|

시장보고서

상품코드

2063359

영국의 식품 물류 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United Kingdom Food Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

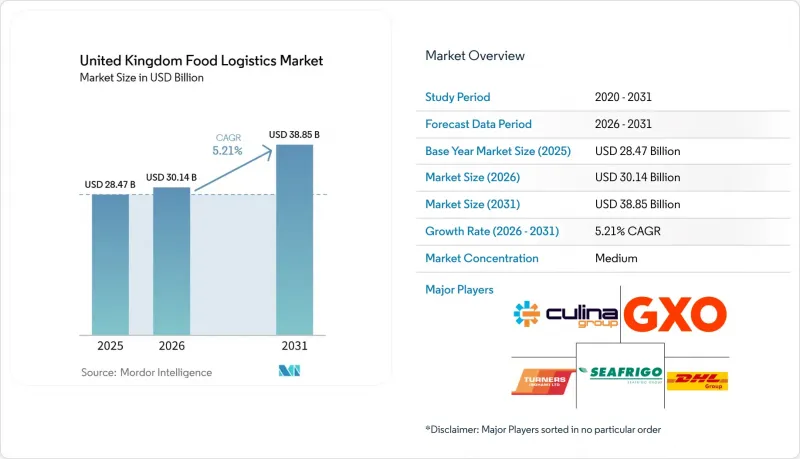

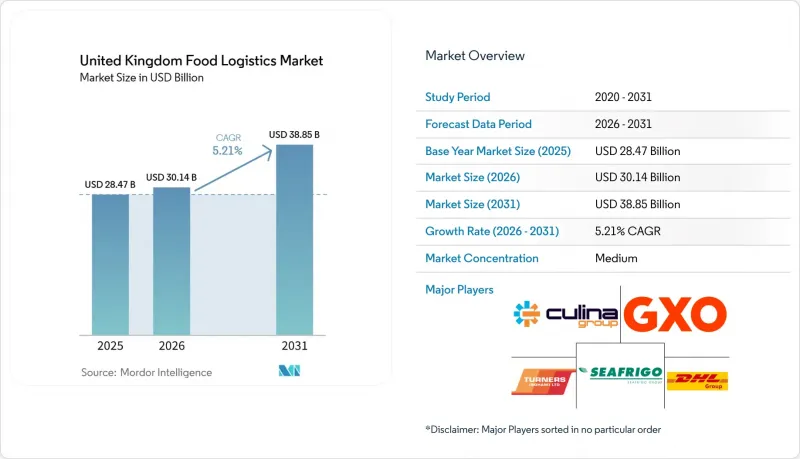

Mordor Intelligence에 의하면, 영국의 식품 물류 시장 규모는 2025년에 284억 7,000만 달러로 평가되었고, 2026년 301억 4,000만 달러로 추정되고, 2031년까지 388억 5,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 5.21%를 나타낼 전망입니다.

펠릭스토우-미들랜드 회랑을 통한 복합 일괄 냉장 운송, 폐기물 디지털 추적 의무화, 그리고 정부의 '레벨업' 프로그램을 통해 자금을 지원받은 지역 처리 허브가 이러한 성장의 기반이 되고 있습니다. 본 보고서는 서비스별(운송, 창고 및 보관, 부가가치 서비스), 온도 관리 유형별(콜드체인(상온, 냉장, 냉동), 비콜드체인), 최종 제품 카테고리별(육류, 수산물 및 가금류, 유제품 및 냉동 디저트, 원예 작물, 가공식품, 반려동물사료, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

영국의 식품 물류 시장 동향 및 인사이트

수출 지향적인 냉장 식품의 급증으로 복합 일괄 운송 수요가 확대되고 있습니다.

2025년 유제품 수출량이 사상 최고치를 기록함에 따라, 아시아태평양 시장을 겨냥한 중온 유제품 및 즉석 식품의 운송량이 두 자릿수 성장세를 보이며, 온도 관리 컨테이너와 심수항으로의 철도 접근성에 대한 수요를 더욱 부추기고 있습니다. 중온 화물은 냉동 화물보다 더 엄격한 2-8℃의 온도 범위와 짧은 운송 시간이 필요하기 때문에 화주들은 운송 전 과정을 통틀어 최대 12시간을 단축할 수 있는 통합형 도로·철도 솔루션을 선택하고 있습니다. GB Railfreight사가 펠릭스토우-미들랜드 간 주요 노선에서 제공하는 전용 냉동 컨테이너 운송 서비스는 탄소 배출 감축량과 연료 절감 효과가 정량화된다면 철도가 장거리 운송 수요를 확보할 수 있음을 보여줍니다. 운송 수단의 전환을 통해 관련 배출량이 76% 감소하므로, 수출업체는 지속가능성 노력을 강조할 수 있습니다. 그러나 이러한 노력이 널리 보급되기 위해서는 냉장 화차의 확충과, 온도 편차를 미연에 방지하기 위한 컨테이너 추적 시스템의 자동화가 필수적입니다.

폐기물 디지털 추적 의무화가 역물류의 흐름을 확대되고 있습니다.

2025년 4월부터 의무화되는 식품 폐기물 보고 제도에 따라, 주요 식료품 소매업체 및 외식업 종사자 모두에게 역물류 요건이 공식적으로 규정되었습니다. 2026년 3월까지 의무화되는 가정용 음식물 쓰레기 분리 수거는 기존 배송 경로와 중복되는 수거 경로를 추가하게 됨에 따라 차량 가동률 향상으로 이어지고 있습니다. 테스코와 같은 소매업체들은 현재 라스트 마일 배송과 잉여 상품 회수를 결합하고, QR 코드를 통한 데이터 추적을 활용하여 재분배를 담당하는 NGO로 배송 경로를 설정하고 있습니다. 혼합 적재 냉장 밴과 API 연동형 스케줄링 도구를 보유한 사업자는 과거에는 빈 차로 돌아오던 귀로 운행을 수익을 창출하는 서비스로 전환할 수 있으며, 배출량을 줄이고 규제상 크레딧을 확보할 수 있습니다. 컴플라이언스 감사에서 엔드투엔드 디지털 가시성에 대한 요구가 점점 더 높아지는 가운데, 조기에 도입한 기업들은 선구자로서의 우위를 누리고 있습니다.

F가스와 암모니아 규제가 강화되면서 냉장 창고 개보수 비용이 상승하고 있습니다.

2030년까지 HFC 할당량이 79% 감축됨에 따라, 영국의 냉장 창고 중 여전히 구형 냉매를 사용하고 있는 3분의 2에 해당하는 시설은 시설당 60만-250만 달러의 비용을 들여 시스템을 개조하거나 교체해야할 것입니다. 암모니아나 이산화탄소를 활용한 설계는 에너지 비용을 대폭 절감해 주지만, 누출 감지 장치 설치, 환기 설비 업그레이드, 그리고 숙련된 기술자 확보가 필요합니다. 자금 사정에 어려움을 겪는 독립 사업자들에게 이 설비 투자액은 감당하기 힘든 수준이므로, 자금 조달, 건설, 장기 운영 계약을 일괄 패키지로 묶은 리니지 로지스틱스(Lineage Logistics) 등의 REIT(부동산 투자 신탁)과의 세일 앤 리스백 거래가 활성화되고 있습니다.

부문별 분석

서비스 유형별로는 2025년 운송이 영국 식품 물류 시장 점유율의 46.77%를 차지했습니다. 라스트 마일 배송에서 도로 운송은 여전히 필수적이지만, 인력 부족과 디젤 연료비 급등으로 인해 이익률이 압박받고 있어, 사업자들은 수익성이 높은 부대 업무로 전환하고 있습니다. 급속 냉동, 재고 관리, 공동 포장, 체계적인 역물류와 같은 부가가치 서비스는 연평균 성장률(CAGR) 7.78%로 성장을 지속하고, 있으며, 이는 영국 식품 물류 시장 전체의 연평균 성장률보다 2% 가까이 높은 수치입니다. 고객들은 WMS와 TMS의 원활한 통합, SKU 단위의 가시성, 그리고 다온도 환경에서 주문 조립이 가능한 공급업체를 높이 평가했습니다. 해상 및 내륙 수운은 항만을 중심으로 한 틸트 터널 보관과 밀접한 관련이 있지만, 운송 능력의 병목 현상이 해소된다면 철도는 복합운송 회랑에서 점차 시장 점유율을 확대해 나갈 것입니다.

바로 자동화가 성과 균등화의 핵심 요소입니다. 웨이크필드에 위치한 NewCold의 자동 AS/RS 시설에서는 평방미터당 팔레트 처리량이 수동 설계 대비 40% 향상되었으며, 취급 단위당 에너지 소비를 줄이는 동시에 거의 비접촉 방식의 안전 프로토콜을 충족하고 있습니다. 슈퍼마켓들이 물류 입찰을 갱신하는 가운데, 운송, 창고 보관, 규정 준수 보고를 통합한 종합적인 계약이 부서별 개별 제안보다 우위를 점하고 있습니다. DFDS Logistics는 이러한 변화를 잘 보여주고 있습니다. 크로스독의 재설계에는 급속 냉동고, 주문 조립 로봇, RFID 지원 폐기물 회수 게이트가 통합되었습니다. 예측 기간 동안 수익 성장은 기존의 '운송 및 보관' 모델을 데이터가 풍부하고 규정 준수가 내재된 서비스 플랫폼으로 전환하는 운송 회사들로 집중될 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the united kingdom food logistics market size was valued at USD 28.47 billion in 2025 and estimated to grow from USD 30.14 billion in 2026 to reach USD 38.85 billion by 2031, at a CAGR of 5.21% during the forecast period (2026-2031).

Intermodal refrigerated transport along the Felixstowe-Midlands corridor, mandatory digital waste-tracking, and regional processing hubs funded by the government's levelling-up program anchor this growth. This report is Segmented by Services (Transportation, Warehousing and Storage, Value-Added Services), by Temperature-Control Type (Cold Chain (Ambient, Chilled, Frozen), Non-Cold Chain), by End-Product Category (Meat/Seafood/Poultry, Dairy Products/Frozen Desserts, Horticulture, Processed Food Products, Pet Food, Others). The Market Forecasts are Provided in Terms of Value (USD).

United Kingdom Food Logistics Market Trends and Insights

Export-Oriented Chilled-Food Surge Amplifying Intermodal Demand

Record dairy export volumes in 2025 accompanied a double-digit rise in chilled meat and ready-to-eat products moving to Asia-Pacific markets, driving incremental demand for temperature-controlled containers and rail access to deep-water ports. Chilled items require tighter 2-8 °C windows and shorter transit times than frozen cargo, which pushes shippers toward integrated road-rail solutions that cut end-to-end journeys by up to 12 hours. GB Railfreight's dedicated reefer services on the Felixstowe-Midlands spine illustrate how rail captures long-haul volumes once carbon abatements and fuel savings are quantified. Exporters gain sustainability credentials as modal shift cuts 76% of associated emissions. However, widespread take-up relies on a larger refrigerated wagon fleet and automated container-tracking to pre-empt temperature excursions.

Mandatory Digital Waste-Tracking Expanding Reverse-Logistics Flows

Compulsory food-waste reporting from April 2025 has formalized reverse-logistics requirements for every major grocer and food-service player. Separate household food-waste collection mandated by March 2026 is adding collection routes that mirror forward distribution lanes, boosting fleet utilization. Retailers such as Tesco now pair last-mile deliveries with surplus pick-ups, routing them to redistribution NGOs aided by QR-coded data trails. Operators with mixed-load refrigerated vans and API-linked scheduling tools can turn what was once empty back-haul into a revenue-generating service, trimming emissions and securing regulatory credits. Early adopters enjoy first-mover advantage as compliance audits increasingly demand end-to-end digital visibility.

Tightening F-Gas and Ammonia Regulations Inflating Cold-Store Retrofit Costs

HFC quotas fall 79% by 2030, forcing two-thirds of the United Kingdom cold stores still running legacy refrigerants to retrofit or replace systems at USD 0.6-2.5 million per site. Ammonia and CO2 designs slash energy bills but require leak-detection, ventilation upgrades, and skilled engineers. For cash-constrained independents the capex outlay is prohibitive, incentivizing sale-and-leaseback deals with REITs such as Lineage Logistics that bundle financing, build, and long-term operating contracts.

Other drivers and restraints analyzed in the detailed report include:

- Regional Processing Hubs under Levelling-Up Agenda Boosting Mid-Mile Reefer Routes

- Predictive-Maintenance Deployment for Refrigerated Assets Cutting Downtime

- Shortage of Refrigerated Rail Wagons Constraining Modal-Shift Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In service type, transportation commanded 46.77% of the United Kingdom food logistics market share in 2025. Road remains indispensable for last-mile coverage, but labor shortages and diesel costs compress margins, steering operators toward higher-yield ancillary work. Value-added services such as blast freezing, inventory management, co-packing, and organised reverse-logistics are on track for a 7.78% CAGR, almost 2 percentage points above the overall United Kingdom food logistics market CAGR. Clients reward providers capable of native WMS-TMS integration, SKU-level visibility, and multi-temperature order assembly. Sea and inland-water moves tie closely to port-centric chill-tunnel storage, while rail's share inches forward on intermodal corridors once capacity bottlenecks ease.

Automation is the performance equalizer. NewCold's automated AS/RS facility in Wakefield lifts pallet-throughput per square meter 40% above manual designs, compressing energy per unit handled and meeting near-zero-touch safety protocols. As supermarkets renew logistics tenders, bundled contracts that fuse transport, warehousing, and compliance reporting beat siloed offerings. DFDS Logistics illustrates the pivot: cross-dock redesigns now include blast-freezers, order-assembly robots, and RFID-enabled waste-capture gates. Over the forecast horizon, earnings growth will be skewed toward fleets that convert traditional "haul and store" models into data-rich, compliance-embedded service platforms.

List of Companies Covered in this Report:

- DHL Group

- GXO Logistics

- Culina Group

- Seafrigo Group

- Turners (Soham) Ltd

- Kuehne+Nagel

- DFDS Logistics

- XPO Logistics

- DACHSER

- Lineage, Inc.

- NewCold

- La Poste Group (Including DPD UK)

- DSV A/S

- Hellmann Worldwide Logistics

- Constellation Cold Logistics

- Kammac

- McCulla Refrigerated Transport

- Rhenus Logistics

- Certa Logistics

- Supply Chain Solution Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Export-Oriented Chilled-Food Surge Amplifying Intermodal Demand

- 4.2.2 Mandatory Digital Waste-Tracking Expanding Reverse-Logistics Flows

- 4.2.3 Regional Processing Hubs Under "Levelling-Up" Agenda Boosting Mid-Mile Reefer Routes

- 4.2.4 Predictive-Maintenance Deployment for Refrigerated Assets Cutting Downtime

- 4.2.5 Expansion of Rail-Based Refrigeration Services on Felixstowe-Midlands Corridor

- 4.2.6 Insurer-Led Temperature-Compliance Requirements Creating Premium Service Tiers

- 4.3 Market Restraints

- 4.3.1 Tightening F-Gas and Ammonia Regulations Inflating Cold-Store Retrofit Costs

- 4.3.2 Shortage of Refrigerated Rail Wagons Constraining Modal Shift Capacity

- 4.3.3 Currency Volatility Elevating Fuel and Equipment Import Costs

- 4.3.4 Rising Insolvency Risk Among SME Food Hauliers Due to Customs-Linked Cash-Flow Stress

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Services

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Sea and Inland Water

- 5.1.1.4 Air

- 5.1.2 Warehousing and Storage

- 5.1.3 Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.)

- 5.1.1 Transportation

- 5.2 By Temperature-Control Type

- 5.2.1 Cold Chain

- 5.2.1.1 Ambient (15-25 °C)

- 5.2.1.2 Chilled (2-8 °C)

- 5.2.1.3 Frozen (Less than 0 °C)

- 5.2.2 Non Cold Chain

- 5.2.1 Cold Chain

- 5.3 By End-Product Category

- 5.3.1 Meat, Seafood, and Poultry

- 5.3.2 Dairy Products and Frozen Deserts (Milk, Ice-cream, Butter, etc.)

- 5.3.3 Horticulture (Fresh Fruits and Vegetables)

- 5.3.4 Processed Food Products

- 5.3.5 Pet Food

- 5.3.6 Others (Spreads, Seasoning, Dressing, Specialty and Functional Foods, etc.)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 GXO Logistics

- 6.4.3 Culina Group

- 6.4.4 Seafrigo Group

- 6.4.5 Turners (Soham) Ltd

- 6.4.6 Kuehne+Nagel

- 6.4.7 DFDS Logistics

- 6.4.8 XPO Logistics

- 6.4.9 DACHSER

- 6.4.10 Lineage, Inc.

- 6.4.11 NewCold

- 6.4.12 La Poste Group (Including DPD UK)

- 6.4.13 DSV A/S

- 6.4.14 Hellmann Worldwide Logistics

- 6.4.15 Constellation Cold Logistics

- 6.4.16 Kammac

- 6.4.17 McCulla Refrigerated Transport

- 6.4.18 Rhenus Logistics

- 6.4.19 Certa Logistics

- 6.4.20 Supply Chain Solution Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment