|

시장보고서

상품코드

2073433

식품 콜드체인 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Food Cold Chain - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

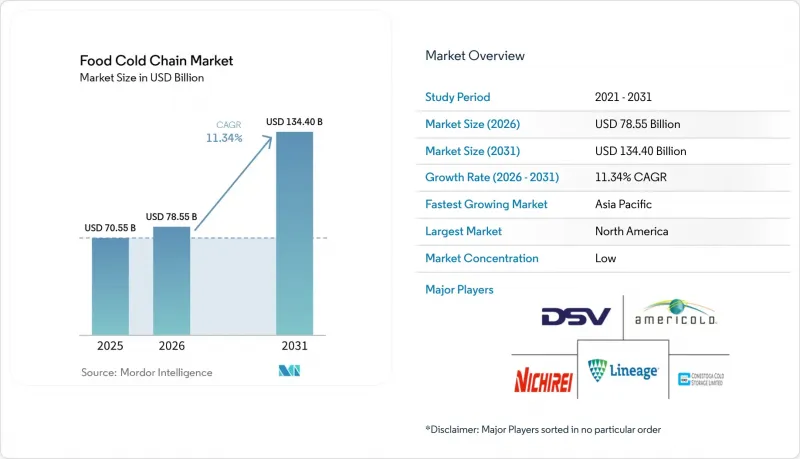

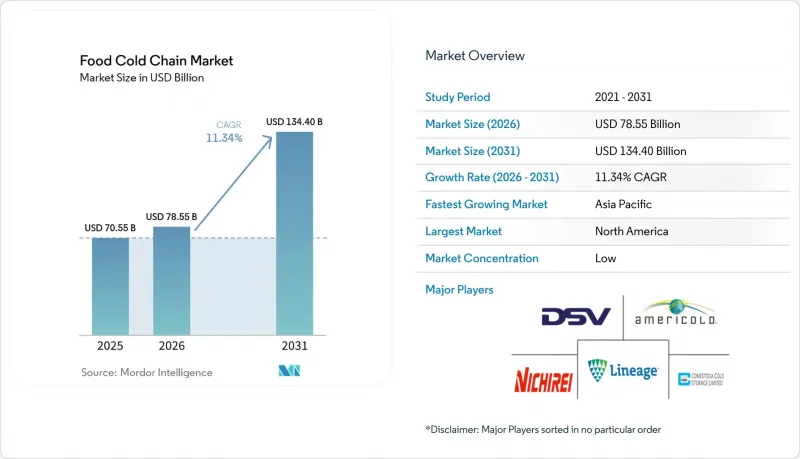

Mordor Intelligence에 의하면, 식품 콜드체인 시장 규모는 2025년 705억 5,000만 달러로 평가되었습니다. 2026년에는 785억 5,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 11.34%로 성장을 지속하여, 2031년에는 1,344억 달러에 이를 것으로 예측됩니다.

본 보고서에서는 업계를 “유형"(콜드체인 보관 등)", “온도 범위"(냉장(0-4°C) 등), “운송 수단"(육상 - 냉장 트럭 및 트레일러, 해상 - 냉장 컨테이너 등), 용도(과일 및 채소, 육류·수산물 등), 기술(RFID 및 실시간 모니터링 등), 지역별로 분류하고 있습니다.) 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 식품 콜드체인 시장 동향 및 인사이트

전 세계적으로 냉동식품 및 신선식품에 대한 수요가 증가하고 있습니다.

냉동식품 소비 증가로 인해 전 세계적으로 콜드체인 용량 요건이 변화하고 있으며, 특히 창고, 운송, 유통 네트워크에 큰 영향을 미치고 있습니다. 이러한 성장에 따라 수급 격차를 해소하기 위한 냉장 창고 인프라에 대한 수요가 증가하면서, 냉장 창고, 온도 관리 차량 및 첨단 모니터링 시스템에 대한 막대한 투자가 이루어지고 있습니다. 팬데믹 기간 동안 소비자의 행동 변화로 인해 냉동식품은 단순한 편의성 상품에서 필수품으로 변모했으며, 레토르트 식품, 채소, 육류, 수산물 등 전체 카테고리에서 구매가 증가했습니다. 이로 인해, 지속적인 인프라 확장이 필요한 장기적인 수요 패턴이 확립되었습니다. 콜드체인 사업자들은 생산 시설에서 물류 센터, 소매점에 이르는 공급망 전반에 걸쳐 일관된 온도 관리를 유지하는 것이 필수적이라고 강조하고 있습니다. 온도 변동은 제품 손실이나 식품 안전성 저하를 초래하고, 막대한 비용이 드는 리콜을 유발하며, 규제 위반으로 이어질 가능성이 있기 때문입니다. 온도 관리의 복잡성은 라스트 마일 배송에도 미치며, 제품의 품질을 유지하기 위해서는 전용 설비와 정밀한 모니터링 절차가 필요합니다.

국제 식품 무역과 국경을 넘는 식품 운송의 성장

국경을 넘는 식품 운송은 온도 관리가 이루어지는 정교하게 조정된 물류 시스템으로 진화하고 있습니다. 중국 상무부는 현대 상업 유통 시스템 강화 계획의 일환으로, 2027년까지 과일 및 채소의 콜드체인 유통 비율을 25%, 육류의 경우 45%로 끌어올리겠다는 목표를 세웠습니다. 이러한 규제 조치는 특히 기후 변화와 지정학적 긴장이 기존공급망을 교란시키고 있는 상황에서 식량 안보에 있어 국제 무역이 수행하는 중요한 역할을 반영하고 있습니다. 여러 관할 구역에 걸쳐 적절한 온도 관리를 유지하는 데 따르는 복잡성은 다양한 규제 요건을 충족하면서 제품의 품질을 보장할 수 있는 전문 물류 업체에게 새로운 비즈니스 기회를 창출하고 있습니다. 블록체인 기술과 IoT 센서의 통합은 수입국이 요구하는 종단 간 추적성을 제공하기 위해 필수적이며, 국경을 넘는 식품 무역을 단순한 물류상의 과제에서 기술을 활용한 경쟁 우위로 변화시키고 있습니다. 온도 관리가 이루어지는 컨테이너 운송은 중요한 병목 현상으로 대두되고 있으며, 첨단 감시·제어 시스템을 갖춘 전용 냉동 컨테이너의 경우 운임이 상대적으로 높게 책정되어 있습니다.

냉장 창고 시설 및 냉장 운송 차량에 대한 막대한 초기 투자 요건

콜드체인 인프라의 자본 집약성은 시장 진입에 있어 큰 장벽이 되고 있습니다. 전용 건축자재나 에너지 효율이 높은 설계에는 막대한 비용이 소요되며, 그 비용은 기존 창고에 비해 300-400%나 더 높을 수 있습니다. 냉장 시설 건설에는 고도의 단열 시스템, 특수 바닥재, 그리고 극한의 온도 조건에서도 확실하게 가동되어야 하는 첨단 냉동 설비가 필요하며, 이로 인해 초기 투자 비용과 지속적인 유지 관리 비용 모두 증가하고 있습니다. 냉장 운송 차량 역시 유사한 비용 압박에 직면해 있으며, 냉장 트럭 및 트레일러의 경우 설비 확충을 정당화하기 위해 두 자릿수 운임 인상이 필요해졌습니다. 자금 조달의 과제는 콜드체인 자산의 특수성으로 인해 더욱 복잡해지고 있습니다. 이러한 자산은 대체 용도가 제한적이며, 전문적인 유지보수 노하우가 필요하기 때문입니다.

부문별 분석

2025년에는 콜드체인 보관이 55.21%로 가장 큰 시장 점유율을 차지했으며, 이는 모든 식품 카테고리에 걸친 온도 관리 물류에 대한 기본적인 인프라 요건을 반영했습니다. 이 부문이 지배적인 위치를 차지하는 배경에는 냉장 창고의 자본 집약적인 특성이 있습니다. 고도의 단열, 자동 랙 시스템, 에너지 효율이 높은 냉각 기술을 갖춘 전문 시설이 콜드체인 생태계에서 가장 큰 비용 요인으로 작용하기 때문입니다.

모니터링 장비는 절대적인 시장 점유율은 작지만, FSMA 204와 같은 규제 요건 및 IoT 기반 온도 추적 시스템의 고도화에 힘입어 2031년까지 연평균 성장률(CAGR) 14.2%라는 가장 빠른 성장 궤도를 보이고 있습니다. 모니터링 장비 부문의 급속한 성장은 수동적인 온도 기록이 장비 고장을 예측하고 에너지 소비를 최적화할 수 있는 실시간 예측 분석 시스템으로 점차 대체되고 있다는 기술적 전환점을 반영하고 있습니다. Rivercity Innovations와 같은 기업은 압축기 고장을 예측하는 ‘조기 중대 고장 감지(ECFD)" 기능을 갖춘 IoT 자동 온도 모니터링 솔루션을 도입하여, 이를 통해 적시에 유지보수를 수행할 수 있게 되어 고액의 제품 손실을 방지할 수 있습니다.

냉장 온도대(0-4°C)는 2025년에 59.62%의 점유율을 차지했으며 시장을 계속 주도하고 있습니다. 이는 신선식품, 유제품, 조리식품 등 신선식품 소비의 대부분을 차지하는 품목에서 이 온도대가 폭넓게 적용되고 있음을 반영합니다. 한편, 냉동 부문(-18°C)은 냉동 가공 식품에 대한 소비자의 선호도 변화와 전 세계 냉동 식품 생산 능력 확대에 힘입어, 2031년까지 연평균 성장률(CAGR)이 15.18%에 달하며 뛰어난 성장세를 보이고 있습니다.

냉동 부문의 성장세를 바탕으로, 주요 소매업체들은 동일한 시설 내에서 냉장 제품과 냉동 제품을 모두 효율적으로 관리할 수 있는 이중 온도 시설에 대한 투자를 확대하고 있으며, 이를 통해 공간 활용 효율을 최적화하고 업무의 복잡성을 줄이고 있습니다. 에미레이트 스카이카고 및 기타 주요 물류 업체들이 지원하는 ‘-15°C로 이동"연합은 표준 온도를 -18°C에서 -15°C로 조정함으로써 냉동 식품의 운송을 최적화하려는 업계 전반의 노력으로, 제품의 품질을 유지하면서 에너지 소비를 줄일 수 있는 가능성이 있습니다. 이 노력은 온도 범위를 최적화함으로써 식품 안전 기준을 유지하면서도 운영 비용과 환경에 미치는 영향을 줄임으로써, 어떻게 경쟁 우위를 확보할 수 있는지를 보여주고 있습니다.

지역별 분석

2025년 북미 시장 점유율 40.10%는 수십 년에 걸친 인프라 투자와 규제 정비의 결과로, 세계에서 가장 정교한 콜드체인 생태계가 구축되었음을 반영했습니다. 그러나 해당 지역은 현재 구식 시설이 전자상거래 수요와 지속가능성 요건을 충분히 충족하지 못하고 있어 현대화 과제에 직면해 있습니다. 대형 소매업체들은 자동화 시설에 대한 전략적 투자를 통해 이에 대응하고 있으며, 그 대표적인 사례로 월마트와 크로거가 운송 거리를 단축하고 지속가능성 지표를 개선하기 위해 도심형 냉장 창고를 개발하고 있다는 점을 들 수 있습니다. 이 지역은 확립된 규제 체계와 품질 보증을 위해 다소 높은 가격을 기꺼이 지불하려는 소비자들의 의지라는 이점을 누리고 있지만, 인프라 노후화와 현대적인 운영 요건을 충족하기 위한 막대한 설비 투자 필요성이라는 역풍에도 직면해 있습니다.

아시아태평양의 콜드체인 시장은 2031년까지 연평균 성장률(CAGR) 16.21%를 나타낼 것으로 예측되며, 이는 세계 최고 수준의 성장률입니다. 이러한 성장은 주로 식품 폐기물 감축과 공급망 효율화를 목표로 한 정부의 지원 정책에 힘입어 이루어지고 있습니다. 중국, 인도, 인도네시아 등 여러 국가에서 급속한 도시화가 진행됨에 따라, 온도 조절이 가능한 보관 및 운송 서비스에 대한 수요가 증가하고 있습니다. 인도에서는 “프라단 만트리 키산 삼파다 요자나(Pradhan Mantri Kisan Sampada Yojana)"에 따르면, 2025년 2월 기준으로 394건의 콜드체인 프로젝트가 승인되었습니다. 이러한 프로젝트들은 냉장 운송, 냉장 창고, 가공 센터 등을 포함하는 통합형 콜드체인 시설 구축에 중점을 두고 있습니다. 이 사업은 신선식품의 보관 상태를 개선하고, 수확 후 손실을 줄이며, 식품 안전 기준을 확보함으로써 지속적으로 성장하고 있는 인도의 식품 가공 산업을 지원하기 위한 것입니다. 또한, 이 프로그램은 콜드체인 인프라 개발에 대한 민간 부문의 투자를 촉진하여, 보다 견고하고 효율적인 식품 유통 시스템 구축에 기여하고 있습니다.

유럽에서는 엄격한 식품 안전 규제, 국경을 넘는 무역의 원활화, 그리고 대륙 전체의 콜드체인 운영을 변화시키고 있는 지속가능성 노력에 힘입어 꾸준한 성장을 이어가고 있습니다. 이 지역에서 지속가능성에 대한 노력은 배출 가스 제로 냉장 트레일러와 에너지 소비 및 운영 효율을 최적화하는 실시간 데이터 관리를 위한 디지털 트윈 시스템을 포함한 첨단 디지털화 기술의 도입을 가속화하고 있습니다. 해당 지역의 성숙한 규제 환경과 신선하고 현지에서 생산된 식품을 선호하는 소비자들의 기호로 인해, 제품의 품질을 유지하면서도 환경에 미치는 영향을 최소화할 수 있는 첨단 콜드체인 솔루션에 대한 수요가 계속해서 증가하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.08According to Mordor Intelligence, the food cold chain market size is expected to grow from USD 70.55 billion in 2025 to USD 78.55 billion in 2026 and is forecast to reach USD 134.4 billion by 2031 at 11.34% CAGR over 2026-2031.

This report Segments the Industry Into Type (Cold-Chain Storage, and More), Temperature Range (Chilled (0-4 °C), and More), Transport Mode (Road - Reefer Trucks and Trailers, Sea - Reefer Containers, and More), Application (Fruits and Vegetables, Meat and Seafood, and More), Technology (RFID and Real-Time Monitoring, and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Food Cold Chain Market Trends and Insights

Rising Demand for Frozen and Perishable Food Products Globally

The increase in frozen food consumption has changed cold chain capacity requirements globally, with particular impact on warehousing, transportation, and distribution networks. This growth has created high demand for cold storage infrastructure to address supply-demand gaps, leading to significant investments in refrigerated warehouses, temperature-controlled vehicles, and advanced monitoring systems. Consumer behavior changes during the pandemic transformed frozen foods from convenience items to essential products, driving increased purchases across categories including ready meals, vegetables, meat, and seafood, thereby establishing long-term demand patterns that necessitate permanent infrastructure expansion. Cold chain operators emphasize that maintaining consistent temperature controls throughout the supply chain is essential, from production facilities through distribution centers to retail locations, as temperature variations can cause product losses, compromise food safety, trigger costly recalls, and result in regulatory non-compliance. The complexity of temperature management extends to last-mile delivery, where maintaining product integrity requires specialized equipment and precise monitoring protocols.

Growth in International Food Trade and Cross-Border Food Transportation

Cross-border food transportation has evolved into a sophisticated orchestration of temperature-controlled logistics, with China's Ministry of Commerce targeting 25% cold chain circulation rates for fruits and vegetables and 45% for meat by 2027 under its modern commercial circulation system enhancement plan . This regulatory push reflects the critical role of international trade in food security, particularly as climate change and geopolitical tensions disrupt traditional supply chains. The complexity of maintaining temperature integrity across multiple jurisdictions has created opportunities for specialized logistics providers who can navigate varying regulatory requirements while ensuring product quality. The integration of blockchain technology and IoT sensors has become essential for providing end-to-end traceability required by importing countries, transforming cross-border food trade from a logistics challenge into a technology-enabled competitive advantage. Temperature-controlled container shipping has emerged as a critical bottleneck, with specialized reefer containers commanding premium rates due to their sophisticated monitoring and control systems.

High Initial Capital Investment Requirements for Cold Storage Facilities and Refrigerated Transport Vehicles

The capital intensity of cold chain infrastructure creates significant barriers to entry, with specialized construction materials and energy-efficient designs commanding premium costs that can exceed conventional warehousing by 300-400%. The construction of cold facilities requires sophisticated insulation systems, specialized flooring, and advanced refrigeration equipment that must operate reliably in extreme temperature conditions, driving up both initial investment and ongoing maintenance costs. Refrigerated transport vehicles face similar cost pressures, with reefer trucks and trailers requiring double-digit rate increases to justify equipment expansion. The financing challenge is compounded by the specialized nature of cold chain assets, which have limited alternative uses and require specialized maintenance expertise.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Consumer Preference for Fresh and Ready-to-Eat Convenience Foods

- Expansion of Organized Retail and Food Service Sectors

- Competition from Alternative Preservation Methods

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cold-chain storage commands the largest market share at 55.21% in 2025, reflecting the fundamental infrastructure requirements for temperature-controlled logistics across all food categories. The segment's dominance stems from the capital-intensive nature of refrigerated warehousing, where specialized facilities with advanced insulation, automated racking systems, and energy-efficient cooling technologies represent the largest cost component in the cold chain ecosystem.

Monitoring components, despite representing a smaller absolute market share, exhibit the fastest growth trajectory at 14.2% CAGR through 2031, driven by regulatory mandates such as FSMA 204 and the increasing sophistication of IoT-enabled temperature tracking systems. The monitoring components segment's rapid expansion reflects a technological inflection point where passive temperature logging is being replaced by real-time, predictive analytics systems that can anticipate equipment failures and optimize energy consumption. Companies like Rivercity Innovations have introduced IoT automated temperature monitoring solutions featuring Early Catastrophic Failure Detection (ECFD) capabilities that predict compressor failures, allowing for timely maintenance and preventing costly product losses.

The chilled temperature range (0-4°C) maintains market leadership with a 59.62% share in 2025, reflecting the broad applicability of this temperature zone across fresh produce, dairy products, and prepared foods that constitute the majority of perishable food consumption. However, the frozen segment (-18°C) demonstrates superior growth momentum with a 15.18% CAGR through 2031, driven by changing consumer preferences toward frozen convenience foods and the expansion of frozen food manufacturing capacity globally.

The frozen segment's growth trajectory has prompted major retailers to invest in dual-temperature facilities that can efficiently manage both chilled and frozen products within the same operation, optimizing space utilization and reducing operational complexity. The Move to -15°C coalition, supported by Emirates SkyCargo and other major logistics providers, represents an industry-wide effort to optimize frozen food transportation by adjusting standard temperatures from -18°C to -15°C, potentially reducing energy consumption while maintaining product quality. This initiative demonstrates how temperature range optimization can create competitive advantages through reduced operational costs and environmental impact, while maintaining food safety standards.

Complete Report Scope:

- By Type

- Cold-chain Storage

- Cold-chain Transport

- Monitoring Components

- By Temperature Range

- Chilled (0-4 °C)

- Frozen (-18 °C)

- Deep-Frozen/Ultra-low (<-40 °C)

- By Transport Mode

- Road - Reefer Trucks and Trailers

- Sea - Reefer Containers

- Rail - Refrigerated Railcars

- Air Cargo

- By Application

- Fruits and Vegetables

- Meat and Seafood

- Dairy and Frozen Dessert

- Bakery and Confectionery

- Ready-to-Eat Meals

- Other Applications

- By Technology

- RFID and Real-time Monitoring

- IoT-Enabled Telematics

- Automated Storage and Retrieval Systems

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East and Africa

- North America

Geography Analysis

North America's 40.10% market share in 2025 reflects decades of infrastructure investment and regulatory development that created the world's most sophisticated cold chain ecosystem, yet the region now confronts modernization challenges as legacy facilities struggle with e-commerce demands and sustainability requirements. Major retailers are responding with strategic investments in automated facilities, exemplified by Walmart and Kroger's development of urban-centric cold storage facilities that reduce transportation distances and improve sustainability metrics. The region benefits from established regulatory frameworks and consumer willingness to pay premium prices for quality assurance, yet faces headwinds from aging infrastructure and the need for substantial capital investment to meet modern operational requirements.

The Asia-Pacific cold chain market is projected to grow at a CAGR of 16.21% through 2031, representing the highest growth rate globally. This expansion is primarily driven by supportive government policies aimed at reducing food waste and improving supply chain efficiency. The rapid urbanization across countries like China, India, and Indonesia has increased demand for temperature-controlled storage and transportation services. In India, the Pradhan Mantri Kisan Sampada Yojana has approved 394 cold chain projects as of February 2025. These projects focus on establishing integrated cold chain facilities, including refrigerated transportation, cold storage units, and processing centers. The initiative supports India's expanding food processing industry by enabling better preservation of perishable goods, reducing post-harvest losses, and ensuring food safety standards. The program also promotes private sector investment in cold chain infrastructure development, creating a more robust and efficient food distribution system.

Europe maintains steady growth supported by stringent food safety regulations, cross-border trade facilitation, and sustainability initiatives that are reshaping cold chain operations across the continent. The region's focus on sustainability has accelerated the adoption of emission-free refrigerated trailers and advanced digitalization technologies, including digital twin systems for real-time data management that optimize energy consumption and operational efficiency. The region's mature regulatory environment and consumer preferences for fresh, locally sourced foods continue to drive demand for sophisticated cold chain solutions that can maintain product quality while minimizing environmental impact.

- Lineage, Inc.

- Americold Logistics, Inc.

- Nichirei Corporation

- DSV A/S

- Conestoga Cold Storage Limited

- STEF

- RLS Logistics

- NewCold Cooperatief UA

- Burris Logistics

- Congebec Logistics Inc.

- John Swire & Sons (H.K.) Limited

- Frialsa Frigorificos S.A. de C.V.

- XPO, Inc

- China COSCO Shipping Corporation Limited

- A.P. Moller - Marsk A/S

- Gateway Distriparks Limited

- SCGJWD Logistics Public Company Limited

- Florida Freezer LP

- DP World

- Raben Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for frozen and perishable food products globally

- 4.2.2 Growth in international food trade and cross-border food transportation

- 4.2.3 Increasing consumer preference for fresh and ready-to-eat convenience foods

- 4.2.4 Expansion of organized retail and food service sectors

- 4.2.5 Technological advancements in refrigeration and temperature monitoring systems

- 4.2.6 Implementation of strict food safety regulations and quality standards

- 4.3 Market Restraints

- 4.3.1 High initial capital investment requirements for cold storage facilities and refrigerated transport vehicles

- 4.3.2 Power-supply volatility in emerging markets

- 4.3.3 Temperature control challenges during transportation and storage transitions

- 4.3.4 Competition from alternative preservation methods

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Cold-chain Storage

- 5.1.2 Cold-chain Transport

- 5.1.3 Monitoring Components

- 5.2 By Temperature Range

- 5.2.1 Chilled (0-4 °C)

- 5.2.2 Frozen (-18 °C)

- 5.2.3 Deep-Frozen/Ultra-low (<-40 °C)

- 5.3 By Transport Mode

- 5.3.1 Road - Reefer Trucks and Trailers

- 5.3.2 Sea - Reefer Containers

- 5.3.3 Rail - Refrigerated Railcars

- 5.3.4 Air Cargo

- 5.4 By Application

- 5.4.1 Fruits and Vegetables

- 5.4.2 Meat and Seafood

- 5.4.3 Dairy and Frozen Dessert

- 5.4.4 Bakery and Confectionery

- 5.4.5 Ready-to-Eat Meals

- 5.4.6 Other Applications

- 5.5 By Technology

- 5.5.1 RFID and Real-time Monitoring

- 5.5.2 IoT-Enabled Telematics

- 5.5.3 Automated Storage and Retrieval Systems

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.1.4 Rest of North America

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 Italy

- 5.6.2.4 France

- 5.6.2.5 Spain

- 5.6.2.6 Netherlands

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 United Arab Emirates

- 5.6.5.4 Rest of Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Lineage, Inc.

- 6.4.2 Americold Logistics, Inc.

- 6.4.3 Nichirei Corporation

- 6.4.4 DSV A/S

- 6.4.5 Conestoga Cold Storage Limited

- 6.4.6 STEF

- 6.4.7 RLS Logistics

- 6.4.8 NewCold Cooperatief UA

- 6.4.9 Burris Logistics

- 6.4.10 Congebec Logistics Inc.

- 6.4.11 John Swire & Sons (H.K.) Limited

- 6.4.12 Frialsa Frigorificos S.A. de C.V.

- 6.4.13 XPO, Inc

- 6.4.14 China COSCO Shipping Corporation Limited

- 6.4.15 A.P. Moller - Marsk A/S

- 6.4.16 Gateway Distriparks Limited

- 6.4.17 SCGJWD Logistics Public Company Limited

- 6.4.18 Florida Freezer LP

- 6.4.19 DP World

- 6.4.20 Raben Group