|

시장보고서

상품코드

2063482

싱가포르의 골판지 포장 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Singapore Corrugated Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

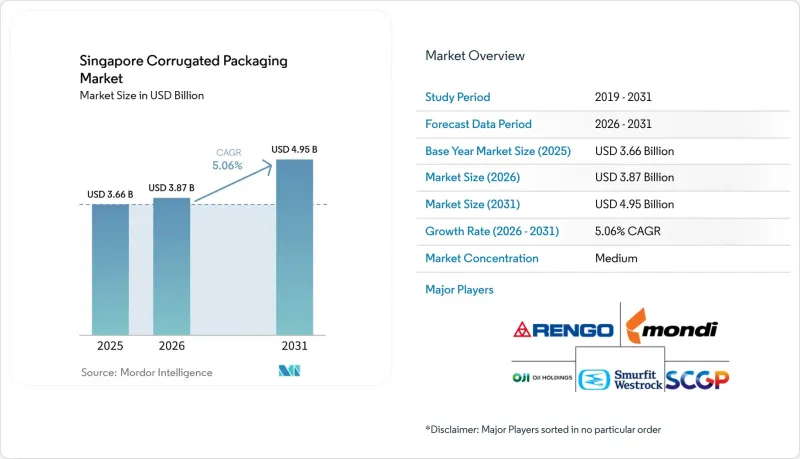

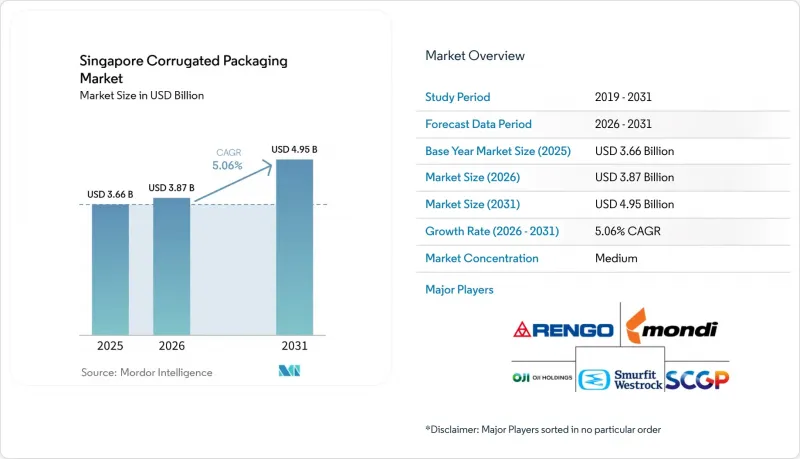

Mordor Intelligence에 의하면, 싱가포르 골판지 포장 시장 규모는 2025년에 36억 6,000만 달러로 평가되었고 2026년 38억 7,000만 달러에서 2031년까지 49억 5,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 5.06%를 나타낼 것으로 예측되고 있습니다.

본 보고서는 원료(버진 크라프트 라이너보드, 재생 라이너보드, 골판지 심재 등), 플루트 유형(A 플루트 등), 포장 유형(레귤러 슬롯 컨테이너 등), 벽 구조(싱글, 더블 등), 인쇄 기술(플렉소 인쇄 등), 그리고 최종 사용자 산업(가공 식품 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

싱가포르 골판지 포장 시장 동향과 인사이트

전자상거래의 급속한 성장이 골판지 상자 수요를 견인하고 있습니다.

일일 소포 처리량은 이미 지난 10년 동안의 최고치를 넘어섰으며, 주요 마켓플레이스들은 도시 지역 소비자들에게 재활용이 가능함을 나타내는 섬유 소재 우편 봉투의 사용을 강력히 권장하고 있습니다. SingPost의 1억 8,200만 싱가포르 달러(1억 3,900만 달러) 규모의 시설과, Maersk의 110만 제곱피트 규모의 ‘World Gateway II’를 포함한 새로운 자동화 허브는 각각 하루 10만 개의 소포를 분류하고 있으며, 치수 안정성이 높은 골판지 상자에 대한 수요를 확고히 하고 있습니다. 따라서 필름의 파손이나 치수 오차 위험을 감수할 수 없는 고속 컨베이어 시스템에서는 골판지가 표준적인 선택지로 자리 잡고 있습니다. 엄격한 공차 기준에 맞추어 좁은 홈이 있는 상자를 생산할 수 있는 변환 업체가 대규모 전자상거래 계약을 수주했습니다. 주문 현황을 명확히 파악할 수 있기 때문에 싱가포르의 높은 에너지 요금에도 불구하고 다품종 생산을 효율적으로 계획할 수 있습니다.

순환형 경제를 향한 정부의 추진

‘포장 보고 의무’에 따라, 매출액이 1,000만 싱가포르 달러(765만 달러)를 초과하는 기업은 자재의 환경 부하를 상세하게 보고해야 하며, 과도한 플라스틱 사용에 대해서는 사실상 벌금이 부과됩니다. ‘음료 용기 반환 제도’는 이러한 환원 논리를 확대하여, 브랜드가 재활용하기 쉬운 포장을 채택하도록 장려하고 있습니다. 기술 기준 109는 일반적인 재활용 가능성 지표를 제공하여, 조달 팀이 공급업체의 섬유 함유율을 비교 평가할 수 있도록 합니다. 이러한 지침을 도입함으로써, 컨버터는 하류 단계에서 재활용 크레딧을 획득할 수 있는 인증된 골판지에 대해 가격 프리미엄을 확보하고 있습니다. 규제 당국이 2026년까지 매립 처분되는 폐기물을 20% 감축하는 것을 목표로 하고 있기 때문에 수요는 이미 높은 회수율을 자랑하는 종이 기반 형태로 결정적으로 이동하고 있습니다.

변환기 업계에 닥친 부동산 및 공과금 가격 급등

JTC의 임대차 계약 갱신으로 인해 산업용 임대료가 높은 수준을 유지하고 있어, 투아스와 창이 주변에 밀집해 있는 중규모 골판지 제조업체들의 이익률이 압박을 받고 있습니다. SP 그룹이 2026년 2분기에 단행한 2.1%의 요금 인상은 싱가포르의 수입 천연가스 의존으로 인해 이미 치솟았던 투입 비용을 더욱 끌어올리고 있습니다. 대기업들은 옥상 태양광 발전 설비나 다년 계약 형태의 에너지 공급 계약을 통해 리스크를 헤지하고, 구조적인 비용 우위를 확보하고 있습니다. 자동화 비용을 상각할 수 없는 소규모 공장은 대량 발주 입찰에서 경쟁하기 어렵습니다. 이러한 압력은 합병을 촉진하고 있으며, 그 대표적인 사례가 타트 센이 유나이티드 패키징 인더스트리즈를 587만 달러에 인수한 사건입니다.

부문별 분석

재활용 라이너보드는 엄격한 순환형 경제 목표에 부합할 뿐만 아니라, 대량 운송업체에게 명확한 단위 비용상의 이점을 제공하기 때문에 2025년에는 싱가포르 골판지 포장 시장 점유율의 45.71%를 차지했습니다. 한편, 버진 크래프트 라이너 보드는 제약, 전자기기, 고급 식품 수출업체들이 진열대에서 브랜드 이미지를 높이기 위해 뛰어난 파열 강도와 완벽한 인쇄면을 요구하고 있기 때문에 2031년까지 연평균 성장률(CAGR) 6.13%로 성장할 것으로 전망됩니다. 이러한 고급 원자재의 채택이 급증함에 따라, 부가가치가 높은 등급의 싱가포르 골판지 포장 시장 규모는 꾸준히 확대되고 있으며, 가공업체들은 식품 접촉 및 의료 추적성에 관한 해외 규제 요건을 충족하면서 더 높은 이익률을 확보할 기회를 얻고 있습니다. 따라서, 동일한 생산 공정 내에서 재생 섬유와 버진 섬유를 유연하게 전환할 수 있는 컨버터는 전환으로 인한 가동 중단 시간을 늘리지 않으면서도 다양한 제품 포트폴리오를 아우를 수 있어, 다국적 바이어들에게 더 큰 매력을 발휘하고 있습니다.

버진크래프트의 도입은 하류 단계의 보증금 반환 물류 시스템과의 일관성을 유지하면서, 지속 가능하고 고성능인 포장재의 지역 디자인 연구소로서의 역할을 수행하려는 싱가포르의 포부와도 부합합니다. 이 도시 국가에 제품을 공급하는 제지 업체는 가볍으면서도 높은 강성을 갖춘 배합을 도입함으로써 이에 대응하고 있으며, 이를 통해 용기 무게를 두 자릿수 비율로 줄여, 결과적으로 항공 및 해상 운송 경로에서의 화물 배출량을 감축하고 있습니다. 표면 평활성이 향상됨에 따라 고해상도 잉크젯 인쇄가 가능해졌으며, 브랜드 매니저는 시각적인 타협 없이 장식용 접이식 상자 디자인을 골판지로 전환할 수 있게 되었습니다. 결국, 버진 크래프트에 대한 지속적인 수요 증가는 출하량 증가세가 둔화되더라도 수익을 끌어올리고, 컨버터를 재생 섬유의 원가 변동으로부터 보호하며, 싱가포르 골판지 포장 시장의 장기적인 안정성을 뒷받침하고 있습니다.

B 플루트는 2025년 싱가포르 골판지 포장 시장 출하량의 37.74%를 차지하며, 여전히 주력 제품으로 자리매김하고 있습니다. 그 이유는 3mm 두께가 풀필먼트 센터용 골판지 상자에서 완충성, 적층성, 경제성 간의 균형을 유지하기 때문입니다. 그러나 소매업체와 택배업체들은 부피 중량 요금을 절감하고 소매용 상자를 선반에 빽빽하게 진열하기 위해 0.8mm 두께의 F 플루트를 지정하는 경향이 강해지고 있으며, 이에 따라 2031년까지 F 플루트의 연평균 성장률(CAGR)은 6.91%를 나타낼 것으로 전망됩니다. 그래픽에 대한 기대가 높아지는 가운데, F 플루트의 매끄러운 표면은 워시보드 현상(물결 무늬)을 일으키지 않고 싱글 패스 잉크젯 인쇄가 가능하여, 퍼스널케어 제품 및 가전제품 패키지의 진열 시 어필력을 높이고 있습니다. 서보 제어식 골판지 제조기에 투자하는 가공업체는 현재 10분 이내에 플루트 형상을 전환할 수 있게 되어, 기계 가동률을 유지하면서 다양한 고객 사양에 대응할 수 있게 되었습니다.

F 플루트의 보급률이 높아짐에 따라, SKU별 색상 일관성을 보장하는 디지털 인쇄용 잉크 및 검사 시스템용 싱가포르 골판지 포장 시장 규모도 동시에 확대되고 있습니다. 소량 생산을 통해 플렉소 인쇄 특유의 제판 비용을 절감할 수 있으므로, 브랜드는 시즌 한정 디자인이나 인플루언서와의 공동 브랜딩을 유연하게 테스트할 수 있게 됩니다. 한편, B 플루트는 진열 시의 미관보다 팔레트의 안정성이 더 중요시되는 식품 및 음료 물류 분야에서 지배적인 위치를 유지하고 있으며, 라이너보드 공급업체에게 중요한 판매량을 확보하고 있습니다. 두 가지 플루트 스타일이 공존함으로써, 제조업체는 가격 체계를 세분화할 수 있게 되어, 고사양 그래픽이 필요한 마이크로 플루트 생산에는 프리미엄 가격을 책정하는 한편, 지역 재수출용 범용 상자에 대해서는 규모의 경제성을 유지할 수 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the singapore corrugated packaging market size was valued at USD 3.66 billion in 2025 and is expected to rise from USD 3.87 billion in 2026 to USD 4.95 billion by 2031, recording a 5.06% CAGR between 2026 and 2031.

This report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, and More), Flute Type (A Flute, and More), Packaging Type (Regular Slotted Containers, and More), Wall Type (Single, Double, and More), Printing Technology (Flexographic, and More), and End-User Industry (Processed Foods, and More). The Market Forecasts are Provided in Terms of Value (USD).

Singapore Corrugated Packaging Market Trends and Insights

E-Commerce Boom Driving Corrugated Box Demand

Daily parcel volumes now exceed prior decade highs, and leading marketplaces insist on fiber mailers that signal recyclability to urban consumers. New automated hubs, including SingPost's SGD 182 million (USD 139 million) facility and Maersk's 1.1 million ft2 World Gateway II, each sort 100,000 parcels daily, entrenching demand for dimensionally stable cartons. Corrugated therefore becomes the default for high-speed conveyor systems that cannot risk film tears or dimensional variance. Converters capable of producing narrow flute boxes at tight tolerances win the largest e-commerce contracts. Robust order visibility lets them schedule multi-grade runs efficiently despite Singapore's high energy tariffs.

Government Push Toward a Circular Economy

Mandatory Packaging Reporting requires companies with a turnover above SGD 10 million (USD 7.65 million) to detail their material footprints, effectively penalizing excessive plastic use. The Beverage Container Return Scheme extends the payback logic, encouraging brands to adopt packaging that is easily recyclable. Technical Reference 109 provides common recyclability metrics, enabling procurement teams to benchmark suppliers on fiber content. Integrating such guidelines, converters secure price premiums for certified corrugated that earn downstream recycling credits. As regulators target a 20% cut in waste sent to landfill by 2026, demand shifts decisively toward paper-based formats that already enjoy strong collection rates.

High Real-Estate and Utility Costs for Converters

JTC lease renewals keep industrial rents elevated, compressing margins for mid-sized corrugators clustered around Tuas and Changi. SP Group's 2.1% tariff increase in Q2 2026 further magnifies input costs, already elevated by Singapore's reliance on imported natural gas. Larger players hedge with rooftop solar arrays and multiyear energy contracts, securing a structural cost advantage. Smaller plants that are unable to amortize automation costs struggle to compete on high-volume tenders. These pressures catalyze mergers, exemplified by Tat Seng's recent USD 5.87 million acquisition of United Packaging Industries.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Singapore's Food Processing Exports

- Accelerating Adoption of Shelf-Ready Packaging by Retailers

- Volatility in Recycled Fiber Import Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled linerboard secured 45.71% of Singapore's corrugated packaging market share in 2025 because it aligns with strict circular-economy goals and offers a clear unit-cost edge for mass-volume shippers. Virgin Kraft linerboard, however, is projected to grow at a 6.13% CAGR through 2031 as pharmaceutical, electronics, and luxury-food exporters demand superior burst strength and pristine print surfaces that elevate brand perception at the shelf. This surge in premium substrate adoption steadily enlarges the Singapore corrugated packaging market size within value-added grades, giving converters opportunities to command higher margins while meeting overseas regulatory requirements for food contact and medical traceability. Converters that can hot-swap between recovered and virgin fibers during the same production run, therefore capture mixed portfolios without increasing changeover downtime, reinforcing their appeal to multinational buyers.

Virgin Kraft uptake also dovetails with Singapore's ambition to serve as a regional design lab for sustainable, high-performance packaging that still aligns with downstream deposit-return logistics. Mills serving the city-state have responded by introducing lightweight yet high-stiffness formulations that trim container weight by double-digit percentages, which subsequently reduces freight emissions on air and sea lanes. Enhanced surface smoothness supports high-definition inkjet graphics, allowing brand managers to shift decorative folding-carton programs onto corrugated without visual compromise. Ultimately, sustained virgin kraft gains lift revenue even when tonnage growth moderates, buffering converters against recycled-fiber cost volatility and underpinning long-term stability in the Singapore corrugated packaging market.

B flute remained the workhorse with 37.74% share of Singapore corrugated packaging market shipments in 2025 because its 3-millimeter profile balances cushioning, stacking, and economics for fulfillment-center cartons. Retailers and parcel carriers, however, increasingly specify 0.8-millimeter F flute to lower dimensional-weight charges and to nest retail cases tightly on shelf, which accelerates its 6.91% CAGR outlook through 2031. As graphics expectations climb, F flute's fine surface accepts single-pass inkjet printing without washboarding, enhancing shelf appeal for personal-care and consumer-electronics packages. Converters investing in servo-controlled corrugators can now switch flute profiles in under ten minutes, preserving machine utilization while satisfying diverse customer specifications.

Rising F flute penetration simultaneously expands the Singapore corrugated packaging market size for digital printing inks and inspection systems that guarantee color consistency across SKU variants. Brands gain agility to test seasonal artwork or influencer co-branding because small production lots avoid plate-making costs inherent to flexography. Meanwhile, B flute maintains dominance in food and beverage logistics where pallet stability outweighs shelf aesthetics, preserving volume critical mass for linerboard suppliers. The coexistence of both flute styles lets converters segment price architecture, charging premiums for high-graphic micro flute runs while protecting scale on commodity boxes destined for regional re-export.

List of Companies Covered in this Report:

- Smurfit Westrock plc

- Mondi Plc

- Oji Holdings Corporation

- SCG Packaging Public Company Limited

- Rengo Co., Ltd.

- International Paper Company

- Asia Pulp & Paper Co., Ltd.

- Nine Dragons Paper Holdings Limited

- Tat Seng Packaging Group Ltd.

- Greatprint Packaging Pte Ltd.

- Pacrimex Packaging Pte Ltd.

- Lee & Man Paper Manufacturing Ltd.

- New Toyo International Holdings Ltd.

- Orora Limited

- Visy Industries Holdings Pty Ltd.

- Sonoco Products Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce Boom Driving Corrugated Box Demand

- 4.2.2 Government Push Toward a Circular Economy

- 4.2.3 Growth in Singapore's Food Processing Exports

- 4.2.4 Accelerating Adoption of Shelf-Ready Packaging by Retailers

- 4.2.5 Automation Investments by Local Converters

- 4.2.6 Rising Demand for Sustainable Secondary Packaging

- 4.3 Market Restraints

- 4.3.1 High Real-Estate and Utility Costs for Converters

- 4.3.2 Volatility in Recycled Fiber Import Regulations

- 4.3.3 Competition From Flexible Plastic Formats in Fresh Produce

- 4.3.4 Limited Domestic Wood Pulp Resources

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Kraft Linerboard

- 5.1.2 Recycled Linerboard

- 5.1.3 Corrugating Medium

- 5.1.4 Semi-Chemical Fluting

- 5.1.5 Other Materials

- 5.2 By Flute Type

- 5.2.1 A Flute

- 5.2.2 B Flute

- 5.2.3 C Flute

- 5.2.4 E Flute

- 5.2.5 F Flute

- 5.3 By Packaging Type

- 5.3.1 Regular Slotted Containers

- 5.3.2 Die-Cut Custom Boxes

- 5.3.3 Folding Cartons

- 5.3.4 Point-of-Purchase Displays

- 5.3.5 Pallet Boxes

- 5.3.6 Other Packaging Types

- 5.4 By Wall Type

- 5.4.1 Single-Wall

- 5.4.2 Double-Wall

- 5.4.3 Triple-Wall

- 5.4.4 Single Face

- 5.5 By Printing Technology

- 5.5.1 Flexographic Printing

- 5.5.2 Digital Inkjet Printing

- 5.5.3 Litho-Lamination

- 5.5.4 Screen Printing

- 5.5.5 Other Printing Technologies

- 5.6 By End-User Industry

- 5.6.1 Processed Foods

- 5.6.2 Fresh Food and Produce

- 5.6.3 Beverages

- 5.6.4 Electrical Products

- 5.6.5 Personal Care and Cosmetics

- 5.6.6 E-Commerce Fulfillment Centers

- 5.6.7 Pharmaceuticals

- 5.6.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Smurfit Westrock plc

- 6.4.2 Mondi Plc

- 6.4.3 Oji Holdings Corporation

- 6.4.4 SCG Packaging Public Company Limited

- 6.4.5 Rengo Co., Ltd.

- 6.4.6 International Paper Company

- 6.4.7 Asia Pulp & Paper Co., Ltd.

- 6.4.8 Nine Dragons Paper Holdings Limited

- 6.4.9 Tat Seng Packaging Group Ltd.

- 6.4.10 Greatprint Packaging Pte Ltd.

- 6.4.11 Pacrimex Packaging Pte Ltd.

- 6.4.12 Lee & Man Paper Manufacturing Ltd.

- 6.4.13 New Toyo International Holdings Ltd.

- 6.4.14 Orora Limited

- 6.4.15 Visy Industries Holdings Pty Ltd.

- 6.4.16 Sonoco Products Company

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment