|

시장보고서

상품코드

2064020

아시아태평양의 백색 LED 패키지 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Asia-Pacific White LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

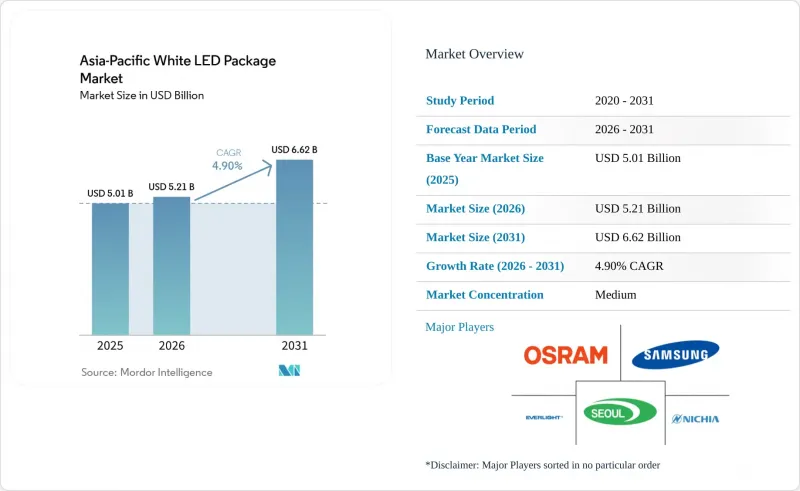

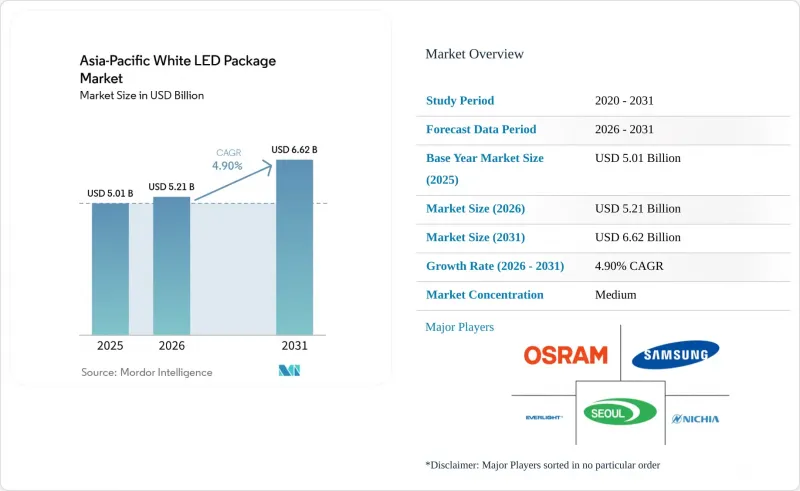

Mordor Intelligence에 의하면, 아시아태평양 백색 LED 패키지 시장 규모는 2025년 50억 1,000만 달러로 평가되었고, 2026년에는 52억 1,000만 달러로 추정되고, 2026-2031년 CAGR 4.9%로 성장을 지속할 전망이며, 2031년에는 66억 2,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 패키지 아키텍처별(SMD, COB, CSP, 플립칩 LED 패키지), 출력 등급별(저출력, 중출력, 고출력), 용도별(일반 조명, 자동차용 조명, 디스플레이 및 백라이트, 특수 용도), 국가 및 지역별(중국, 일본, 인도, 동남아시아, 기타 아시아태평양)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

아시아태평양의 백색 LED 패키지 시장 동향 및 분석

스마트 TV용 미니 및 마이크로 LED 백라이트 수요의 급증

고급 TV 브랜드 각사는 2026년 1월 열린 소비자 가전 전시회(CES)에서 RGB 미니 LED TV를 공개하며, 최대 43,000개의 조명을 지원하는 구역과 4,000니트를 넘는 최고 밝기 성능을 입증했습니다. 양자점 필름을 제거함으로써 칩 수율이 안정화되면 부품 비용을 15% 절감할 수 있으며, 절감된 비용을 부가가치가 높은 칩 스케일 패키지(CSP)에 재투자할 수 있게 됩니다. 광둥성과 장쑤성의 패널 조립 제조업체들은 더 좁은 피치에 대응하기 위해 5마이크로m 미만의 정밀도를 갖춘 실장 장비를 도입하고 있으며, 모듈 공장에서 50 km 반경 내에 후공정 조립 거점을 둔 LED 공급업체를 우선적으로 선정하고 있습니다. 100마이크로m 미만의 다이(die)가 양산 단계에 접어들면, 아시아태평양의 백색 LED 패키지 시장은 범용 SMD에서 3 W/mm²의 방열 능력을 갖춘 고출력 웨이퍼 레벨 CSP로 전환될 것입니다. 이러한 추세로 인해 휘도 요구 사항이 높아지면서, 높은 전류 밀도 하에서도 색좌표의 안정성을 유지할 수 있는 첨단 형광체 블렌드에 대한 업스트림 수요가 증가하고 있습니다.

동남아시아 전역에서 시행되는 적극적인 SSL 인센티브 프로그램

태국은 LED 개조에 대한 법인세 2배 공제 혜택을 2028년까지 연장하고, 인도네시아는 30%의 국가 에너지 절약 목표를 유지하며, 베트남은 아시아개발은행(ADB)의 지원을 받아 에너지 절약 체계를 마련할 계획입니다. 이러한 인센티브 덕분에 조명 투자 회수 기간이 18개월 미만으로 단축되었으며, 이는 연색성이나 수명보다 발광 효율을 우선시하는 공공 부문의 조달을 촉진하고 있습니다. 지자체 구매 담당자들이 100 lm/W라는 기준을 표준화해 나가면서, 중출력 SMD 공급업체들은 상품화 속도를 높여야 하는 상황에 직면하고 있습니다. 그 결과, 아시아태평양 지역의 백색 LED 패키지 시장에서는 부가가치가 높은 자동차용 및 디스플레이용 틈새 시장으로 시장 집중이 이루어지는 한편, 보급형 디바이스의 출하량은 급증하고 있습니다. 정책적 측면에서 가장 큰 성장세를 보이고 있는 분야는 상업용 하이베이 조명 및 도로 조명 부문으로, 태국과 베트남의 수출가공구에서 제조되는 2835 및 3030 규격 제품에 대해 향후 수년에 걸친 수요 기반이 확보되어 있습니다.

플립칩 아키텍처를 둘러싼 지속적인 지적재산권 소송

에버라이트 일렉트로닉스는 2026년 2월, 직접 본딩·플립칩 기법에 관한 미국 특허 제7,554,126호의 침해를 이유로 루미레즈 및 서울반도체를 상대로 특허 침해 소송을 제기했습니다. 금지 명령의 위험과 법정 비용 증가로 인해 2차 조립 제조업체들은 플립칩용 설비에 대한 투자를 자제하고 있으며, 그 결과 수직 통합형 대기업들 사이에 생산 능력이 집중되고 있습니다. 현재 OEM 각사는 계약 가격에 3-5%를 가산하는 보상 조항을 협상 중이며, 열적 이점이 명백한 경우에도 도입 속도는 둔화되고 있습니다. 그 결과, 아시아태평양 지역의 백색 LED 패키지 시장에서는 고출력 CSP의 보급에 단기적인 제동이 걸리고 있지만, 기존 공급업체들은 이 분쟁을 이유로 인증된 패키지에 대해 프리미엄 가격을 책정하는 것을 정당화하고 있습니다.

부문별 분석

2025년, 아시아태평양의 백색 LED 패키지 시장에서 표면 실장 소자(SMD) 패키지가 58.48%의 점유율을 차지했습니다. 이는 레트로핏용 전구 및 형광등에 널리 채택된 사실을 반영한 것입니다. 웨이퍼 레벨 CSP 형식은 연평균 성장률(CAGR) 5.49%로 성장하고 있으며, 2031년까지 자동차 헤드램프 및 프리미엄 디스플레이 수주에서 상당한 비중을 차지할 것으로 예측됩니다. 각 OEM 업체들이 더 작은 실적, 더 높은 구동 전류, 그리고 더 낮은 열저항을 요구함에 따라, CSP 기술과 관련된 아시아태평양의 백색 LED 패키지 시장 규모는 꾸준히 확대될 것으로 전망됩니다. 그러나 선전이나 동관의 수탁 제조 공장이 기기당 0.02달러라는 조립 가격을 제시하고 있어, 기존 브랜드보다 40%나 낮은 SMD 라인에서는 여전히 이익률 압박이 심각한 상황입니다.

하이베이 및 경기장 운영 업체에서는 여전히 강력한 루멘 출력을 요구하기 때문에 칩 온 보드(COB) 어레이가 선호되고 있습니다. 한편, 소송이 진행 중임에도 불구하고, 프리미엄 자동차용 주간 주행등(DRL) 시장에서는 플립칩 패키지가 주류를 이루고 있습니다. 예측 기간 동안 월간 생산량이 1,000만 개를 초과하면 경제성 측면에서 CSP 라인이 유리해지며, 기존 SMD 제조업체들은 틈새 시장인 개조 시장으로 전환하거나 기술 업그레이드를 단행해야 할 상황에 처하게 될 것입니다. TV 패널 제조업체들이 제품 주기를 단축하고 적시 생산(JIT) 재고 목표를 달성하기 위해 단일 거점에서의 조립을 요구하는 가운데, 팬아웃 기술에 정통한 공급업체는 경쟁 우위를 확보하게 됩니다. 그 결과, 아시아태평양 지역의 백색 LED 패키지 시장에서는 비용과 성능 양면에서 우위를 점할 수 있는 웨이퍼 레벨 공정에 대한 설비 투자가 진행되고 있습니다.

기타 혜택 :

- Excel 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the asia-Pacific white LED package market size is expected to grow from USD 5.01 billion in 2025 to USD 5.21 billion in 2026 and is forecast to reach USD 6.62 billion by 2031 at a 4.9% CAGR over 2026-2031.

This report is Segmented by Package Architecture (SMD, COB, CSP, and Flip-Chip LED Packages), Power Class (Low Power, Mid Power, and High Power), Application (General Lighting, Automotive Lighting, Display and Backlighting, and Specialty), and Country (China, Japan, India, Southeast Asia, and the Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific White LED Package Market Trends and Insights

Surging Mini And Micro-LED Backlighting Demand In Smart TVs

Premium television brands introduced RGB mini-LED sets at the January 2026 Consumer Electronics Show, demonstrating zone counts as high as 43,000 and peak brightness above 4,000 nits. Eliminating quantum-dot films trims the bill of materials by 15% once die yields stabilize, redirecting savings toward higher-value chip-scale packages. Guangdong and Jiangsu panel assemblers are installing placement tools with sub-5 µm accuracy to manage the tighter pitch, favoring LED suppliers that co-locate back-end assembly within 50 km of module plants. As sub-100 µm die enters volume production, the Asia-Pacific white LED package market migrates from commodity SMD to high-power wafer-level CSP capable of dissipating 3 W mm-2. The trend lifts luminance requirements, driving upstream demand for advanced phosphor blends that maintain color-point stability at elevated current densities.

Aggressive SSL Incentive Programs Across Southeast Asia

Thailand extended double corporate-tax deductions for LED retrofits through 2028, Indonesia preserved its 30% national energy-savings target, and Vietnam plans an Asian Development Bank-backed efficiency framework. These incentives compress lighting payback periods to below 18 months, catalyzing public-sector procurement that prioritizes efficacy over color rendering or lifetime. As municipal buyers standardize on 100 lm/W thresholds, mid-power SMD suppliers face accelerated commoditization. The Asia-Pacific white LED package market therefore sees a volume swell in entry-level devices even as value pools migrate to premium automotive and display niches. Policy momentum is strongest in the commercial high-bay and roadway categories, locking in a multi-year demand base for 2835- and 3030-footprint footprints fabricated in Thai and Vietnamese export-processing zones.

Persistent IP Litigation Over Flip-Chip Architectures

Everlight Electronics lodged patent claims against Lumileds and Seoul Semiconductor in February 2026, citing infringement of U.S. Patent 7,554,126 covering direct-bond flip-chip methods. Injunction risk and escalating legal expenses deter tier-two assemblers from investing in flip-chip tooling, consolidating capacity among vertically integrated giants. OEMs now negotiate indemnification clauses that add 3-5% to contract prices, tempering adoption velocity even where thermal benefits are clear. The Asia-Pacific white LED package market thus experiences a short-term drag on high-power CSP penetration, although incumbent suppliers leverage the dispute to justify premium pricing on authenticated packages.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Build-Out Of EV Charging-Station Lighting Networks

- Cost Downsizing Via Wafer-Level CSP Adoption

- Thermal Management Challenges Above 3 W Power Class

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Surface-mount device packages captured 58.48% of the Asia-Pacific white LED package market share in 2025, reflecting entrenched adoption in retrofit bulbs and tubes. Wafer-level CSP formats are expanding at a 5.49% CAGR and, by 2031, are expected to shoulder a sizeable portion of automotive headlamp and premium display orders. The Asia-Pacific white LED package market size tied to CSP technology is projected to rise steadily as OEMs seek smaller footprints, higher drive currents, and lower thermal resistance. Margin pressure, however, remains acute in SMD lines where Shenzhen and Dongguan contract factories quote assembly at USD 0.02 per device, undercutting legacy brands by 40%.

High-bay and stadium operators still favor chip-on-board arrays for punchy lumen outputs, while flip-chip packages dominate premium automotive daytime running lamps despite pending litigation. Over the forecast horizon, economics favor CSP lines once monthly volumes top 10 million units, pulling SMD incumbents into retrofit niches or prompting technology upgrades. Suppliers with fan-out expertise gain leverage as television panel makers compress product cycles and demand co-located assembly to meet just-in-time inventory goals. Consequently, the Asia-Pacific white LED package market aligns capital spending with wafer-level processes that promise both cost and performance advantages.

List of Companies Covered in this Report:

- Nichia Corporation

- Samsung Electronics Co. Ltd. (Samsung LED)

- Seoul Semiconductor Co. Ltd.

- Everlight Electronics Co. Ltd.

- Lumileds Holding B.V.

- Hongli Zhihui Group Co. Ltd.

- LG Innotek Co. Ltd.

- San'an Optoelectronics Co. Ltd.

- NationStar Optoelectronics Co. Ltd.

- CreeLED, Inc.

- Refond Optoelectronics Co. Ltd.

- Osram GmbH (ams-Osram)

- Edison Opto Corporation

- Dominant Opto Technologies Sdn. Bhd.

- Lextar Electronics Corporation

- Toyoda Gosei Co. Ltd.

- Sharp Corporation

- Rohm Semiconductor

- MLS Co. Ltd. (Forest Lighting)

- Shenzhen Jufei Optoelectronics Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Mini- and Micro-LED Backlighting Demand in Smart TVs

- 4.2.2 Aggressive SSL Incentive Programs Across Southeast Asia

- 4.2.3 Rapid Build-out of EV Charging-Station Lighting Networks

- 4.2.4 Cost Downsizing via Wafer-Level CSP Adoption

- 4.2.5 Proliferation of UV-Free Health-Oriented Lighting in Japan

- 4.2.6 Mandatory Energy-Efficiency Labelling in India and China

- 4.3 Market Restraints

- 4.3.1 Persistent IP Litigation Over Flip-Chip Architectures

- 4.3.2 Thermal Management Challenges Above 3 W Power Class

- 4.3.3 Supply Tightness of High CRI Phosphors

- 4.3.4 Rising Mini-LED Die Cost Due to Sapphire Substrate Inflation

- 4.4 Industry Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Package Architecture

- 5.1.1 SMD (Surface Mount Device)

- 5.1.2 COB (Chip-on-Board)

- 5.1.3 CSP (Chip Scale Package)

- 5.1.4 Flip-Chip LED Packages

- 5.2 By Power Class

- 5.2.1 Low Power (Less than 0.5 W)

- 5.2.2 Mid Power (0.5 -1 W)

- 5.2.3 High Power (More than 1 W)

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display and Backlighting

- 5.3.4 Specialty / Niche

- 5.4 By Country

- 5.4.1 China

- 5.4.2 Japan

- 5.4.3 India

- 5.4.4 Southeast Asia

- 5.4.5 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Samsung Electronics Co. Ltd. (Samsung LED)

- 6.4.3 Seoul Semiconductor Co. Ltd.

- 6.4.4 Everlight Electronics Co. Ltd.

- 6.4.5 Lumileds Holding B.V.

- 6.4.6 Hongli Zhihui Group Co. Ltd.

- 6.4.7 LG Innotek Co. Ltd.

- 6.4.8 San'an Optoelectronics Co. Ltd.

- 6.4.9 NationStar Optoelectronics Co. Ltd.

- 6.4.10 CreeLED, Inc.

- 6.4.11 Refond Optoelectronics Co. Ltd.

- 6.4.12 Osram GmbH (ams-Osram)

- 6.4.13 Edison Opto Corporation

- 6.4.14 Dominant Opto Technologies Sdn. Bhd.

- 6.4.15 Lextar Electronics Corporation

- 6.4.16 Toyoda Gosei Co. Ltd.

- 6.4.17 Sharp Corporation

- 6.4.18 Rohm Semiconductor

- 6.4.19 MLS Co. Ltd. (Forest Lighting)

- 6.4.20 Shenzhen Jufei Optoelectronics Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment