|

시장보고서

상품코드

2073616

남미의 비료 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)South America Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

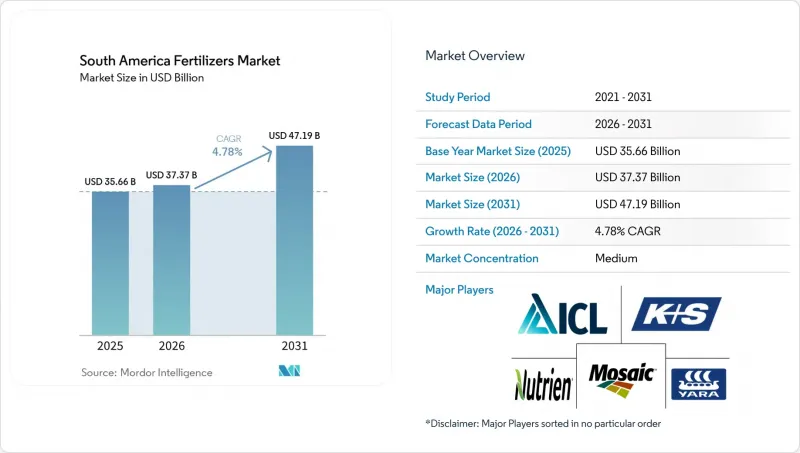

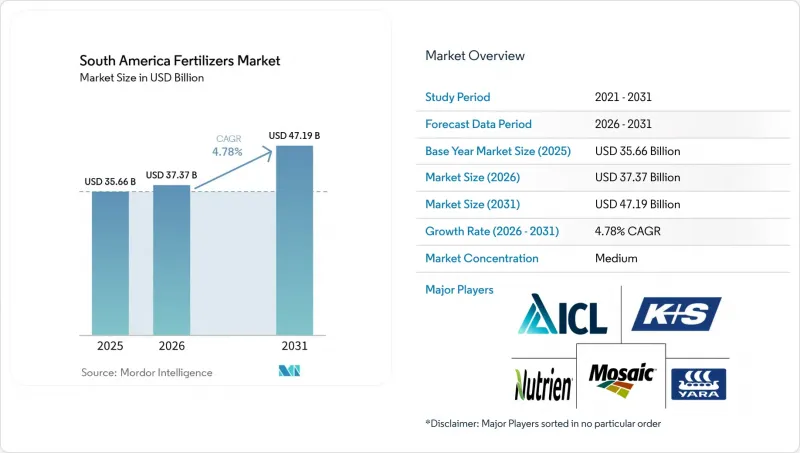

Mordor Intelligence에 의하면, 남미 비료 시장 규모는 2025년에 356억 6,000만 달러로 평가되었고 2026년 373억 7,000만 달러에서 2031년까지 471억 9,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 4.78%를 나타낼 전망입니다.

본 보고서는 유형별(복합비료 및 단일비료), 형태별(기존 및 특수형), 시비 방법별(시비 관개, 엽면 시비, 토양 시비), 작물 유형별(밭작물, 원예작물, 잔디 및 관상용 작물), 국가별(아르헨티나, 브라질, 기타 남미 국가)로 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(미터톤) 단위로 제시되어 있습니다.

남미 비료 시장 동향과 인사이트

대두 및 옥수수 재배 면적 확대

브라질에서는 2025-2026년 작기 동안 4,910만 헥타르의 대두가 재배되어 2.8% 증가했습니다. 작물 재배는 마토그로소 주와 마토피바(MATOPIBA) 프론티어 지역에 집중되어 있으며, 이 지역의 산성 세라도 토양에서는 인산 함량이 높은 스타터 비료가 필요합니다. “사플린하"라고 불리는 옥수수 이모작은 해당국의 옥수수 생산량을 늘리는 한편, 질소 추비 시기를 20일 미만으로 단축시켜 살포기를 통해 신속하게 시비할 수 있는 액체 요소·질산암모늄 혼합 비료에 대한 수요를 촉진하고 있습니다. 이모작 전략으로 인해 물류 일정이 촉박해지면서, 작물 전환을 신속하게 뒷받침할 수 있는 즉시 입수 가능한 비료에 대한 수요가 증가하고 있습니다. “사프리냐”로 알려진 이모작 옥수수는 브라질의 총 옥수수 생산량에서 큰 비중을 차지하고 있습니다. 2월부터 3월까지의 파종 기간에 따라, 질소 추가 시비 기간은 18일로 제한됩니다. 이에 따라, 입상 비료를 살포하는 방법보다 살포기를 이용해 신속하게 시비할 수 있는 액체 요소·질산암모늄 혼합액 수요가 증가하고 있습니다.

정밀 농업 및 특수 자재의 도입

Sentinel-2 및 Planet의 위성 이미지를 기반으로 한 가변 시비 기술을 통해, 2025년에는 브라질의 대두 및 옥수수 재배에서 요소 사용량이 14% 감소했으며, 동시에 수확량은 기존 수준을 유지했습니다. 이러한 양분 이용 효율의 향상으로 인해, 살포기나 점적 관개 시스템을 통해 정확하게 계량할 수 있는 수용성, 억제제 강화형 및 코팅형 제제로 제품 선호도가 이동하고 있습니다. 사탕수수 실험에서 폴리머 코팅 요소 덕분에 질소의 이용 가능 기간이 90일로 연장되어 두 번의 시비 작업이 필요 없어졌으며, 1헥타르당 28달러의 연료비와 인건비가 절감되었습니다. 남미 비료 시장 전반에서 생산자들이 투입 자재 비용 절감과 지속가능성 지표 달성을 추구하는 가운데, 정밀 농업 도구의 등장으로 특수 자재가 틈새 시장에서 주류로 자리 잡아가고 있습니다.

영양염 유출 및 온실가스(GHG)에 관한 규제 강화

브라질의 수역으로의 방류 규제를 정한 CONAMA 결의 제430/2011호는 질소 및 기타 오염 물질에 대해 더 엄격한 기준을 마련했습니다. 결의 제357/2005호를 개정 및 보완하는 이 규정은 지표수 및 지하수 자원의 오염을 줄이기 위해, 사탕수수와 쌀 생산자를 포함한 산업 및 농업 사업자에게 보다 엄격한 영양염 배출 제한을 준수할 것을 의무화하고 있습니다. 이 규제는 수질 및 수질이 생태계와 공중보건에 미치는 영향에 대한 우려가 커지는 상황에 대응하기 위한 것입니다. 규제 비용 증가는 초기 가격 프리미엄을 상쇄할 수 있는 신용 인센티브가 없다면 소규모 농가들의 특수 자재 도입을 저해할 가능성이 있습니다. 이러한 조치들은 환경에 미치는 영향을 최소화하면서, 규정 준수 요건을 충족하기 위한 지속 가능한 관행 및 기술의 도입을 촉진할 것으로 예측됩니다.

부문별 분석

2025년, 남미 비료 시장 점유율의 89.4%를 차지한 최대 부문은 단일 성분 비료였습니다. 이는 생산자가 노동력을 절약할 수 있는 ‘원패스”솔루션을 찾고 있기 때문입니다. 농가들로부터, 특히 마토그로소 주의 대규모 대두 밭에서 복합비료(NPK) 제품을 사용함으로써 노동력이 30-40% 절감되고, 시비 오류가 감소했다는 보고가 접수되고 있습니다. 또한, 정밀 농업의 실천을 통해 지역 토양에서 아연, 붕소, 망간의 결핍이 광범위하게 확인됨에 따라, 미량 영양소 첨가제는 꾸준한 성장을 이루고 있습니다. 세라 드 살리트로 시설에서 국내 인산염 생산이 시작됨에 따라, 일암모늄인산염(MAP) 및 이암모늄인산염(DAP)의 현지 공급이 강화되고 있습니다. 한편, 칼륨의 경우 여전히 수입 의존도가 높은 상황이 이어지고 있습니다. 유황과 칼슘 결핍이 증가하고 있는 점도 조달 목록에서 2차 주요 영양소의 중요성을 높이고 있으며, 이로 인해 남미 비료 시장의 영양소 기반이 확대되고 있습니다.

복합비료는 가장 빠르게 성장하고 있는 부문으로, 2031년까지 연평균 성장률(CAGR) 7.8%를 기록하며 성장하고 있습니다. 이는 여러 영양소가 부족한 토양이 세라두 지역을 넘어 MATOPIBA의 새로운 개척지로 확산되고 있는 데다, 비료 혼합 업체들이 철도와 연계된 허브를 활용하여 현지 토양 분석 결과를 바탕으로 NPK 배합을 맞춤화하고 있기 때문입니다. 이러한 접근 방식 덕분에 지역 내 운송비와 보관 비용을 절감할 수 있게 되었습니다. 농가들은 단순히 가격 비교에 중점을 두는 것에서 벗어나 프로그램 전체의 경제성을 평가하는 방향으로 전환하고 있으며, 기후 스트레스 상황에서 균형 잡힌 배합 비료가 수확량의 안정성과 양분 이용 효율 향상에 도움이 된다는 점을 인식하고 있습니다. 한편, 단일 성분 비료도 발전하고 있어, 요소 제조업체는 코팅형 제품을 출시하고 있으며, 인산염 공급업체는 미량 영양소를 첨가하고 있습니다. 이러한 동향에 따라, 두 부문은 남미 비료 시장에서 계속해서 중요한 위치를 차지할 것으로 확실시되고 있습니다.

2025년 기준으로 남미 비료 시장 규모의 92.8%를 차지하는 최대 부문은 기존 비료였습니다. 이러한 압도적인 시장 점유율은 농업 현장에서의 광범위한 활용, 높은 비용 대비 효과, 그리고 다양한 작물의 영양 요구를 충족시키는 능력에서 기인합니다. 기존 비료의 높은 보급률은 해당 지역 전체의 농업 생산성을 뒷받침하는 데 있어, 이러한 비료가 수행하는 지극히 중요한 역할을 여실히 보여주고 있습니다.

특수 비료 부문은 가장 빠르게 성장하고 있으며, 2031년까지 연평균 성장률(CAGR) 6.0%로 확대되고 있습니다. 방출 조절 비료(CRF)는 생육기 내내 작물에 영양분을 공급하는 일회 시비 시스템으로 주목받고 있으며, 이를 통해 많은 노동력이 필요한 여러 차례의 시비 필요성을 줄이고 있습니다. 액체 비료 및 수용성 비료는 가변 시비율 시비 시스템의 도입에 힘입어, 관개가 이루어지는 과수 재배 지역이나 온실 재배 분야에서 성장을 거듭하고 있습니다. 폴리머 코팅 요소는 해당 지역의 질소 시장에서 상당한 점유율을 차지하고 있으며, 특히 사탕수수 재배의 경우 90일간의 영양분 방출 주기가 작물의 영양분 흡수 주기와 일치하기 때문에 생육기 중반에 추가 시비를 할 필요가 없습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 개 보고서의 내용

제3장 주요 요약 및 주요 조사 결과

제4장 주요 업계 동향

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 비료 업계 CEO가 직면하는 중요 전략적 과제

JHS 26.07.09According to Mordor Intelligence, the south america fertilizers market size was valued at USD 35.66 billion in 2025 and estimated to grow from USD 37.37 billion in 2026 to reach USD 47.19 billion by 2031, at a CAGR of 4.78% during the forecast period (2026-2031).

This report is Segmented by Type (Complex and Straight), by Form (Conventional and Specialty), by Application Mode (Fertigation, Foliar, and Soil), by Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental), and by Country (Argentina, Brazil, and the Rest of South America). The Market Forecasts are Provided in Terms of Value (USD ) and Volume (Metric Tons)

South America Fertilizers Market Trends and Insights

Rising Soybean and Corn Acreage Expansion

Brazil planted 49.1 million ha of soybeans in the 2025-2026 crop year, a 2.8% rise, concentrated in Mato Grosso and the MATOPIBA frontier, where acidic cerrado soils require high phosphate starters. Safrinha corn production increases the country's corn output and compresses the nitrogen top-dress window to fewer than 20 days, stimulating demand for liquid urea-ammonium-nitrate blends that sprayers can deliver quickly. Double-cropping strategies tighten logistics calendars and increase the premium on readily available fertilizers that support rapid crop transitions. Second-crop corn, known as safrinha, accounts for a significant share of Brazil's total corn production. Its planting window, from February to March, limits the top-dress nitrogen application period to 18 days. This has increased demand for liquid urea-ammonium-nitrate solutions, which can be applied more quickly with spray rigs than with granular broadcast methods.

Adoption of Precision Farming and Specialty Inputs

Variable-rate technology guided by Sentinel-2 and Planet imagery cut urea use by 14% of Brazilian soybean and corn in 2025 while keeping yields flat. The gain in nutrient-use efficiency shifts product preference toward water-soluble, inhibitor-enhanced, and coated formulations that sprayers and drip systems meter precisely. Polymer-coated urea extended nitrogen availability to 90 days in sugarcane trials, eliminating the need for two application passes and saving USD 28 per ha in fuel and labor. Across the South America fertilizer market, precision tools are moving specialty inputs from niche to mainstream as growers chase input savings and sustainability metrics.

Stricter Nutrient-Runoff and Greenhouse Gas (GHG) Regulations

Resolution 430/2011 of CONAMA, which regulates the discharge of effluents into receiving water bodies in Brazil, established stricter standards for nitrogen and other pollutants. This regulation, which modifies and supplements Resolution 357/2005, mandates that industries and agricultural operations, including sugarcane and rice producers, adhere to tighter nutrient discharge limits to reduce pollution in surface and groundwater resources. The regulation aims to address the growing concerns over water quality and its impact on ecosystems and public health. Increased regulatory costs could hinder the adoption of specialty inputs by smallholders unless credit incentives help offset the initial price premium. These measures are projected to encourage the adoption of sustainable practices and technologies to meet compliance requirements while minimizing environmental impact.

Other drivers and restraints analyzed in the detailed report include:

- Brazil National Fertilizer Plan 2050 Implementation

- Emergence of Green-Ammonia Production Capacity

- Agronomy Talent Shortage Slowing Tech Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Straight was the largest segment, accounting for 89.4% of South America fertilizers market share in 2025, as growers seek single-pass solutions that save labor. Farmers have reported labor savings of 30-40% and reduced application errors when using complex NPK products, particularly in large-scale soybean fields in Mato Grosso. Additionally, micronutrient additives are experiencing steady growth driven by precision farming practices that have identified widespread deficiencies in zinc, boron, and manganese in regional soils. The commencement of domestic phosphate production at the Serra do Salitre facility is bolstering the local supply of monoammonium phosphate (MAP) and diammonium phosphate (DAP). Potash continues to rely heavily on imports. Increasing deficiencies in sulfur and calcium are also elevating the importance of secondary macronutrients on procurement lists, thereby expanding the nutrient base of the South America fertilizers market.

Complex is the fastest-growing segment, advancing at an 7.8% CAGR through 2031, as multi-deficiency soils expand beyond the Cerrado into new MATOPIBA frontiers, fertilizer blenders are utilizing rail-linked hubs to customize NPK formulations based on localized soil analyses. This approach helps reduce regional freight and storage costs. Farmers are transitioning from focusing solely on price comparisons to evaluating total-program economics, acknowledging the benefits of balanced blends in improving yield stability and nutrient-use efficiency under climate stress. Meanwhile, straight grades are evolving, with urea producers introducing coated variants and phosphate suppliers adding micronutrient enrichments. These developments ensure that both segments remain significant in South America fertilizer market.

Conventional fertilizers were the largest segment, accounting for 92.8% share of the South America fertilizers market size in 2025. This dominance can be attributed to their widespread use in agricultural practices, cost-effectiveness, and the ability to meet the nutrient requirements of various crops. The high adoption rate of conventional fertilizers highlights their critical role in supporting agricultural productivity across the region.

The specialty segment is the fastest-growing, advancing at a 6.0% CAGR through 2031. Controlled-release fertilizers (CRF) are gaining prominence as a single-application system that provides nutrients to crops throughout the growing season, thereby reducing the need for multiple labor-intensive applications. Liquid and water-soluble fertilizers are experiencing growth in irrigated fruit-growing regions and greenhouse operations, supported by the adoption of variable-rate fertigation systems. Polymer-coated urea holds a notable share of the regional nitrogen market, particularly in sugarcane cultivation, where its 90-day nutrient release cycle aligns with the crop's nutrient uptake, eliminating the need for additional mid-season applications.

Complete Report Scope:

- By Type

- Complex

- Straight

- Micronutrients

- Boron

- Copper

- Iron

- Manganese

- Molybdenum

- Zinc

- Others

- Nitrogenous

- Urea

- Others

- Phosphatic

- Di-ammonium Phosphate (DAP)

- Monoammonium phosphate (MAP)

- Single Super Phosphate (SSP)

- Triple Superphosphate (TSP)

- Potassic

- Muriate of Potassium (MoP)

- Sulphate of Potash (SoP)

- Others

- Secondary Macronutrients

- Calcium

- Magnesium

- Sulfur

- Micronutrients

- By Form

- Conventional

- Speciality

- Controlled Release Fertilizers (CRF)

- Liquid Fertilizer

- Slow-release fertilizers (SRF)

- Water Soluble

- By Application Mode

- Fertigation

- Foliar

- Soil

- By Crop Type

- Field Crops

- Horticultural Crops

- Turf and Ornamental

- By Geography

- Argentina

- Brazil

- Rest of South America

List of Companies Covered in this Report:

- Coromandel International Limited

- EuroChem Group AG

- COMPO EXPERT GmbH

- Haifa Group

- Kingenta Ecological Engineering Group Co., Ltd.

- Koch Fertilizer LLC

- Nutrien Ltd.

- Sociedad Quimica y Minera de Chile S.A.

- The Mosaic Company

- Yara International ASA

- ICL Group Ltd.

- K+S Aktiengesellschaft

- Indian Farmers Fertiliser Cooperative Ltd.

- Omex Agriculture Ltd.

- Agro-Culture Liquid Fertilizers LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped for Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Rising soybean and corn acreage expansion

- 4.6.2 Government credit programs boosting affordability

- 4.6.3 Adoption of precision farming and specialty inputs

- 4.6.4 Brazil National Fertilizer Plan 2050 implementation

- 4.6.5 Emergence of green ammonia production capacity

- 4.6.6 AI-enabled variable-rate advisory services

- 4.7 Market Restraints

- 4.7.1 Volatility in natural-gas and potash prices

- 4.7.2 Stricter nutrient-runoff and Greenhouse Gas (GHG) regulations

- 4.7.3 Freight bottlenecks via the Panama Canal and the Red Sea

- 4.7.4 Agronomy talent shortage is slowing tech adoption

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Type

- 5.1.1 Complex

- 5.1.2 Straight

- 5.1.2.1 Micronutrients

- 5.1.2.1.1 Boron

- 5.1.2.1.2 Copper

- 5.1.2.1.3 Iron

- 5.1.2.1.4 Manganese

- 5.1.2.1.5 Molybdenum

- 5.1.2.1.6 Zinc

- 5.1.2.1.7 Others

- 5.1.2.2 Nitrogenous

- 5.1.2.2.1 Urea

- 5.1.2.2.2 Others

- 5.1.2.3 Phosphatic

- 5.1.2.3.1 Di-ammonium Phosphate (DAP)

- 5.1.2.3.2 Monoammonium phosphate (MAP)

- 5.1.2.3.3 Single Super Phosphate (SSP)

- 5.1.2.3.4 Triple Superphosphate (TSP)

- 5.1.2.4 Potassic

- 5.1.2.4.1 Muriate of Potassium (MoP)

- 5.1.2.4.2 Sulphate of Potash (SoP)

- 5.1.2.4.3 Others

- 5.1.2.5 Secondary Macronutrients

- 5.1.2.5.1 Calcium

- 5.1.2.5.2 Magnesium

- 5.1.2.5.3 Sulfur

- 5.1.2.1 Micronutrients

- 5.2 By Form

- 5.2.1 Conventional

- 5.2.2 Speciality

- 5.2.2.1 Controlled Release Fertilizers (CRF)

- 5.2.2.2 Liquid Fertilizer

- 5.2.2.3 Slow-release fertilizers (SRF)

- 5.2.2.4 Water Soluble

- 5.3 By Application Mode

- 5.3.1 Fertigation

- 5.3.2 Foliar

- 5.3.3 Soil

- 5.4 By Crop Type

- 5.4.1 Field Crops

- 5.4.2 Horticultural Crops

- 5.4.3 Turf and Ornamental

- 5.5 By Geography

- 5.5.1 Argentina

- 5.5.2 Brazil

- 5.5.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Landscape

- 6.5 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.5.1 Coromandel International Limited

- 6.5.2 EuroChem Group AG

- 6.5.3 COMPO EXPERT GmbH

- 6.5.4 Haifa Group

- 6.5.5 Kingenta Ecological Engineering Group Co., Ltd.

- 6.5.6 Koch Fertilizer LLC

- 6.5.7 Nutrien Ltd.

- 6.5.8 Sociedad Quimica y Minera de Chile S.A.

- 6.5.9 The Mosaic Company

- 6.5.10 Yara International ASA

- 6.5.11 ICL Group Ltd.

- 6.5.12 K+S Aktiengesellschaft

- 6.5.13 Indian Farmers Fertiliser Cooperative Ltd.

- 6.5.14 Omex Agriculture Ltd.

- 6.5.15 Agro-Culture Liquid Fertilizers LLC