|

시장보고서

상품코드

2063710

이탈리아의 접이식 카톤 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Italy Folding Carton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

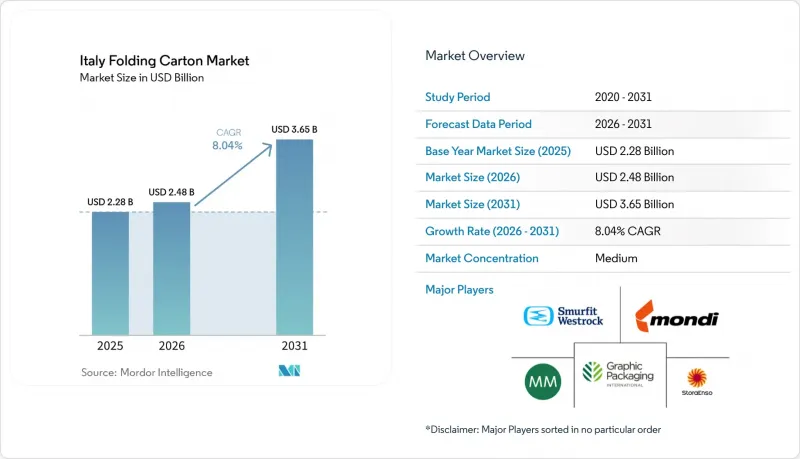

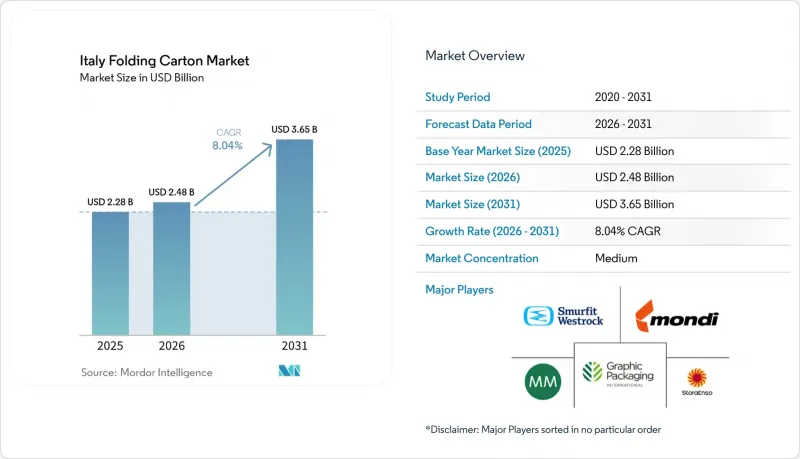

Mordor Intelligence에 의하면, 이탈리아의 접이식 카톤 시장 규모는 2025년 22억 8,000만 달러로 평가되었습니다. 2026년에는 24억 8,000만 달러로 확대되어 2031년까지 36억 5,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR은 8.04%를 나타낼 전망입니다.

본 보고서는 원료 유형(고형 표백 황산 펄프, 접이식 골판지, 코팅 미표백 크라프트지, 화이트라인 칩보드 등), 인쇄 기술(오프셋 인쇄, 플렉소 인쇄, 디지털 인쇄 등), 최종 사용자 산업(식품 및 음료, 헬스케어 및 의약품, 퍼스널케어 및 화장품 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

이탈리아의 접이식 카톤 시장 동향 및 인사이트

재활용 가능한 포장에 대한 선호도 증가

CONAI가 부과하는 확대 생산자 책임(EPR) 수수료는 재활용이 불가능한 구조에 대해 벌금을 부과하기 때문에 브랜드 소유자들은 관세가 더 낮은 단일 소재 골판지 상자로 라미네이트 처리된 플라스틱을 빠르게 대체하고 있습니다. 소비자 조사에 따르면, 이탈리아인의 77%가 구매 결정 시 포장의 지속가능성을 고려하고 있으며, 이에 따라 소매업체들은 폐기 방법이 명확하게 표시된 SKU를 우선적으로 취급하고 있습니다. 페드리고니(Fedrigoni)가 2025년에 Papkot에 투자한 것은 이 변환업체가 내유성을 유지하면서도 재활용 가능성 지침을 충족하는 PFAS 무함유 코팅재를 어떻게 상용화하고 있는지를 보여줍니다. 국가 부흥 계획에서는 재활용 센터와 디지털 추적 시스템에 15억 유로(17억 달러)가 배정되어 있으며, 이 프로젝트가 가동되면 사용 후 섬유공급량이 증가하게 될 것입니다. 이러한 요인들로 인해, 적어도 2031년까지는 기판 수요가 시장 평균을 상회하는 수준을 유지할 것으로 예측됩니다.

프리미엄 지향 FMCG 제품의 성장

고급 식품, 음료, 화장품 브랜드에서는 핫 포일 스탬핑, 엠보싱 가공, 소프트 터치 니스 가공에 내성이 있는 고형 표백 황산 펄프(SBS)나 메탈라이즈드 보드의 사용이 점점 더 늘어나고 있습니다. 25억 유로(28억 3,000만 달러) 규모의 레디밀 키트에는 내유성이 있고 전자레인지 사용이 가능한 골판지가 요구되며, 이러한 골판지는 범용 등급에 비해 두 자릿수의 가격 프리미엄이 붙습니다. 소매업체의 자체 브랜드(PB) 시장 침투율은 2024년에 32%에 달했으나, 슈퍼마켓들은 패키지 디자인을 개선함으로써 프리미엄 제품군을 차별화하고 있습니다. Bobst사의 QualiTronic 시스템 등 인라인 분광광도계와 자동 검사 장치를 도입한 컨버터는 고급 브랜드가 요구하는 것보다 더 엄격한 색차 허용 범위를 실현하고 있습니다. 재량 지출이 회복됨에 따라, 하이데코(고급 장식) 부문의 출하량은 이탈리아의 접이식 카톤 시장 전체를 웃도는 속도로 증가할 것으로 예측됩니다.

버진 펄프 가격 변동

2024년에는 크래프트 라이너 가격이 20% 이상 상승했으며, 북유럽산 표백 침엽수 펄프 가격도 17.6% 상승했습니다. 전가 조항이 현물 가격보다 최대 90일 늦게 적용되기 때문에 컨버터의 이익률은 압박을 받고 있습니다. 재활용지 함유율 의무화로 인해 폐지 시장을 둘러싼 경쟁이 치열해지고 있으며, 2025년 북부 이탈리아의 폐지 가격은 톤당 평균 120-150유로(136-170달러)였습니다. 남부 지역의 회수율이 낮아 제지 회사는 베일을 북쪽에서 남쪽으로 트럭으로 운송할 수밖에 없어, 물류 비용이 추가로 발생하고 있습니다. RDM이나 Burgo와 같은 수직 통합형 그룹은 자사가 소유한 펄프 및 탈색 설비를 통해 가격 변동 위험을 헤지하고 있지만, 많은 중소기업은 여전히 가격을 수동적으로 받아들일 수밖에 없는 처지에 머물러 있어 투자 의욕이 위축되고 있습니다.

부문별 분석

2025년, 이탈리아의 접이식 카톤 시장 규모 중 접이식 보드가 38.56%를 차지했습니다. 이는 주류 식품 용도에서 강성, 인쇄 적합성, 비용 간의 균형이 잘 잡혀 있어 선호되고 있습니다. 화장품 및 제약 브랜드들이 핫포일, 엠보싱 가공, 배리어 코팅에 적합한 고광택 표면을 요구함에 따라, 고형 표백 황산 펄프 시장은 연평균 성장률(CAGR) 9.21%를 나타낼 것으로 전망됩니다. 재생 섬유로 제조되는 화이트라인 칩보드는 표면의 미관이 부차적인 요소인 전자기기 및 가정용품 분야에서 수요가 증가하고 있습니다. 2026년에 출시된 RDM사의 ‘Vincicoat PLUS’는 85%의 재생 섬유를 함유하면서도 15-20% 더 높은 강도를 실현하여, 경량적이고 순환형인 기재 개발을 위한 혁신의 발자취를 보여주고 있습니다.

재생 섬유 함유율이 높은 제품을 생산하기 위해 제지 공장을 재구축하고 있는 각 제조업체는 PPWR이 제시한 ‘사용 후 제품 유래 재생 섬유 30%’라는 목표를 선제적으로 이행하고 있으며, 이러한 변화에 따라 검증된 폐쇄형 순환 섬유를 공급하는 제지 공장으로 조달처가 재편될 것으로 예측됩니다. 경쟁의 초점은 재활용성을 유지하는 코팅으로 옮겨가고 있으며, Papkot사의 나노 구조 라이너는 내유성을 유지하면서도 PFAS를 대체하는 소재로 자리 잡고 있습니다. 비셀룰로오스층이 5% 미만인 기질은 CONAI의 최저 요금 구간에 해당하기 때문에 구매자들은 분산 코팅이나 바이오 대체재로 전환하고 있습니다. 브랜드 소유주들이 탄소 발자국을 공개하는 가운데, 제조 단계까지의 배출량 데이터를 제공하는 제조업체가 조달 과정에서 우선적으로 선정됨에 따라, 이탈리아의 접이식 카톤 시장에서 재활용률이 높은 등급의 제품을 뒷받침하는 선순환이 강화되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the italy folding carton market size is expected to increase from USD 2.28 billion in 2025 to USD 2.48 billion in 2026 and reach USD 3.65 billion by 2031, growing at a CAGR of 8.04% over 2026-2031.

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and More), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, and More), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, and More). The Market Forecasts are Provided in Terms of Value (USD).

Italy Folding Carton Market Trends and Insights

Increasing Preference for Recyclable Packaging

Extended Producer Responsibility fees imposed by CONAI penalize non-recyclable structures, so brand owners are rapidly substituting laminated plastics with mono-material cartons that qualify for lower tariffs. Consumer polling shows that 77% of Italians factor packaging sustainability into their purchase decisions, prompting retailers to favor SKUs with clear disposal labels. Fedrigoni's 2025 investment in Papkot demonstrates how converters are commercializing PFAS-free coatings that pass recyclability guidelines while retaining grease resistance. The national recovery plan earmarks EUR 1.5 billion (USD 1.70 billion) for reuse centers and digital traceability, which will raise post-consumer fiber availability once projects come online. These factors are expected to underpin above-trend substrate demand through at least 2031.

Growth of Premium-Positioned FMCG Products

Premium food, beverage, and cosmetics lines increasingly specify solid bleached sulfate or metalized boards that tolerate hot-foil stamping, embossing, and soft-touch varnishes. Ready-to-eat meal kits valued at EUR 2.5 billion (USD 2.83 billion) require grease-resistant, microwave-safe cartons that command double-digit price premiums over commodity grades. Retail private-label penetration reached 32% in 2024, yet supermarkets differentiate premium tiers through upgraded pack aesthetics. Converters that add inline spectrophotometers and automated inspection, such as Bobst QualiTronic systems, achieve the tighter color tolerances demanded by luxury brands. As discretionary spending recovers, volumes in high-decor segments are expected to outpace the overall Italy folding carton market.

Volatility in Virgin Fiber Pulp Prices

Kraftliner rose more than 20% in 2024, while northern bleached softwood pulp climbed 17.6%, compressing converter margins because pass-through clauses lag spot prices by up to 90 days. Recycled-content mandates intensify competition for recovered paper, which averaged EUR 120-150 (USD 136-170) per tonne in Northern Italy during 2025. Southern regions' lower collection rates force mills to truck bales north-to-south, adding logistics premiums. Vertically integrated groups like RDM and Burgo hedge volatility through captive pulp and deinking capacity, but most SMEs remain price takers, dampening investment appetite.

Other drivers and restraints analyzed in the detailed report include:

- E-commerce Boom and Small-Batch Custom Runs

- Brand Owner Migration from Plastics to Paperboard

- Capital-Intensive Nature of High-End Digital Presses

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Folding boxboard accounted for 38.56% of the Italian folding carton market size in 2025, favored for balanced stiffness, printability, and cost in mainstream food applications. Solid bleached sulfate is forecast to post a 9.21% CAGR as cosmetics and pharma brands demand high-brightness surfaces compatible with hot-foil, emboss, and barrier coatings. White line chipboard, produced from recycled fibers, is gaining traction in electronics and household goods where surface aesthetics are secondary. RDM's Vincicoat PLUS, launched in 2026, incorporates 85% recycled fibers yet delivers 15-20% greater strength, illustrating the innovation trajectory toward lightweight, circular substrates.

Producers recasting mills for higher recycled-content output are pre-positioning for the PPWR's 30% post-consumer target, a shift expected to realign procurement toward mills offering validated closed-loop fibers. Competitive emphasis is moving to coatings that preserve recyclability, with Papkot's nanostructured liner replacing PFAS while maintaining grease resistance. Substrates with non-cellulosic layers below 5% qualify for CONAI's lowest fee bracket, nudging buyers toward dispersion-coated or bio-based alternatives. As brand owners publish carbon footprints, mills offering cradle-to-gate emissions data gain sourcing preference, reinforcing a virtuous cycle that favors high-recycled-content grades within the Italy folding carton market.

List of Companies Covered in this Report:

- Smurfit WestRock plc

- Mayr-Melnhof Karton AG

- Graphic Packaging International LLC

- International Paper Company

- RDM Group

- GPack Group

- Lucaprint Group

- Box Marche SpA

- Pozzoli SpA

- Burgo Group S.p.A.

- Metsa Board Corporation

- Schur Pack Italy Srl

- Stora Enso Oyj

- Fedrigoni Group

- Seda International Packaging Group SpA

- Artigrafiche Reggiane & Lai SpA

- Italpack Cartons Srl

- Mondi plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Preference for Recyclable Packaging

- 4.2.2 Growth of Premium-Positioned FMCG Products

- 4.2.3 E-commerce Boom and Small-Batch Custom Runs

- 4.2.4 Brand Owner Migration From Plastics to Paperboard

- 4.2.5 Expansion of Italy's Ready-to-Eat Meal Segment

- 4.2.6 Retailer Demand for Shelf-Ready Multipacks

- 4.3 Market Restraints

- 4.3.1 Volatility in Virgin Fiber Pulp Prices

- 4.3.2 Capital-Intensive Nature of High-End Digital Presses

- 4.3.3 Limited Folding Carton Recycling Infrastructure in Southern Italy

- 4.3.4 Stringent Food-Contact Compliance Costs for SMEs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-commerce and Retail-ready Packaging

- 5.3.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Smurfit WestRock plc

- 6.4.2 Mayr-Melnhof Karton AG

- 6.4.3 Graphic Packaging International LLC

- 6.4.4 International Paper Company

- 6.4.5 RDM Group

- 6.4.6 GPack Group

- 6.4.7 Lucaprint Group

- 6.4.8 Box Marche SpA

- 6.4.9 Pozzoli SpA

- 6.4.10 Burgo Group S.p.A.

- 6.4.11 Metsa Board Corporation

- 6.4.12 Schur Pack Italy Srl

- 6.4.13 Stora Enso Oyj

- 6.4.14 Fedrigoni Group

- 6.4.15 Seda International Packaging Group SpA

- 6.4.16 Artigrafiche Reggiane & Lai SpA

- 6.4.17 Italpack Cartons Srl

- 6.4.18 Mondi plc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment