|

시장보고서

상품코드

2063952

중출력 LED 패키지 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Mid-Power LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

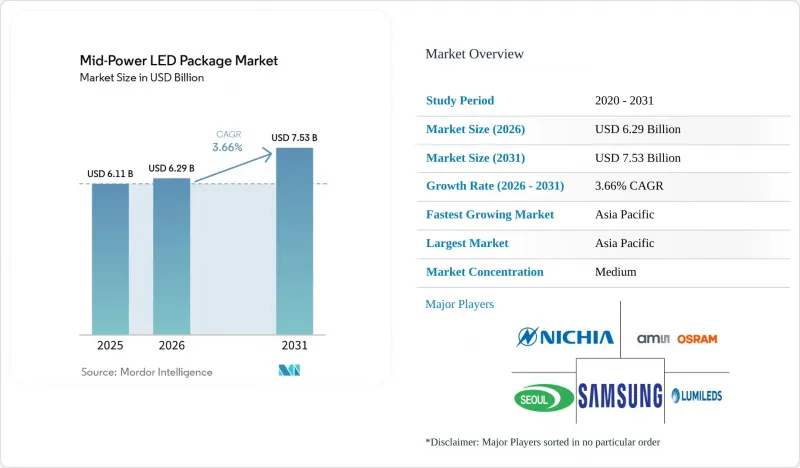

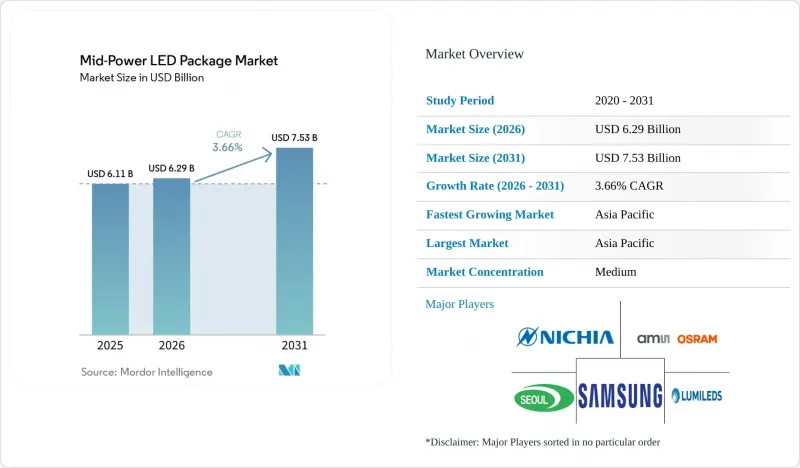

Mordor Intelligence에 의하면, 중출력 LED 패키지 시장 규모는 2025년 61억 1,000만 달러로 평가되었고, 2026년 62억 9,000만 달러로 추정되고, 2031년까지 75억 3,000만 달러로 확대될 전망이며, 2026-2031년 CAGR 3.66%를 나타낼 것으로 예측됩니다.

본 보고서는 출력 범위별(0.2W-0.5W 및 0.5W-1W), 패키지 아키텍처별(2835, 3014 등을 포함한 SMD, 기타, CSP), 용도별(일반 조명, 자동차용 조명, 디스플레이 및 백라이트, 기타), 지역별(북미, 유럽, 아시아태평양, 남미, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

세계의 중출력 LED 패키지 시장 동향 및 분석

에너지 절약형 일반 조명에 대한 수요 급증

2025년, 중국의 조명 기구 시장에서 LED 기술이 큰 점유율을 차지했습니다. 또한, 2026년 1월부터 캐나다에서 시행된 수은계 소형 형광등의 전국적인 사용 금지 조치로 인해 북미 전역에서 이와 유사한 전환이 가속화되고 있습니다. 2028년 7월까지 일반용 조명 기구에 대해 120루멘/와트의 광속 효율을 의무화하는 미국 에너지부의 기준은 할로겐 제품의 수명을 더욱 단축시키고 있습니다. 전 세계 주거용 조명의 약 30%는 여전히 교체해야 하며, 게다가 10년 전에 설치된 1세대 LED의 15%가 교체 주기에 접어들게 됩니다. 이를 통해 비용 효율성이 뛰어난 중출력 패키지용 수십억 개 규모의 잠재 시장이 창출될 것입니다. 이러한 램프에는 기존 인쇄회로기판 제조 라인과 원활하게 통합될 수 있는 2835 및 3030 표면 실장형 구성이 적합합니다. 정부의 리베이트 프로그램과 전력 회사의 인센티브 덕분에 조달은 계속해서 ENERGY STAR 인증 제품으로 유도되고 있으며, 이로 인해 검증된 루멘 유지 성능을 갖춘 제품에 대한 수요가 증가함에 따라 대량 생산되는 A형 램프와 선형 용도의 중출력 제품의 입지가 더욱 공고해지고 있습니다.

자동차용 LED 헤드램프의 급속한 확산

UN ECE R149의 시행과 FMVSS 108의 채택에 따라, 2025년에는 주요 자동차 시장에서 적응형 주행 빔 헤드램프 도입을 위한 법적 기반이 마련되었습니다. 엔트리 모델에는 24-48개의 제어 가능한 픽셀이 탑재되어 있지만, 플래그십 모델의 경우 100픽셀을 초과하며, 이로 인해 순방향 전압과 색도 빈의 정밀도가 더욱 요구됨에 따라 고휘도 중출력 어레이에 대한 수요를 견인하고 있습니다. 전기차 제조업체들은 브랜드 정체성을 강화하고 효율성을 높이기 위해 시그니처 라이팅을 우선시하고 있으며, 과도한 열 부하를 유발하지 않으면서 웰컴 애니메이션이나 차선 안내를 표시하기 위해 중출력 매트릭스 시스템을 채택하고 있습니다. 자동차 등급 0의 온도 범위에서 수행되는 인증 사이클에서는 접합부 온도가 105°C 전후일 때의 패키지 신뢰성이 검증되었으며, 이에 따라 세라믹 기반 중출력 다이에 대한 선호도가 더욱 높아지고 있습니다. ams OSRAM 등 Tier 1 공급업체들은 확립된 AEC-Q102 인증을 활용하여 가격 프리미엄을 확보하는 한편, 비용 효율적으로 화소 밀도를 높이는 것을 목표로 하는 OEM 업체들에 대해 안정적인 공급을 유지하고 있습니다.

치열해지는 경쟁이 이익률을 압박하고 있습니다.

2026년 1월, MLS와 Kinglight를 비롯한 중국의 LED 패키지 기업들은 견적 가격을 5-10% 인상했습니다. 이번 가격 조정은 수년에 걸친 지속적인 가격 하락에 따른 것으로, 많은 중견 기업의 수익성을 크게 압박해 왔습니다. 이번 가격 인상은 주로 패키지 비용 전체의 상당 부분을 차지하는 금, 은 구리의 원자재 가격 급등에 기인한 것입니다. 그러나 표준 2835 LED 패키지공급 과잉이 지속되고 있으며, 고객의 대체 장벽이 낮아 가격 결정력이 제한받고 있어, 이러한 가격 인상의 지속가능성은 여전히 불투명한 상태입니다. 그 결과, 제품 차별화를 통해 비용 상승을 상쇄할 수 없는 기업들은 시장에서 철수하거나 합병 및 인수와 같은 통합 전략을 추진하고 있습니다. 한편, 살아남은 기업들은 자동차용 조명, 원예, MiniLED 백라이트 등 부가가치가 높은 분야로 주력하고 있습니다. 이러한 부문에서는 더 엄격한 성능 요건이 적용되므로, 보다 안정적인 가격 책정 및 장기적인 공급 계약이 가능해집니다.

부문별 분석

0.5W-1W 이하 대역은 2025년에 중출력 LED 패키지 시장 점유율의 62.80%를 차지한 것으로 평가되었으며, 4.12%로 예측되는 연평균 성장률(CAGR)은 일반 조명 개조 시장과 신흥 자동차용 매트릭스 어레이 시장에서 지속적인 주도적 입지를 뒷받침하고 있습니다. 이 전력 등급은 드라이버 집적회로의 제약 조건을 충족하며, 열 부하를 관리 가능한 다이 면적 전체에 분산시켜, 대중화 가격에도 불구하고 공급업체의 이익률을 유지할 수 있는 매력적인 루멘당 단가를 유지하고 있습니다. 2026년에 증가가 예상되는 엔트리 레벨 적응형 주행 빔 모듈은 주로 0.5W급 소자를 지정하고 있으며, 접합부 온도를 상승시키지 않으면서 48픽셀을 초과하는 화소 수를 실현함으로써 자동차 헤드램프 시장에서 이 부문의 중요성을 더욱 높이고 있습니다. 반면, 0.2W-0.5W 부문은 표시등이나 웨어러블 기기에 사용되고 있지만, 더 작은 실적로 동등한 광속을 제공하는 칩 스케일 패키지로의 대체가 진행되면서 성장세가 주춤하고 있습니다.

자동차용 조명에서 적용되는 엄격한 순방향 전압 및 색도 비닝 허용오차로 인해, 중급 패키지에서는 보다 정밀한 전기적 선별과 색상 분산 저감이 요구되며, 프리미엄 모델에서는 ±0.1 V의 비닝과 2-3 맥아담 단계가 요구됩니다. 직접 구리 본딩 및 낮은 보이드율의 SAC305 납땜과 같은 열 설계 개선을 통해, 가속 열화 시험에서 L70 수명이 5만 시간을 초과하여 OEM의 보증 조건을 충족하고 있습니다. MiniLED TV가 주류 가격대에 보급됨에 따라, 0.5W 디바이스도 하이엔드 백라이트에 채택되기 시작했으며, 광속, 효율, 픽셀 피치의 균형이 잘 잡혀 있습니다. 이처럼 미드레인지 제품은 저출력 CSP 및 고출력 COB(Chip-on-Board) 대체 제품 시장 진출을 저지하는 한편, 중출력 LED 패키지 시장 규모 확대를 지속적으로 뒷받침하고 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 68.90%를 차지했으며, 중국, 대만, 한국, 일본의 웨이퍼부터 모듈에 이르는 긴밀한 생태계의 뒷받침을 받아 2031년까지 연평균 성장률(CAGR) 5.10%를 유지할 전망입니다. 2025년 4월 중국이 이트륨에 대한 라이선스 규제를 도입함에 따라 산화물 가격이 급등했고, 패키지 제조업체들은 미국과 유럽에서 대체 정제원을 모색할 수밖에 없게 되었습니다. 한국은 수익성이 높은 기판 및 카메라 모듈 사업을 전략적으로 확대하고 있으며, 그 일례로 2026년 완공을 예정하고 있는 LG이노텍의 6,000억 원(4억 900만 달러) 규모의 구미 프로젝트가 있습니다. 이처럼, 해당 지역의 클러스터는 일반 상품과 프리미엄 상품 두 부문 모두를 뒷받침하는 기반이 되고 있습니다.

북미와 유럽은 절대적인 수량 면에서는 적지만, 캘리포니아주의 ‘Title 24-2025’와 같은 엄격한 에너지 규제나, 저효율 램프 사용을 금지하는 에코디자인 지침 덕분에 1루멘당 매출총이익률은 높은 임베디드니다. 국내 에피택셜 생산 능력이 부족하기 때문에 부품 공급의 대부분은 여전히 아시아에 의존하고 있지만, 2026년 2월 Cree Lighting이 체결한 수탁 제조 계약은 국내에서의 통합이 서서히 진행되고 있음을 시사합니다. 성과 기반 계약을 통해 자금을 조달한 지자체의 가로등 교체 사업에서는 나트륨 램프의 교체가 진행되고 있으며, 서지 보호 기능이 내장된 중출력 모듈에 적합한 커넥티드 조명의 요건이 추가되고 있습니다.

남미, 중동 및 아프리카에서는 보급률이 낮아, 많은 지역에서 LED 채택률이 50% 이하에 그치고 있습니다. 인도에서는 Energy Efficiency Services Limited를 통해 독자적인 대량 조달 모델이 운영되고 있습니다. 해당 기관은 월정액 서비스 요금으로 조명 기구를 임대하고 있으며, 가격 민감도를 높이는 동시에 출력 및 수명 기준을 충족하는 공급업체에 대량으로 발주하고 있습니다. 이러한 신흥 지역에서는 검증된 2835 패키지가 여전히 주류를 이루고 있으며, 중출력 LED 패키지 시장의 점진적인 성장은 기술적 도약에 기인하기보다는 LED로의 초기 전환이나 전력망의 신뢰성에 대한 고려에 기인하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the mid-power LED package market size is projected to expand from USD 6.11 billion in 2025 and USD 6.29 billion in 2026 to USD 7.53 billion by 2031, registering a CAGR of 3.66% between 2026- 2031.

This report is Segmented by Power Range (0. 2W-0. 5W and 0. 5W- Less Than 1W), Package Architecture (SMD Including 2835, 3014, and More, and Others; CSP), Application (General Lighting, Automotive Lighting, Display and Backlighting, and More), and Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Mid-Power LED Package Market Trends and Insights

Surging Demand for Energy-Efficient General Lighting

LED technology supplied a significant share of China's lamp stock in 2025, and Canada's nationwide ban on mercury-based compact fluorescent lamps, which began in January 2026, is accelerating a similar transition across North America. The U.S. Department of Energy standard requiring 120 lumens-per-watt efficacy for general service lamps by July 2028 further compresses the viable window for halogen products. Roughly 30% of the global residential base still needs to convert, and another 15% of first-generation LEDs installed a decade ago will enter the replacement cycle, supplying a multibillion-unit addressable pool for cost-efficient mid-power packages. These lamps favor 2835 and 3030 surface-mount configurations that integrate seamlessly with legacy printed-circuit manufacturing lines. Government rebate programs and electric-utility incentives continue to steer procurement toward ENERGY STAR-qualified devices, reinforcing demand for packages with proven lumen-maintenance credentials and solidifying mid-power incumbency in volume A-lamp and linear applications.

Rapid Expansion of Automotive LED Headlamps

UN ECE R149 enforcement and FMVSS 108 adoption unlocked legal pathways for adaptive driving-beam headlamps across major automotive regions in 2025. Entry variants integrate 24-48 controllable pixels, whereas flagship trims exceed 100 pixels, dictating tighter forward-voltage and chromaticity bins and driving volumes for high-luminance mid-power arrays. Electric vehicle makers prioritize signature lighting for brand identity and efficiency, using mid-power matrix systems to display welcome animations and lane guides without excessive thermal load. Qualification cycles in automotive-grade 0 temperature ranges validate package reliability at junction temperatures near 105 °C, reinforcing the preference for ceramic-based mid-power dies. Tier-one suppliers such as ams OSRAM leverage established AEC-Q102 credentials to command price premiums while maintaining supply security for original equipment manufacturers looking to scale pixel densities cost-effectively.

Intensifying Price Competition Squeezing Margins

In January 2026, Chinese LED packaging companies, including MLS and Kinglight, increased quoted prices by 5-10%. This adjustment followed several years of sustained price declines that significantly compressed profitability for many mid-sized firms. The price increase is primarily due to rising input costs for gold, silver, and copper, which account for a substantial portion of overall packaging expenses. However, the sustainability of these price increases remains uncertain due to persistent oversupply in standard 2835 LED packages and the low switching barriers for customers, which limit pricing power. As a result, companies that are unable to balance rising costs through product differentiation are either exiting the market or pursuing consolidation strategies such as mergers and acquisitions. At the same time, surviving players are shifting their focus toward higher-value applications, including automotive lighting, horticulture, and MiniLED backlighting. These segments impose stricter performance requirements, enabling more stable pricing and longer-term supply agreements.

Other drivers and restraints analyzed in the detailed report include:

- MiniLED Adoption in TVs Boosting Mid-Power Backlights

- Cost Declines from Flip-Chip and CSP Manufacturing

- Thermal Management Limits for Higher Watt Density

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 0.5 W- less than 1 W band accounted for 62.80% of mid-power LED package market share in 2025, and its 4.12% forecast CAGR underlines sustained leadership in general lighting retrofits and emerging automotive matrix arrays. This power class aligns with driver-integrated circuit constraints, spreads thermal load across a manageable die area, and maintains compelling cost-per-lumen ratios that preserve vendor margin despite commodity pricing. Entry-level adaptive driving-beam modules, now projected to increase in 2026, predominantly specify 0.5 W-range devices that achieve pixel counts above 48 without exacerbating junction temperature, reinforcing the segment's relevance in vehicle headlamps. In contrast, the 0.2 W-0.5 W segment serves indicators and wearables but faces substitution by smaller chip-scale packages offering similar flux within reduced footprints, restricting its growth pace.

Automotive lighting's stringent forward-voltage and chromaticity binning tolerances are pushing mid-range packages toward finer electrical screening and narrower hue dispersion, with premium models demanding bins of +-0.1 V and two-to-three MacAdam steps. Thermal upgrades such as direct copper bonding and low-void SAC305 soldering uphold L70 life beyond 50 000 h under accelerated-aging protocols, meeting original equipment manufacturer warranty terms. As MiniLED televisions penetrate mainstream price tiers, 0.5 W devices are also appearing in high-end backlights, balancing flux, efficiency, and pitch. The mid-range thus continues to anchor the mid-power LED package market size expansion while holding off encroachment from both lower-power CSPs and higher-power chip-on-board alternatives.

Geography Analysis

The Asia-Pacific accounted for 68.90% of sales in 2025 and is sustaining a 5.10% CAGR through 2031, buoyed by dense wafer-to-module ecosystems in China, Taiwan, South Korea, and Japan. China's April 2025 export-licensing rule on yttrium triggered a significant spike in oxide prices, compelling packagers to explore alternative refining sources in the United States and Europe. South Korea is strategically expanding higher-margin substrate and camera-module lines, evidenced by LG Innotek's 600 billion KRW (USD 409 million) Gumi project slated for completion in 2026. The regional cluster thus anchors both commodity and premium segments.

North America and Europe contribute lower absolute volumes yet deliver higher gross margins per lumen thanks to stringent energy codes, such as California Title 24-2025, and eco-design directives that disallow low-efficiency lamps. Domestic epitaxial capacity is thin, so most component supply remains Asia-sourced, although Cree Lighting's contract manufacturing deal in February 2026 signals incremental onshore integration. Municipal streetlight retrofits financed through performance-based contracts continue to replace sodium lamps, adding connected-lighting provisions that favor mid-power modules with integrated surge protection.

South America, the Middle East, and Africa trail in penetration, with LED adoption under 50% in many jurisdictions. India operates a unique bulk-procurement model through Energy Efficiency Services Limited, which leases fixtures under monthly service fees, driving price sensitivity while awarding large volumes to suppliers that meet output and lifetime standards. In these emerging territories, proven 2835 packages retain dominance, and the mid-power LED package market derives incremental growth less from technological leapfrogging and more from first-time conversions and grid-reliability considerations.

- Nichia Corporation

- Samsung Electronics Co., Ltd.

- OSRAM GmbH

- Seoul Semiconductor Co., Ltd.

- Lumileds Holding B.V.

- Cree LED, Inc.

- LG Innotek Co., Ltd.

- Lite-On Technology Corporation

- Everlight Electronics Co., Ltd.

- NationStar Optoelectronics Co., Ltd.

- Dominant Opto Technologies Sdn. Bhd.

- Harvatek Corporation

- Toyoda Gosei Co., Ltd.

- Honglitronic Co., Ltd.

- MLS Co., Ltd. (Forest Lighting)

- Refond Optoelectronics Co., Ltd.

- Kingbright Electronic Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for Energy-Efficient General Lighting

- 4.2.2 Rapid Expansion of Automotive LED Headlamps

- 4.2.3 MiniLED Adoption in TVs Boosting Mid-Power Backlights

- 4.2.4 Cost Declines From Flip-Chip and CSP Manufacturing

- 4.2.5 Government Phasing-Out of Halogen Lamps

- 4.2.6 Growing Smart-City Streetlighting Projects

- 4.3 Market Restraints

- 4.3.1 Intensifying Price Competition Squeezing Margins

- 4.3.2 Thermal Management Limits for Higher Watt Density

- 4.3.3 Supply Chain Volatility of Key Phosphor Materials

- 4.3.4 Regulatory Push Toward Chip-on-Board Alternatives

- 4.4 Industry Supply-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Power Range

- 5.1.1 0.2W - 0.5W

- 5.1.2 0.5W - Less Than 1W

- 5.2 By Package Architecture

- 5.2.1 SMD (Surface Mount Device)

- 5.2.1.1 2835

- 5.2.1.2 3014

- 5.2.1.3 3030

- 5.2.1.4 Others (3528, 3020, 5050, etc.)

- 5.2.2 CSP (Chip Scale Package)

- 5.2.1 SMD (Surface Mount Device)

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display and Backlighting

- 5.3.4 Specialty / Niche

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Southeast Asia

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.5 Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Samsung Electronics Co., Ltd.

- 6.4.3 OSRAM GmbH

- 6.4.4 Seoul Semiconductor Co., Ltd.

- 6.4.5 Lumileds Holding B.V.

- 6.4.6 Cree LED, Inc.

- 6.4.7 LG Innotek Co., Ltd.

- 6.4.8 Lite-On Technology Corporation

- 6.4.9 Everlight Electronics Co., Ltd.

- 6.4.10 NationStar Optoelectronics Co., Ltd.

- 6.4.11 Dominant Opto Technologies Sdn. Bhd.

- 6.4.12 Harvatek Corporation

- 6.4.13 Toyoda Gosei Co., Ltd.

- 6.4.14 Honglitronic Co., Ltd.

- 6.4.15 MLS Co., Ltd. (Forest Lighting)

- 6.4.16 Refond Optoelectronics Co., Ltd.

- 6.4.17 Kingbright Electronic Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment