|

시장보고서

상품코드

2062023

아시아태평양의 식품 물류 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Asia-Pacific Food Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

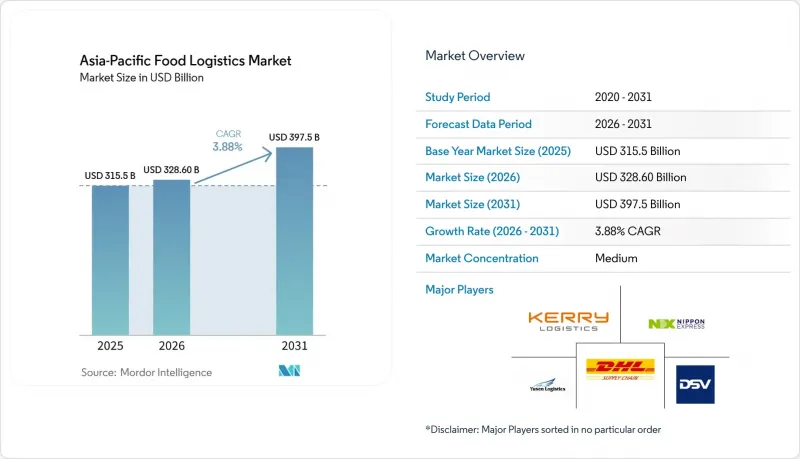

Mordor Intelligence에 의하면, 아시아태평양 식품 물류 시장 규모는 2025년 3,155억 달러에서 2026년에는 3,286억 달러로 확대되어 2031년까지 3,975억 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 3.88%로 성장할 전망입니다.

본 보고서는 서비스별(운송, 창고, 부가가치 서비스), 온도 관리 유형별(콜드체인, 비콜드체인), 최종 제품 카테고리별(육류·수산물, 유제품, 과일 및 채소, 식품 및 음료, 기타), 지역별(중국, 일본, 인도, 한국, 호주, 동남아시아, 기타 아시아태평양)으로 분류되어 있습니다. 시장 전망은 금액(달러)으로 제시되어 있습니다.

아시아태평양 식품 물류 시장 동향과 인사이트

외국 투자와 물류 현대화

베트남의 국가 로드맵에서는 물류를 경제의 기반이 되는 분야로 규정하고, 농산물의 냉장 보관을 우선 과제로 삼고 있으며, 청정 에너지를 활용한 친환경 물류에 장기적인 초점을 맞추어 농업·식품 밸류체인을 지원하고 있습니다. 싱가포르의 ‘푸드서비스 산업 디지털 계획’에서는 AI를 활용한 서류 대조 및 물류 컨트롤 타워 도입 절차를 제시하고 있으며, 이는 중소기업이 온도 관리가 이루어지는 물류 흐름을 더 높은 가시성과 보안 수준으로 관리하는 데 도움이 됩니다. 동시에, 해당 분야의 기술 역량과 사이버 보안 수요를 조화시키는 것 또한 목표로 하고 있습니다. 중국의 부처 간 통합 계획에 따르면, 2027년까지 대기업 경영 관리의 80%를 디지털화하고 주요 프로세스의 75%를 디지털 제어하는 것을 목표로 하고 있으며, 실증 프로젝트와 대표적인 적용 사례를 통해 이를 뒷받침하고 있어, 이러한 움직임이 물류 업무로까지 확산되고 있습니다. 이러한 국가 프로그램들은 아시아태평양의 식품 물류 시장 전반에 걸쳐 온도 원격 모니터링, 안전한 데이터 교환, 창고 자동화에 대한 투자를 위한 일관된 방향을 제시하고 있습니다. 이러한 현대화 노력은 선진적인 허브와 자금 조달에 어려움을 겪고 있는 소규모 사업자들이 있는 신흥 회랑 간의 역량 격차를 줄이는 데에도 기여할 것입니다. 도입이 확대됨에 따라 서비스에 대한 기대치는 감사 가능한 콜드체인 기록 및 통합된 예외 처리를 포함하게 되었으며, 이를 통해 온도 관리가 필요한 국경 간 운송에 대한 구매자의 신뢰가 강화되고 있습니다.

전자상거래와 퀵커머스의 급성장

온라인 식료품 및 배달 플랫폼의 급속한 확산으로 인해 배송 시간대가 단축되면서, 단거리 냉장 배송이 중요시되고 있습니다. 싱가포르에서는 2023년부터 2030년까지 전자상거래 규모가 두 배로 증가할 것으로 예상되며, 신선식품 콜드체인 시장도 2034년까지 두 배로 성장할 것으로 전망됩니다. 이로 인해 재수출 활동이 활발한 수입 거점에서는 견고한 냉장·냉동 보관 능력의 필요성이 더욱 커지고 있습니다. 디지털 컨트롤 타워와 자동 발주 시스템을 통해 조달, 생산, 유통 간의 연계가 개선되어, 아시아태평양 식품 물류 시장 전반에 걸쳐 좁은 배송 시간대 내에서의 신뢰성을 뒷받침하고 있습니다. 또한 2028년까지 항공 화물 운송 능력 증가와 지역 게이트웨이의 콜드체인 기능 확충이 크로스보더 전자상거래의 성장을 뒷받침하고 있어, 시간적 제약이 엄격한 식품이 더 높은 서비스 수준으로 소비자에게 전달되고 있습니다. 퀵 커머스 모델은 네트워크 설계를 혁신하고 있습니다. 사업자는 인구 밀집 도시 지역의 3km 배송 반경을 커버하기 위해 마이크로 풀필먼트 센터에 냉장·냉동 재고를 미리 비치해 두고 있습니다. 이러한 변화로 인해 아시아태평양의 식품 물류 시장에서 온도 관리, 가시성, 라스트 마일 배송을 단일 서비스 계층에서 통합적으로 조정할 수 있는 공급업체가 유리한 입지를 점하고 있습니다.

분산된 콜드체인 인프라

인도의 콜드체인은 신선 식품 수요의 극히 일부만을 감당하고 있으며, 대량 보관 능력의 약 4분의 3은 다양한 원예 작물을 수용할 수 없는 단일 품목(감자) 전용 시설에 집중되어 있습니다. 농장의 예냉 장치나 포장 시설 등의 설비가 부족하여, 농산물이 정식 물류망에 진입하기 전에 열 스트레스가 가중되고, 성수기 동안 손실 위험이 높아지고 있습니다. 많은 구형 시설은 비효율적인 시스템과 불충분한 단열에 의존하고 있어, 전력 공급이 제한되는 지역에서는 에너지 소비량이 증가하고 정밀한 온도 관리 능력을 유지하기 어렵습니다. 태국에서는 농업 물자의 운송이 여전히 도로 운송이 주류를 이루고 있으며, 철도나 내륙 수운과 같은 대안은 충분히 활용되지 못하고 있습니다. 그 결과, 국제적인 기준과 비교했을 때 물류 비용이 높은 수준을 유지하고 있어, 장거리 노선에서 온도 변동 위험이 커지고 있습니다. 통합된 네트워크의 부재와 운송 능력의 불균형으로 인해, 수출업체들은 ‘퍼스트 마일(수거)’, 간선 운송, 보관, 국경 통과 등 각 단계에서 여러 업체를 조합하여 이용할 수밖에 없습니다. 이러한 수작업 전달이 반복되면서 체류 시간과 온도 관련 위험이 모두 증가하여, 아시아태평양 식품 물류 시장에서 품질 확보를 저해하고 있습니다.

부문별 분석

2025년 기준, 아시아태평양 식품 물류 시장 점유율의 61.34%를 운송 부문이 차지하고 있으며, 부가가치 서비스 및 기타 물류 솔루션은 2031년까지 연평균 성장률(CAGR) 5.41%로 확대될 것으로 전망됩니다. 태국에서는 톤킬로당 비용 면에서 우위를 점하고 있음에도 불구하고 철도가 충분히 활용되지 못하고 있어, 농산물 운송의 대부분은 도로 운송에 의존하고 있으며, 빈번하고 소량으로 이루어지는 보충 운송에는 유연한 라스트 마일 운송 수단에 대한 의존이 계속되고 있습니다. 인도에서는 ICD 캄푸르와 문드라 항구를 연결하는 전용 냉장 특급 서비스가 2026년 3월에 시작되었습니다. 이를 통해 보다 엄격한 온도 관리와 장거리 국내 운송 시 연료비 절감을 실현하는 철도 회랑이 마련되어, 신뢰성 높은 수출 인계가 가능해집니다. 옴니채널 물류 운영을 지원하기 위해 물류 센터의 거점 확충이 진행되고 있으며, 지역 허브에는 온도 조절이 가능한 공간이 마련되어 지역 내 및 국경을 넘는 유통을 위한 다양한 품목의 물류 흐름 확장에 대응하고 있습니다. 부가가치 솔루션은 현재 예냉, 소분, 라벨 부착, 자동화된 서류 확인을 결합하여 인계 횟수를 줄이고 가시성을 높이고 있으며, 이는 아시아태평양 식품 물류 시장에서 통합 콜드체인 관리에 대한 구매자의 기대에 부응하는 것입니다. ISO 9001 및 ISO 22000과 같은 인증은 다국적 바이어들에게 일반적인 전제조건으로 자리 잡고 있으며, 이에 따라 공급업체는 품질 절차를 공식적으로 수립하고 모든 서비스 분야에 걸쳐 철저한 문서 관리를 유지해야 합니다.

항공 화물은 신속한 국제 운송이 필요한 고가 신선 식품을 취급하며, DHL의 ‘항공 화물 콜드체인 네트워크’ 확장과 같은 네트워크 업그레이드를 통해 GDP(적정 보관 및 배송 기준)를 준수하는 30개 이상의 허브가 아시아를 대상으로 하는 추가 노선으로 연결되어 있습니다. 2028년까지 지역 항공 화물량이 증가할 것으로 예상되며, 이에 따라 신선·냉장 제품의 국경 간 운송 주기가 단축될 것으로 기대됩니다. 해상 운송 경로는 여전히 벌크 화물 운송에서 핵심적인 역할을 하고 있으며, 2025년 초 홍콩으로의 식음료 수입량은 해상 운송에 대한 수요가 안정적임을 입증하고 있습니다. 아세안 통관 환적 시스템(ASEAN Transit System)에 따라 국경 간 트럭 운송이 개선됨에 따라, 쿠네 나겔(Kuehne Nagel)은 전자상거래 및 첨단 제품에 대한 수요에 대응하고 비용과 국경 체류 시간을 줄이기 위해 태국에서 견인차와 컨테이너를 증강했습니다. 싱가포르에서 추진되고 있는 디지털 컨트롤 타워를 통해 경로 및 온도 관리를 실시간으로 수행할 수 있게 됨에 따라, 예외 처리 건수가 감소하고 아시아태평양 식품 물류 시장에서 화주의 규정 준수 대응 체제가 강화될 것입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the asia-Pacific food logistics market size is expected to increase from USD 315.5 billion in 2025 to USD 328.60 billion in 2026 and reach USD 397.5 billion by 2031, growing at a CAGR of 3.88% over 2026-2031.

This report is Segmented by Services (Transportation, Warehousing, and Value-Added Services), by Temperature-Control Type (Cold Chain, Non Cold Chain), by End-Product Category (Meat & Seafood, Dairy, Fruits & Vegetables, Food and Beverages, and Others), and by Geography (China, Japan, India, South Korea, Australia, Southeast Asia, and Rest of Asia-Pacific). Market Forecasts are Provided in Value (USD).

Asia-Pacific Food Logistics Market Trends and Insights

Foreign Investment and Logistics Modernization

Vietnam's national roadmap elevates logistics to a foundational economic sector and prioritizes cold storage for agricultural outputs, with a long-term focus on green logistics that uses clean energy to support the agri-food value chain. Singapore's Food Services Industry Digital Plan provides adoption tracks for AI-enabled document reconciliation and logistics control towers that help SMEs manage temperature-controlled flows with higher visibility and security, while aligning skills and cybersecurity needs for the sector. China's cross-ministry plan targets 80% digitalization for business management and 75% digital control over key processes in large food enterprises by 2027, backed by demonstration projects and typical application scenarios that cascade into logistics operations. These national programs set a consistent direction for investment in temperature telemetry, secure data exchanges, and warehouse automation across the Asia-Pacific food logistics market. The push to modernize also narrows capability gaps between advanced hubs and emerging corridors where smaller operators face financing constraints. As uptake increases, service expectations now include auditable cold chain records and integrated exception handling that reinforce buyer confidence in temperature-sensitive movements across borders.

E-commerce and Quick Commerce Boom

Rapid adoption of online grocery and meal platforms is compressing delivery windows and placing a premium on short-radius cold distribution. In Singapore, e-commerce is projected to double between 2023 and 2030, and the cold chain perishables market is expected to double by 2034, reinforcing the need for robust chilled and frozen capacity in importer hubs with significant re-export activity. Digital control towers and automated ordering are improving coordination between procurement, production, and distribution to support reliability at narrow delivery intervals across the Asia-Pacific food logistics market. Cross-border e-commerce growth also benefits from rising air cargo capacity and expanded cool-chain capability at regional gateways through 2028, helping time-sensitive food products reach consumers with higher service levels. Quick commerce models are changing network design as operators pre-position chilled and frozen inventory in micro-fulfillment centers to meet three-kilometer delivery radii in dense urban areas. These shifts reward integrated providers that can orchestrate temperature, visibility, and last-mile handoffs in one service layer across the Asia-Pacific food logistics market.

Fragmented Cold Chain Infrastructure

India's cold chain supports only a small portion of the fresh produce needs, and roughly three-quarters of the bulk storage capacity is concentrated in single-commodity potato facilities that cannot flex for diversified horticulture. Sparse assets at the farmgate, such as pre-cooling units and packhouses, increase thermal stress before produce enters formal networks and raise the risk of losses during peak seasons. Many older facilities rely on inefficient systems and poor insulation, which heighten energy intensity in power-constrained regions and limit the ability to maintain precise temperature controls. In Thailand, agricultural freight remains dominated by road, while rail and inland water transport options are underused, which keeps logistics costs elevated relative to international benchmarks and increases exposure to temperature excursions on longer routes. The lack of integrated networks and uneven capacity distribution forces exporters to stitch together multiple providers across the first mile, line-haul, storage, and border processes. These handoffs increase both dwell time and temperature risk, which limits quality outcomes in the Asia-Pacific food logistics market.

Other drivers and restraints analyzed in the detailed report include:

- Cold Chain Infrastructure Development

- Organized Retail and Modern Trade Growth

- High Capital and Operating Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation commanded 61.34% of the Asia-Pacific food logistics market share in 2025, and value-added services and other logistics solutions are projected to expand at 5.41% CAGR through 2031 for the Asia-Pacific food logistics market size. Road carries the majority of agricultural loads in Thailand, where rail is underused despite per-ton-kilometer advantages, which sustains reliance on flexible last-mile assets for frequent, small-batch replenishment. India's dedicated Reefer Express service connecting ICD Kanpur and Mundra Port was launched in March 2026 to provide a rail corridor with tighter temperature controls and fuel savings on long domestic legs with reliable export handoffs. Warehousing footprints are growing to support omnichannel fulfillment, including temperature-controlled space in regional hubs that can scale multi-category flows for regional and cross-border distribution. Value-added solutions now bundle pre-cooling, portioning, labeling, and automated document checks to reduce handoffs and increase visibility, which aligns with buyer expectations for integrated cold chain orchestration in the Asia-Pacific food logistics market. Certifications such as ISO 9001 and ISO 22000 are becoming common prerequisites for multinational buyers, which push providers to formalize quality procedures and maintain robust documentation across all service lines.

Air freight supports high-value perishables that require rapid international connections, and network upgrades like DHL's expanded Airfreight Cold Chain Network connect more than 30 GDP-compliant hubs with additional routes targeted in Asia. Regional air cargo volumes are projected to rise through 2028, which supports shorter cycles for cross-border shipments of fresh and chilled products. Maritime routes remain central for bulk commodity movements, and Hong Kong's inbound food and beverage volumes in early 2025 confirm stable demand for seaborne distribution. Cross-border trucking is improving under the ASEAN Customs Transit System, and Kuehne+Nagel has added prime movers and containers in Thailand to meet e-commerce and high-tech demand while lowering cost and dwell time at borders. Digital control towers promoted in Singapore enable real-time management of routes and temperature performance, which reduces exception handling and strengthens compliance readiness for shippers across the Asia-Pacific food logistics market.

List of Companies Covered in this Report:

- DHL Group

- Nippon Express Holdings

- Kerry Logistics Network

- Yusen Logistics (Part of NYK Line)

- DSV

- Toll Group

- SF Express

- AIT Worldwide Logistics

- CEVA Logistics

- Kuehne + Nagel

- Kintetsu World Express

- Geodis

- Hellmann Worldwide Logistics

- JWD InfoLogistics

- SEKO Logistics

- Sagawa Express

- Crane Worldwide Logistics

- CWT PTE. LIMITED

- Nichirei Logistics Group

- CJ Rokin Logistic

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Foreign Investment and Logistics Modernization

- 4.2.2 E-commerce and Quick Commerce Boom

- 4.2.3 Cold Chain Infrastructure Development

- 4.2.4 Organized Retail and Modern Trade Growth

- 4.2.5 Cross-Border Food Trade Expansion

- 4.2.6 Food Safety and Quality Standards

- 4.3 Market Restraints

- 4.3.1 Fragmented Cold Chain Infrastructure

- 4.3.2 High Capital and Operating Costs

- 4.3.3 Regulatory Complexity and Inconsistency

- 4.3.4 Infrastructure and Connectivity Challenges

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Hybrid Distribution Models Addressing Diversity

- 4.9 Government-Led Cold Chain Corridors Emerging

5 Market Size & Growth Forecasts

- 5.1 By Services

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Water

- 5.1.1.4 Air

- 5.1.2 Warehousing

- 5.1.3 Value-Added Services and Others

- 5.1.1 Transportation

- 5.2 By Temperature-Control Type

- 5.2.1 Cold Chain

- 5.2.1.1 Ambient (15-25 °C)

- 5.2.1.2 Chilled (2-8 °C)

- 5.2.1.3 Frozen (Less than 0 °C)

- 5.2.2 Non Cold Chain

- 5.2.1 Cold Chain

- 5.3 By End-Product Category

- 5.3.1 Meat & Seafood

- 5.3.2 Dairy & Frozen Desserts

- 5.3.3 Fruits & Vegetables

- 5.3.4 Food and Beverages

- 5.3.5 Others

- 5.4 By Country (Value, USD)

- 5.4.1 China

- 5.4.2 Japan

- 5.4.3 India

- 5.4.4 South Korea

- 5.4.5 Australia

- 5.4.6 Indonesia

- 5.4.7 Malaysia

- 5.4.8 Philippines

- 5.4.9 Singapore

- 5.4.10 Thailand

- 5.4.11 Vietnam

- 5.4.12 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 Nippon Express Holdings

- 6.4.3 Kerry Logistics Network

- 6.4.4 Yusen Logistics (Part of NYK Line)

- 6.4.5 DSV

- 6.4.6 Toll Group

- 6.4.7 SF Express

- 6.4.8 AIT Worldwide Logistics

- 6.4.9 CEVA Logistics

- 6.4.10 Kuehne + Nagel

- 6.4.11 Kintetsu World Express

- 6.4.12 Geodis

- 6.4.13 Hellmann Worldwide Logistics

- 6.4.14 JWD InfoLogistics

- 6.4.15 SEKO Logistics

- 6.4.16 Sagawa Express

- 6.4.17 Crane Worldwide Logistics

- 6.4.18 CWT PTE. LIMITED

- 6.4.19 Nichirei Logistics Group

- 6.4.20 CJ Rokin Logistic