|

시장보고서

상품코드

2063362

중동의 식품 물류 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Middle East Food Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

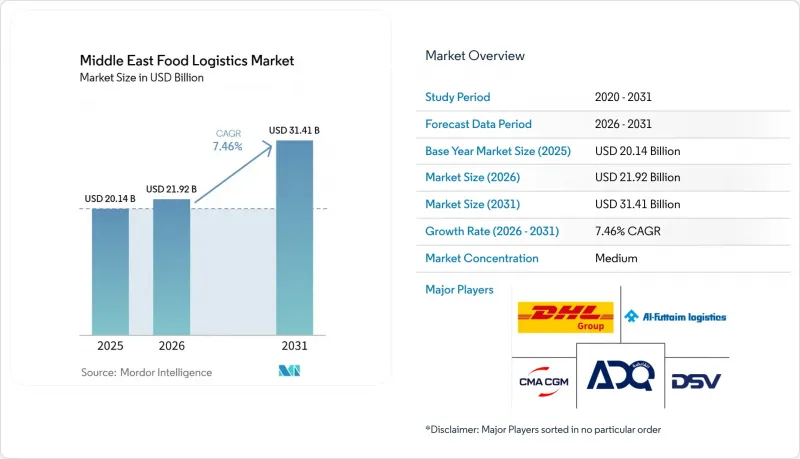

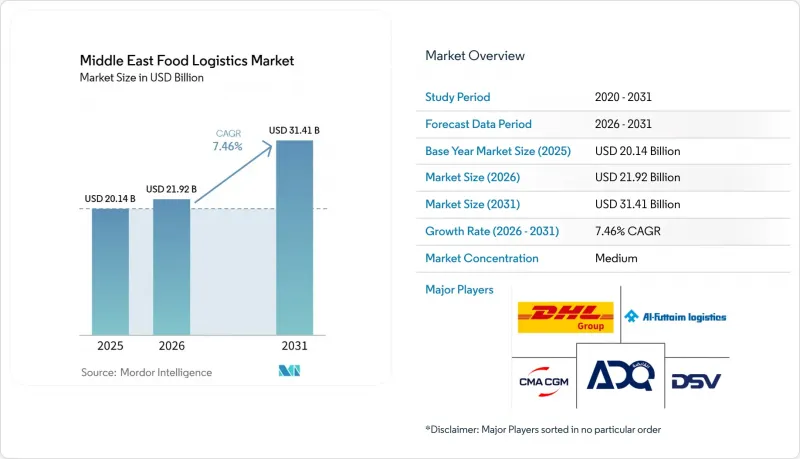

Mordor Intelligence에 의하면, 중동의 식품 물류 시장 규모는 2025년 201억 4,000만 달러로 평가되었고, 2026년 219억 2,000만 달러로 추정되고, 2031년까지 314억 1,000만 달러로 확대될 전망이며, 2026-2031년 CAGR 7.46%를 나타낼 것으로 예측됩니다.

정부 주도의 식량 안보 관련 규제 강화로 인해 전략적 비축 계획이 실물 자산인 창고 건설로 전환되고 있는 한편, GCC 전역의 세관 업무 디지털화로 인해 과거 신선식품 무역을 지연시켰던 국경에서의 마찰이 해소되고 있습니다. 본 보고서는 서비스 유형별(운송, 창고 및 보관, 부가가치 서비스), 온도 관리별(콜드체인, 비콜드체인), 최종 제품 카테고리별(육류, 수산물 및 가금류, 유제품, 기타), 국가별(사우디아라비아, UAE, 카타르, 쿠웨이트, 오만, 바레인, 이집트, 기타 중동 국가)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

중동의 식품 물류 시장 동향 및 인사이트

전략적 식량 안보 비축 프로그램이 지역 창고 용량을 확대

각국 정부는 식량 안보에 관한 논의를 다온도대 창고 건설로 구체화하고 있습니다. 그 예로, 12개월 분의 소비량에 해당하는 곡물 비축을 의무화하는 사우디아라비아의 요건, 85%의 자급률 달성을 목표로 하는 UAE의 목표를 들 수 있습니다. 장기 인수 계약은 사업자에게 연금과 같은 안정적인 수익을 보장하지만, 제품 노후화를 방지하기 위해서는 고도의 재고 회전 시스템 도입이 필수적입니다. 비축 시설에서는 실시간 IoT 모니터링 시스템 도입이 확대되면서 비축품의 신선도를 시각화하고 폐기물을 줄이고 있습니다. 이러한 프로그램들은 중동 식품 물류 시장의 전문화를 가속화하여, 정부의 감사 기준을 충족하지 못하는 소규모 업체들을 시장에서 배제하고 있습니다. 장기적으로는 공공 부문의 잉여 물량이 상업용 임대 시장으로 유입될 것으로 예상되며, 이에 따라 가격 경쟁이 더욱 치열해질 것으로 보입니다.

GCC의 세관 디지털화와 통합 관세표가 신선식품의 국경 간 유통을 가속화

GCC 공동 관세법과 블록체인을 활용한 통관 플랫폼 덕분에 국경에서의 체류 시간이 며칠에서 몇 시간으로 단축되었으며, 부패 위험과 Kg당 운송 비용이 대폭 감소했습니다. 통일된 전자 식물 검역 증명서 및 할랄 인증서를 통해 서류 절차가 표준화됨에 따라, 3PL(제3자 물류) 사업자는 다국간 허브 간 재고를 통합 관리하면서 배송 기간을 보장할 수 있게 되었습니다. 이러한 물류 속도 향상으로 인해 중동의 식품 물류 시장은 유럽이나 북미의 성숙한 무역 루트에 필적하는 원활한 거대 회랑으로서의 위상을 확립하고 있습니다. 이 시스템은 다모드 운송 솔루션을 더욱 촉진하고 있으며, 제벨 알리에서 리야드나 무스카트로 향하는 트럭 운송은 속도와 비용 면에서 모두 근해 운송과 직접적으로 경쟁하게 되었습니다. 그러나 사업자들은 기존 TMS 플랫폼과 새로운 정부 API를 연동하기 위한 초기 통합 비용에 직면해 있습니다.

도시 지역의 냉장 창고 개발은 높은 지가와 자본 집약성으로 인해 제약을 받고 있습니다.

제벨 알리나 킹 칼리드 공항 인근의 산업용 토지는 주변 대체 부지보다 30-50% 높은 가격에 거래되고 있어, 이로 인해 투자 회수 기간이 7년을 초과하게 되어 중소기업에게는 진입 장벽이 되고 있습니다. 또한, 에너지 효율이 높은 자연 냉매 시스템은 초기 비용을 증가시키는 반면, 비용 절감 효과는 장기적으로만 나타나기 때문에 차입을 통한 자금 조달 의욕은 더욱 떨어지고 있습니다. 개발업체들은 다층 창고나 자동 팔레트 셔틀의 도입을 시도하고 있지만, 구조적 개조는 설계의 복잡성과 보험료 인상을 초래합니다. 그 결과, 라마단이나 하즈 성수기에는 공급 부족이 발생하여 현물 운임이 급등하고, 이는 중동 식품 물류 시장 전체로 파급되고 있습니다. 재정적 여력이 있는 기관 투자자들이 저가에 부실 자산을 임베디드함에 따라 업계 재편이 진행되고 있습니다.

부문별 분석

2025년, 중동 식품 물류 시장 점유율의 54.84%를 운송 부문이 차지했으며, 그 기반이 되는 것은 수입 허브와 소비지를 연결하는 육상 및 근해 운송 노선입니다. 그러나 부가가치 서비스는 연평균 성장률(CAGR) 10.03%라는 놀라운 성장세를 보이고 있으며, 이는 화주들이 단순한 운송에서 급속 냉동, 라벨 부착, 통관 서류 작성을 통합한 패키지형 서비스로 전환하고 있음을 반영합니다. FMCG(일용소비재) 고객들이 SKU 확충과 판로 다각화를 추구하는 가운데, 생산 일정을 온라인 쇼핑몰의 플래시 세일과 연동하여 주문부터 배송까지의 주기를 24시간 이내로 단축할 수 있는 3PL(제3자 물류 업체)이 주목받고 있습니다.

연비 향상과 텔레매틱스를 활용한 경로 최적화가 진행되는 가운데, 상품화된 간선 운송의 이익률은 계속해서 축소되고 있어 기존 사업자들은 부수적인 수익원으로의 전환을 모색해야 하는 상황에 놓여 있습니다. 첨단 창고 관리 시스템(WMS)와 예측 분석을 결합한 업체들은 현재 유통기한 관리 및 반품 처리 분야에서 수익을 창출하고 있습니다. 그 결과, 부가가치 기능에 기인한 중동 식품 물류 시장 규모는 2031-2025년 수준에서 두 배로 증가할 것으로 예상되며, 이는 기술에 정통한 사업자의 경쟁 우위를 더욱 공고히할 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the middle east food logistics market size is projected to expand from USD 20.14 billion in 2025 and USD 21.92 billion in 2026 to USD 31.41 billion by 2031, registering a CAGR of 7.46% between 2026 to 2031.

Intensifying sovereign-backed food-security mandates are converting strategic stockpiling ambitions into hard-asset warehouse construction, while GCC-wide customs digitalization dismantles legacy border friction that once slowed perishable trade. This report is Segmented by Service Type (Transportation, Warehousing and Storage, Value-Added Services), by Temperature-Control (Cold Chain, Non Cold Chain), by End-Product Category (Meat/Seafood/Poultry, Dairy Products, and More), and by Country (Saudi Arabia, UAE, Qatar, Kuwait, Oman, Bahrain, Egypt, Rest of Middle East). The Market Forecasts are Provided in Terms of Value (USD).

Middle East Food Logistics Market Trends and Insights

Strategic Food-Security Stockpiling Programs Expanding Regional Warehouse Capacity

Governments are translating food-security rhetoric into multi-temperature storage construction, illustrated by Saudi Arabia's grain reserve requirements that hold 12-months consumption equivalent and the UAE's 85% self-sufficiency ambition. Long-term offtake agreements guarantee annuity-style revenues for operators but oblige sophisticated inventory-rotation systems to limit obsolescence. Stockpiling facilities increasingly integrate real-time IoT monitoring, ensuring visibility into reserve freshness and reducing waste. The programs accelerate professionalization of the Middle East food logistics market, crowding out smaller entrants unable to meet government audit thresholds. Over the long term, excess public-sector capacity is expected to bleed into commercial leasing, further tightening competitive pricing.

GCC Customs Digitalization and Unified Tariff Schedules Accelerating Cross-Border Perishable Flows

The GCC Common Customs Law and blockchain-enabled clearance platforms now shrink border dwell time from days to hours, materially lowering spoilage risk and freight cost per kilogram. Unified electronic phytosanitary and halal certificates standardize paperwork, empowering 3PLs to guarantee delivery windows while pooling inventory across multi-country hubs. Enhanced velocity positions the Middle East food logistics market as a seamless mega-corridor that rivals mature trade lanes in Europe and North America. The system further stimulates multimodal solutions, trucking from Jebel Ali to Riyadh or Muscat, now competes directly with short-sea transits on both speed and cost. However, operators face upfront integration costs to interface legacy TMS platforms with new government APIs.

Urban Cold-Storage Development Hampered by High Land Prices and Capital Intensity

Industrial plots near Jebel Ali or King Khalid Airport are priced 30-50% above ambient alternatives, translating into payback periods that exceed seven years, a hurdle for smaller firms. Debt-funding appetite tightens further because energy-efficient natural-refrigerant systems raise up-front costs while delivering savings only over time. Developers are experimenting with multilevel warehouses and automated pallet shuttles, but structural retrofits increase engineering complexity and insurance premiums. Consequently, capacity shortfalls manifest during Ramadan and Hajj peaks, forcing spot-rate spikes that ripple across the Middle East food logistics market. Consolidation ensues as well-capitalized institutional investors purchase distressed assets at discounts.

Other drivers and restraints analyzed in the detailed report include:

- Halal Tourism and Hospitality Projects Demanding Premium Food-Service Logistics

- FDI-Backed Mega-Agri Clusters Requiring End-to-End Cold Chains

- Fragmented National Food-Safety Regulations Raising Multi-Country Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation held 54.84% of the Middle East food logistics market share in 2025, anchored by road and short-sea corridors connecting import hubs with consumption centers. However, value-added services are on track for a blistering 10.03% CAGR, reflecting shippers' pivot from pure haulage to bundled offerings that integrate blast-freezing, labeling, and customs documentation. As FMCG customers pursue SKU proliferation and channel diversification, they prize 3PLs capable of synchronizing production runs with e-commerce flash-sales, compressing order-to-delivery cycles to under 24 hours.

Margins in commoditized line-haul continue to tighten amid fuel-efficiency gains and telematics-driven route optimization, pushing incumbents toward ancillary revenue streams. Providers that meld advanced WMS with predictive analytics now monetize shelf-life management and returns processing. Consequently, the Middle East food logistics market size attributable to value-added functions is forecast to double its 2025 base by 2031, fortifying competitive moats for tech-savvy operators.

List of Companies Covered in this Report:

- Al-Futtaim Logistics

- GAC Group

- DHL Group

- DSV

- NAQEL Express

- Wared Logistics

- RSA Global

- Total Freight International

- Al Talib Shipping Co. LLC

- System8Group

- CUBES International Logistics

- TLM International Freight Services LLC

- EPx Logistics

- ILS Egypt

- PIL Logistics

- Clarion Shipping Services L.L.C

- Four Winds

- Noatum Logistics

- CMA CGM

- ADQ

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government-Led Food-Security Stockpiling Programs Expanding Regional Warehouse Capacity

- 4.2.2 GCC-Wide Customs Digitalization and Unified Tariff Schedules Accelerating Cross-Border Perishables Flows

- 4.2.3 Surge in Halal Tourism and Hospitality Projects Demanding Premium Food-Service Logistics

- 4.2.4 FDI-Backed Mega-Agri Clusters (E.G., Desert Dairies & Greenhouse Farms) Requiring End-To-End Cold Chains

- 4.2.5 Roll-Out of Solar-Powered Micro-Cold Rooms Integrating Rural Producers into Modern Supply Chains

- 4.2.6 Smart-City Pilots Deploying Autonomous Temperature-Controlled Delivery Vehicles for Last-Mile Fulfilment

- 4.3 Market Restraints

- 4.3.1 Urban Cold-Storage Development Hampered by High Land Prices and Capital Intensity

- 4.3.2 Fragmented National Food-Safety Regulations Raising Multi-Country Compliance Costs

- 4.3.3 Impending Phase-Out of High-GWP Refrigerants Crimping Availability of CO2-Grade Retrofits for Reefers

- 4.3.4 Rising Cyber-Attacks on IoT-Linked Warehouses Disrupting Temperature Monitoring Systems

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD Billion)

- 5.1 By Services

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Sea and Inland Water

- 5.1.1.4 Air

- 5.1.2 Warehousing and Storage

- 5.1.3 Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.)

- 5.1.1 Transportation

- 5.2 By Temperature-Control Type

- 5.2.1 Cold Chain

- 5.2.1.1 Ambient (15-25 °C)

- 5.2.1.2 Chilled (2-8 °C)

- 5.2.1.3 Frozen (Less than 0 °C)

- 5.2.2 Non Cold Chain

- 5.2.1 Cold Chain

- 5.3 By End-Product Category

- 5.3.1 Meat, Seafood, and Poultry

- 5.3.2 Dairy Products and Frozen Deserts (Milk, Ice-cream, Butter, etc.)

- 5.3.3 Horticulture (Fresh Fruits and Vegetables)

- 5.3.4 Processed Food Products

- 5.3.5 Pet Food

- 5.3.6 Others (Spreads, Seasoning, dressing, Specialty and Functional Foods, etc.)

- 5.4 By Country

- 5.4.1 Saudi Arabia

- 5.4.2 United Arab Emirates

- 5.4.3 Qatar

- 5.4.4 Kuwait

- 5.4.5 Oman

- 5.4.6 Bahrain

- 5.4.7 Egypt

- 5.4.8 Rest of Middle East

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Al-Futtaim Logistics

- 6.4.2 GAC Group

- 6.4.3 DHL Group

- 6.4.4 DSV

- 6.4.5 NAQEL Express

- 6.4.6 Wared Logistics

- 6.4.7 RSA Global

- 6.4.8 Total Freight International

- 6.4.9 Al Talib Shipping Co. LLC

- 6.4.10 System8Group

- 6.4.11 CUBES International Logistics

- 6.4.12 TLM International Freight Services LLC

- 6.4.13 EPx Logistics

- 6.4.14 ILS Egypt

- 6.4.15 PIL Logistics

- 6.4.16 Clarion Shipping Services L.L.C

- 6.4.17 Four Winds

- 6.4.18 Noatum Logistics

- 6.4.19 CMA CGM

- 6.4.20 ADQ

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment