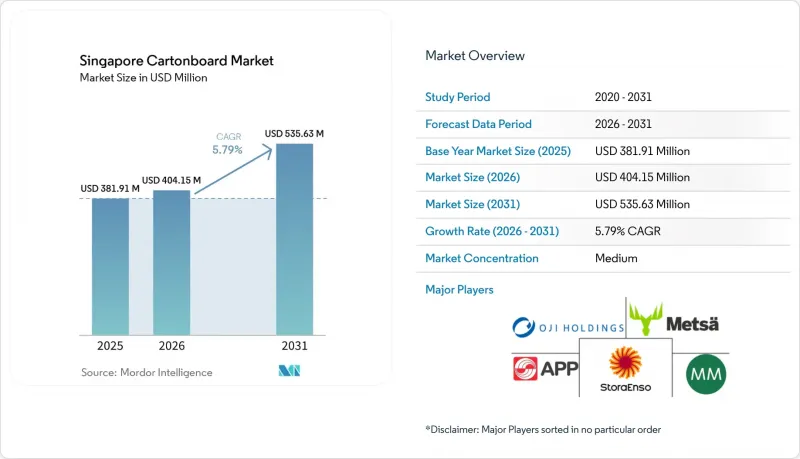

Mordor Intelligence에 의하면, 싱가포르의 카톤 보드 시장 규모는 2025년에 3억 8,191만 달러로 평가되었고, 2026년 4억 415만 달러로 추정되고, 2031년까지 5억 3,563만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 5.79%를 나타낼 전망입니다.

본 보고서는 제품 등급별(고형 표백 카톤 보드, 고형 미표백 카톤 보드, 접이식 상자용 카톤 보드, 화이트 라이닝 칩보드, 액체 포장용 카톤 보드, 푸드서비스용 카톤 보드), 포장 형태별(접이식 상자, 액체 포장, 슬리브 및 트레이 등), 그리고 최종 사용자 산업별(식품, 음료, 제약 및 헬스케어, 담배, 화장품 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

싱가포르의 카톤 보드 시장 동향 및 분석

플라스틱에서 섬유 기반 포장으로의 전환

싱가포르의 카톤 보드 시장은 규제 대상 기업들이 원자재 보고 및 감축 계획을 가시화하고 실무에 적용할 수 있도록 촉진하는 포장 규제로부터 직접적인 지원을 받고 있습니다. 싱가포르의 ‘포장 보고 의무 제도'에서는 대상 기업에 대해 포장 데이터 및 연간 3R 계획의 제출을 의무화하고 있으며, 2025년 개정 규정은 2025년 7월 1일부터 시행되었습니다. 2025년도 데이터 제출 기간은 2026년 1월부터 3월까지였기 때문에 현재의 주기에서는 포장에 관한 의사결정이 이미 더욱 엄격해진 보고 체계에 따라 이루어져야 합니다. 또한, 싱가포르에서는 2026년 4월에 '음료 용기 반환 제도'가 도입되어, 플라스틱 및 금속 음료 용기에는 0.10 싱가포르 달러(0.07 달러)의 보증금이 부과되는 반면, 종이 음료 용기는 이 부과 대상에서 제외되어, 관련 용도에서 섬유 소재의 선택을 장려하고 있습니다. 2024년 싱가포르에서 발생한 플라스틱 중 재활용된 비율은 고작 5%에 불과했지만, 플라스틱은 전체 폐기물의 14% 가까이 차지하고 있어, 공공 정책 및 기업 보고서에서 사용 후 처리에 대한 우려가 적은 대체재에 대한 관심이 높아지고 있습니다. 이러한 상황에서 싱가포르의 카톤 보드 시장은 플라스틱 대체 수요뿐만 아니라, 규정 준수 및 식품 접촉 적합성 요건으로 인해 보다 명확한 포장 형태를 필요로 하는 브랜드 소유자들이 직면한 의사결정 기간 단축이라는 이점도 누리고 있습니다.

포장 식품 및 음료 수요의 확대

싱가포르의 카톤 보드 시장은 인쇄용, 매장 진열용, 운송용, 식품 접촉용 등 다양한 유형의 포장이 필요한 식품 및 음료 산업의 기반에 힘입어 성장하고 있습니다. 2025년에도 식품은 여전히 최대의 최종 소비 부문으로, 총 수요의 38.76%를 차지했으며, 카톤 보드 소비량과 소매, 편의점, 외식 산업 등 각 유통 채널에서의 일상적인 포장 식품 유통 사이에 강한 상관관계가 있음을 보여주고 있습니다. 접이식 카톤 보드 상자는 체계화된 소매 채널 및 유통 채널을 통해 유통되는 건조 식품, 과자, 즉석 식품, 멀티팩 용도의 2차 포장재로 기능하고 있기 때문에 이러한 구조에서 여전히 핵심적인 역할을 수행하고 있습니다. 2026년 4월에 시작된 '음료 용기 반환 제도' 또한 음료 판매 분야에서 섬유 기반의 2차 포장 및 보완적인 포장 형태를 장려하는 또 하나의 정책적 신호가 되고 있습니다. 싱가포르의 카톤 보드 시장에서 이러한 수요는 단순히 수량 증가에 기인한 것에 그치지 않습니다. 제품 구성 또한 더 높은 품질의 인쇄 마감, 높은 강성, 그리고 더 신뢰할 수 있는 식품 접촉 성능을 요구하는 형태로 전환되고 있기 때문입니다. 이러한 구성의 변화로 인해, 포장 식품의 품목 확대에 비해 톤수 기준의 성장세가 완만하더라도 가공업체는 부가가치를 유지할 수 있게 됩니다.

수입 카톤 보드와 운임의 변동

싱가포르 카톤 보드 시장의 가장 큰 구조적 제약은 카톤 보드 등급용 국내 펄프 및 제지 기반 시설이 부족하다는 점입니다. 현지 가공업체들은 접이식 상자용 카톤 보드, 고형 표백 카톤 보드, 액체 포장용 카톤 보드 및 기타 등급의 제품을 수입할 수밖에 없으며, 그 결과 운송비와 공급업체의 가격 책정이 조달 비용에 직접적인 영향을 미칩니다. 이러한 의존 관계는 공급 경로가 위축되었을 때 가장 중요해집니다. 왜냐하면 싱가포르는 더 큰 규모의 지역 시장과 달리, 수요의 일부를 현지 제지 공장으로 돌릴 수 없기 때문입니다. 또한, 이러한 의존 관계로 인해 가공업체들은 유럽산 고급 등급 제품에 계속 의존하게 될 것입니다. 이러한 등급은 대체 조달처가 제한적인 의약품, 고급 식품, 화장품 분야에서 중요합니다. 이에 따라 싱가포르의 카톤 보드 시장에서는 최종 소비자 수요가 견조함에도 불구하고 이익률이 취약한 상태입니다. 가공업체는 주문을 확보하더라도, 카톤 보드의 실거래 가격이 여전히 높은 수준을 유지할 경우 수익성을 유지하는 데 어려움을 겪기 때문입니다. 이러한 영향은 고객이 가격을 꼼꼼히 비교하고, 인근 국가에서 가공된 카톤 보드를 조달할 수 있는 선택권을 가진 일반적인 사례에서 더욱 심각해집니다.

부문별 분석

2025년, 싱가포르의 카톤 보드 시장에서 접이식 상자용 카톤 보드는 34.45%의 점유율을 차지했으며, 제품 등급 중 가장 높은 점유율을 기록했습니다. 이러한 위상은 식품, 화장품, 의약품, 담배 포장 등 다양한 분야에서 활용되고 있음을 반영하고 있습니다. 선반 진열 시의 외관과 카톤 보드의 성능이 모두 중요한 용도에서 가공업체들은 뛰어난 인쇄 적합성, 강성 및 안정적인 두께를 위해 이 등급을 선호하고 있으므로, 그 중요성은 여전히 높습니다. 싱가포르의 카톤 보드 업계에서 접이식 카톤 보드는 현지 수요 동향과도 잘 부합하고 있습니다. 이는 해당 시장이 고급 소매품을 중심으로 이루어져 있으며, 마감 처리가 아름다운 2차 포장이 필요한 수입 소비재의 비중이 높기 때문입니다. 무표백 단판, 표백 단판 및 화이트 라이닝 칩보드는 각각 서로 다른 가격대와 성능을 가진 틈새 시장에서 계속해서 수요가 있으며, 특히 무표백 단판은 더 깨끗한 표면과 엄격한 인증 기준이 중시되는 의약품 및 고급 화장품 분야에서 중요한 역할을 하고 있습니다.

외식 산업용 카톤 보드 부문은 2031년까지 연평균 성장률(CAGR) 6.27%를 나타낼 것으로 예측되며, 싱가포르의 카톤 보드 시장에서 가장 두드러진 성장세를 보일 것으로 전망됩니다. 이러한 성장은 배달 중심의 식품 소비와 퀵서비스 채널에서 컵, 트레이, 제과용 포장재, 서빙용 용기의 사용 증가와 밀접한 관련이 있습니다. 스토라 엔소(Stora Enso)는 2026년 4월, 푸드서비스 및 제과 포장용 분산 코팅 접이식 상자용 카톤 보드 'Performa Natura Aqua'를 발매했습니다. 평량 범위는 195-320 g/m²이며, 이는 공급업체가 내유성 및 종이 재활용성 향상과 같은 요구 사항에 부응하기 위해 등급을 최적화하고 있음을 나타냅니다. 의약품 분야 수요도 제품 구성에 영향을 미치고 있습니다. 보건과학청(Health Sciences Authority)이 2025년에 시행한 표시 규정 개정에서는 인쇄 적합성이 향상되고 기계 판독이 가능한 코드를 통합할 수 있는 카톤의 필요성이 강조되었습니다. 이로 인해 규제 대상 용도에서 더 두꺼운 프리미엄 보드의 사용이 촉진되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the singapore cartonboard market size was valued at USD 381.91 million in 2025 and estimated to grow from USD 404.15 million in 2026 to reach USD 535.63 million by 2031, at a CAGR of 5.79% during the forecast period (2026-2031).

This report is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and More), and End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics, and More). The Market Forecasts are Provided in Terms of Value (USD).

Singapore Cartonboard Market Trends and Insights

Shift From Plastic to Fiber-Based Packaging

The Singapore cartonboard market is receiving direct support from packaging rules that make material reporting and reduction plans more visible and more operational for regulated companies. Singapore's Mandatory Packaging Reporting scheme requires covered businesses to submit packaging data and annual 3R plans, and the 2025 amendment regulations took effect on July 1, 2025. The 2025 data submission window ran from January to March 2026, meaning packaging decisions must already align with a tighter reporting structure in the current cycle. Singapore also activated its Beverage Container Return Scheme in April 2026, with a SGD 0.10 (USD 0.07) deposit on plastic and metal beverage containers, keeping paper-based beverage formats outside that levy structure and supporting fiber-based options in adjacent applications. Only 5% of the plastics generated in Singapore were recycled in 2024, while plastics accounted for nearly 14% of total waste generated, drawing attention to alternatives that create fewer end-of-life concerns in public policy and corporate reporting. In this setting, the Singapore cartonboard market is benefiting not only from substitution away from plastics, but also from the shorter decision window that brand owners now face when they need packaging formats with clearer compliance and food-contact credentials

Growth in Packaged Food and Beverage Demand

The Singapore cartonboard market is also supported by a food and beverage base that needs a broad mix of printed, shelf-ready, transport, and food-contact packaging. Food remained the largest end-user in 2025, accounting for 38.76% of total demand, underscoring the strong link between board consumption and daily packaged food distribution across retail, convenience, and foodservice channels. Folding cartons remained central to this structure because they serve secondary packaging in dry foods, confectionery, ready-to-eat products, and multipack applications that move through organized retail and delivery channels. The Beverage Container Return Scheme, which started in April 2026, also adds another policy signal in favor of fiber-based secondary and complementary packaging formats for beverage sales. Within the Singapore cartonboard market, this demand is not only volume-led, as the product mix is also moving toward formats that require better print finish, greater stiffness, and more reliable food-contact performance. That mix shift helps converters defend value even when tonnage growth is more measured than the expansion in packaged food offerings.

Imported Board and Freight Cost Volatility

The biggest structural limit on the Singapore cartonboard market is the lack of a domestic pulping or papermaking base for cartonboard grades. Local converters have to import folding boxboard, solid bleached board, liquid packaging board, and other grades, which means freight costs and supplier pricing move directly into procurement economics. That dependency matters most when supply routes tighten, because Singapore cannot shift part of its requirements to local mills as larger regional markets can. The same dependence also keeps converters exposed to premium European grades, which are important in pharmaceutical, premium food, and cosmetic applications, where alternative sourcing is limited. In the Singapore cartonboard market, this leaves margins vulnerable even when end-user demand is healthy, because converters can win orders but still struggle to protect profitability when landed board costs stay high. The effect is more severe in standard jobs where customers closely compare prices and have the option to source converted cartons from neighboring countries.

Other drivers and restraints analyzed in the detailed report include:

- Pharmaceutical and Healthcare Compliance Needs

- Premiumization in Cosmetics and Toiletries Packaging

- Competition From Lower-Cost Regional Converters

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Folding boxboard held 34.45% of the Singapore cartonboard market share in 2025, the largest among product grades, and that position reflects its wide use across food, cosmetics, pharmaceutical, and tobacco packaging. The grade remains central because converters rely on it for strong printability, stiffness, and consistent caliper in applications where shelf appearance and carton performance both matter. Within the Singapore cartonboard industry, folding boxboard also aligns well with the local demand profile, as the market has a premium retail mix and a high share of packaged imported consumer goods that require well-finished secondary packaging. Solid bleached board, solid unbleached board, and white-lined chipboard each continue to serve distinct price and performance niches, with solid bleached board particularly important in pharmaceutical and premium cosmetic uses where cleaner surfaces and strict certification standards carry more weight.

The food service board segment is projected to grow at a 6.27% CAGR through 2031, making it the fastest-growing grade in the Singapore cartonboard market. That growth is tied to rising use of cups, trays, bakery packs, and service containers in delivery-led food consumption and quick-service channels. Stora Enso launched Performa Natura Aqua in April 2026 as a dispersion-coated folding boxboard for foodservice and bakery packaging, with grammages ranging from 195 to 320 g/m2, demonstrating how suppliers are tailoring grades to meet grease resistance and improved paper recovery needs. Pharmaceutical demand is also influencing the product mix, as the Health Sciences Authority's 2025 labeling update highlighted the need for cartons with better printability and machine-readable code integration, which supports the use of higher-caliper premium board in regulated applications.

Complete Report Scope:

- By Product Grade

- Solid Bleached Board

- Solid Unbleached Board

- Folding Boxboard

- White-Lined Chipboard

- Liquid Packaging Board

- Food Service Board

- By Packaging Format

- Folding Cartons

- Liquid Packaging

- Sleeve and Tray

- Other Packaging Formats (Cups, Foodservice Containers)

- By End-User Industry

- Food

- Beverage

- Pharmaceutical and Healthcare

- Tobacco

- Cosmetics and Toiletries

- Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

List of Companies Covered in this Report:

- PT APP Purinusa Ekapersada

- Stora Enso Oyj

- Metsa Board Corporation

- Mayr-Melnhof Karton AG

- Oji Holdings Corporation

- Rengo Co., Ltd.

- Graphic Packaging International, LLC

- Smurfit Westrock plc

- Tetra Pak International S.A.

- SIG Group AG

- Elopak ASA

- Billerud Aktiebolag (publ)

- ITC Limited

- Nine Dragons Paper (Holdings) Limited

- Sappi Limited

- Sonoco Products Company

- Huhtamaki Oyj

- OVOL Singapore Pte. Ltd.

- SCG Packaging Public Company Limited

- Singapore Cartons (Pte) Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift From Plastic to Fiber-Based Packaging

- 4.2.2 Growth in Packaged Food and Beverage Demand

- 4.2.3 Pharmaceutical and Healthcare Compliance Needs

- 4.2.4 Premiumization in Cosmetics and Toiletries Packaging

- 4.2.5 Tightening Food-Contact Traceability and Import-Compliance Requirements

- 4.2.6 Short-Run SKU Proliferation and Digital Conversion Demand

- 4.3 Market Restraints

- 4.3.1 Imported Board and Freight Cost Volatility

- 4.3.2 Competition From Lower-Cost Regional Converters

- 4.3.3 Limited Domestic Recovered Fiber Availability

- 4.3.4 Migration-Testing and Food-Contact Qualification Costs

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Grade

- 5.1.1 Solid Bleached Board

- 5.1.2 Solid Unbleached Board

- 5.1.3 Folding Boxboard

- 5.1.4 White-Lined Chipboard

- 5.1.5 Liquid Packaging Board

- 5.1.6 Food Service Board

- 5.2 By Packaging Format

- 5.2.1 Folding Cartons

- 5.2.2 Liquid Packaging

- 5.2.3 Sleeve and Tray

- 5.2.4 Other Packaging Formats (Cups, Foodservice Containers)

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Tobacco

- 5.3.5 Cosmetics and Toiletries

- 5.3.6 Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 PT APP Purinusa Ekapersada

- 6.4.2 Stora Enso Oyj

- 6.4.3 Metsa Board Corporation

- 6.4.4 Mayr-Melnhof Karton AG

- 6.4.5 Oji Holdings Corporation

- 6.4.6 Rengo Co., Ltd.

- 6.4.7 Graphic Packaging International, LLC

- 6.4.8 Smurfit Westrock plc

- 6.4.9 Tetra Pak International S.A.

- 6.4.10 SIG Group AG

- 6.4.11 Elopak ASA

- 6.4.12 Billerud Aktiebolag (publ)

- 6.4.13 ITC Limited

- 6.4.14 Nine Dragons Paper (Holdings) Limited

- 6.4.15 Sappi Limited

- 6.4.16 Sonoco Products Company

- 6.4.17 Huhtamaki Oyj

- 6.4.18 OVOL Singapore Pte. Ltd.

- 6.4.19 SCG Packaging Public Company Limited

- 6.4.20 Singapore Cartons (Pte) Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment