|

시장보고서

상품코드

2038793

식품 물류 시장 : 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Food Logistics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

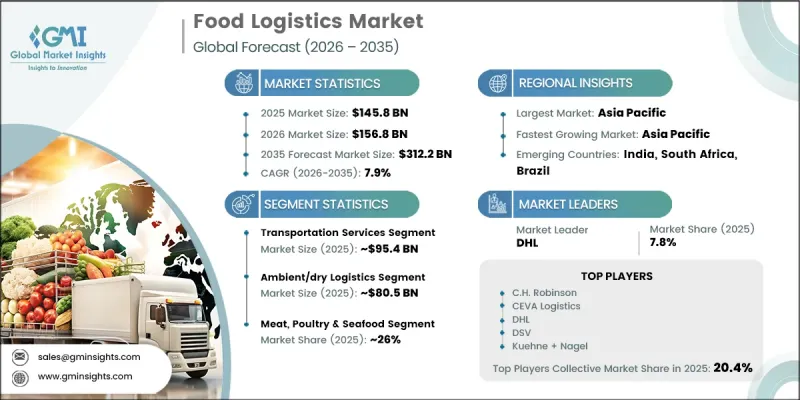

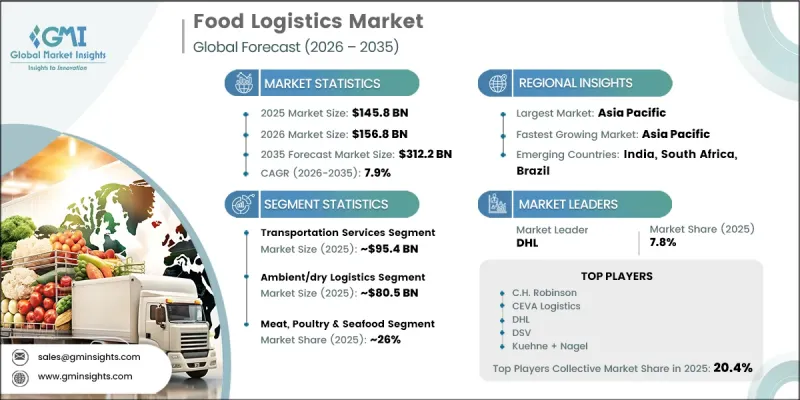

세계의 식품 물류 시장은 2025년에 1,458억 달러로 평가되었고, CAGR 7.9%로 성장할 전망이며, 2035년까지 3,122억 달러에 이를 것으로 예측됩니다.

시장 성장은 인구 증가와 식습관 변화에 따른 세계 식품 소비 패턴의 확대에 의해 주도되고 있습니다. 도시화의 진전, 가처분 소득 증가, 라이프스타일의 변화로 인해 효율적인 식품 공급망 시스템에 대한 수요가 증가하고 있습니다. 광범위하고 복잡해지는 유통망 전체에서 식품의 품질을 유지해야 할 필요성 때문에 첨단 물류 인프라에 대한 관심이 높아지고 있습니다. 콜드체인 물류는 운송 및 보관의 전 과정에서 온도에 민감한 상품을 보존하는 데 필수적인 역할을 하기 때문에 중요한 성장 분야로 부상하고 있습니다. 국제 무역의 확대는 신선식품과 비신선식품을 취급할 수 있는 안정적이고 확장 가능한 물류 솔루션에 대한 수요를 더욱 가속화시키고 있습니다. 그러나 개발도상국의 인프라 격차는 여전히 문제로 남아 있으며, 현대적 보관 및 운송 시스템에 대한 투자 확대를 촉구하고 있습니다. 정부와 이해관계자들은 효율성 향상과 폐기물 감소를 위해 물류 역량 향상을 적극 지원하고 있습니다. 전 세계 식품 수요가 지속적으로 증가함에 따라 통합 기술을 활용한 물류 시스템의 중요성은 전 세계 식품 안전, 공급 보장 및 유통 효율성을 보장하는 데 있어 점점 더 핵심적인 역할을 하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 1,458억 달러 |

| 예측 시장 규모 | 3,122억 달러 |

| CAGR | 7.9% |

2025년에는 운송 서비스 부문이 65.4%의 점유율을 차지했으며, 954억 달러 시장 규모를 창출했습니다. 이 부문은 전체 공급망에서 식품의 적시적이고 안전한 이동을 보장하는 데 매우 중요한 역할을 하기 때문에 식품 물류의 중추적인 역할을 담당하고 있습니다. 생산기지와 최종 시장 간의 안정적인 연계를 통해 신선식품과 비신선식품의 효율적인 유통을 지원하고 있습니다. 식품의 신속하고 통제된 배송에 대한 수요가 증가함에 따라 제품 품질을 유지하고 전체 공급망에서 손실을 최소화하는 데 있어 이 부문의 중요성이 더욱 커지고 있습니다.

상온-건조 물류 부문은 2025년 55.2%의 점유율을 차지했으며, 시장 규모는 805억 달러에 달했습니다. 이 부문은 온도 관리 환경을 필요로 하지 않는 비신선한 식품의 대규모 운송으로 인해 시장을 주도하고 있습니다. 비용 효율성, 간소화된 보관 요건 및 확립된 유통 네트워크는 광범위한 보급에 기여하고 있습니다. 인프라의 복잡성을 최소화하면서 대량의 화물을 처리할 수 있는 능력으로 인해 이 부문은 세계 식품 물류 생태계의 기반이 되어 다양한 식품 카테고리의 안정적인 수요를 뒷받침하고 있습니다.

미국의 식품 물류 시장은 2025년 408억 달러에 달했으며, 2026-2035년 연평균 7.6%의 성장률을 보일 것으로 예측됩니다. 시장 확대는 연방정부 차원에서 시행되고 있는 엄격한 식품 안전, 추적성 및 운송 표준의 영향을 크게 받고 있습니다. 규제 프레임워크는 공급망 전반의 투명성을 높이고 오염 위험을 줄이기 위해 고안되었습니다. 이러한 컴플라이언스 요건은 특히 온도 관리가 필요한 식품이나 위험도가 높은 식품 카테고리에서 첨단 물류 방식을 도입하여 업계 전반의 안전성과 업무 효율성을 향상시키고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 서비스별(2022-2035년)

제6장 시장 추산 및 예측 : 온도 요건별(2022-2035년)

제7장 시장 추산 및 예측 : 식품 카테고리별(2022-2035년)

제8장 시장 추산 및 예측 : 최종 용도별(2022-2035년)

제9장 시장 추산 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

AJY 26.06.11The Global Food Logistics Market was valued at USD 145.8 billion in 2025 and is estimated to grow at a CAGR of 7.9% to reach USD 312.2 billion by 2035.

Market growth is driven by rising global food consumption patterns linked to population expansion and shifting dietary preferences. Increasing urbanization, higher disposable incomes, and evolving lifestyles are intensifying demand for efficient food supply chain systems. The need to maintain food quality across extended and more complex distribution networks is placing greater emphasis on advanced logistics infrastructure. Cold chain logistics is emerging as a critical growth area due to its essential role in preserving temperature-sensitive goods throughout transport and storage. Expanding international trade is further accelerating the requirement for reliable and scalable logistics solutions capable of handling perishable and non-perishable food items. However, infrastructure gaps in developing economies continue to pose challenges, prompting increased investments in modern storage and transportation systems. Governments and industry stakeholders are actively supporting upgrades in logistics capabilities to improve efficiency and reduce waste. As global food demand continues to rise, the importance of integrated, technology-enabled logistics systems is becoming increasingly central to ensuring food safety, availability, and distribution efficiency worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $145.8 Billion |

| Forecast Value | $312.2 Billion |

| CAGR | 7.9% |

The transportation services segment accounted for 65.4% share in 2025, generating USD 95.4 billion. This segment remains the backbone of food logistics due to its critical role in ensuring timely and secure movement of food products across supply chains. It supports the efficient distribution of perishable and non-perishable goods by enabling reliable connectivity between production centers and end markets. The growing need for fast and controlled delivery of food items continues to reinforce the importance of this segment in maintaining product integrity and minimizing losses across the supply chain.

The ambient and dry logistics segment held 55.2% share in 2025, valued at USD 80.5 billion. This segment leads the market due to the large-scale movement of non-perishable food products that do not require temperature-controlled environments. Its cost efficiency, simplified storage requirements, and well-established distribution networks contribute to its widespread adoption. The ability to handle high-volume shipments with minimal infrastructure complexity makes this segment a fundamental part of the global food logistics ecosystem, supporting consistent demand across various food categories.

U.S. Food Logistics Market reached USD 40.8 billion in 2025 and is projected to grow at a CAGR of 7.6% between 2026 and 2035. Market expansion is strongly influenced by stringent food safety, traceability, and transportation standards enforced at the federal level. Regulatory frameworks are designed to enhance transparency and reduce contamination risks throughout the supply chain. These compliance requirements have increased the adoption of advanced logistics practices, particularly for temperature-sensitive and high-risk food categories, ensuring improved safety and operational efficiency across the industry.

Key players operating in the Global Food Logistics Market include DHL, Maersk, C.H. Robinson, CEVA Logistics, DSV, GEODIS, Kuehne + Nagel, Lineage Logistics, Nippon Express, and XPO Logistics. Companies in the Food Logistics Market are focusing on strengthening supply chain efficiency, expanding cold chain capabilities, and adopting advanced digital technologies to improve operational performance. Investments in automation, real-time tracking systems, and data-driven logistics platforms are enhancing visibility and control across distribution networks. Firms are also prioritizing infrastructure development, particularly in temperature-controlled storage and transportation, to support growing demand for perishable goods. Strategic partnerships and global network expansion are enabling companies to improve service coverage and market reach. Additionally, businesses are emphasizing sustainability initiatives and energy-efficient logistics solutions to align with evolving environmental standards while maintaining cost efficiency and service reliability.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Service

- 2.2.3 Temperature Requirement

- 2.2.4 Food Category

- 2.2.5 End Use

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 E-commerce & online grocery growth

- 3.2.1.2 Rising food safety & traceability requirements

- 3.2.1.3 Expansion of cold chain infrastructure in emerging markets

- 3.2.1.4 Consumer demand for fresh & perishable products

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Fragmented regulatory landscape

- 3.2.2.2 Energy costs & cold chain operating expenses

- 3.2.3 Market opportunities

- 3.2.3.1 Technology integration (IoT, Blockchain, AI)

- 3.2.3.2 Sustainability-driven logistics solutions

- 3.2.3.3 Emerging market penetration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. - Food and Drug Administration (FDA)

- 3.4.1.2 U.S. - United States Department of Agriculture (USDA)

- 3.4.1.3 Canada - Canadian Food Inspection Agency (CFIA)

- 3.4.2 Europe

- 3.4.2.1 Germany - Federal Office of Consumer Protection and Food Safety (BVL)

- 3.4.2.2 EU - European Food Safety Authority (EFSA)

- 3.4.3 Asia Pacific

- 3.4.3.1 China - Ministry of Agriculture and Rural Affairs (MARA)

- 3.4.3.2 India - FSSAI

- 3.4.4 Latin America

- 3.4.4.1 Mexico - SADER (Secretaria de Agricultura y Desarrollo Rural)

- 3.4.4.2 Mexico - COFEPRIS

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE - Ministry of Climate Change and Environment (MOCCAE)

- 3.4.5.2 South Africa - Department of Health

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technologies

- 3.7.1.1 Refrigerated Trucks & Containers

- 3.7.1.2 Warehouse Management Systems (WMS)

- 3.7.1.3 Barcode & RFID Tracking

- 3.7.2 Emerging technologies

- 3.7.2.1 Autonomous Delivery Vehicles & Drones

- 3.7.2.2 Digital Twin Technology in Supply Chains

- 3.7.2.3 AI & Predictive Analytics

- 3.7.1 Current technologies

- 3.8 Patent landscape (Driven by Primary Research)

- 3.9 Cost breakdown analysis

- 3.9.1 Transportation costs

- 3.9.2 Storage & warehousing costs

- 3.9.3 Packaging & handling costs

- 3.9.4 Technology & monitoring costs

- 3.9.5 Regulatory compliance & safety costs

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly Initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Trade Data Analysis (Driven by Paid Database)

- 3.11.1 Import/Export Volume & Value Trends

- 3.11.2 Key Trade Corridors & Tariff Impact

- 3.12 Impact of AI & Generative AI on the Market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 GenAI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Cross-border operations and international partnerships

- 3.13.1 International trade and customs compliance

- 3.13.2 International partner selection and evaluation

- 3.13.3 Cross-border risk management

- 3.13.4 Multimodal transportation & infrastructure coordination

- 3.14 Infrastructure & cold chain capabilities

- 3.14.1 Global cold storage capacity distribution

- 3.14.2 Refrigerated fleet & transport infrastructure

- 3.14.3 Temperature monitoring & quality control systems

- 3.15 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.15.1 Base Case - key macro & industry variables driving CAGR

- 3.15.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Service, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Transportation services

- 5.2.1 Roadways

- 5.2.1.1 Full truck load (FTL)

- 5.2.1.2 Less than truck load (LTL)

- 5.2.2 Seaways

- 5.2.2.1 Full container load (FCL)

- 5.2.2.2 Less than container load (LCL)

- 5.2.3 Railways

- 5.2.4 Airways

- 5.2.1 Roadways

- 5.3 Warehousing & storage services

- 5.4 Value-added services

- 5.5 Freight forwarding & brokerage

- 5.5.1 Third-Party Logistics (3PL)

- 5.5.2 Fourth-Party Logistics (4PL)

- 5.5.3 In-house / Direct Distribution

Chapter 6 Market Estimates & Forecast, By Temperature Requirement, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Frozen/cold chain

- 6.3 Chilled/refrigerated logistics

- 6.4 Ambient/dry logistics

Chapter 7 Market Estimates & Forecast, By Food Category, 2022 - 2035 ($Mn, 000, tons)

- 7.1 Key trends

- 7.2 Fruits & vegetables

- 7.3 Meat, Poultry & Seafood

- 7.4 Dairy Products

- 7.5 Bakery & Confectionery

- 7.6 Frozen Foods

- 7.7 Dry/Packaged Foods

- 7.8 Beverages

Chapter 8 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Mn, 000, tons)

- 8.1 Key trends

- 8.2 Food manufacturers

- 8.3 Food retailers

- 8.3.1 Supermarkets & hypermarkets

- 8.3.2 Convenience stores

- 8.3.3 Specialty food stores

- 8.4 Food service operators

- 8.5 E-commerce & direct-to-consumer

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, 000, tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Poland

- 9.3.7 Netherlands

- 9.3.8 Norway

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Singapore

- 9.4.7 Malaysia

- 9.4.8 Indonesia

- 9.4.9 Vietnam

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Colombia

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 DHL

- 10.1.2 Kuehne + Nagel

- 10.1.3 DSV

- 10.1.4 C.H. Robinson

- 10.1.5 XPO Logistics

- 10.1.6 Nippon Express

- 10.1.7 CEVA Logistics

- 10.1.8 Kerry Logistics

- 10.1.9 Lineage Logistics

- 10.1.10 Maersk

- 10.1.11 FedEx

- 10.1.12 UPS

- 10.1.13 GEODIS

- 10.2 Regional players

- 10.2.1 DACHSER

- 10.2.2 Gist

- 10.2.3 Nichirei Logistics

- 10.2.4 Snowman Logistics

- 10.3 Emerging players

- 10.3.1 Zipline

- 10.3.2 ColdStar Logistics

- 10.3.3 STEF