|

시장보고서

상품코드

2063339

독일의 식품 물류 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Germany Food Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

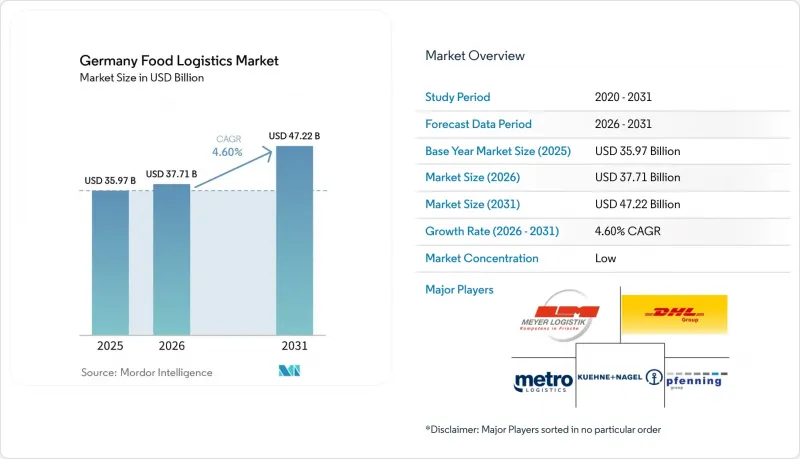

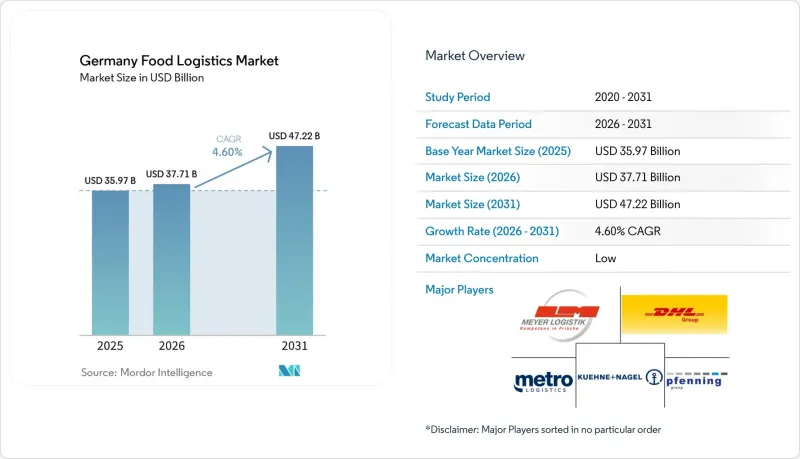

Mordor Intelligence에 의하면, 독일의 식품 물류 시장 규모는 2025년에 359억 7,000만 달러로 평가되었고, 2026년 377억 1,000만 달러로 추정되고, 2031년까지 472억 2,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 4.60%를 나타낼 전망입니다.

본 보고서는 서비스별(운송, 창고 보관, 부가가치 서비스, 기타), 온도 관리 유형별(콜드체인 및 비콜드체인), 최종 제품 카테고리별(육류 및 수산물, 유제품 및 냉동 디저트, 과일 및 채소, 식품 및 음료, 기타), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

독일의 식품 물류 시장 동향 및 인사이트

온라인 식료품 및 음식 배달 서비스의 확대

2025년, 식품 전자상거래는 독일 식료품 매출의 약 4.3%를 차지했으며, 이에 따라 콜드체인 이용률이 높은 수준을 유지했고, 도시 지역 거점으로의 배송 빈도는 증가했으나 1회당 배송량은 감소했습니다. 소매업체들은 매장 내 피킹과 집중형 마이크로 허브를 결합한 하이브리드형 주문 처리 방식을 선호하는데, 이를 통해 자산 회전율이 향상되고 신선도 관리가 중요한 품목의 폐기량이 줄어듭니다. 경로 기반 배달 모델은 단위당 수익성을 확보하기 위해 예측 가능한 주문 밀도와 최소 구매 금액 정책에 의존하고 있으며, 이로 인해 예약 슬롯 및 동적 가격 책정 방식의 활용이 촉진되고 있습니다. 계획적인 주 단위 장바구니 시스템으로의 전환은 차량 이용률 향상과, 집적 밀도가 높은 도시권 전체에서 냉장 운송 노선의 안정적인 흐름을 뒷받침하고 있습니다. 이러한 추세는 대도시권 물류 네트워크 내의 다온도대 대응 거점망을 강화함으로써, 독일의 식품 물류 시장에서 냉장 및 냉동 통합 운송 능력에 대한 수요를 높이고 있습니다.

할인 소매업체의 지배

자사 브랜드의 확산이 진행되고, 저가형 매장이 유통망을 확대함에 따라 할인 채널이 가격과 상품 구색의 기본 방향을 결정하게 되었으며, 이는 생활 필수품 및 일용잡화의 구매 패턴을 형성했습니다. 2024년 하반기에 문을 연 아르디 노르트의 새로운 레르테-알리크세 물류 센터는 단일 거점의 처리 규모와, 신뢰할 수 있는 냉장 보관 및 도크 도어의 계획적 관리가 필요한 신선 식품 부문에 중점을 두고 있음을 여실히 보여주고 있습니다. 상권 확대와 높은 재고 회전율 덕분에 할인점들은 더욱 엄격한 배송 시간대 및 일관된 온도 관리를 요구할 수 있게 되었으며, 이로 인해 운송업체에 대한 기본적인 서비스 의무 수준이 높아지고 있습니다. 자사 브랜드의 프리미엄화는 포장 및 키트화 작업을 추가하게 되며, 이러한 작업은 종종 물류 파트너에게 이관되기 때문에 할인점의 밸류체인과 관련된 부가가치 업무의 성장을 가져오고 있습니다. 할인점들이 신뢰할 수 있는 신선도와 효율성을 추구하는 가운데, 이러한 영향으로 인해 독일 식품 물류 시장에서 다온도대 물류 및 공동 포장의 역할이 커지고 있습니다.

심각한 운전기사 부족 사태

독일은 심각한 운전기사 부족에 직면해 있으며, 이로 인해 차량 가동률과 배송 신뢰성에 부담이 가중되고 있습니다. 업계 및 언론 보도에 따르면, 향후 10년 동안 퇴직자 수가 신규 입사자 수를 상회할 것으로 예상되어 이러한 인력 부족 현상은 지속될 것으로 보입니다. 동서 지역 간의 임금 격차가 채용과 인재 유지를 어렵게 만들고 있는 반면, 연수 기간이나 보험 요건 등은 면허 제도의 개혁을 통해 공급 능력을 개선할 수 있는 속도를 제한하고 있습니다. 각 운송업체들은 임금 인상, 상여금 지급, 배송 경로 재설계 등으로 대응하고 있지만, 인력 부족으로 인해 신선식품의 계절적 성수기에는 여전히 입찰 포기나 매장에 대한 납품 지연이 발생하고 있습니다. 현재의 운영 모델에서는 인력 중심의 취급, 인수·인계 업무 및 경비 업무를 대체할 수 없기 때문에 자율주행은 여전히 장기적인 대안으로만 남아 있습니다. 이러한 제약으로 인해, 신규 시장 진출기업나 선택적 자동화를 통해 공급 부족이 완화될 때까지 독일 식품 물류 시장에서는 운송 능력과 비용에 대한 단기적인 압박이 지속될 것으로 보입니다.

부문별 분석

2025년, 운송 서비스는 매출의 53.78%를 차지했으며, 주요 사업 분야로 자리매김했습니다. 이는 전국적인 운송 노선과 대도시권에서 신선식품 및 회전율이 높은 생활용품의 빈번한 지역 간 유통에 힘입은 결과입니다. 도로 운송 분야에서는 중단거리 노선이 냉장 및 냉동 상품의 적시 보충을 뒷받침하고 있으며, 이에 따라 트레일러 이용률과 도크 회전율은 독일 식품 물류 시장의 네트워크 성과에서 여전히 핵심적인 요소로 자리 잡고 있습니다. 창고업은 다온도대 구역과 도시 지역의 마이크로 풀필먼트 거점을 중심으로 계속 확장되고 있으며, 업체들은 주요 도시의 피크일 주문 패턴에 맞추어 재고 배치를 조정하고 있습니다. 철도는 업스트림 공정의 원자재 및 포장 자재 운송에서 다시금 그 중요성이 커지고 있으며, 2026년 계약에 따라 산업 단지를 연결하는 열차가 연간 1,000편 이상 증편되어 도로 운송에 비해 배출량을 줄일 것으로 예측됩니다. 라벨링, 키팅, 클린룸 내 재포장 등의 부가가치 서비스는 2031년까지 연평균 성장률(CAGR) 5.64%로 확대될 것으로 전망됩니다. 이는 자사 브랜드의 현지화, 프로모션 관리, 그리고 콜드체인 시설 내 사전 조립 유닛을 통한 매장 인건비 절감의 필요성을 반영한 것입니다.

IFS Logistics 버전 3에서는 상시 온도 기록, 문서화된 청소 주기, 그리고 현장 및 차량 전체에 걸친 통합 시스템이 필요한 질량 균형 추적이 요구되므로, 규모와 규정 준수는 독일 식품 물류 업계에서 매우 중요한 강점으로 작용하고 있습니다. 2026년 인수로 100개 이상의 물류 전문 업체와 차량 네트워크가 더욱 광범위한 유럽 네트워크로 통합된 것에서 알 수 있듯이, 이러한 전략적 움직임을 통해 국내 혼재 운송 및 전문 노선이 지속적으로 강화되고 있습니다. 이러한 네트워크와 역량의 향상으로 인해, 확실한 하역 예약과 유통기한 보장이 필요한 식품 화주에게 제공되는 서비스 수준이 한 단계 높아졌습니다. 부가가치 서비스의 비중이 높아지는 가운데, 사업자들은 온도 관리가 이루어지는 공간에 HACCP 준수 워크플로를 도입하여 감사 대응 체제를 유지하면서도 대규모 맞춤형 서비스를 지원하고 있으며, 이는 독일 식품 물류 시장에서 풀서비스 제공업체의 차별화를 한층 더 강화하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the germany food logistics market size was valued at USD 35.97 billion in 2025 and is estimated to grow from USD 37.71 billion in 2026 to reach USD 47.22 billion by 2031, at a CAGR of 4.60% during the forecast period (2026-2031).

This report is Segmented by Services (Transportation, Warehousing, Value-Added Services, and Others), by Temperature-Control Type (Cold Chain and Non-Cold Chain), by End-Product Category (Meat & Seafood, Dairy & Frozen Desserts, Fruits & Vegetables, Food and Beverages, and Others), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Germany Food Logistics Market Trends and Insights

Online Grocery and Food Delivery Expansion

Food e-commerce reached an estimated 4.3% share of German grocery revenues in 2025, which sustained higher cold-chain utilization and more frequent, smaller drops to urban nodes. Retailers favor hybrid fulfillment that combines store-based picking and centralized micro-hubs, which improves asset turns and reduces spoilage in time-sensitive categories. Route-based home delivery models rely on predictable order densities and minimum-basket policies to protect unit economics, which encourages the use of scheduled slots and dynamic pricing. The shift to planned weekly baskets supports higher vehicle utilization and steadier refrigerated-lane flows across cities with dense catchment zones. These dynamics reinforce a multi-temperature footprint inside metropolitan distribution networks, which strengthens demand for integrated chilled and frozen capacity in the Germany food logistics market.

Discount Retailer Dominance

The discount channel set the tone on price and assortment as private-label penetration deepened and value formats expanded their distribution footprints, which shaped replenishment patterns for staples and convenience items. Aldi Nord's new Lehrte-Aligse logistics center, opened in late 2024, illustrates the scale of single-site throughput and the emphasis on fresh categories that require reliable cold storage and dock-door planning. Larger catchment areas and high pallet turns allow discounters to negotiate tighter delivery windows and consistent temperature controls, which lifts baseline service obligations for carriers. Premiumization within private labels adds packaging and kitting tasks that often shift to logistics partners, which creates growth for value-added operations linked to discount supply chains. These effects elevate the role of multi-temperature distribution and co-packing inside the Germany food logistics market as discounters seek efficiency with reliable freshness.

Acute Driver Shortage Crisis

Germany faces an acute driver deficit that strains fleet utilization and delivery reliability, with industry and media reports pointing to persistent gaps as retirements outpace new entrants through the decade. Wage differentials between western and eastern regions complicate recruitment and retention, while training timelines and insurance requirements limit the speed at which licensing reforms can improve availability. Carriers respond with higher pay, bonuses, and route redesign, but staffing imbalances still trigger rejected tenders and missed store windows during seasonal peaks for perishables. Autonomous driving remains a long-horizon option as human handling, custody transfer, and security roles cannot be replaced in current operating models. This constraint keeps short-term pressure on capacity and costs in the Germany food logistics market until new entrants and selective automation ease the shortage.

Other drivers and restraints analyzed in the detailed report include:

- Cold Chain Infrastructure Modernization

- Sustainability and Green Logistics Mandates

- High Energy and Operational Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation services accounted for 53.78% of revenues in 2025 as the dominant activity set, supported by dense regional flows for perishable foods and fast-moving staples across national corridors and urban catchments. Within road transport, short- to medium-haul routes underpin just-in-time replenishment for chilled and frozen items, which keeps trailer utilization and dock turns central to network performance in the Germany food logistics market. Warehousing continues to scale around multi-temperature zones and urban micro-fulfillment nodes, with operators aligning inventory placement to peak-day order profiles in major cities. Rail is regaining relevance for upstream ingredients and packaging, as seen in a 2026 contract that added more than 1,000 trains per year to connect industrial sites and reduce emissions versus road. Value-added services, including labeling, kitting, and cleanroom repacking, are projected to expand at a 5.64% CAGR to 2031, which reflects the need to localize private labels, manage promotions, and reduce store labor through pre-assembled units inside cold-chain facilities.

Scale and compliance are pivotal advantages in the Germany food logistics industry as IFS Logistics Version 3 demands always-on temperature logging, documented cleaning cycles, and mass-balance traceability that require integrated systems across sites and fleets. Strategic moves continue to strengthen national groupage and specialty routes, evidenced by a 2026 acquisition that integrated more than 100 logistics specialists and a fleet footprint into a broader European network. These network and capability upgrades lift the service floor for food shippers that depend on reliable dock appointments and shelf-life assurance. As value-added share rises, operators are embedding HACCP-compliant workflows in temperature-controlled spaces to support customization at scale while preserving audit readiness, which further differentiates full-service providers inside the Germany food logistics market.

List of Companies Covered in this Report:

- Nagel-Group

- DHL Group

- Pfenning group

- Metro Logistics

- Meyer Logistik

- Bruggemann Spedition + Logistik GmbH and Co. KG

- Kuehne Nagel

- Dachser

- Rhenus Logistics

- DSV

- Geodis

- Fiege Logistics

- Hellmann Worldwide Logistics

- BLG Logistics

- Quehenberger Logistics

- Worldwide Logistics Group

- NewCold

- Den Hartogh Logistics

- Kerry Logistics

- AIT Worldwide Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Online Grocery and Food Delivery Expansion

- 4.2.2 Discount Retailer Dominance

- 4.2.3 Cold Chain Infrastructure Modernization

- 4.2.4 Sustainability and Green Logistics Mandates

- 4.2.5 Central European Distribution Hub Position

- 4.2.6 Convenience Food and Ready-Meals Growth

- 4.3 Market Restraints

- 4.3.1 Acute Driver Shortage Crisis

- 4.3.2 High Energy and Operational Costs

- 4.3.3 Stringent Regulatory Compliance

- 4.3.4 Limited Urban Logistics Space

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Retail Landscape Influence

5 Market Size and Growth Forecasts

- 5.1 By Services

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Water

- 5.1.1.4 Air

- 5.1.2 Warehousing

- 5.1.3 Value-Added Services and Others

- 5.1.1 Transportation

- 5.2 By Temperature-Control Type

- 5.2.1 Cold Chain

- 5.2.1.1 Ambient (15-25 °C)

- 5.2.1.2 Chilled (2-8 °C)

- 5.2.1.3 Frozen (Less than 0 °C)

- 5.2.2 Non-Cold Chain

- 5.2.1 Cold Chain

- 5.3 By End-product Category

- 5.3.1 Meat & Seafood

- 5.3.2 Dairy & Frozen Desserts

- 5.3.3 Fruits & Vegetables

- 5.3.4 Food and Beverages

- 5.3.5 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Nagel-Group

- 6.4.2 DHL Group

- 6.4.3 Pfenning group

- 6.4.4 Metro Logistics

- 6.4.5 Meyer Logistik

- 6.4.6 Bruggemann Spedition + Logistik GmbH and Co. KG

- 6.4.7 Kuehne Nagel

- 6.4.8 Dachser

- 6.4.9 Rhenus Logistics

- 6.4.10 DSV

- 6.4.11 Geodis

- 6.4.12 Fiege Logistics

- 6.4.13 Hellmann Worldwide Logistics

- 6.4.14 BLG Logistics

- 6.4.15 Quehenberger Logistics

- 6.4.16 Worldwide Logistics Group

- 6.4.17 NewCold

- 6.4.18 Den Hartogh Logistics

- 6.4.19 Kerry Logistics

- 6.4.20 AIT Worldwide Logistics

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment