|

시장보고서

상품코드

2063981

인도의 중출력 LED 패키지 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)India Mid-Power LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

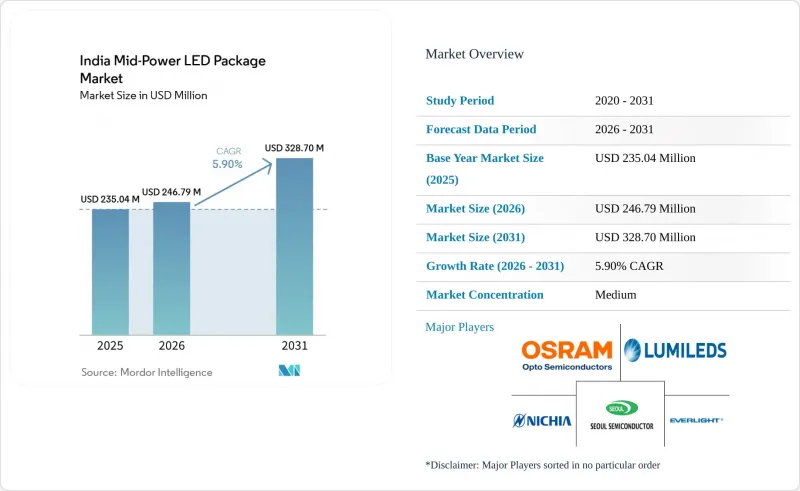

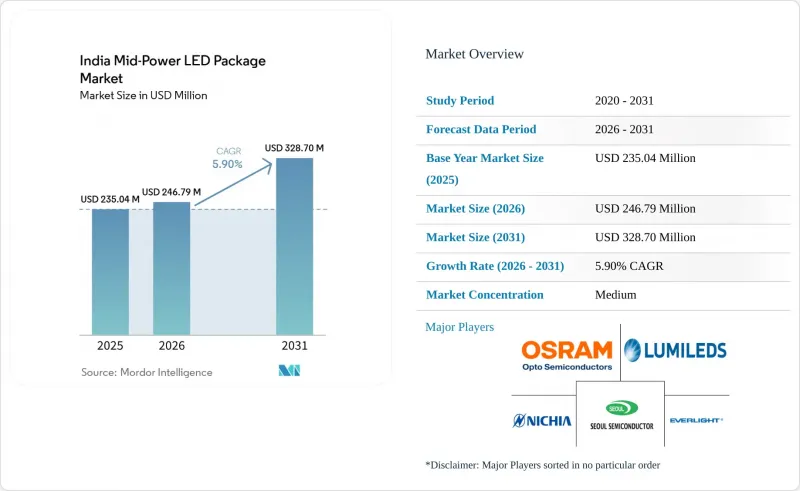

Mordor Intelligence에 의하면, 인도의 중출력 LED 패키지 시장 규모는 2025년 2억 3,504만 달러로 평가되었고, 2026년에는 2억 4,679만 달러로 추정되고, 2031년까지 3억 2,870만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 5.9%로 성장할 전망입니다.

본 보고서는 출력 범위별(0.2-0.5W 및 0.5-1W 미만), 패키지 구조별(2835, 3014, 3030, 기타를 포함한 SMD 및 CSP), 용도별(일반 조명, 자동차용 조명, 디스플레이 및 백라이트, 특수 및 틈새 용도)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

인도의 중출력 LED 패키지 시장 동향 및 인사이트

가로등 입찰에서 LED의 주류화

지방 자치 단체는 2025년 이후에 발주된 가로등 입찰의 90% 이상에 최소 효율 및 연색성 기준을 포함시켰습니다. 이에 따라 고압 나트륨 램프 기구는 사실상 제외되었으며, 1와트당 120-140루멘의 광속을 제공하는 0.5W-1W 중출력 패키지로의 조달이 진행되고 있습니다. 에너지 효율 서비스(EESL)는 중앙 정부의 공동 자금 지원을 통해 교체 주기를 가속화하고 있습니다. 이러한 움직임 덕분에 향후 수년에 걸친 수주 전망이 보장되고 있습니다. BIS(인도 표준국) 기준을 준수함을 입증하고, 4킬로볼트를 초과하는 서지 보호 등급을 자랑하는 공급업체가 꾸준히 최대 규모의 물량을 수주하고 있습니다. 이러한 추세에 따라 현지 봉합 라인의 가동 규모가 점차 확대되고 있습니다.

BIS에 의한 발광 효율 기준 상향 조정

BIS 규격군인 IS 10322, 2026, IS 16102, 2026, IS 16103, 2025에 따라, 가장 일반적인 와트 수 등급에서 발광 효율의 하한이 1와트당 100루멘에서 110-120루멘으로 상향 조정되었습니다. 사내에 광도 측정 실험실을 갖춘 대형 제조업체는 신속하게 개선된 제품 라인을 출시했습니다. 한편, 소규모 조립 제조업체들은 최대 6개월에 달하는 인증 지연으로 어려움을 겪고 있습니다. 이러한 의무화로 인한 변화로 인해 판매 부진한 SKU는 구형이 되어버리게 되었고, 인도의 중출력 LED 패키지 시장에서는 재고 보충이 급증하고 있습니다.

형광체 공급 가격의 변동

2026년 4월 중국이 시행한 이트륨 화합물 수출 규제로 인해, 유럽의 이트륨 산화물 현물 가격은 6주 만에 1kg당 8달러에서 126달러로 급등했으며, 수입된 적색 및 황색 형광체에 의존하는 인도의 패키지 제조업체들의 영업이익률은 최대 200베이시스포인트 감소했습니다. 선물 계약 및 가돌리늄계 혼합물을 통한 부분적인 대체로 충격은 완화되었으나, 지속적인 지정학적 리스크로 인해 시장 성장률은 1.3포인트 하락했습니다.

부문별 분석

2025년, 0.5W-1W 미만의 대역은 인도 중출력 LED 패키지 시장 점유율의 63.33%를 차지했습니다. 정부의 가로등 프로그램이나 자동차용 어댑티브 헤드램프의 경우, 발광 효율과 열적 여유 사이의 균형을 맞추기 위해 이 와트수가 지정되어 있으며, Lumax Industries사의 LED 관련 미수주 잔고 1,759 카롤 루피(2억 1,100만 달러)가 수요를 뒷받침하고 있습니다. 인도 대부분의 지역에서 실외 기온이 40°C를 넘기 때문에 접합부 온도 상승 위험이 높아지고 있으며, 5만 시간의 루멘 유지 목표를 달성하기 위해서는 0.5W-1W 다이스의 낮은 전류 밀도가 필수적입니다.

이 부문의 성장은 PLI(생산 연계형 인센티브)에 따른 형광체 코팅 및 와이어 본딩 라인의 현지화도 뒷받침하고 있으며, 이를 통해 수입품에 비해 부품 비용을 8% 가까이 절감하고, 2031년까지 연평균 성장률(CAGR) 6.78%를 유지하고 있습니다. 이 출력 범위 내 인도 중출력 LED 패키지 시장 규모는 예측 기간 동안 총 300만 개 이상의 조명 기구를 대상으로 하는 지방자치단체의 입찰 증가와 발맞추어 성장할 것으로 전망됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the india mid-power LED package market size is expected to increase from USD 235.04 million in 2025 to USD 246.79 million in 2026 and reach USD 328.70 million by 2031, growing at a CAGR of 5.9% over 2026-2031.

This report is Segmented by Power Range (0. 2-0. 5 W and 0. 5- Less Than 1 W), Package Architecture (SMD Including 2835, 3014, 3030, Others, and CSP), and Application (General Lighting, Automotive Lighting, Display and Backlighting, and Specialty/Niche). The Market Forecasts are Provided in Terms of Value (USD).

India Mid-Power LED Package Market Trends and Insights

Mainstream LED Adoption in Street-Lighting Tenders

Municipal corporations embedded minimum efficacy and color-rendering thresholds into more than 90% of street-lighting tenders issued since 2025, effectively disqualifying high-pressure sodium fixtures and pushing procurement toward 0.5 W-to-1 W mid-power packages that deliver 120-140 lumens per watt. Energy Efficiency Services Limited (EESL) is accelerating replacement cycles through central co-financing. This move guarantees multi-year order visibility. Vendors that showcase BIS compliance and boast surge-protection ratings exceeding 4 kilovolts are consistently landing the largest lots. This trend is prompting local encapsulation lines to expand their operations.

Rising Luminous-Efficacy Mandates By BIS

The BIS suite, IS 10322:2026, IS 16102:2026, and IS 16103:2025, has raised efficacy floors from 100 lumens per watt to 110-120 lumens for the most prevalent wattage classes. Major players, equipped with in-house photometric labs, have swiftly rolled out upgraded product lines. In contrast, smaller assemblers grapple with certification delays that can stretch up to 6 months. This mandatory shift renders slower-moving SKUs obsolete, prompting a surge in restocking in India's mid-power LED package market.

Volatility In Phosphor Supply Prices

China's April 2026 export controls on yttrium compounds drove European yttrium-oxide spot prices from USD 8 per kg to USD 126 per kg within six weeks, compressing operating margins by up to 200 basis points for Indian package makers reliant on imported red and yellow phosphors. Although forward contracts and partial substitution with gadolinium-based blends temper the shock, persistent geopolitical risk subtracts 1.3 percentage points from market expansion.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Expansion of Indian Contract Electronics Manufacturing

- Indigenous Smartphone Assembly Shifting to Mid-Power LEDs

- Low Switching-Cost Toward COB Imports from China

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 0.5 W-to-Less Than 1 W band captured 63.33% of India's mid-power LED package market share in 2025. Government street-lighting programs and automotive adaptive headlamps specify this wattage to balance efficacy with thermal headroom, and demand is reinforced by Lumax Industries' INR 1,759 crore (USD 211 million) LED-heavy order book. Outdoor ambient temperatures exceeding 40 °C in much of India elevate junction-temperature risk, making the lower current density of 0.5 W to 1 W dice indispensable for 50,000-hour lumen maintenance targets.

Segment growth also benefits from PLI-funded localization of phosphor coating and wire-bonding lines, which trim bill-of-materials costs by nearly 8% versus imported equivalents, sustaining a 6.78% CAGR through 2031. The Indian mid-power LED package market size for this power range is projected to move in lockstep with the ramp-up of municipal tenders that collectively cover more than 3 million luminaire points over the forecast horizon.

List of Companies Covered in this Report:

- Nichia Corporation

- Seoul Semiconductor Co. Ltd.

- Lumileds Holding B.V.

- Osram Opto Semiconductors GmbH

- Everlight Electronics Co. Ltd.

- CreeLED Inc.

- Samsung Electronics Co. Ltd.

- MLS Co. Ltd. (Forest Lighting)

- Dominant Opto Technologies Sdn Bhd

- Lextar Electronics Corp.

- Edison Opto Corp.

- Havells India Ltd.

- Dixon Technologies (India) Ltd.

- HPL Electric and Power Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mainstream LED Adoption in Street-Lighting Tenders

- 4.2.2 Rising Luminous-Efficacy Mandates by BIS

- 4.2.3 Rapid Expansion of Indian Contract Electronics Manufacturing

- 4.2.4 Indigenous Smartphone Assembly Shifting to Mid-Power LEDs

- 4.2.5 Government's PLI Scheme for LED Components

- 4.2.6 Micro-Retailers Embracing Smart-Lighting Retrofits

- 4.3 Market Restraints

- 4.3.1 Volatility in Phosphor Supply Prices

- 4.3.2 Low Switching-Cost Toward COB Imports from China

- 4.3.3 Thermal-Management Issues in High-Ambient Zones

- 4.3.4 Persistent GST-Rate Uncertainty on LED Inputs

- 4.4 Industry Value-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Power Range

- 5.1.1 0.2-0.5 W

- 5.1.2 0.5- Less Than 1 W

- 5.2 By Package Architecture

- 5.2.1 SMD (Surface Mount Device)

- 5.2.1.1 2835

- 5.2.1.2 3014

- 5.2.1.3 3030

- 5.2.1.4 Others (3528, 3020, 5050, etc.)

- 5.2.2 CSP (Chip Scale Package)

- 5.2.1 SMD (Surface Mount Device)

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display and Backlighting

- 5.3.4 Specialty / Niche

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Seoul Semiconductor Co. Ltd.

- 6.4.3 Lumileds Holding B.V.

- 6.4.4 Osram Opto Semiconductors GmbH

- 6.4.5 Everlight Electronics Co. Ltd.

- 6.4.6 CreeLED Inc.

- 6.4.7 Samsung Electronics Co. Ltd.

- 6.4.8 MLS Co. Ltd. (Forest Lighting)

- 6.4.9 Dominant Opto Technologies Sdn Bhd

- 6.4.10 Lextar Electronics Corp.

- 6.4.11 Edison Opto Corp.

- 6.4.12 Havells India Ltd.

- 6.4.13 Dixon Technologies (India) Ltd.

- 6.4.14 HPL Electric and Power Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment