|

시장보고서

상품코드

2063979

중국의 중출력 LED 패키지 시장 : 시장 점유율 분석, 업계 동향 통계, 성장 예측(2026-2031년)China Mid-Power LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

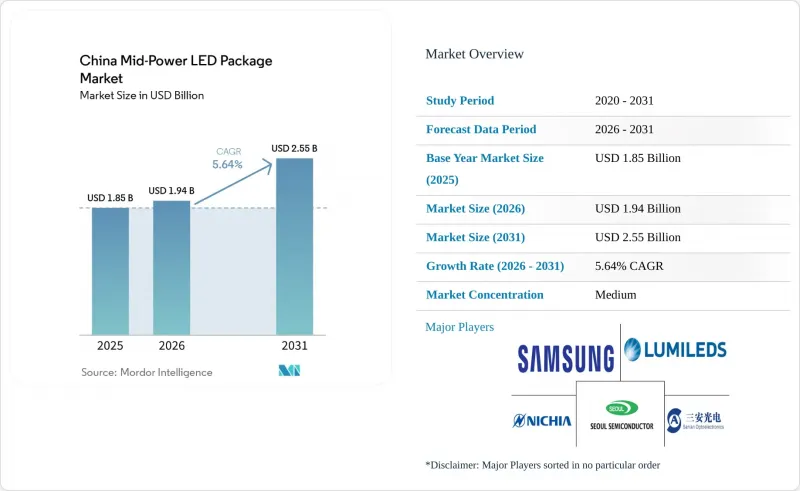

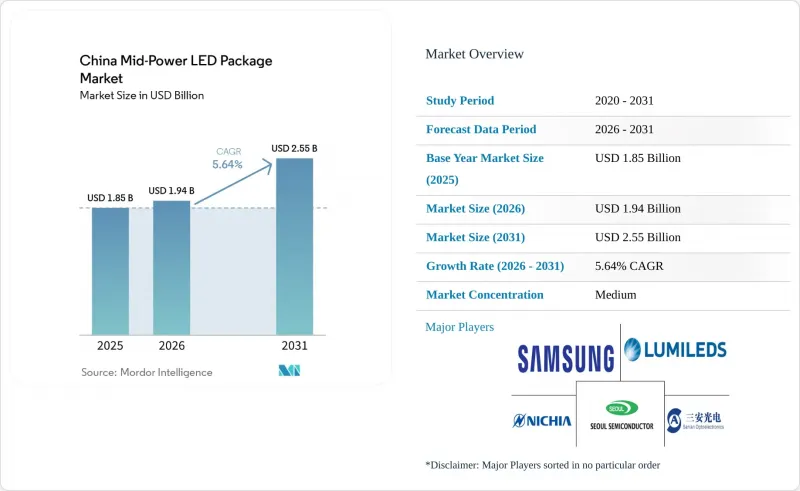

Mordor Intelligence에 의하면, 중국의 중출력 LED 패키지 시장 규모는 2025년에 18억 5,000만 달러로 평가되었고, 2026년에 19억 4,000만 달러로 추정되고, 2031년까지 25억 5,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 5.64%로 성장할 전망입니다.

본 보고서는 출력 범위별(0.2-0.5W 및 0.5-1W 미만), 패키지 구조별(2835, 3014, 3030, 기타를 포함한 SMD 및 CSP), 용도별(일반 조명, 자동차용 조명, 디스플레이 및 백라이트, 특수 및 틈새 용도)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

중국의 중출력 LED 패키지 시장 동향 및 분석

중국 2선 도시에서 에너지 절약형 조명에 대한 수요 증가

에너지 성능 계약을 통해 자금을 조달한 지자체의 조명 개보수 사업이 허페이, 전장, 퉁링, 증청에서 확대되고 있으며, 조명기 한 대 단위의 IoT 제어를 통해 유지보수 대응 시간이 최대 80% 단축되고 있습니다. 검증된 에너지 절약 보증을 통해 민간 투자자들은 9-10년 내에 프로젝트 비용을 회수할 수 있으며, 이는 예측 가능한 중출력 LED 패키지에 대한 수요 창출로 이어지고 있습니다. GB 30255-2026 규격에서는 최소 광속 효율이 105 lm/W로 상향 조정되고, 대기 전력이 0.5 W로 제한됨에 따라, 가로등 개보수 시에는 고효율이며 0.5 W 이하(1 W 미만)인 패키지가 선호되고 있습니다. 2030년까지 탄소 배출량 정점 달성 목표를 내세우는 2급 도시가 늘어남에 따라, 리모델링 프로젝트의 파이프라인이 장기화되고 있으며, 향후 수년에 걸친 수요 전망이 뒷받침되고 있습니다. 이러한 추세에 따라, 새로운 광학 성능 및 플리커 제한 기준을 충족하는 수명이 긴 세라믹 및 플립칩 SMD 형식에 대한 공급업체들의 관심이 높아지고 있습니다.

LED 제조 분야의 산업 고도화를 위한 정부 보조금 프로그램

재무부는 탄소 감축 프로젝트에 936억 위안(130억 달러)을 배정했으며, 중국인민은행은 공장 현대화를 가속화하기 위해 8,000억 위안(1,110억 달러) 규모의 저금리 재융자 한도를 마련했습니다. 이러한 자금은 TCL CSOT의 푸저우 화자오 광전 인수와 NationStar 및 Leyard의 생산 능력 확대와 같은 수직 통합 사업을 뒷받침하고 있습니다. 보조금 대상 기준은 중국 에너지 라벨 1등급 기준을 상회하는 Mini/Micro LED, 자동차용 및 원예용 패키지를 생산하는 라인을 우대하고 있으며, 이로 인해 시장 점유율은 수직 통합형 기업 쪽으로 더욱 기울고 있습니다. 각 성 정부는 신규 설비 비용의 최대 20%를 보전해 주는 매칭 보조금을 추가로 지급하고 있으며, 이에 따라 고속 플립칩 본더 및 자동 형광체 스프레이 라인의 도입이 가속화되고 있습니다. 그 결과, 자본력이나 자동차 등급 인증을 갖추지 못한 중소 패키지 제조업체들은 보조금과 연계된 수주 경쟁에서 점차 밀리고 있습니다.

중국 LED 패키징 라인의 과잉 생산 능력으로 인한 가격 하락

2022-2025년 신규 진출기업들이 수요를 상회하는 속도로 생산 능력을 확대함에 따라, 중출력 패키지의 평균 판매 가격이 하락했습니다. 2026년 초, 업계가 한마음으로 노력한 결과 가격은 반등했으나, 시장에서는 여전히 범용 조명 제품공급 과잉으로 어려움을 겪고 있습니다. 소매업체들은 신중한 태도를 보이며, 비용 상승분을 소비자에게 전가하는 데 주저하고 있어, 그 결과 포장재 제조업체의 운전자금 회수 주기가 길어지고 있습니다. 2025년에는 원자재 가격 변동으로 인해 금, 은 구리 가격이 급등하여 매출총이익률에 압박을 가했습니다. 2025년 3분기까지, 이 추세는 주요 시장 참여자인 산안광전이 이익률 하락을 보고하면서 분명해졌습니다. 시장 재편으로 인해 가격 결정력이 강화될 전망이지만, 독자적인 기술을 보유하지 않은 중소 벤더들은 시장 균형이 달성되기 전에 시장에서 배제될 것이라는 절박한 위협에 직면해 있습니다.

부문별 분석

2025년 기준으로 0.5W-1W 미만 등급은 중국 중출력 LED 패키지 시장 점유율의 62.1%를 차지했으며, 해당 시장 규모는 2031년까지 연평균 성장률(CAGR) 5.99%로 확대될 것으로 전망됩니다. 이 범위는 광속, 방열, 비용의 균형이 잘 잡혀 있어 실내등, 가로등 및 Mini LED의 로컬 디밍 영역에서 주력 제품으로 자리 잡고 있습니다. 접합부 온도 125℃에 대응하는 세라믹 및 플립칩 3030 포맷은 자동차의 사이드 마커 및 주간 주행등 분야에서 플라스틱 패키지를 대체하는 추세가 강해지고 있습니다.

효율 5.05마이크로mol J-1의 짙은 적색 3535 원예용 LED 등 재료 기술의 발전에 힘입어, 이 부문은 환경 제어형 농업 분야로 확대되고 있습니다. GB 31831-2025에 따른 발광 효율 목표의 강화와 더불어, 플리커 관련 기준의 강화로 인해 중전류 0.5W 발광 소자의 채택이 더욱 보편화되고 있습니다. 저전력(0.2-0.5 W) 장치는 장식용 스트립이나 휴대용 기기에서 틈새 시장을 유지하고 있는 반면, 1 W 이하의 패키지는 하이베이 조명 및 UV 시장으로 전환되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the china mid-power LED package market size is projected to be USD 1.85 billion in 2025, USD 1.94 billion in 2026, and reach USD 2.55 billion by 2031, growing at a CAGR of 5.64% from 2026 to 2031.

This report is Segmented by Power Range (0. 2-0. 5 W and 0. 5- Less Than 1 W), Package Architecture (SMD Including 2835, 3014, 3030, Others, and CSP), and Application (General Lighting, Automotive Lighting, Display and Backlighting, and Specialty/Niche). The Market Forecasts are Provided in Terms of Value (USD).

China Mid-Power LED Package Market Trends and Insights

Growing Demand for Energy-Efficient Lighting in China's Tier-2 Cities

Municipal retrofits financed through energy-performance contracts are scaling across Hefei, Qianjiang, Tongling, and Zengcheng, where single-lamp IoT controls cut maintenance response times by as much as 80%. Verified energy-savings guarantees allow private investors to recover project costs over 9- to 10-year terms, creating a predictable mid-power LED package pull-through. The GB 30255-2026 standard boosts minimum efficacy to 105 lm/W and caps standby power at 0.5 W, thereby favoring high-efficacy 0.5 W- less than 1 W packages for streetlighting retrofits. As more Tier-2 cities commit to carbon-peaking goals before 2030, retrofit pipelines are lengthening, underpinning multi-year demand visibility. The dynamic is reinforcing supplier interest in long-lifetime ceramic and flip-chip SMD formats that meet the new optical and flicker limits.

Government Subsidy Programs for Industrial Upgrades in LED Manufacturing

The Ministry of Finance earmarked RMB 93.6 billion (USD 13 billion) for carbon-reduction projects, while the People's Bank of China opened RMB 800 billion (USD 111 billion) in low-cost refinancing to accelerate factory upgrades. These funds are underwriting vertical-integration deals such as TCL CSOT's purchase of Fuzhou Huazhao Optoelectronics and capacity expansions at NationStar and Leyard. Subsidy criteria favor lines producing Mini/Micro LED, automotive, and horticultural packages that exceed Level 1 China Energy Label thresholds, further tilting market share toward integrated players. Provincial governments add matching grants that offset up to 20% of new equipment costs, hastening adoption of high-speed flip-chip bonders and automated phosphor-spray lines. Smaller packagers lacking capital or automotive-grade qualifications are consequently losing bids for subsidy-linked orders.

Price Erosion Due To Overcapacity in Chinese LED Packaging Lines

Between 2022 and 2025, new entrants ramped up capacity faster than demand, leading to a drop in average selling prices for mid-power packages. While a concerted effort in early 2026 led to a price rebound, the market still grapples with an oversupply of commodity lighting. Retailers tread carefully, hesitant to transfer rising costs to consumers, which in turn elongates working-capital cycles for packagers. In 2025, fluctuations in raw-material prices led to surges in gold, silver, and copper prices, exerting pressure on gross margins. By Q3 2025, this was evident as San'an Optoelectronics, a key market player, reported a dip in its margins. While consolidation in the market promises to bolster pricing power, smaller vendors lacking unique technology face the looming threat of being edged out before market equilibrium is achieved.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Expansion of Automotive LED Headlamp Adoption

- Surge In Mini-LED Backlight Adoption in TVs And Monitors

- Supply Chain Disruptions for High-Purity Phosphors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 0.5 W- Less Than 1 W class accounted for 62.1% of the China mid-power LED package market share in 2025, with its market size forecast to expand at a 5.99% CAGR to 2031. This range balances luminous flux, heat dissipation, and cost, making it the workhorse for indoor lamps, streetlights, and Mini LED local-dimming zones. Ceramic and flip-chip 3030 formats rated to 125 °C junction temperature are increasingly displacing plastic packages in automotive side markers and daytime running lamps.

Material advances, such as deep-red 3535 horticultural LEDs with an efficiency of 5.05 µmol J-1, extend the segment into controlled-environment agriculture. Tightening efficacy targets under GB 31831-2025, plus stricter flicker metrics, further entrench the adoption of mid-current 0.5 W emitters. Lower-power 0.2-0.5 W devices keep a niche in decorative strips and portable gadgets, while less than or equal to 1 W packages migrate toward high-bay and UV markets.

List of Companies Covered in this Report:

- Nichia Corporation

- Samsung Electronics Co., Ltd.

- Lumileds Holding B.V.

- Seoul Semiconductor Co., Ltd.

- Cree LED, Inc.

- ams Osram GmbH

- Shenzhen NationStar Optoelectronics Co., Ltd.

- Everlight Electronics Co., Ltd.

- Hongli Zhihui Group Co., Ltd.

- Refond Optoelectronics Co., Ltd.

- San'an Optoelectronics Co., Ltd.

- MLS Co., Ltd. (Forest Lighting)

- Lextar Electronics Corporation

- Bridgelux, Inc.

- Shenzhen Jufei Optoelectronics Co., Ltd.

- Dominant Opto Technologies Sdn. Bhd.

- Lite-On Technology Corporation

- Toyoda Gosei Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Energy-Efficient Lighting in China's Tier-2 Cities

- 4.2.2 Government Subsidy Programs for Industrial Upgrades in LED Manufacturing

- 4.2.3 Rapid Expansion of Automotive LED Headlamp Adoption

- 4.2.4 Surge in Mini-LED Backlight Adoption in TVs and Monitors

- 4.2.5 Rising Investments in Smart City Infrastructure Lighting

- 4.2.6 Localization of LED Supply Chain Due to Geopolitical Tech Self-Reliance

- 4.3 Market Restraints

- 4.3.1 Price Erosion Due to Overcapacity in Chinese LED Packaging Lines

- 4.3.2 Supply Chain Disruptions for High-Purity Phosphors

- 4.3.3 Stringent Blue-Light Hazard Regulations Limiting Drive Current

- 4.3.4 Competition from Integrated COB and High-Power Packages

- 4.4 Industry Value-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Power Range

- 5.1.1 0.2-0.5 W

- 5.1.2 0.5- Less Than 1 W

- 5.2 By Package Architecture

- 5.2.1 SMD (Surface Mount Device)

- 5.2.1.1 2835

- 5.2.1.2 3014

- 5.2.1.3 3030

- 5.2.1.4 Others (3528, 3020, 5050, etc.)

- 5.2.2 CSP (Chip Scale Package)

- 5.2.1 SMD (Surface Mount Device)

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display and Backlighting

- 5.3.4 Specialty / Niche

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Samsung Electronics Co., Ltd.

- 6.4.3 Lumileds Holding B.V.

- 6.4.4 Seoul Semiconductor Co., Ltd.

- 6.4.5 Cree LED, Inc.

- 6.4.6 ams Osram GmbH

- 6.4.7 Shenzhen NationStar Optoelectronics Co., Ltd.

- 6.4.8 Everlight Electronics Co., Ltd.

- 6.4.9 Hongli Zhihui Group Co., Ltd.

- 6.4.10 Refond Optoelectronics Co., Ltd.

- 6.4.11 San'an Optoelectronics Co., Ltd.

- 6.4.12 MLS Co., Ltd. (Forest Lighting)

- 6.4.13 Lextar Electronics Corporation

- 6.4.14 Bridgelux, Inc.

- 6.4.15 Shenzhen Jufei Optoelectronics Co., Ltd.

- 6.4.16 Dominant Opto Technologies Sdn. Bhd.

- 6.4.17 Lite-On Technology Corporation

- 6.4.18 Toyoda Gosei Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment