|

시장보고서

상품코드

2064348

유럽의 백색 LED 패키지 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Europe White LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

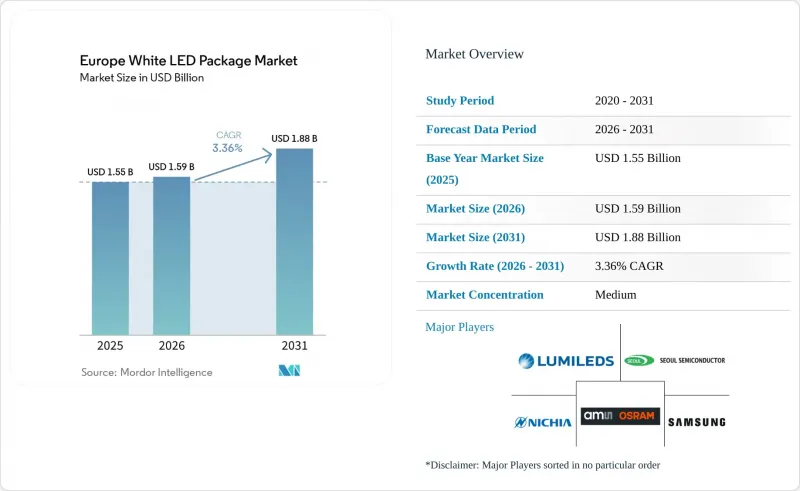

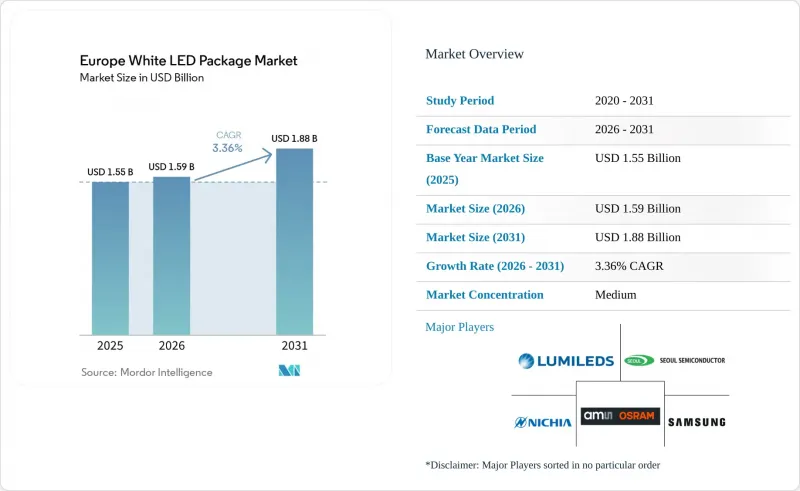

Mordor Intelligence에 의하면, 유럽의 백색 LED 패키지 시장 규모는 2025년에 15억 5,000만 달러로 평가되었고, 2026년에 15억 9,000만 달러로 추정되고, 2031년까지 18억 8,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 3.36%로 성장할 전망입니다.

본 보고서는 패키지 구조별(SMD, COB, CSP, 플립칩 LED 패키지), 전력 등급별(저전력(0.5W 미만), 중전력(0.5-1W), 고전력(1W 이상)), 용도별(일반 조명, 자동차용 조명, 디스플레이 및 백라이트 등), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

유럽의 백색 LED 패키지 시장 동향 및 분석

EU 전역에서 에너지 효율 규제가 강화됩니다.

에너지 효율 지침 2023/1791/EU는 회원국들에게 2030년까지 최종 에너지 소비량을 11.7% 감축할 것을 의무화하고 있는 반면, 에코디자인 규정 2019/2020은 발광 효율이 1와트당 85루멘 미만인 비지향성 램프를 금지하고 있으며, 이에 따라 공공기관은 모든 신규 입찰에서 LED로 교체하도록 지정해야 하는 상황에 놓여 있습니다. 지자체는 조명을 중요 인프라로 간주하고 있습니다. 파리시는 2025년까지 7만 개의 조명 기구를, 10년 동안 240GWh의 전력 절감 효과가 예상되는 커넥티드 LED 시스템으로 교체하기 위해 7억 유로 규모의 계약을 체결했습니다. 뮈루즈와 레딩에서 체결된 유사한 성과 연계형 운영권 계약에는 고효율 패키지와 추적 가능한 부품 명세서가 필요한 원격 관리 노드의 설치가 포함되어 있습니다. 이러한 규제 요건으로 인해 단가가 하락하더라도 기준 수요량은 유지됩니다. 규정을 준수하지 않는 조명 기구가 철거될 때마다 패키지에 대한 직접적인 수요가 발생하기 때문입니다. LM-80 파일이나 수리 가능성에 관한 문서를 보유한 공급업체는 입찰 전제조건을 보다 쉽게 충족할 수 있으며, 규정 준수 관련 전문 지식을 바탕으로 높은 낙찰률을 달성할 수 있습니다.

규모의 경제에 따른 LED 패키지 비용의 감소

150mm 및 200mm 생산 라인을 가동 중인 아시아의 웨이퍼 공장은 2023년 이후 중출력 SMD 가격을 연평균 8-12% 인하하고 있으며, 이에 따라 유럽의 개조 프로젝트에서는 전기 요금이 0.15유로/kWh를 초과하는 경우에도 2년 내에 투자 회수가 가능해졌습니다. 이에 대해 Lumileds는 ‘LUXEON Altilon SMD-A’를 발표했습니다. 이 패키지는 픽 앤 플레이스 공정에 최적화되어 있으며, 빈 간 순방향 전압의 일관성을 0.2V로 유지하면서 조립 사이클 타임을 18% 단축함으로써, 각 OEM 업체가 신뢰성을 저해하지 않고 비용을 절감할 수 있도록 지원합니다. 조달 비용의 감소로 인해 트로퍼 및 패널 라이트에의 채택이 가속화되고, 매출 총이익률이 압박받는 상황 속에서도 패키지 벤더의 잠재적 판매량은 확대되고 있습니다. 또한, 가격 곡선은 범용 중출력 칩과 프리미엄 칩 스케일 및 플립 칩 옵션 간의 성능 격차를 확대함으로써, 공급업체가 제품 포트폴리오를 세분화하고 고출력 틈새 시장에서 이익률을 유지할 수 있도록 돕고 있습니다. 그 결과, 규모의 경제는 기본적인 조명을 보급하는 한편, 특수한 건축 양식을 위한 연구개발(R&D) 자금도 창출하고 있습니다.

상품화로 인한 가격 압박

아시아의 2선 제조업체들이 0.50달러 미만의 중출력 패키지를 공급하고 있기 때문에 유럽의 조명 기구 OEM 제조업체들은 이중 조달을 통해 대량 구매 할인을 협상하고 있습니다. 이로 인해 공급업체에 대한 충성도가 떨어지고 있습니다. 레트로핏용 전구 및 형광등 분야에서는 구매자들이 LED를 호환 가능한 제품으로 간주하기 때문에 잘 알려진 브랜드조차도 루멘당 비용 경쟁력을 유지하기 위해 이익률을 낮출 수밖에 없습니다. 일부 중견 유럽 조립업체들은 일반 상품 시장에서 철수하고, 기술적 장벽으로 인해 직접적인 가격 경쟁이 억제되는 자동차 및 원예 분야로 연구개발(R&D) 자원을 재분배하고 있습니다. 이러한 압박은 최저 입찰가로 낙찰되는 공공 입찰에서 가장 심각하며, 수명이나 보증 조항에 측정 가능한 페널티가 설정되어 있지 않은 한, 프리미엄 포지셔닝을 취할 여지는 거의 없습니다. 따라서 지속적인 가격 하락으로 인해 출하 대수는 견조한 수준을 유지하고 있음에도 불구하고, 전체 매출 성장세는 둔화되고 있습니다.

부문별 분석

2025년, 표면 실장 소자(SMD) 패키지는 유럽 백색 LED 패키지 시장 점유율의 58.38%를 차지했으며 선도적인 위치를 유지했습니다. 이는 플라스틱 하우징, 검증된 픽 앤 플레이스 호환성, 그리고 현장에서 수리가 가능한 설계가 유럽연합(EU)의 수리 가능성 관련 규정에 부합하기 때문입니다. 지자체 가로등 사업이나 상업용 천장 패널 개보수 공사에서는 계속해서 SMD 방식이 지정되고 있으며, 이에 따라 조립 제조업체는 예측 가능한 생산량을 확보할 수 있고, 조명 기구 제조업체는 보증 청구 건수를 계약상 기준치 이하로 억제할 수 있게 되었습니다. 자동 광학 검사용 마커나 비닝 허용 오차의 엄격화 등 제품 수명 주기 중반에 이루어지는 개선은 확립된 생산 흐름을 방해하지 않으면서 품질을 향상시킵니다. 또한, 광범위한 도입 실적이 예비 부품에 대한 2차 수요를 뒷받침하고 있어, 단가가 해마다 하락하고 있음에도 불구하고 SMD의 수익은 견조한 추세를 유지하고 있습니다.

칩 스케일 패키지는 더욱 가파른 성장 곡선을 그리고 있으며, 자동차용 어댑티브 헤드램프와 마이크로 LED 백플레인이 0.5mm 미만의 초박형화와 높은 열전도율을 중시함에 따라 2031년까지 연평균 성장률(CAGR) 3.88%로 확대되고 있습니다. 성형 하우징을 제거함으로써 열 저항이 약 20% 감소하여, 루멘 저하를 초래하지 않으면서 더 좁은 픽셀 간격과 더 높은 구동 전류를 구현할 수 있습니다. 유럽의 1차 공급업체는 웨이퍼 수준의 형광체, 드라이버 ASIC, 질화알루미늄 기판을 통합하여 이 소형 폼 팩터를 경쟁력 있는 가격으로 제공할 수 있는 단일 공급원 모듈로 변모시키고 있습니다. 플립칩과 칩 온 보드 방식은 인접한 틈새 시장을 채우고 있습니다. 플립 칩은 대전류가 흐르는 주간 주행등에, 칩 온 보드는 산업용 하이베이 조명에 채택되고 있으며, 이는 아키텍처 선택이 더 이상 획일적인 비용 지표에 따라 이루어지는 것이 아니라 최종 용도의 성능 목표에 맞추어 이루어지고 있음을 여실히 보여주고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the europe white lED package market size is projected to be USD 1.55 billion in 2025, USD 1.59 billion in 2026, and reach USD 1.88 billion by 2031, growing at a CAGR of 3.36% from 2026 to 2031.

This report is Segmented by Package Architecture (SMD (Surface Mount Device), COB (Chip-On-Board), CSP (Chip Scale Package), Flip-Chip LED Packages), Power Class (Low Power (Below 0. 5 W), Mid Power (0. 5-1 W), High Power (Above 1 W)), Application (General Lighting, Automotive Lighting, Display and Backlighting, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe White LED Package Market Trends and Insights

Energy Efficiency Regulations Tightening Across the EU

The Energy Efficiency Directive 2023/1791/EU compels member states to reduce final energy consumption by 11.7% by 2030, while the Ecodesign Regulation 2019/2020 bans non-directional lamps with a luminous efficacy below 85 lumens per watt, pushing public agencies to specify LED retrofits in every new tender. Municipalities treat lighting as critical infrastructure: Paris signed a EUR 700 million contract in 2025 to replace 70,000 luminaires with connected LED systems that promise 240 GWh in savings over 10 years. Similar performance-based concessions in Mulhouse and Reading involve installing remote-management nodes that require high-efficiency packages and traceable component bills. These regulatory mandates sustain baseline volumes even as unit prices fall, because every non-compliant lamp removed drives direct package demand. Suppliers with LM-80 files and reparability documentation meet tender prerequisites more easily, translating compliance expertise into higher bid-win ratios.

Declining LED Package Costs Due to Economies Of Scale

Asian wafer fabs running 150 mm and 200 mm lines have lowered mid-power SMD prices by 8-12% annually since 2023, enabling European retrofit projects to achieve 2-year paybacks at electricity tariffs above EUR 0.15/kWh. Lumileds answered with its LUXEON Altilon SMD-A, a pick-and-place-optimized package that reduces the assembly cycle time by 18% while maintaining 0.2 V forward-voltage consistency across bins, helping OEMs squeeze costs without sacrificing reliability. Lower landed costs accelerate adoption in troffers and panel lights, expanding the addressable volume for package vendors even as gross margins compress. The price curve also widens the performance gap between commodity mid-power and premium chip-scale or flip-chip options, allowing suppliers to segment portfolios and defend margin in high-power niches. Consequently, economies of scale both democratize basic lighting and finance R&D for specialty architectures.

Commoditization-Driven Price Pressure

Second-tier Asian manufacturers offer sub-USD 0.50 mid-power packages, prompting European luminaire OEMs to dual-source and negotiate bulk discounts that erode supplier loyalty. In retrofit bulbs and tubes, buyers judge LEDs as interchangeable, so even established brands must shave margins to keep per-lumen costs competitive. Some mid-tier European assemblers have exited commodity bins, reallocating R&D toward automotive or horticultural segments where technical barriers curb direct price fights. The squeeze is most acute in public tenders that award on the lowest bid, leaving little room for premium positioning unless lifetime or warranty clauses carry measurable penalties. Persistent price deflation, therefore, drags on overall revenue growth despite steady unit shipments.

Other drivers and restraints analyzed in the detailed report include:

- Accelerated Adoption of Automotive Adaptive Headlamps

- EU RoHS Phase-Out of Mercury-Based Backlights

- Supply Chain Volatility for Rare-Earth Phosphors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Surface-mount device packages captured 58.38% of the Europe White LED Package market share in 2025, retaining leadership because their plastic housing, proven pick-and-place compatibility, and field-serviceable design align with the European Union's reparability rules. Municipal street-lighting concessions and commercial ceiling-panel retrofits continue to specify SMD formats, providing assemblers with predictable volumes and helping luminaire makers keep warranty claims below contract thresholds. Mid-cycle product updates, such as automated optical inspection markers and tighter binning tolerances, improve quality without disrupting established production flows. The broad installed base also underpins secondary demand for spare parts, keeping SMD revenues resilient even as unit prices decline each year.

Chip-scale packages are on a faster growth curve, advancing at a 3.88% CAGR through 2031 as automotive adaptive headlamps and micro-LED backplanes favor sub-0.5 millimeter profiles and high thermal conductivity. Eliminating the molded housing drops thermal resistance by roughly 20%, enabling tighter pixel spacing and higher drive currents without lumen sag. European Tier-1 suppliers integrate wafer-level phosphor, driver ASICs, and aluminum nitride substrates, turning the compact form factor into a single-sourced module with defensible pricing. Flip-chip and chip-on-board formats fill adjacent niches-flip-chip in high-current daytime running lamps, chip-on-board in industrial high-bays-highlighting how architecture choice now tracks end-use performance targets rather than one-size-fits-all cost metrics.

List of Companies Covered in this Report:

- Signify N.V.

- Osram Opto Semiconductors GmbH

- Lumileds Holding B.V.

- Nichia Europe B.V.

- Samsung Electronics Co., Ltd.

- Seoul Semiconductor Co., Ltd.

- Cree LED, an SGH Company

- Everlight Electronics Co., Ltd.

- Lextar Electronics Corp.

- ROHM Co., Ltd.

- Citizen Electronics Co., Ltd.

- Lite-On Technology Corp.

- Honglitronic Co., Ltd.

- Dominant Opto Technologies Sdn. Bhd.

- MLS Co., Ltd. (Forest Lighting)

- ProPhotonix Ltd.

- TT Electronics plc

- Wurth Elektronik GmbH AND Co. KG

- Bicom Optoelectronics Co., Ltd.

- Opto Tech Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Energy Efficiency Regulations Tightening Across EU

- 4.2.2 Declining LED Package Costs Due to Economies of Scale

- 4.2.3 Accelerated Adoption in Automotive Adaptive Headlamps

- 4.2.4 EU RoHS Phase-Out of Mercury-Based Back-Lights

- 4.2.5 Expansion of Vertical Farming Using White LEDs

- 4.2.6 Rising Electricity Costs Driving Commercial Retrofit Acceleration

- 4.3 Market Restraints

- 4.3.1 Commoditization-Driven Price Pressure

- 4.3.2 Supply Chain Volatility for Rare-Earth Phosphors

- 4.3.3 EU Ecodesign Reparability Rules Limiting CSP Uptake

- 4.3.4 Extended Replacement Cycles in Mature LED Installations

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Package Architecture

- 5.1.1 SMD (Surface Mount Device)

- 5.1.2 COB (Chip-on-Board)

- 5.1.3 CSP (Chip Scale Package)

- 5.1.4 Flip-Chip LED Packages

- 5.2 By Power Class

- 5.2.1 Low Power (Below 0.5 W)

- 5.2.2 Mid Power (0.5-1 W)

- 5.2.3 High Power (Above 1 W)

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display AND Backlighting

- 5.3.4 Specialty / Niche

- 5.4 By Country

- 5.4.1 United Kingdom

- 5.4.2 Germany

- 5.4.3 France

- 5.4.4 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Signify N.V.

- 6.4.2 Osram Opto Semiconductors GmbH

- 6.4.3 Lumileds Holding B.V.

- 6.4.4 Nichia Europe B.V.

- 6.4.5 Samsung Electronics Co., Ltd.

- 6.4.6 Seoul Semiconductor Co., Ltd.

- 6.4.7 Cree LED, an SGH Company

- 6.4.8 Everlight Electronics Co., Ltd.

- 6.4.9 Lextar Electronics Corp.

- 6.4.10 ROHM Co., Ltd.

- 6.4.11 Citizen Electronics Co., Ltd.

- 6.4.12 Lite-On Technology Corp.

- 6.4.13 Honglitronic Co., Ltd.

- 6.4.14 Dominant Opto Technologies Sdn. Bhd.

- 6.4.15 MLS Co., Ltd. (Forest Lighting)

- 6.4.16 ProPhotonix Ltd.

- 6.4.17 TT Electronics plc

- 6.4.18 Wurth Elektronik GmbH AND Co. KG

- 6.4.19 Bicom Optoelectronics Co., Ltd.

- 6.4.20 Opto Tech Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment